{kind=link}

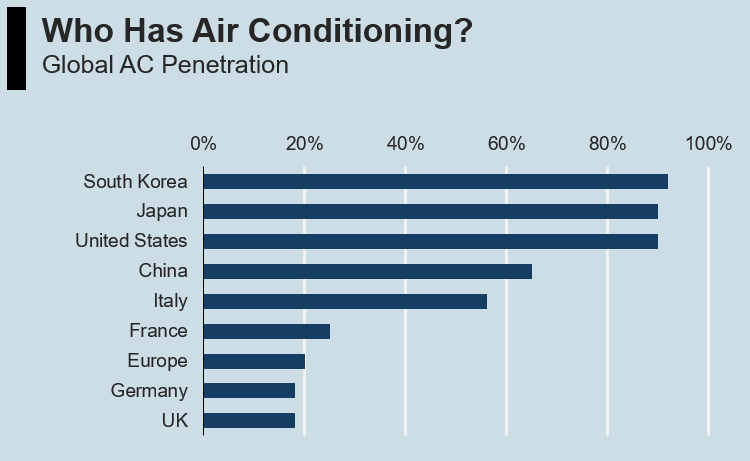

- Europe’s AC deficit: Europe sits at roughly 20% air-conditioning penetration, significantly lower than other major economies such as the United States and Japan, which both sit above 90%. A Chinese product innovation is breaking the installation barrier that kept AC out of reach for most households.

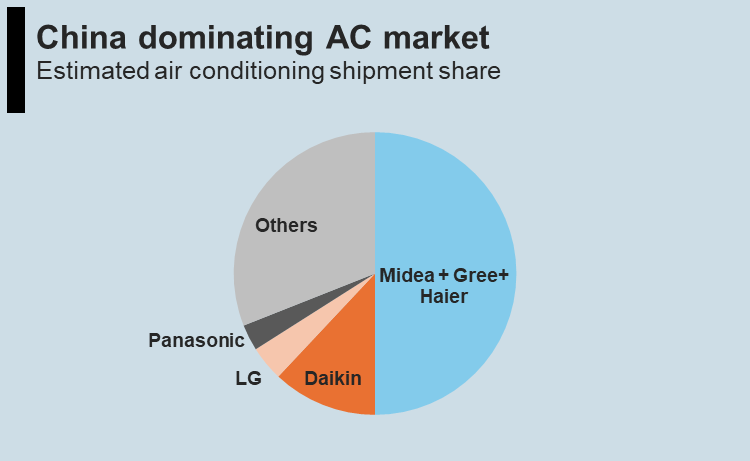

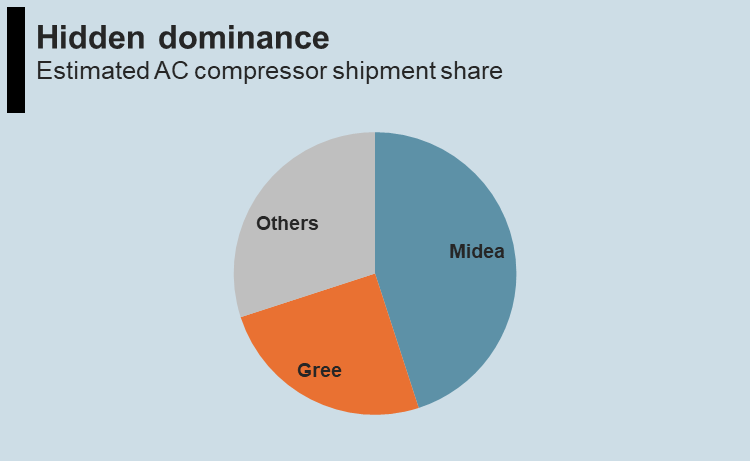

- Who Controls the Pyramid: Haier, Midea and Gree produce roughly 50% of residential ACs globally. In addition, Midea and Gree control 70-75% of global AC compressors – a hidden dominance inside every AC and heat pump, regardless of brand badge.

- Hidden second wave: Heat pumps are ACs that run in reverse, using the same compressors and valves. Europe’s regulation is accelerating heat pump adoption, effectively adding a second demand stream through the same Chinese supply chain.

An €800 air conditioner selling for nearly €3,000 on Germany’s secondary market.

That is the price of a Midea PortaSplit (split AC), during Europe’s latest heat wave in June 2026. It has been sold out across Germany for weeks. According to braucheklima.de, a Midea PortaSplit tracker site in Germany, only one store out of 1179 branches in Germany has stock on June 30, 2026.

Europe’s AC Deficit

Europe sits at roughly 20% air-conditioning penetration, significantly lower than other major countries such as the United States and Japan, which both sit above 90%.

The deficit is structural, not cyclical. The World Meteorological Organization has documented that Europe is warming at more than twice the global average.

Europe can be divided into three distinct cooling markets.

- Southern Europe — Replacement/upgrade demand: Spain and Italy run at 40-60% penetrations, and Greece is estimated to have a higher penetration rate of over 70%. This represents an established installed base where the primary demand driver is replacement cycles and efficiency upgrades.

- Western and Northern Europe — first-time buyer market: France and Germany run at 20-25% penetration. These represent the lowest penetration among major global economies. Heatwaves in recent years have shifted consumer behaviour, stimulating AC demand.

- Central and Eastern Europe — price-sensitive growth market: This region is estimated in the 15–30% range. This is the entry point for Chinese brands on price-competitive branded units, competing against incumbents on cost.

Crossing the Installation Hurdle

Installing a traditional split AC in Europe is not straightforward.

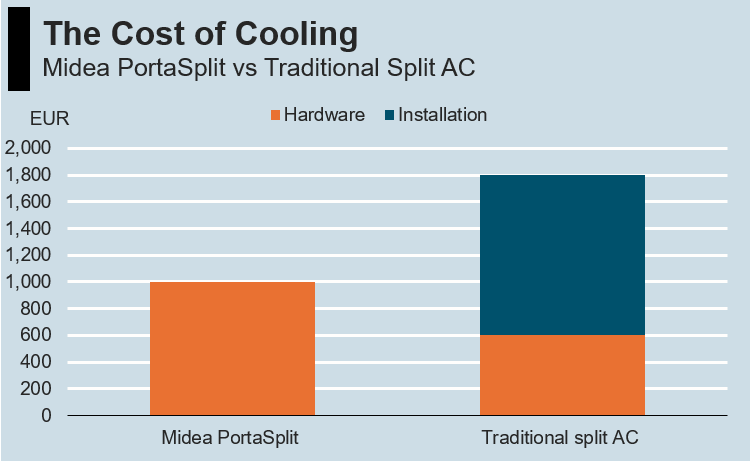

The installation costs €1,000 to €1,500 in labour alone. For a €500 to €800 hardware purchase, the installation cost multiplies the total.

In addition, it must meet various country-level regulations:

- Spain: the outdoor unit alters the building facade, which is a shared property right. Installation requires a three-fifths majority vote by the owners’ community.

- Italy: only certified professional technicians may install split systems.

- France: any system with more than 2 kg of refrigerant charge requires a certified inspection. Most traditional split units exceed this threshold.

- Switzerland: energy efficiency must reach SEER class A++ or higher, a rating many older or low-cost models cannot meet.

Midea’s innovative product, PortaSplit, addresses this. It is a split AC: an indoor unit connected to an outdoor condenser by a pre-charged refrigerant line with quick-connect fittings.

It is designed around the above installation barriers.

- The outdoor unit sits on a bracket that clamps into the open window frame. No drilling or modification is required.

- Its 0.62 kg of refrigerant stays under the French 2 kg threshold.

- Its energy efficiency fits into the Swiss A++ bracket.

The product category, DIY split ACs, did not exist at scale before. It won TIME’s “Best Inventions of 2025” award.

Midea debuted it in Germany in 2025, and expanded to France, Italy, Denmark, and the Netherlands in 2026. It was met with stockout across Germany by mid-June 2026.

Who Controls the Pyramid

The air conditioning supply chain is dominated by Chinese players.

Haier, Midea and Gree produce roughly 50% of residential ACs globally. Including OEM production for legacy brands, China accounts for ~70% of room ACs.

Daikin: The “Last Samurai”: Daikin remains the major non-Chinese player with a strong position in the premium and commercial segment.

How did three Chinese companies dominate the world’s AC market?

- Japan ruled the 1980s and 1990s: Daikin, Mitsubishi Electric, Panasonic, Toshiba, Sanyo commanded premium pricing and margins.

- Korea rose in the 2000s: LG and Samsung added design and marketing and undercut on price.

- China’s domestic housing boom: created a 100M+ unit-per-year domestic AC market. Midea, Gree, and Haier scaled on that structural trend. The volume gave them economies of scale.

- Brand acquisition: Chinese brands then bought the pyramid: Haier acquired Sanyo (2012), Fisher & Paykel (2012), and GE Appliances (2016). Midea bought Toshiba’s appliance business (2016).

The “Component Toll”

Midea and Gree control 70-75% of global AC compressors. Sanhua controls over 45% of HVAC thermal expansion valves and electronic expansion valves, the precision components that determine inverter-class energy efficiency. These are the bottlenecks inside every AC unit and heat pump, regardless of brand badge.

For example, Europe’s AC and heat pump makers are largely assembly operations. They import compressors and valves from Asia and assemble branded finished units in European factories.

Europe has almost no domestic compressor capacity at scale.

- Capacity concentration: China produces roughly 80% of the world’s AC compressors. Building equivalent capacity in Europe would take three to five years and require a skilled industrial workforce that does not exist at scale.

- Cost advantages: Chinese compressor costs benefit from a domestic market that installed roughly 100M AC units per year. European demand, measured in low millions, cannot match this scale economics.

The Hidden Second Wave

China’s dominance in AC compressors and valves positions it to capture the European heat pump market — a market currently riding on the regulatory tailwind.

The technology connection: Every modern AC with a heat mode is already a heat pump. The refrigeration cycle is identical — a compressor circulates refrigerant between two coils, and a reversing valve flips the flow direction. The same Chinese factories that supply AC compressors also supply heat pump compressors.

Cost and efficiency: Heat pumps do not burn fuel. They run at 3-4x efficiency compared with traditional gas boilers. Despite Europe’s high electricity prices, a heat pump’s efficiency advantage makes running costs roughly equal to a gas boiler — and cheaper with subsidies.

Regulatory tailwind: European governments are accelerating heat pump penetration via legalisation.

- EU: Targets to double heat pump deployment every 4 years; fossil boiler phase-out by 2040 and ~60M additional heat pumps by 2030.

- Germany: New heating must be ≥65% renewable from 2024 — effectively banning gas boilers.

- UK: 600K installs per year by 2028; gas boiler ban signalled for 2035 — £7,500 grant per installation.

- France: New buildings must have low-carbon heating — heat pumps are default compliance

- Netherlands: Gas grid connections banned for new buildings from 2018.

The European Heat Pump Association estimates roughly 25.5M heat pumps installed as of end-2024, while the REPowerEU target requires 60M by 2030. EHPA warns the EU could be 15M units short. Daikin itself projects 250% market growth by 2030.

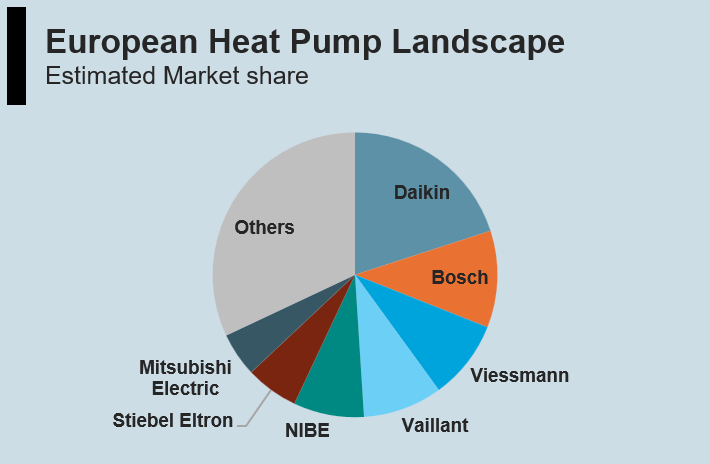

Who dominates today

The European heat pump market is led by Japanese and German brands. Daikin is the single largest player. Bosch, Vaillant, Viessmann, NIBE, Stiebel Eltron, and Mitsubishi Electric follow. Chinese brands are not yet major players.

But these market leaders are assembly operations that depend on Chinese components. The compressors inside likely come from GMCC or Gree. The valves likely come from Sanhua.

Midea’s PortaSplit is the bridge. It is marketed as “the first DIY heat pump”. It is currently a minor player in the broader heat pump market, where whole-house hydronic systems generally cost €12,000 to €40,000. The PortaSplit at €900-€1,200 is a room-level solution, not a whole-house replacement, but it demonstrates that the underlying technology does not need to cost five figures.

As heat pumps shift from premium green technology to regulated compliance item, the category could commoditise. Chinese brands, with vertically integrated supply chains and the lowest component costs, are structurally positioned to capture the volume end of this transition.

Daikin: The Last Samurai

Daikin (TYO:6367) dominates European heat pumps through premium branding and installer relationships. But its position is currently under pressure.

- Price-sensitive demand: Europe’s fastest-growing AC segment is first-time buyers at the low end. PortaSplit at €800 delivers split-AC performance at a fraction of the €2,000+ installed cost of a Daikin premium split product.

- Dependent on Chinese supply: Daikin’s volume models use compressors from GMCC and Gree, leading to higher costs than vertically integrated Chinese players.

- Commoditisation by regulation: As heat pumps shift from premium green technology to regulated compliance, customers tend to go for budget options. Premium branding matters less when demand is driven by regulation.

This article is a “periodical publication” for information only and is not investment advice or a solicitation to buy or sell securities. This article does not constitute a “personal recommendation” or “investment advice” under UK FCA regulations. Investing in equities involves significant risk. The author holds NO position in the securities mentioned. There is no warranty as to completeness or correctness. Please do your own due diligence or consult a licensed financial adviser. Please read the Full Disclaimer before acting on any information. Images created with the assistance of AI.