CFO Jonny Mason commented on the results:

“We are pleased with the overall performance of the Group in the 15 week period given the difficult UK retail environment. We achieved record sales for Black Friday and Christmas thanks to great planning and execution and compelling product and service offers. Particular highlights included the growth in fitting services for car parts, cycle repair and increased sales of bikes, electric bikes and dash cams.”

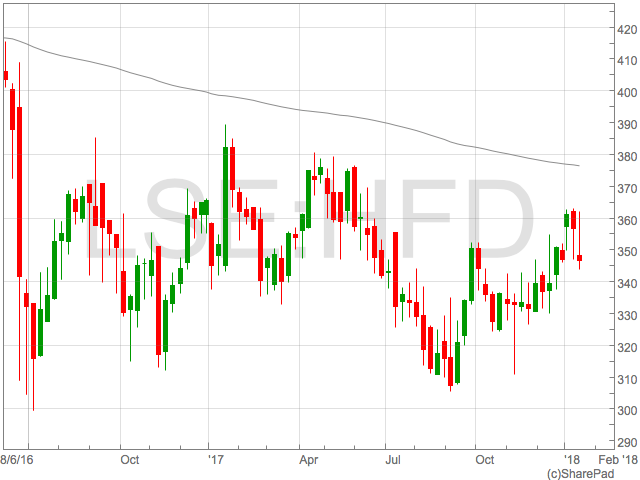

Shares in Halfords were flat on Thursday morning up 0.06% at 350.2p. The stock hit highs of 361.8p on the 1st January 2018.

Graham Stapleton started his tenure as Halfords’ CEO on 15th January having left his post at Dixon Carphone’s Honeybee.

CFO Jonny Mason commented on the results:

“We are pleased with the overall performance of the Group in the 15 week period given the difficult UK retail environment. We achieved record sales for Black Friday and Christmas thanks to great planning and execution and compelling product and service offers. Particular highlights included the growth in fitting services for car parts, cycle repair and increased sales of bikes, electric bikes and dash cams.”

Shares in Halfords were flat on Thursday morning up 0.06% at 350.2p. The stock hit highs of 361.8p on the 1st January 2018.

Graham Stapleton started his tenure as Halfords’ CEO on 15th January having left his post at Dixon Carphone’s Honeybee. Halfords enjoys strong Christmas trading after record Black Friday

Halfords released their Christmas trading statement on Thursday and pointed to a record Black Friday and a 3.2% increase in sales for the 15 week period to January 12th.

One of the strongest areas of growth was the retail sales of services such as bulb fitting and window blade fitting, up 8%.

Online sales jumped 13% as many customers choose to order online and pick up in store so they could still benefit from the advice given my Halfords staff.

Halfords also gave an update on there corporate strategy pointing to 40 refurbished stores and the growth of their Cycle Republic stores to 19.

CFO Jonny Mason commented on the results:

“We are pleased with the overall performance of the Group in the 15 week period given the difficult UK retail environment. We achieved record sales for Black Friday and Christmas thanks to great planning and execution and compelling product and service offers. Particular highlights included the growth in fitting services for car parts, cycle repair and increased sales of bikes, electric bikes and dash cams.”

Shares in Halfords were flat on Thursday morning up 0.06% at 350.2p. The stock hit highs of 361.8p on the 1st January 2018.

Graham Stapleton started his tenure as Halfords’ CEO on 15th January having left his post at Dixon Carphone’s Honeybee.

CFO Jonny Mason commented on the results:

“We are pleased with the overall performance of the Group in the 15 week period given the difficult UK retail environment. We achieved record sales for Black Friday and Christmas thanks to great planning and execution and compelling product and service offers. Particular highlights included the growth in fitting services for car parts, cycle repair and increased sales of bikes, electric bikes and dash cams.”

Shares in Halfords were flat on Thursday morning up 0.06% at 350.2p. The stock hit highs of 361.8p on the 1st January 2018.

Graham Stapleton started his tenure as Halfords’ CEO on 15th January having left his post at Dixon Carphone’s Honeybee.

CFO Jonny Mason commented on the results:

“We are pleased with the overall performance of the Group in the 15 week period given the difficult UK retail environment. We achieved record sales for Black Friday and Christmas thanks to great planning and execution and compelling product and service offers. Particular highlights included the growth in fitting services for car parts, cycle repair and increased sales of bikes, electric bikes and dash cams.”

Shares in Halfords were flat on Thursday morning up 0.06% at 350.2p. The stock hit highs of 361.8p on the 1st January 2018.

Graham Stapleton started his tenure as Halfords’ CEO on 15th January having left his post at Dixon Carphone’s Honeybee. China growth hits 6.9 percent in 2017

China’s latest economic growth figures have topped expectations, with the economy growing at 6.9 percent in 2017.

This was above a government target of 6.5 percent, according to official figures released on Thursday, and an improvement on 2016’s figure in which the world’s second largest economy expanded by 6.8 percent.

This will come as a pleasant surprise to analysts, who have been concerned over the financial risks in China as the government underwent a restructuring programme.

The government is aiming to keep its growth at 6.5 percent in 2018.

Whitbread released strong year-to-date figures, despite weakness in Q3

Costa and Premier Inn owner Whitbread (LON:WTB) released their third quarter trading update on Thursday, recording strong sales growth despite warning that the environment would be “tough” in the coming year.

The group reported a total sales growth of 6.8 percent in the year to date, and confirmed it was on track to meet full year expectations.

Their hotel chain, Premier Inn, achieved total hotel sales growth of 5.5 percent in the quarter after investment in new hotel capacity, despite weak performance in the third quarter and a lack of demand in London. This was reflected in a flat like-for-like sales figure for the hotels during those three months.

Its coffee chain, Costa, has continued to deliver strong results, with a total sales growth of 7.2 percent. in the quarter. However the markets have reacted badly to its like-for-like sales figure, which fell 1.5 percent in the 13 weeks to 30th November, and could account for why Whitbread shares are currently trading in the red.

The group confirmed that business at its High Street cafes has declined and is likely to remain “subdued”, with Alison Brittain, Whitbread’s CEO, saying that the group “expects the tough UK high street environment and inflation in our sector to continue to pose challenges in the year ahead.”

However she added, “we have good momentum in the delivery of our plan to enhance our UK market leadership positions, create an international business of scale in Germany, China and Costa Express, and develop a more efficient infrastructure.”

Shares in Whitbread are currently down marginally, at 3,853.00 (0815GMT).

Adept4 shares rise as 2017 revenues double

IT service provider Adept4 (LON:AD4) saw shares rise on Wednesday, after reporting strong preliminary results for the year to September 2017.

The group reported revenues of £10.3 million, up from £4.9 million last year, with a gross profit margin of 60 percent.

Recurring revenues came in at £7.3 million, up from £3.2 million the previous year, representing 71 percent of total revenues. The group’s losses before tax also shrunk, to 0.8 million from £1.4 million the year before.

Simon Duckworth, Adept4’s chairman, commented:

“The creation of a single operating platform for future growth has been at the heart of everything that we have sought to do in the last 12 months. The successful establishment of an integrated business with a single brand, proposition, structure and platform was imperative, and I am pleased to report our success in achieving this objective. We look forward to success in the future with this business model.”

Adept4 shares are currently trading up 1.41 percent at 3.60 (1020GMT).

Burberry shares fall after weak performance in foreign markets

Shares in luxury retailer Burberry (LON:BRBY) fell 6.5 percent on Wednesday, as the company fails to keep up with competition in foreign markets.

Retail revenue fell 2 percent during the three months to December compared to the same period last year, from £735 million to £719 million.

Comparable store sales for the group overall rose by 2 percent, with the best performance seen in the Asia Pacific region, where it “grew by a mid-single digit percentage”. In EMEIA performance was less favourable, falling by declined by a low single digit percentage and impacted by strong UK comparatives, with US revenue remaining broadly flat.

Competitors such Hugo Boss performed better during the period, with Burberry continuing to struggle in the American market.

However, the group confirmed its guidance for the full year 2018 in Wednesday, with operating profit remaining unchanged. The group added that it was on track to deliver cumulative cost savings of £60 million in FY 2018.

Marco Gobbetti, Chief Executive Officer, said: “We are making good progress embedding our strategic vision into the organisation and remain on track to meet our full year profit target. We are building on strong foundations and are fully focussed on the successful delivery of our multi-year plan to position Burberry firmly in luxury and deliver long-term sustainable value.”

Burberry shares are currently trading down 6.47 percent at 1669.50 (0847GMT).

8000 Carillion workers on edge as extent of problems revealed

Over 8000 Carillion workers are being faced with the prospect of their wages being stopped, as tougher demands from the company’s banks pushed the bank into insolvency.

Minister David Lidington has confirmed that the Government will continue to pay Carillion’s 11,000 staff who who work in public services jobs, but the clock is ticking for those who work for Carillion’s private sector companies.

Around 8,000 of them face having their wages stopped on Wednesday unless other firms take over the work. According to insolvency documents, the firm is set to run out of cash by the end of the day.

The company entered insolvency on Monday, after insolvency experts skipped the administration process because there was simply not enough cash in the business to keep it running. The depth of the group’s problems, revealed in the insolvency documents, show there is no hope for Carillon’s 30,000 trade creditors to regain the cash they are owed.

Greggs profit sales up 7.4% in 17th consecutive quarter of growth

Greggs, the UK baking group, today announced a respectable seventeenth consecutive quarter of growth in the fourth quarter.

Total sales were up 7.4% and like-for-like sales were up 3.4%.

The company said higher sales were helped by strong demand for their seasonal products and additions to their drink menu.

The firm traditionally know for pasties and sausage rolls, also said more balanced, healthier options had been received well.

Revenue growth was also enjoyed through 90 net new store openings; 131 were opened while 41 were closed. The increase brings Greggs’ total stores to 1854 with an estimated 110-130 net additions in the coming year. CEO Roger Whiteside commented: “We finished 2017 well, delivering our seventeenth consecutive quarter of like-for-like sales growth, and anticipate that we will report full year results for 2017 in line with our previous expectations. “In the year ahead, we will continue to focus on delivering the outstanding value and taste that Greggs is famous for. 2018 will be a record year for investment in our supply chain and we intend to increase the rate of new shop openings as we continue to grow Greggs as a leading food-on-the-go brand.”Making the Balanced Choice… #staystrong pic.twitter.com/HMH6tIv0Cd

— Greggs (@GreggsOfficial) 15 January 2018

Average UK property prices up £2,000 in January, says Rightmove

Average UK property prices were up £2,000 in January, according to data from Rightmove.

Britain’s biggest property website said average asking prices rose 0.7 per cent month on month in January to £297,587. Conversely, asking prices fell 2.3 per cent in December.

However, property prices in the capital were dragged down by falls in Zones 2 and 3. Sellers in Zone 3 witnessed the largest drop, with prices dipping 7.7 percent, and Zone 2 prices falling 6.4 percent.

Remaining cautious over future outlook, Miles Shipside, Rightmove director and housing market analyst, warned:

“Considering some of the gales that buffeted the market in the latter part of 2017, these early readings for 2018 show that there is currently a good following wind of search activity. To keep this year’s initial buyer momentum with you rather than against, serious sellers should note that all regions are currently selling at a slower rate than a year ago, indicating choosier buyers”.

Rightmove revealed that the average asking price for a home in London in January was £600,926, 3.5 percent lower than a year previously, and marking the biggest drop since June 2009.

In the November Autumn Statement, The Chancellor Philip Hammond announced a cut in stamp-duty for first time buyers for properties of up to £300,000.

This reduction in stamp duty and low supply has in turn offset “stretched buyer affordability” and and continued political uncertainy, Rightmove said.

In addition, the website data revealed that visits this month thus far are over nine per cent higher than the same period a year previously, averaging over four million visits each day.

Carillion shares suspended as it goes into liquidation

Carillion entered liquidation on Monday as it failed to secure a deal with lenders, putting thousands of jobs at risk.

Shares in the support services group have been suspended from trading until further notice.

Last ditch talks over the weekend failed to secure Carillion’s future as the banks said they were not prepared to lend them anymore money, effectively pulling the plug on the group who has issued six profit warnings over the past two years.

The government also decided not to bail Carillion out but instead ensured workers would be paid and the Pensions Protection Fund (PPF) said those with Carillion pensions would be protected.

“We want to reassure members of Carillion’s defined benefit pension schemes that their benefits are protected by the PPF,” said a spokesman for PPF.

Carillion employs thousands of worker’f working a broad range of projects from high speed railways to the provision of school dinners.

Chairman Philip Green said:

“This is a very sad day for Carillion, for our colleagues, suppliers and customers that we have been proud to serve over many years. Over recent months huge efforts have been made to restructure Carillion to deliver its sustainable future and the Board is very grateful for the huge efforts made by Keith Cochrane, our executive teamand many others who have worked tirelessly over this period. In recent days however we have been unable to secure the funding to support our business plan and it is therefore with the deepest regret that we have arrived at this decision. We understand that HM Government will be providing the necessary funding required by the Official Receiver to maintain the public services carried on by Carillion staff, subcontractors and suppliers.”

Government makes ‘contingency plans’ for Carillion collapse

The government is preparing for the collapse of the UK’s second largest construction firm, Carillion, after the company entered talks with creditors on Wednesday to save the troubled company from bankruptcy.

The contractor, which has seen its share price plunge over the last year after issuing three profit warnings in a five month period, is also under investigation from the Financial Conduct Authority for “timeliness and content of announcements” made in the summer of 2017.

It entered last-ditch talks with creditors on Wednesday, including HSBC and Royal Bank of Scotland, to encourage them to back restructuring plans. However, on Thursday it emerged that the UK government has drawn up contingency plans for the collapse of the company, which is one of the largest contractors in the government’s HS2 rail programme.

Carillion’s has faced financial difficulties over the last year, dealing with net debts of roughly £900 million and a pension deficit of £590 million. These massively outweigh its stock market valuation of less than £100 million.

Oliver Dowden, the Cabinet Office parliamentary secretary, said in Parliament that the government has made “contingency plans for all eventualities … Carillion is a major supplier to the government with a number of long-term contracts. We are committed to maintaining a healthy supply market and working closely with key suppliers.”

Carillion shares sunk another 15 percent on Thursday, currently trading down 15.18 percent at 19.17 (1208GMT).