Tekcapital shares gained on Friday after the technology incubator released a comprehensive operational update for portfolio company Guident ahead of its proposed IPO.

Guident has made strides forward on numerous fronts in recent months. The autonomous vehicle safety company has been busy improving its technology stack and developing commercial relationships as it pursues the $25 billion opportunity in automotive active safety systems.

The key to a successful IPO will be demonstrating commercial traction and validating Tekcapital’s investment thesis. Today’s update goes a long way toward this by announcing deployments of Guident’s Remote Monitoring and Control Centers (RMCC) and several proposals for additional deployments.

The Jacksonville Transportation Authority has extended its contract with Guident for several autonomous vehicle projects. Simultaneously, negotiations are underway for Remote Monitoring and Control Center (RMCC) deployments at two major educational institutions: Michigan State University and the University at Buffalo.

In Georgia, a new proposal has been submitted for an autonomous vehicle project that includes RMCC capabilities for the City of Peachtree Corners.

Guident hasn’t shared any revenue figures yet, but given the scale of the organisations they partner with, one would assume these deployments would run into millions of dollars.

On the technical front, significant improvements have been implemented, including a redundant multi-network connectivity system that integrates private and public mobile networks using 4G/5G technology alongside both GEO and LEO satellite systems.

The user interface has been enhanced to better manage multi-vehicle and AV fleet operations, while safety features have been upgraded with advanced AI-based Incident Risk Level algorithms.

“We are very excited about the recent progress of Guident and the performance of its leadership,” said Clifford M. Gross, Ph.D., Executive Chairman of Tekcapital.

“We believe the timing for Guident’s potential IPO next year is quite opportune considering the transformative capital market events in the AV industry during the past sixty days. We are looking forward to Guident realising its first mover advantage in the rapidly developing AV industry and the potential contribution it can make to saving lives.”

As Clifford Gross alludes to, Guident is seeking an IPO as autonomous vehicle capital markets activity enters a boom phase.

WeRide’s public offering and concurrent private placement are expected to generate $458.5 million in proceeds, while Waymo secured its largest-ever funding round of $5.6 billion from investors. Meanwhile, Pony.ai has announced plans to raise $200 million at a proposed $4 billion valuation.

Tesla made headlines with its Robotaxi launch announcement in October, and Elon Musk’s new role in the White House is expected to accelerate the rollout of autonomous vehicles as regulations are addressed.

Many states, including California, Florida, Michigan, Arizona, Nevada, and Louisiana, require all autonomous vehicles to have remote control and monitoring functionality.

Tavistock Investments (LON: TAVI) is acquiring Alpha Beta Partners, which is an asset manager with £3bn under management. The business is focused on retail investors, and this will scale up the existing business of offering asset management services to third party advisers. Operating profit was more than £500,000 on revenues of £4m in the year to September 2024. The initial payment is £6m, with the maximum consideration of up to £18m. Two disposals have been completed and the initial payment of £22m will be received in early December. They could eventually generate £37.75m. The share price increased 9.86% to 3.9p.

Portable oxygen devices developer Belluscura (LON: BELL) has secured a credit facility of up to $4m with Sallyport Commercial Finance. This will last for three years and enable the formal launch of the DISCOV-R portable oxygen concentrator, which will be in full production by early 2025. The share price is 7.89% higher at 10.25p.

Recruitment firm RTC Group (LON: RTC) says economic conditions are challenging but it its trading in line with expectations. The shore price is 7.69% ahead at 105p.

Sustainable fuel technology developer Quadrise (LON: QED) says progress has been slower than anticipated, but three projects are moving towards commercialisation and there are other projects in the pipeline. The trial agreement with Cargill and MSC should be signed by the end of the year. Proof of concept should start in the first quarter of 2025. The share price improved 4.05% to 1.605p.

Frontier IP (LON: FIPP) is raising £3m via a placing and subscription at 28p/share. A retail offer via Primary Bid could raise up to £1m. Minimum subscription is £250. The offer closes at 5pm on 25 November. Frontier IP made unrealised gains of £1.3m in the year to June 2024, but there was an overall loss of £1.3m. NAV is 79.7p/share. Despite that, there is a shortage of cash in the balance sheet and the additional cash should last 12 months as the company tries to generate some additional cash from investment realisations. The share price rose 3.57% to 29p.

FALLERS

Webis (LON: WEB) has decided to leave AIM. The US-focused gaming company will seek shareholder approval on 18 December. This will help to reduce costs. The operations remain loss making. The share price slumped 68.8% to 0.125p.

Alien Metals (LON: UFO) says that general meeting resolutions have been sent to some shareholders by mistake. The AGM is on 16 December. The share price fell 8.11% to 0.085p.

Electrical products supplier LPA Group (LON: LPA) traded at near to breakeven in 2023-24 as expected. There will be a restructuring charge, though. Revenues were 10% ahead at £23.8m, but orders fell because of rail project delays. Year-end order book is £25m. There is a potential small acquisition. The share price dipped 4.13% to 58p, which is near to the low for the year.

The Vietnam Holding Investment Trust has achieved something no other London-listed Vietnam-focussed Investment Trust has been able to do for over 15 years – expand the size of its fund by issuing shares to investors.

Vietnam Holding’s strong performance has captured the attention of investors to the extent it has completely erased its share price discount to net asset value (NAV), enabling managers Dynam Capital to issue new shares to investors.

Investment Trusts can only issue new shares to investors when the share price trades at a premium to NAV to avoid diluting existing shareholders.

Vietnam Holding’s ability to do this is remarkable not only because no other Vietnamese Investment Trust has issued shares in over a decade but also because very few Investment Trusts of any asset class or size have delivered a premium to investors and issued shares in recent years.

Vietnam’s growth story has been a core driving force in VNH’s success. However, Dynam Capital’s high-conviction approach to fast-growing Vietnamese equities has set it apart from its peers.

To add context to VNH’s achievement, its peers are still trading at well over 20% discounts to NAV despite having access to the same universe of Vietnamese equities.

While some investors may see value in the wide discounts when considering Investment Trusts, it should be noted that Vietnam Holding has produced the best NAV returns of the single country emerging market Investment Trust space in recent years and has been rewarded with a CityWire AAA Rating for doing so.

Vietnam Holding takes a high-conviction approach to Vietnamese stocks and has built a concentrated portfolio of stocks that play into key themes of digitalisation, industrialisation, and urbanisation.

Their strategy has been amplified by an innovative share redemption scheme that allows investors to realise their shares in VNH at fair market value annually.

The UK Investor Magazine was delighted to welcome Marc Kimsey, Director at F&O Research, back to the podcast for a deep dive into a range of US and UK equities.

We start with a look at macroeconomics and geopolitics before moving on to individual shares.

We discuss Nvidia results and the implications for the wider equity market. The reaction in shares was fairly muted, but Nvidia still holds the key to the entire AI-related rally.

Marc explores UK shares BP, Barclays, and Natwest. Oil prices have weighed on BP and we question how long the softness in BP can last.

Vistry shares have been punished by cost miscalculations that will wipe at least £165m off profit before tax over three years.

The impact is severe, but it’s not an existential threat. Although earnings will be significantly lower this year and damaged next year, the investment case remains very much intact.

There are reasons to be wary of Vistry. However, there are also many compelling arguments as to why the stock now looks very good value.

The risks of discovering further cost miscalculations shouldn’t be ignored. The auditors' forensic investigation into the cause of the problem shou...

One of the best, if not the best, performer in the market yesterday was a tiny loss-making company – Ferro-Alloy Resources (LON:FAR).

Its shares reacted to some very positive corporate news, rising throughout the day to close up over 120% higher at 5.16p, valuing the company at £24.9m.

The company, which is a vanadium producer and developer of the large Balasausqandiq vanadium deposit in Southern Kazakhstan, announced an update on its carbon black substitute product following the completion of a new marketing study.

The ore-resource at the Balasausqandiq deposit contains over...

Main Market miner Hamak Gold (LON: HAMA) has sold its 10.1% stake in Vela Technologies (LON: VELA). These are the remaining shares used to pay for £300,000 of convertible loan notes. The deemed issue price was 0.012375p/share. The Vela Technologies share price has recovered 27.3% to 0.007p.

Iron treatment provider Shield Therapeutics (LON: STX) says it will hit the 2024 target revenues of $31.5m, up from $13.1m, as revenue peer prescription has increased. Recruitment has been completed for an Accrufer phase III study in China. The proposed $10m investment by AOP Health still requires shareholder approval. Costs are being lowered by 10%. Cash flow breakeven should be hit by the end of 2025, if the sales growth momentum continues. The share price rebounded 21.5% to 3.25p.

Airline and tour operator Jet2 (LON: JET2) had a successful summer with first half operating profit improving from £617m to £701.5m. This was better than expected. The interim dividend is 10% higher at 4.4p/share. More than 80% of revenues come from holidays and consumers continue to spend on them. Winter sales are 14% ahead, which suggests market share gains. Canaccord Genuity has raised its full year pre-tax profit forecast from £535.5m to £563.9m. The share price rose 6.06% to 1504p.

Atome (LON: ATOM) says that the IDB proposes to increase its debt funding for the 145MW Villeta fertiliser project in Paraguay to $200m. Environmental and social appraisal has been completed. This means that all the proposals for debt funding outstrip the requirements for the project, although they have not been signed up yet. The share price increased 5.88% to 54p.

FALLERS

Nostra Terra Oil & Gas (LON: NTOG) raised £500,000 at 0.023p/share. This will fund the continuation of a major workover at the Pine Mills asset covering a further four wells. This will boost cash flow from operations. The share price slipped 37.3% to 0.0235p.

Proton Motor Power Systems (LON: PPS) is still falling after it confirmed yesterday that it is going ahead with winding down and leaving AIM. The company has net liabilities. The share price declined 10.4% to 0.145p.

Cambridge Nutritional Sciences (LON: CNSL) reported a 16% decline in interim revenues because of previous stockpiling by customers, but the diagnostics and health company still moved into positive EBITDA – although there was a pre-tax loss. Gross margins are improving, and overheads reduced. Cavendish has cut its full year forecast revenues from £9.4m to £8.8m, but the full year loss is still expected to be £200,000. The share price fell 10% to 3.15p.

Cornish Metals (LON: CUSN) is progressing the NCK shaft refurbishment at South Crofty tin mine. There is cash of £7.1m, including a £7m facility provided by 26% shareholder Vision Blue, which is repayable in March. This will have to be replaced by new financing. The plan is to be producing tin by 2027. The share price is 6.1% to 7.7p.

Ex-dividends

Cake Box (LON: CBOX) is paying an interim dividend of 3.4p/share and the share price dipped 7.5p to 192.5p.

Caledonia Mining Corporation (LON: CMCL) is paying a dividend of 14 cents/share and the share price is unchanged at 885p.

Cavendish Financial (LON: CAV) is paying an interim dividend of 0.3p/share and the share price is unchanged at 10.75p.

Fonix (LON: FNX) is paying a final dividend of 5.7p/share and the share price slid 8.5p to 217.5p.

FRP Advisory (LON: FRP) is paying a dividend of 0.95p/share and the share price is unchanged at 159p.

Jarvis Securities (LON: JIM) is paying a dividend of 1p/share and the share price fell 0.5p to 52p.

Tatton Asset Management (LON: TAM) is paying an interim dividend of 9.5p/share and the share price declined 6p to 696p.

Young & Co’s Brewery (LON: YNGA) is paying an interim dividend of 11.53p/share and the share price fell 3p to 975p.

Yu Group (LON: YU.) is paying an interim dividend of 19p/share and the share price is 20p lower at 1855p.

The FTSE 100 again showed no signs of conviction to move in either direction on Thursday, with a mix of corporate earnings driving trade.

Nvidia was the big talking point on Thursday after the chip maker missed sales guidance expectations for Q4, despite smashing Q3 revenue and earnings estimates.

A 3% drop in the US premarket reflected mild disappointment with the numbers rather than out-and-out fear the AI trade is over. The trend higher for Nvidia earnings is intact, but the massive beats of earnings estimates now seem to be a thing of the past.

Demand for its chips is rising, and there are no signs of a material slowdown. That said, like all growth stories, there will ultimately be a point when growth rates ease back. It doesn’t mean Nvidia sales are going to splutter, although the meteoric rise may be slowing.

The fall in Nvidia shares dragged on US equity futures, lowering the tone and leaving FTSE 100 range on Thursday.

JD Sport was the biggest FTSE 100 detractor on Thursday. The sports fashion retailer sank 15% after announcing a tough trading period and a warning on profits.

“A cautious consumer and unusual weather seems to be a familiar story for many retailers at the moment and JD Sports is no exception,” said Adam Vettese, market analyst at investment platform eToro.

“Cost of living is hardly news anymore but some pre-election trepidation seems to have seen Americans waver on acquiring their latest sportswear purchases. This side of the pond, a mild October caused sales to slump and as such, the company has warned that profit will come in at the lower end of guidance.”

Halma was at the top of the FTSE 100 leaderboard after announcing record sales driven by its ‘Sustainable Growth Model’, which allows its portfolio companies to operate like entrepreneurial smaller companies and capture opportunities.

“Halma continues to shine, delivering record-breaking results as sales pass £1bn for the first time off the back of strong growth across its safety and environmental businesses, even as healthcare faces challenges,” said Matt Britzman, senior equity analyst, Hargreaves Lansdown.

“The company’s focus on sustainability and long-term trends like stricter safety rules and climate change solutions keeps it ahead of the curve. With a series of smart acquisitions boosting its portfolio, Halma’s steady strategy and innovative approach show it’s not just growing – it’s thriving. Looking ahead, Halma’s proven resilience and commitment to making the world safer and cleaner leave it well-positioned for future success.”

George Barrow, co-manager of the Polar Capital Global Financials Trust

Rather than thinking of financials as UK banks plus a couple of insurance stocks, it might be time to see the sector as more like technology or healthcare. Although clearly different in many respects, they are all major global sectors with varied subsectors that diversify risk and offer superior risk-adjusted returns to the well-known large-cap stocks you might otherwise invest in.

Financials is in fact the second-largest global equity sector by market cap, representing 16%1 of the MSCI All Country World Index (ACWI): technology is bigger at 25%, but financials outweighs the next largest sectors – healthcare and industrials (both 11%), and consumer discretionary (10%). It is the most regionally balanced sector, with good exposure to Asia-Pacific and emerging markets. Crucially, it offers excellent diversification benefits against concentrated markets and would be the biggest beneficiary of a rotation from growth to value.

Generally, the sector is economically robust, well-regulated and in our view offers exceptional value. As with technology and healthcare, an informed way to gain exposure to its attractive dynamics, subsectors and themes is through a specialist fund, such as the Polar Capital Global Financials Trust.

Paradigm shift

Following a prolonged period of ultra-low rates which depressed bank returns, the normalisation in interest rates has supported the sector’s profitability. This shift has been recognised by investors, with the sector having outperformed over one and three years2.

The reworking of supply chains, shifts in demographics and the clean energy transition are likely to add to longer-term inflationary pressures. Consequently, we attach a low probability to a repeat of the post-global financial crisis world of zero or negative interest rates, particularly given the unintended social consequences of quantitative easing which exacerbated income inequality. Overall, this points to very different environment for investors to navigate and increases the potential for value stocks to outperform.

The sector dynamics are also attractive as shown by the recent results of the leading UK banks. Regulators’ efforts have paid off and the sector is now extremely well capitalised: indeed, investment returns from UK and European banks are expected to be boosted by strong dividends and share buybacks over the next three years. With around one third of their capital being returned to shareholders, they are projected to sustain around 10% total capital return per annum over the next three years (including dividends and buybacks), assuming a fall in interest rates to around 2%.

Banks and much more

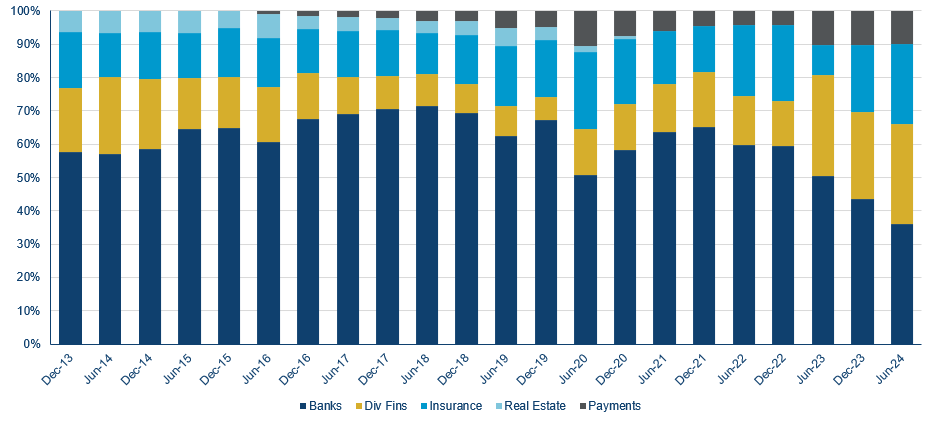

The composition of global financials is also particularly interesting and far broader than many people realise. Banks may account for c43% of the MSCI All Country World Financials Index sector benchmark3, but this is made up of banks from the US, Asia, UK and Europe, and ‘other’, including Canada.

As an example, the Trust’s exposure to North American, UK and European banks (as mentioned above) is complemented by emerging market banks with strong economic growth, increasing penetration of the population, a fast-growing middle class and a shift from public to private sector banks.

We take genuinely active positions in the financials subsectors

Source: Polar Capital Global Financials Team, September 2024.

Otherwise, the subsectors are insurance (c20%: including general, life and multi-line insurers, brokers and reinsurance); diversified financials (c27%: financial exchanges and data, asset management and diversified financial services as well as some niche areas); and payments (c10%: most notably the large credit card operators but also core banking software providers).

Active management

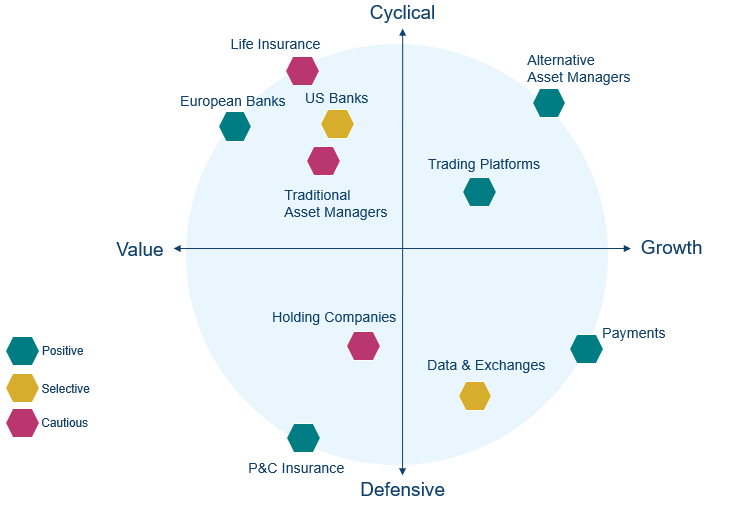

The sector is widely diversified, but as active managers we can also use our insight and experience to allocate to the most attractive regions, subsectors and themes – including technology which is increasing the value of the proprietary data held by financial exchanges (see the chart above). In practice, this means that while financials are overall considered to be value investments, within the Trust we have sub-themes around quality, cyclical and recovery sectors and stocks (see the chart below).

As active managers, we can take advantage of different subsector dynamics

Source: Polar Capital Global Financials Team, September 2024.

Within insurance, which has a low sensitivity to interest rates, reinsurers are experiencing the hardest market for 10+ years, reflecting the higher frequency and severity of losses related to climate change and social inflation. Returns on equity have risen materially from below the cost of capital to the mid-high teens, with this summer’s active hurricane season set to sustain the hard market for at least another year.

The ‘secret sauce’ in the Trust, however, is arguably the diversified financials subsector, which includes financial exchanges and data, trading platforms and alternative asset managers. These can be difficult for generalist investors to follow, but the returns can be compelling as some of the companies are at the forefront of innovation and benefitting from structural trends in the sector.

Summary

The real kicker, however, is valuations: at 12x, the 2025 P/E multiple4 for the financials sector is still low compared to 22x for the broad market (MSCI ACWI)5, and relative to its historical levels. In our view, it is discounting a significant and unlikely deterioration in the macroeconomic environment. The potential for rerating is clear, particularly if there is a general rebalancing of the market away from technology.

2 MSCI All Country World Financials Index versus MSCI ACWI to 30 September 2024; Polar Capital, Bloomberg.

3 MSCI, September 2024.

4 P/E stands for price-to-earnings ratio, which relates a company’s share price to its earnings per share.

5 Polar Capital, September 2024.

This is a marketing communication. Capital at risk. For informational purposes only. This material is not intended to provide advice of any kind. Issued by Polar Capital LLP and Polar Capital (Europe) SAS. Polar Capital LLP is authorised and regulated by the United Kingdom’s Financial Conduct Authority (“FCA”) and the United States’ Securities and Exchange Commission (“SEC”). Registered address: 16 Palace Street, London SW1E 5JD. Polar Capital (Europe) SAS is authorised and regulated by France’s Autorité des marchés financiers (AMF). Registered address: 18 Rue de Londres, Paris 75009, France. Past performance is not indicative of future results. Some information contained herein has been obtained from third party source and has not been independently verified by Polar Capital. All opinions and estimates constitute the best judgement of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital, and may not be achieved.

Nvidia shares were lower in the US market after the chip maker smashed Q3 revenue and earnings estimates but fell short of analysts’ expectations for Q4 revenue guidance.

The 4% drop in Nvidia shares despite sales nearly doubling in Q3 compared to the prior year underscores just how high investors’ expectations are for the chip maker that has led the AI-fueled rally in US tech stocks.

Some called yesterday’s earnings release the biggest ‘macro’ event of the week, highlighting the narrow nature of the US equity rally focused on just seven tech shares and the impact their earnings can have on the global equity market.

Despite missing revenue guidance predictions, Nvidia’s results were nothing short of astounding. The company has nearly doubled its revenue in a year and expects revenue growth to continue apace through the rest of the year. Bloomberg News pointed out that Nvidia’s data centre revenue is larger than the total revenue of both AMD and Intel combined.

“Nvidia has once again breezed past expectations and set the scene for a blockbuster finish to the year. Data Center took the lion’s share of the glory, growing revenue 112% to $30.8bn,” said Derren Nathan, head of equity research, Hargreaves Lansdown.

“And the base of that demand is growing beyond the AWS’s and Azures of this world, with customers of note including Softbank, who are set to become an early adopter of next-generation Blackwell chips and the Danish government. It’s also helping to underpin AI infrastructure with local cloud providers across India, Japan and Indonesia.”

The big question for investors is whether Nvidia’s softer-than-expected sales guidance is enough to derail the broader AI rally. Lower US equity future indicates investors aren’t entirely happy with the results. However, the small scale of the declines suggests investors are marginally disappointed with the results rather than fearful the AI trade is over.