Philip Hammond slams Boris Johnson ahead of Conservative Conference speech

Phillip Hammond has criticised former foreign secretary Boris Johnson in a series of interviews prior to his speech at the conservative conference in Birmingham.

In particular, the chancellor expressed doubts over Mr Johnson’s leadership ambitions in an interview with the Daily Mail.

Hammond said of Boris becoming PM: “I don’t expect it to happen”.

Hammond dismissed the former London Mayor as proving incapable of “grown-up politics”.

Moreover, the chancellor criticised Johnson’s tendency to prove weak on detail, indicating that his only political achievement were London’s “Boris Bikes” that were installed during his time as Mayor.

Specifically, Hammond said: “Boris is a wonderful character, but he’s never been a detail man. I’ve had many discussions with him on Brexit.”

Alongside suggesting that Johnson proved more of a style over substance man, he also took the opportunity to mimic Johnson.

Describing discussions he had with the former foreign secretary over a Canada trade deal, Hammond said:

“Boris sits there and at the end of it he says ‘yeah but, er, there must be a way, I mean, if you just, if you, erm, come on, we can do it Phil, we can do it. I know we can get there.’ ‘And that’s it!”

Similarly, in another interview with Good Morning Britain ahead of his conference speech, Hammond took issue with Johnson’s “fantasy world” idea of Brexit.

He commented:

“It isn’t about taking back control, it’s about fantasy world. The European Union have been very clear that as they negotiate with us they have their red lines, just as we have our red lines, and they are not prepared to negotiate for a free trade agreement which includes the whole of the United Kingdom because of the impact that would have on the border between Northern Ireland and the Republic of Ireland.”

The chancellor is set to deliver his speech at 12PM on Monday at the party conference in Birmingham.

The Conservative conference comes a week after the Labour party’s counterpart conference in Liverpool, in which Jeremy Corbyn committed the party to a “green jobs revolution”.

Theresa May’s party has come under increased pressure in recent months, amid much publicised division within the cabinet over how best to proceed after Brexit.

This was only compounded by the resignation of high profile cabinet ministers such as David Davis and Boris Johnson, who have condemned the government’s strategy.

Whilst the conservatives have long prided themselves as a party of competence, Brexit seems to be exposing widening gulfs within the party.

It seems the so-called ‘Night of the long knives’, a notoriously brutal cabinet reshuffle amid party disarray under conservative party leader Macmillan, may be well on its way to receiving a sequel.

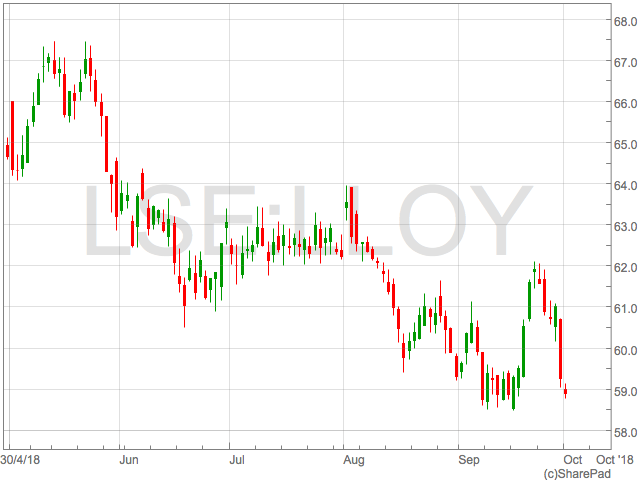

Lloyds share price remains in downtrend

The Lloyd’ Banking Group (LON:LLOY) share price remains in a steady down trend having broken back below 60p towards the lowest levels since late 2016.

The bank posted highs of 72.6p in January 2018 but has since shed nearly 20% of its value.

The persistent declines come in spite of strong results released in August in which the company announced an interim dividend hike to 1.07p from 1p. Underlying profits jumped 23% to £3.1 billion for the first half of the year.

However, investors have shunned Lloyd’s as mounting concerns over Brexit create uncertainity for the future of the bank.

In their half year report, CEO António Horta-Osório commented on the results:

“The UK faces a period of political and economic uncertainty in the run-up to the UK’s departure from the European Union, however the UK economy remains resilient and, excluding the impact of adverse weather, continues to demonstrate robust growth. The economy is benefiting from the highest employment rate in half a century and household indebtedness remains significantly below pre-crisis levels, with strong growth in the world economy also positive for UK exports.”

Adding to souring sentiment surrounding the stock, fund management star Neil Woodford has reduced his stake in the company over the past year.

Woodford is not alone in disposing of Lloyd’s shares. Goldman Sachs released a sell rating for the stock in September with a price target of 55p.

Despite negativity from Woodford and Goldmans, some analysts are positive on the stock with Credit Suisse recently issues an outperform rating on the share and Hargreaves Lansdown analysts say the bank is in ‘rude health’.

Adding to souring sentiment surrounding the stock, fund management star Neil Woodford has reduced his stake in the company over the past year.

Woodford is not alone in disposing of Lloyd’s shares. Goldman Sachs released a sell rating for the stock in September with a price target of 55p.

Despite negativity from Woodford and Goldmans, some analysts are positive on the stock with Credit Suisse recently issues an outperform rating on the share and Hargreaves Lansdown analysts say the bank is in ‘rude health’.

Adding to souring sentiment surrounding the stock, fund management star Neil Woodford has reduced his stake in the company over the past year.

Woodford is not alone in disposing of Lloyd’s shares. Goldman Sachs released a sell rating for the stock in September with a price target of 55p.

Despite negativity from Woodford and Goldmans, some analysts are positive on the stock with Credit Suisse recently issues an outperform rating on the share and Hargreaves Lansdown analysts say the bank is in ‘rude health’.

Adding to souring sentiment surrounding the stock, fund management star Neil Woodford has reduced his stake in the company over the past year.

Woodford is not alone in disposing of Lloyd’s shares. Goldman Sachs released a sell rating for the stock in September with a price target of 55p.

Despite negativity from Woodford and Goldmans, some analysts are positive on the stock with Credit Suisse recently issues an outperform rating on the share and Hargreaves Lansdown analysts say the bank is in ‘rude health’. Avocet Mining shares plunge amid possible break-up

Shares in Avocet Mining (LON:AVM) plunged more than 30 percent on Monday morning, after the company issued an interim update.

The gold mining firm said that it still remains in talks with its largest shareholder, Elliot Management, to restructure its debts.

Whilst the company said it had sufficient funds providing capital and interest from the loan, Elliot Management does not need to be repaid during the period.

The company said that loans of $29.9 million as of 30 June from Manchester Securities Corp (an affiliate of Elliott) ultimately ‘remain an unsustainable debt burden’.

The statement added that a potential of these ongoing discussions could be that ‘the Avocet Group is broken up further in an orderly manner and eventually wound up.’

Should that occur, Avocet said given the amount of debt owed, there will be ‘very minimal or no return’s for company shareholders.’

Earlier this month, the mining firm announced that it had transferred 30 percent of its Tri-K gold project to the Moroccan mining group Managem SA.

Following the transfer, Managem SA will hold a majority 70 percent stake in the project.

Avocet is a gold mining and exploration company, which is primarily focused in West African Gold. It has operations in both Burkina Faso and Guinea.

The company has been listed on the London Stock Exchange as of 1996, as well as the Oslo Børs.

Shares in Avocet Mining are currently trading -38.08 percent as of 11.08AM (GMT).

Ryanair warns on profits as strike action hits

Ryanair has warned on profits for the year, attributing the weaker performance to the impact of strike action and rising fuel prices.

The budget Irish airline said full-year profits will be down 12 percent.

It now expects profits to fall within the range of between €1.1 billion and €1.2 billion, down from the previously forecast €1.25 billion-€1.35 billion.

The company said that pilot and cabin crew strikes in September had particularly affected profits, proving a deterrent for customers booking future flights.

Moreover, Ryanair said that rising oil prices had also continued to add to profit pressure across the period.

Earlier this month, Ryanair pilots across Germany, Spain, Italy, Portugal and Belgium announced plans to coordinate strike action for 24 hours.

The action led to the airline cancelling as many as 250 flights, affecting some 40,000 customers.

Chief executive, Michael O’Leary, said: “While we successfully managed five strikes by 25% of our Irish pilots this summer, two recent co-ordinated strikes by cabin crew and pilots across five EU countries has affected passenger numbers (through flight cancellations), bookings and yields (as we re-accommodate disrupted passengers), and forward air fares into Q3.

“While we regret these disruptions, we have on both strike days operated over 90% of our schedule.

“However, customer confidence, forward bookings and Q3 fares have been affected, most notably over the October school midterms and Christmas, in those five countries where unnecessary strikes have been repeated.”

The airline said that it has taking the decision to close certain routes and bases, in a bid to slim down costs.

It said that its Eindhoven base in the Netherlands will close, however routes to the location will continue.

This is also the case at its base in Germany, amid cuts at its Niederrhein base.

Shares in Ryanair (LON:RYA) are currently trading -8.73 percent as of 10.29 AM (GMT).

Tesco Bank faces £16.4m penalty over cyber attack

Tesco Bank has been fined £16.4 million by the Financial Conduct Authority (FCA) for failing to protect customers during a cyber attack back in 2016.

The FCA said the attack netted cyber-attackers £2.26 million after fraudsters targeted customers accounts.

Tesco have admitted that the attack results in 34 fraudulent transactions, in which funds were lifted from its customers.

The FCA said that the attack could have been avoided and that Tesco’s banking business failed to respond adequately to the security breach.

Mark Steward, executive director of enforcement and market oversight at the FCA, commented on the decision:

“The fine the FCA imposed on Tesco Bank today reflects the fact that the FCA has no tolerance for banks that fail to protect customers from foreseeable risks,” he said.

“In this case, the attack was the subject of a very specific warning that Tesco Bank did not properly address until after the attack started. This was too little, too late. Customers should not have been exposed to the risk at all.”

He added: “Banks must ensure that their financial crime systems and the individuals who design and operate them work to substantially reduce the risk of such attacks occurring in the first place.”

Gerry Mallon, Tesco Bank’s chief executive, said:-“We are very sorry for the impact that this fraud attack had on our customers. Our priority is always the safety and security of our customers’ accounts and we fully accept the FCA’s notice.”

“We have significantly enhanced our security measures to ensure that our customers’ accounts have the highest levels of protection. I apologise to our customers for the inconvenience caused in 2016.”

Last week it had been reported that the FCA was considering imposing a larger record fine of £33.6 million.

However, amid negotiations between the financial regulator and the bank, the fine was reduced after agreeing upon an early settlement.

Tesco shares (LON: TSCO) are currently trading -0.29 percent as of 10.17AM (GMT).

Netflix sued by easyJet founder over “brand thief” claims

Netflix (NASDAQ: NFLX) is being sued by the founder of easyJet (LON: EZJ) over the new series Easy, claiming it infringes his company’s European trademarks.

The easyJet founder, Sir Stelios Haji-Ioannou, will take legal action over the streaming service claiming that it is simply another “brand thief” attempting to “piggyback” off his easyGroup business.

The new series on Netflix has been described as an “eclectic, star-studded anthology [which] follows diverse Chicagoans fumbling through the modern maze of love, sex, technology and culture”.

The easyGroup business, which also owns easyBus, easyCar, easyVan easyHotel (LON: EZH), as well as many other brands, is seeking a high court injunction to prevent Netflix from using the programme name in Europe.

A spokesman for easyGroup said: “EasyGroup now owns more than 1,000 registered trademarks within the easy family of brands all over the world and takes its protection from unauthorised use very seriously.”

Haji-Ioannou said: “This is a case of typically arrogant behaviour by a very large American tech company who never bothered to check what legal rights other companies have outside the US.”

“When Joe Swanberg came up with the name ‘easy’ for his new TV series a couple of years ago they should have checked with their European lawyers before using it. We own the European trademark in the word easy and another thousand trademarks with easy as a prefix and we can’t allow people to use it now as a brand name, especially when they are doing it mostly with our colours and font.”

“At least I am pleased that Netflix have said that they will stop at series three anyway. However, we have to stop them from promoting the older series in Europe for online streaming.”

Netflix said in a statement that “viewers can tell the difference between a show they watch and a plane they fly in”.

Aldi sales surpass £10bn in UK & Ireland

Sales at Aldi have exceeded £10 billion across the UK and Ireland for the first time.

The German chain has reported a rise in sales by 29 percent to £265 million in 2017, which was pushed by the opening of many new stores.

Aldi is the fifth biggest supermarket in the UK, as it overtook the Co-op last year. The chain has 775 stores in the UK and Ireland and plans to open 130 new stores in the UK over the next two years.

Giles Hurley, the chief executive, said: “The revolution in British grocery shows no sign of slowing.”

“In 2020, Aldi will have been serving British shoppers for 30 years. In that time, we’ve become part of the fabric of British life. We’re proud to be reaffirming our commitment today.”

“Our fundamental purpose remains – to bring outstanding quality groceries at the lowest prices for our customers, creating jobs and supporting British farming and manufacturing.”

“While other grocers introduced more complexity into their businesses in their struggle to win back customers, we stuck to our guns and focused on doing what Aldi does best – buying smart, staying lean, improving quality and keeping prices low,” Hurley added.

Aldi hopes to create 5,000 jobs in the UK over the next two years.

In response to Aldi and Lidl’s growing popularity, Tesco (LON: TSCO) has opened its new discount supermarket, Jack’s. The first store opened last week.

Tesco, Sainsbury’s (LON: SBRY), Asda and Morrisons (LON: MRW) have had to approach Aldi and Lidl’s success by cutting costs and improving their cheapest own-label ranges.

Tesco’s chief executive, Dave Lewis, said of the new chain: “We will be the cheapest in town. There are full-range, full-service supermarkets, and clearly people want that, but there is a gap in terms of people wanting smaller, simpler, quicker shops and local produce.”

Musk & Tesla given $40m fine to settle SEC case

Following a deal with the US financial regulator, Elon Musk is to step down as the group’s chair and pay a fine.

Following the misleading tweets that Musk wrote about taking the firm private, he will step down as chair within the next 45 days as well as pay a combined fine of $40 million (£30.6 million) fine.

Musk will continue with his role as chief executive.

In a tweet sent in August, Musk said he was considering taking Tesla (NASDAQ: TSLA) private and had the “funding secured”, which would value Tesla at $420 a share.

The plan was abandoned just two weeks later, causing havoc to shares and investors accusing the chief executive of having no basis to the tweets.

Last Friday the share price in the car company was down close to 14 percent as investors lost yet further confidence.

The group’s boss is well known for his erratic behaviour. In the past few months he has smoked marijuana while appearing on a podcast and attacked a British cave expert involved in the rescue of a Thai football team by accusing him of being a paedophile.

Stephanie Avakian, who is the SEC’s co-director of enforcement, said in a statement: “The total package of remedies and relief announced today are specifically designed to address the misconduct at issue by strengthening Tesla’s corporate governance and oversight in order to protect investors.”

$20 million of the fine will be paid by Musk, whilst the remaining $20 million will be paid by Tesla. The group is worth over $20 billion and will not struggle in paying the fine.

Following the boss’s departure from the board, the group will appoint two new independent board directors to check on Musk’s control over the business.

Tesla and Musk have not yet commented on the fine.

Italy’s budget causes EU backlash, euro falls

Italy’s budget has stirred backlash from the EU and investors. In fact, it could result in the country’s finance minister’s exit. In addition to the euro, Italian shares and government bonds have also dropped. This is following the Italian government’s agreement of a budget that will increase borrowing by more than expected.

The budget has agitated the financial market for several reasons. First, the Italian economy is the third largest in the Eurozone following Germany and France. Next, its banking system is facing deep fragility after two decades of poor economic growth. Finally, the country’s new populist government has a controversial agenda involving raising pensions and a basic income.

The government insists this will have “abolished poverty”.

Italy’s coalition government was formed earlier in June. It unites the anti-establishment Five Star Movement and the hard-right League. Moreover, the coalition government made an overnight agreement to set forth a budget deficit next year equalling 2.4% of Italian GDP. But, the country’s finance minister, Giovanni Tria, had been promoting a 1.6%. Mr Tria remains unaffiliated to either party in the coalition.Italian media have reported that the finance minister was persuaded by the president not to resign following Italy’s budget.

Following the news, the yield on 10-year government bonds rose above 3%. Moreover, the Milan stock exchange dropped by over 2% earlier today. Indeed, a handful of banks saw a decline of at least 5%. Despite being under the EU’s deficit limit of 3% of GDP, the news has caused controversy. Italy is indeed the third-largest economy in the Eurozone but debt currently stands at 131% of national output. This makes Italy’s government debt second to Greece. Italy’s populist government rose to power through the promise of tax cuts, new social welfare policies and improved pensions. In fact, a minimum basic unemployment income is predicted to cost €10 billion alone. All these programmes have a very high price. Luigi Di Maio, deputy prime minister and leader of the Five Star party, insists that: “We, in a decisive manner, with this budget law, will have abolished poverty”.Unilever bosses’ jobs at risk as shareholders oppose HQ move

Top Unilever jobs are at risk of influential investor revolts at next year’s annual general meeting. This is due to their handling of plans to scrap the company’s UK headquarters. The company’s chairman and other board members are among the few who investors may target.

A variety of influential institutional shareholders are planning to oppose the re-election of chairman Marjin Dekkers. In addition, investors plan on opposing the company’s senior independent director, Professor Youngme Moon.

One of Unilever’s top investors also added that it was highly likely they would vote against Graeme Pitkethly. This is as a result of the chief financial officer’s ‘aggressive’ attempted justification of the move.