{kind=link}

Overview

Majedie Investments (MAJE), managed by Marylebone Partners, pursues a liquid endowment-style investment strategy with the objective to deliver an annualised return of at least 4 per cent above UK CPI (consumer price inflation) over rolling five-year periods.

The approach is long-term and fundamentally driven. Like the leading US university endowments, it seeks to emulate, the strategy avoids market timing and instead emphasises patient capital allocation, drawing on a combination of actively managed equities and a select range of complementary asset classes. Unlike many endowment portfolios, however, Majedie avoids illiquid assets such as private equity, private credit, venture capital and real estate. All holdings are marked to market, preserving liquidity and transparency.

The portfolio is organised across three segments: specialist external managers (spanning equity and absolute-return strategies), direct investments, and special investments. The latter provides exposure to differentiated opportunities that are unlikely to feature in conventional portfolios.

Since Marylebone Partners assumed responsibility for the trust at the end of January 2023, Majedie has comfortably exceeded its CPI + 4 per cent objective. Over the period (to the end of March 2026), the trust generated an NAV total return of 34 per cent and a share price total return of 57 per cent, compared with cumulative UK CPI inflation of 11.6 per cent. The trust employs no gearing. Dividends remain a core component of total return, with quarterly distributions targeted at 0.75 per cent of quarter-end NAV, equivalent to an annualised yield of 3 per cent.

Introduction

Over the second quarter of Majedie’s financial year, Net Asset Value (NAV) rose by +0.2%, with gains in January and February largely given back in March. This was a strong relative outcome against weaker equity markets and heightened volatility. The MSCI ACWI fell -7.2% in March and ended the quarter down -3.2%, while Asian equities fell -13.7% in March and ended the quarter down -1.2%. For the first half of the financial year, NAV has risen +4.3%.

Majedie’s resilience reflected two structural features of the portfolio. First, the underlying investments are idiosyncratic. Despite the portfolio’s equity-centric nature, returns can be substantially independent of broader market direction over periods beyond the short term. Second, our decision-making protocol leads us, and our underlying managers, to take profits when long-term investments approach medium-term price targets. In February, we reduced positions in copper and uranium stocks, leaving dry powder to deploy during the subsequent pullback.

Market Commentary and Outlook

Markets began the year anchored to resilient U.S. growth, cooling inflation and expectations of lower policy rates. That backdrop supported equities through January and February, while industrial and precious metals rallied sharply. At the same time, investors increasingly treated successive sectors as potential AI casualties, with software particularly affected.

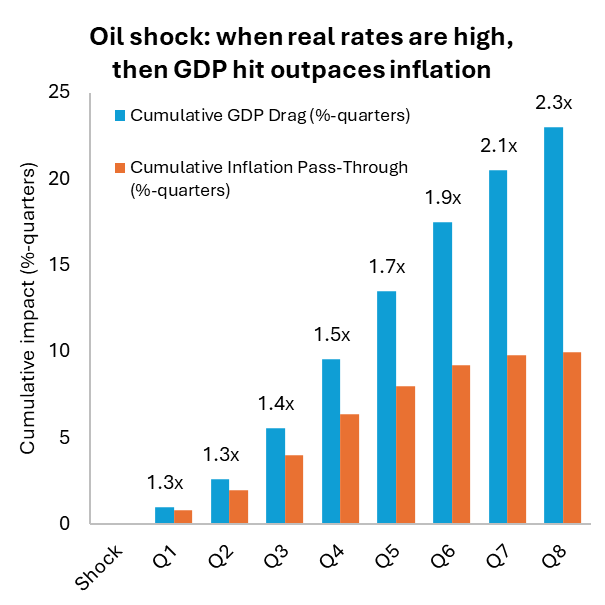

The market course changed in March as hostilities in the Gulf and disruption to tanker traffic through the Strait of Hormuz brought energy security back into focus. Oil prices rose as supply disruption shifted from tail risk to reality. The shock fed into rates, with higher crude prices reviving inflation concerns and leading markets to scale back expectations for near-term policy easing. The result was tighter financial conditions at the same time as growth expectations were revised down. The U.S. dollar strengthened, pressuring non-U.S. markets and contributing to a reversal in gold and other precious metals. Asian equities were particularly hard hit, reflecting the region’s dependence on imported energy.

Following events in the Middle East, scenarios previously treated as tail risks may warrant greater weight in base-case thinking. We see three broad paths. The first is regime fracture within Iran, which could create short-term uncertainty but ultimately support markets if oil prices ease and regional stability improves. The second is a negotiated settlement, allowing passage through the Strait of Hormuz to resume under some form of arrangement, but with oil prices likely settling above prior levels. The third is destructive escalation, with energy infrastructure becoming both target and leverage. While precise probabilities are difficult to assign, the second path appears most likely.

An oil shock is often treated first as an inflation problem, but history suggests the larger and more durable effect can fall on growth, particularly when real interest rates are already restrictive. Higher fuel costs act like a regressive tax on households and a margin squeeze for companies. In the current monetary regime, demand destruction may be more likely than a persistent inflation cycle. If growth falters and inflation proves less persistent than feared, the next move could be towards lower policy rates rather than the higher rates currently assumed by markets.

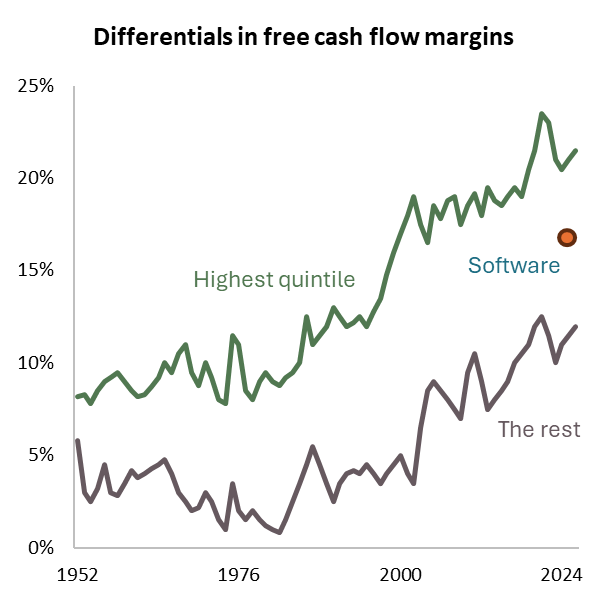

Over time, share prices follow the delivery of earnings and, even more importantly, of free cash flow. Data shows that the most consistently cash-generative companies have outperformed the rest, by a meaningful margin.

Some investors are currently extending confidence to one class of historically cash-generative growth company while withholding it from another. Hyperscalers are being given latitude to absorb near-term pressure on free cash flow margins, on the assumption that current investment will drive materially higher future cash generation. In contrast, software companies are increasingly being discounted on fears that AI will erode growth and margins. We view that assessment as too blunt. Some software models will come under pressure, especially those with limited differentiation. Others remain well positioned through customer data, systems-of-record status and deep operational embedding.

Source: Empirical Research. Large-Capitalisation Stocks: Forward Relative Returns of the Highest and Lowest Quintiles of Free Cash Flow Yield

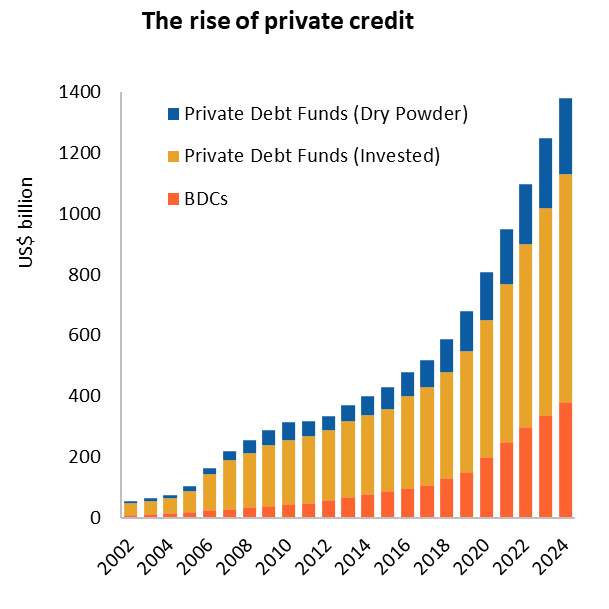

Private credit is also showing fault lines. Roughly US$1.2 trillion has been raised by private-credit firms over the past five years. As capital has flowed into a finite opportunity set, underwriting discipline is unlikely to have remained intact. Concerns are particularly acute in software lending, where loans have often been underwritten against high valuation assumptions, limited creditor protection, loose covenants and Payment-in-Kind features. Majedie has no exposure to private credit, and exposure to more liquid credit instruments was reduced last year. However, we remain mindful of second-order effects, including forced selling by overextended allocators. Our specialist credit managers remain focused on idiosyncratic positions already priced for adverse outcomes, with seniority, actionable catalysts and portfolio-level hedges providing downside protection.

Attribution

The strongest contribution over the quarter came from commodity-related investments, followed by external manager allocations to the biotech specialist and a low-net exposure Shipping & Energy fund. The weakest performance came from the Software specialist and Brown Advisory’s Global Focus strategy. We viewed this weakness as an opportunity and added to both on 1 April.

Within External Managers, Absolute-return strategies mitigated the effect of weaker equity markets. All Absolute-return strategies made money, with the largest contribution from Fearnley Energy Alpha, supported by Contrarian Emerging Markets Fund. The Equity-centric component was down, broadly in line with markets, reflecting deliberate overweighting to Asia and some exposure to software stocks. Paradigm, the Biotech manager, performed well, benefiting from positive clinical data and takeover approaches for some of its largest holdings.

Within Direct Investments, the largest contribution came from copper exposure through the Global X Copper Miners ETF and options, which were sold in January after copper stocks rose sharply. Computacenter plc., IMI plc. and ArcBest also contributed positively whilst Stabilus SE, Cancom SE and SS&C Technologies detracted.

Special Investments performed well, led by the Sprott Uranium Miners ETF, which rallied sharply before retracing; we used the strength to trim the position. Bank of Cyprus was exited after a successful holding period, during which the company delivered strong earnings growth, increased its dividend payout ratio and re-rated. Bow Street Global Opportunities Fund and Orizon Valorizacao de Residuos also contributed positively. Oxford Biomedica plc., detracted after giving back gains following a takeover approach from EQT that did not progress, although we continue to see strategic value and fundamental upside.

Positioning and Conclusion

Amid geopolitical and macro uncertainty, we expect further volatility. Having reassessed probabilities, we believe the fundamental case for Majedie’s investments remains intact and have made few adjustments. In several cases, recent weakness has improved prospective returns. There were no meaningful changes to the team or business during the quarter, and integration within Brown Advisory is progressing well.

Disclaimer:

This publication is intended to be of general interest only and does not constitute legal, regulatory, tax, accounting, investment or other advice nor is it an offer to buy or sell shares in the Company (or any other investments mentioned herein).

Nothing in this publication should be construed as a personal recommendation to invest in the Company (or any other investment mentioned herein) and no assessment has been made as to the suitability of such investments for any investor. In deciding to invest prospective investors may not rely on the information in this document. Such information is subject to change and does not constitute all the necessary information to adequately evaluate the consequences of investing in the Company.

The shares in the Company are listed on the London Stock Exchange, and their price is affected by supply and demand and is therefore not necessarily the same as the value of the underlying assets. Changes in currency rates of exchange may have an adverse effect on the value of the Company’s shares (and any income derived from them). Any change in the tax status of the Company could affect the value of the Company’s shares or its ability to provide returns to its investors. Levels and bases of taxation are subject to change and will depend on your personal circumstances.

Past performance is not a reliable indicator of future returns. Any return estimates or indications of past performance cited in this document are for informational purposes only and can in no way be construed as a guarantee of future performance. No representation or warranty is given as to the performance of the Company’s shares and there is no guarantee that the Company will achieve its investment objective.