Aquis weekly movers: Chairman provides funds for Valereum

Valereum (LON: VLRM) has completed the £2m raising from chairman James Formolli, while a warrant exercise has generated £9,458. Shares were issued at 0.36p each and on top of that he received 15 million GATE tokens. The cash will finance the growth of the business and development of the GATE token. The share price recovered 14.1% to 4.05p.

Eight Capital Partners (LON: ECP) was hit by a £14.6m unrealised loss on its investments in 2023. That is predominantly down to a reduction in the value of a bond issue by 1AF2, which is due for repayment on 22 July. NAV has declined from £25.3m to £12.8m. Net debt is £862,000. Even so, the share price improved 10.2% to 0.027p.

FALLERS

Shares in Watchstone Group (LON: WTG) went ex-dividend on 4 July. It is returning 8p/share in cash. The share price declined 6p to 2p.

Chris Potts reduced his stake in Shortwave Life Sciences (LON: PSY) from 15.2% to 11.65%. The share price fell 32.6% to 1.55p.

Tap Global Group (LON: TAP) has secured a commercial agreement with Tap N Go for the launch of the XTP cashback programme. XTP is a token for trading via Tap Global exchange services. The share price is 11.1% lower at 0.8p.

Coinsilium (LON: COIN) has been signed a collaboration agreement with Web3b developer Lifeflow Inc, which will have access to $1m of dedicated seed funding. Investee company Greengage is collaborating with global crypto currency exchange Coinbase. The share price slipped 8.57% to 1.6p. Coinsilium is purchasing $75,000 of future tokens in the early backers round of the Otomato Web3 automation protocol. There is an option for $150,150 future tokens.

AIM weekly movers: Helium One Global making progress at Rukwa

Brain tumour treatment developer CRISM Therapeutics Corporation (LON: CRTX) has been hit by a declining share price since joining AIM via the reverse takeover of Amur Minerals Corporation at the end of May. The opening share price was 24p and it had fallen by nearly three-quarters. Non-executive director Gerry Beaney bought 25,000 shares at 9.25p each. Other than that, there was no news from the company. CRISM has developed ChemoSeed, which is a treatment for glioblastoma and high-grade glioma, which are brain tumours where there is no current cure. It is an implantable, bioresorbable drug delivery platform. The share price recovered 200% to 15.75p.

Sancus Lending (LON: LEND) published 2023 results at the end of the previous week showing a £4.8m provision against loans made by previous management. The pro forma loan book was £202m at the end of 2023. UK property loans more than halved during the period. Withdrawal from Guernsey and Gibraltar has been completed. Revenues in the first five months of 2024 were £6.3m. There was initially a fall in the share price, but share buying by chief investment officer James Waghorn and finance director Keith Lawrence helped the share price to improve 144% to 0.55p.

Bluejay Mining (LON: JAY) says there are indications of potential helium and hydrogen accumulations at the Outokumpu licences in Finland. There is up to 5.6% helium and 46% hydrogen, plus other gases. Seismic data has been acquired to identify high potential areas. Helium and hydrogen is the new focus of the company. Non-exec Roderick McIllree bought six million shares at 0.35p each. The share price jumped 65% to 0.495p.

Helium One Global (LON: HE1) is making progress at the Rukwa helium project. An extended well test will start later this month. The required equipment is being delivered. A feasibility study is underway. This helped the share price rebounded 60.8% to 1.174p, which is around the level when the 0.5p/share fundraising was announced.

FALLERS

Pipehawk (LON: PIP) shares slumped 75.3% to 2.1p because of financial difficulties at QM Systems, which had moved to larger premises. Two large orders have not been obtained. QM Systems is likely to be put into administration. QM Systems accounted for 65% of group revenues last year and lost £970,000. The rest of the group should be able to continue as a going concern, although continuing activities made a loss in the year to June 2023.

Martin Andersson has stepped down as executive chairman Chaarat Gold Holdings (LON: CGH) as the company is in restructuring discussions with Labro Investors, which he is associated with. He remains a non-exec. David Mackenzie is acting chief executive. The company has enough cash for the next few weeks but cannot fund the $1.2m repayment due on the Labro convertible loan in September. The restructuring discussions relate to this. The share price fell 63.2% to 1.03p.

Fertiliser producer Harvest Minerals (LON: HMI) has raised £425,000 via a placing and settled £575,000 of director fees through the issue of shares at 1p each. The cash will be spent on the Arapua project to test for rare earth elements. The share price slipped 47.6% to 1.075p.

Pharma mathematical modelling services provider Physiomics (LON: PYC) raised £381,000 at 0.6p/share, which is 50% of the previous market price. A WRAP retail offer generated a further £25,000. In June 2023, £380,000 was raised at 1p/share. The cash will finance the recruitment of a head of mathematical modelling service line and investment in marketing. It also wants to build a biostatics capability and implement a personalised dosing tool on the DoseMeRx platform. The share price dipped 45.8% to 0.65p.

UK stocks cheer Labour victory as housebuilders rally

The FTSE 100 and FTSE 250 jumped in early trade on Friday as investors cheered a Labour victory providing the UK with an opportunity to shake up its economy under Keir Starmer’s leadership.

Labour won a bumper 412 seats on a platform of growth that resonated with both voters and the markets.

The FTSE 100 surged in the early hours of Friday’s session before falling back. However, it was the more UK-centric FTSE 250 that produced a sharp rally as investors jumped into shares well-placed to benefit from Labour’s growth agenda.

A relief rally in the pound demonstrated financial markets’ views on the election result, yet the stronger pound acted as a counterweight to the FTSE 100’s housebuilders and retailers with overseas earners such as HSBC, Rio Tinto, Shell and BP falling on the day.

The FTSE 100 was up just 0.05% at the time of writing, while the FTSE 250 gained 1.2%.

“There is always a sense of nervousness ahead of markets opening the day after a general election, but we only get extreme volatility when investors are caught by surprise. This time round, there was nothing to get heads spinning as the result was widely expected. Instead, investors appeared to welcome the news with open arms,” said Dan Coatsworth, investment analyst at AJ Bell.

“Political uncertainty is over and this removes one of the key risks around UK equities, so it’s feasible that more domestic and foreign investors are now looking for opportunities on the market. This suggests today’s reaction might not be a one-day sensation.”

Coatsworth continued to explain the Labour government could be a turning point for the UK’s beleaguered equity markets:

“Theoretically, we could see a snowball effect whereby the more the UK market goes up in response to the election, the more people start to get drawn in. There is no guarantee that will happen, but such a response would certainly be long overdue given how UK equities have been unloved since the Brexit vote in 2016.”

Housebuilders were clear winners on Friday with Persimmon, Barratt Developments, Taylor Wimpey, and Vistry dominating the FTSE 100 leaderboard.

“Housing was a hot topic during the election campaign, and with Labour vowing to kickstart the development of thousands of additional new homes, the pressure will be on to get the ball rolling. UK house builders such as Persimmon and Barrett have suffered steep drops in share price following interest rate hikes, so they will be hoping for a reversal in fortune if and when these initiatives get underway,” said Mark Crouch, analyst at investment platform eToro.

Expert Opinion: What does a Labour government mean for your investments?

Labour has secured a historic mandate in the general election. It will now set about delivering on its manifesto and providing the policy detail critics say their campaign lacked.

The market was a little moved on Friday, reflecting the telegraphed nature of the result. That said, subtle moves in financial markets could be signs of things to come.

We examine what investment experts think a Labour government could mean for UK investors and your investments.

UK shares

Judging by the market reaction on Friday, equity traders were encouraged by the magnitude of Labour’s victory and freedom it affords them to push through their growth agenda.

Strategists have highlighted several sectors that will enjoy tailwinds under Labour, most notably clean energy and construction.

“In terms of investment strategies, we can expect sectors related to clean energy and infrastructure to experience a boost based on Labour’s pledged policies in these areas. Other key sectors likely to benefit include banking, construction, and retail,” said Yazmin Boden, Partner of GSB Wealth.

“Labour’s pro-growth funding strategy is likely to provide a favourable environment for medium-sized companies listed on the FTSE 250 index. The creation of a national wealth fund and support for key sectors like financial services and automotive should stimulate business investment.

“The anticipated stability of a Labour government – following a merry-go-round period of Conservative prime ministerial changes in such quick succession – is likely to be warmly welcomed by the Markets, its centrist platform having a net positive effect on financial markets, and we could see a stock market uptick going into Q3.”

Housebuilding Shares

Housebuilders were the standout performers in the very early hours of Starmer’s tenure. At the time of writing, Vistry was the FTSE 100’s top gainer, as investors piled into the builder in the hope that Labour would deliver on its pledge to build 1.5 million homes. Persimmon, Taylor Wimpey, and Barratt Developments were not far behind Vistry on Friday.

Mark Crouch, analyst at investment platform eToro, highlighted that Labour were likely to move supportive of home building than the Tories and provide the sector a much-needed boost after years of high interest rates.

Crouch explains, “Housing was a hot topic during the election campaign, and with Labour vowing to kickstart the development of thousands of additional new homes, the pressure will be on to get the ball rolling.”

“UK house builders such as Persimmon and Barrett have suffered steep drops in share price following interest rate hikes, so they will be hoping for a reversal in fortune if and when these initiatives get underway.”

House Prices

Labour’s victory coincided with the release of the Halifax Price Index revealing the average UK prices fell 0.2% in the month to June. So while Labour promises a boost in the number of homes built, it has its work cut out to support prices explained Sarah Coles, head of personal finance, Hargreaves Lansdown.

“The property market is likely to be near the top of the government’s agenda in the coming weeks – and not just the removal van at Number 10,” Coles said.

“However, it isn’t going to make much of a difference in the short-term. House prices and sales have been tepid for most of 2024 so far, and they don’t look likely to warm up any time soon.

“The market is suffering from a dearth of demand, as higher mortgage rates and sky-high house prices have priced so many buyers out of purchases. During the election campaign, there was plenty of talk of stimulating the demand side, but not from Labour. Aside from guaranteeing mortgages for buyers with smaller deposits, it is committed to tackling the supply side of the equation instead. It promised to get stuck into reforming the property market and the planning system, as soon as its collective feet are under the desk in Number 10, but we know this is likely to be a gradual and tortuous process.”

Smaller Companies

William Tamworth, co-manager of the Artemis Smaller Companies Fund, believes Labour’s focus on growth could revive the fortunes of the UK’s smaller companies. Although Labour’s policy details are scant, Tamworth sees the change in government as a positive catalyst for UK sentiment that will ultimately filter down into the UK’s most innovative growth companies.

“The Labour manifesto was light on big promises, but it actually made a welcome commitment to stability – despite being titled ‘Change’,” William Tamworth said.

“Economic and political stability, together with an aspiration to strengthen relationships with Europe, could be an important step in rewriting the current negative narrative surrounding the UK.

“After years of outflows, a small change in sentiment could have a magnified impact on the share prices of listed smaller companies.

“Labour also appears to be supportive towards financial services, describing it as ‘one of Britain’s greatest success stories’. The party suggests it will create the conditions to support innovation and growth in the sector through backing new technology and ensuring a pro-innovation regulatory framework.”

UK Gilt Yields

Gilt yields are likely to fall as the furore around the election subsides and investors settle into a Labour government cautious about pushing through radical changes that could upset sentiment, explained Samer Hasn Market Analyst at XS.com.

“While the Labor Party had made promises to make British politics pragmatic and put rule in the hands of technocrats, in addition to “stopping the chaos” brought by the Conservatives,” Hasn said.

“I believe that these promises, if fulfilled, may provide a state of comfort in the street after the dramatic developments in recent years, thus enhancing the state of certainty, whether economic or political. This is what I also believe may push gilt yields further below, which may put pressure on the pound in turn.

“British bond yields have already declined, but the weakness of the dollar and the decline in Treasury yields appear to have moderated that negative effect and ultimately led to further gains in the pound.”

AIM movers: Pipehawk closing QM Systems and Emmerson proves effectiveness

There is a further rise in the share price of x-ray imaging technology developer Image Scan (LON: IGE) following yesterday’s announcement that it has won a £3m contract to supply ThreatScan portable x-ray systems to NP Aerospace for bomb technicians. There will be a three-month trial process before the contract commences in September. The share price is 12.8% higher at 12.8%. Thart is the highest level since November 2023.

Emmerson (LON: EML) says crop trials confirm the effectiveness of products from the KMP (Khemisset Multi-mineral Process) as a source of phosphate. The process improves potash recovery to 91% and halves water consumption. There is a non-binding offtake agreement with Hexagon, which has agreed to take up to 300,000 tons per annum of struvite-based products and 50,0000 tons per annum of vivianite-based products. Management focus is on securing environmental approval for the Khemisset potash project. The share price recovered 6.25% to 1.7p.

Location data management services provider 1Spatial (LON: SPA) says trading is in line with expectations with new contracts in the US and Europe. There is a strong order book and substantial sales pipeline. The share price rose 1.41% to 72p.

FALLERS

Pipehawk (LON: PIP) shares have slumped 74.7% to 2.15p because of financial difficulties at test and manufacturing systems company QM Systems, which had moved to larger premises. Two large orders have not been obtained. QM Systems is likely to be put into administration. QM Systems accounted for 65% of group revenues last year and lost £970,000. The rest of the group should be able to continue as a going concern, although continuing activities made a loss in the year to June 2023.

Baron Oil has changed its name to Sunda Energy (LON: SNDA) and the share price dipped 3.03% to 0.08p.

1Spatial shares rise after issuing AGM statement

1Spatial, the AIM-listed global leader in Location Master Data Management (LMDM) software and solutions, has released a brief trading update ahead of its Annual General Meeting.

The company reports that full-year trading is expected to align with market expectations as the company purses a growth strategy across the Uk and US.

1Spatial shares were 2% higher at the time of writing.

“Trading for the full year is expected to be in line with expectations. We have secured several new contracts in Europe and the US (as previously announced) in recent months, and we continue to make progress with our innovative 1Streetworks SaaS offering,” Andrew Roberts, Non-Executive Chairman, will say in a statement at the AGM today

“Planned targeted headcount increases across the US Enterprise and 1Streetworks businesses are well underway. With the onboarding of an NG9-1-1 (public safety) specialist in May and a highly experienced sales director joining the Company early in H2 to strengthen the 1Streetworks team. This reflects our approach to ensure our sales and delivery teams have a greater sector focus.

“The Group has a strong order book, a growing recurring revenue stream and substantial sales pipeline underpinning the Board’s confidence in the outturn for FY25. We believe the investments we continue to make in people and technology have positioned the business well to take advantage of the huge opportunity ahead.”

Celebrus Technologies – Next Tuesday Sees Good Set Of Finals Being Announced, Broker Predicts The Shares To Almost Double

It is ‘music to my ears’ – especially when this company clearly states that:

“Annual Recurring Revenue, driven by selling our Celebrus software, is a core focus for the business to drive more value for our shareholders.

Our goal, given the nature of our business, is to have ARR comprise roughly 75% of our total revenues in a given year.”

I really like to see a build-up of ARR by any company, so that statement pleases me as I look at this company’s background.

The Business

Previously known as D4T4, the company which changed its name late last year, classes itself as a disruptive data technology platform, Celebrus Technologies (LON:CLBS) is focused on improving the relationships between brands and consumers via better data.

It redefines what ‘digital identity verification’ means to power both next-level marketing and fraud prevention use cases.

With a blue-chip international customer base, the group, which has offices in the UK, USA and in India, works across over 30 countries and markets itself throughout the financial services, healthcare, retail, travel, and telecommunications sectors.

Celebrus automatically captures, contextualises, and activates consumer behavioural data in live-time across all digital channels and empowers brands to detect and prevent fraud before it occurs through the addition of behavioural biometrics and AI.

By selling more software, the group continues to focus on driving ARR growth with higher gross margins, increasing shareholder value, and building upon its high customer retention rates across the business to drive organic growth.

Celebrus Cloud allows the company to gradually shift away from a reliance on third-party hardware and into a hosting model that drives ARR Managed Services Revenue.

The strong management team has a track record of success in growing software businesses.

While the company, which has a strong balance sheet with ample cash to fund investment into revenue growth, is profitable, cash generative, and dividend paying.

Management Comment

In the company’s 19th March Trading Update, CEO Bill Bruno stated that:

“We continue to emphasize our focus on the Celebrus software platform, with the primary deployment option being Celebrus Cloud.

As the upcoming financial year approaches, we are pleased with our ARR growth and revenue visibility; we will continue to invest accordingly to ensure we execute our strategy successfully.”

The Equity

There are some 40,047,009 shares in issue.

The larger holders include Canaccord Genuity Wealth (11.91%), Investec Wealth & Investment (10.28%), Ennismore Fund Management (4.81%), Chelverton Asset Management (6.34%), Close Asset Management (5.78%), Rathbones Investment Management (4.78%), Peter Kear (2.73%), Peter Simmonds (0.88%), Octopus Investments (0.38%) and Ash Mehta, CFO (0.20%).

Broker Views

The group believes market consensus for FY24 to be revenue of £32.1m, and adjusted profit before tax of £5.4m.

Analysts Andrew Darley and Kimberley Carstens at Cavendish Capital Markets have concluded that:

“With contracts, confidence, and visibility, here is a very interesting stock at the wrong price.”

They currently have a 450p a share Price Objective on the stock.

Their estimates for the results, that are due next Tuesday morning, are for £32.0m (£21.4m) revenues for the year to end March, with adjusted pre-tax profits having risen to £5.5m (£3.7m), lifting earnings to 10.4p (7.7p) and the dividend to 3.2p (3.0p) per share.

For the current year they look for £35.5m sales, £6.0m profits, 11.8p earnings and 3.4p dividend.

Over at Canaccord Genuity Capital Markets its analysts have a Buy rating on the shares, with 330p as their target.

They have fairly similar 2024 estimates but are more bullish for the 2025 year – £34m sales, £6.6m profits, 13.0p earnings and a 3.5p dividend.

My View

The high price-to earnings ratio is said to be more than acceptable within the Software and Services sector.

The £98m capitalised group’s shares are currently trading at around the 245p level, which is on the year’s High.

The broker’s price estimates hold out that there is more upside to go for – so will next Tuesday’s results underline their feelings?

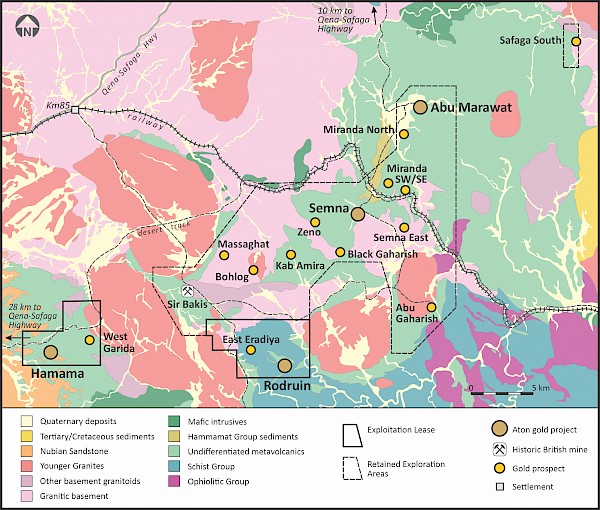

Aton Resources encounter bumper gold grades during Egyptian drill programme

Aton Resources has reported outstanding results from their Semna project with gold grades of up to 11.69 g/t Au, accompanied by 19.1 g/t Ag and 1.38% Cu over a 5.19m interval in their recent phase 2 diamond drilling programme at the Semna gold mine project.

TSX-listed Aton’s Semna gold mine is situated within the Abu Marawat Concession in Egypt’s Eastern Desert, approximately 27km east-northeast of the Hamama West deposit and 13km north-northeast of the Rodruin deposit.

The latest results are a major boost for the company, which is undertaking a three-part strategy to begin production at Abu Marawat while continuing an aggressive exploration programme. Aton plans to begin production at the Hamama project in 2026, and today’s results suggest Semna could not be far behind, with bumper grades pointing to an economically viable deposit.

Aton Resources counts London-listed Centamin as a neighbour. UK investors may be familiar with Centamin’s Sukari gold mine, which is forecast to produce 500,000 ounces of gold in 2024. Aton’s Abu Marawat Concession is approximately 200km north of Centamin’s mine.

For context, Aton Resources’s market cap is equivalent to £15m, compared to Centamin’s £1.5bn valuation.

Aton’s drilling programme, consisting of 28 diamond drill holes totalling 4,701m, was designed to test the Main Vein zone and its eastern extension. The results have confirmed the continuation of blind, high-grade gold mineralisation in the Main Vein zone eastern extension, which remains open at depth and along the strike.

“I am happy to now announce the final results from the recently completed phase 2 diamond drilling programme at Semna, which has continued to show excellent promise with more very significant drill intersections from the eastern extension of the previously mined Main Vein” said Tonno Vahk, CEO.

“The drilling has shown that the high grade mineralisation continues over a strike length of at least 500m, with good mineralisation drilled in the easternmost hole. As always a drill programme raises new questions, including an issue with one of the RC holes, and now is a suitable moment to review the data from the first two drill programmes.

“The presence of abundant coarse gold at Semna suggests that it is important to use as large diameter drill holes as possible, and we plan to return to Semna in the coming months, to continue with a combination of RC percussion and PQ size diamond drilling. However the most important thing is that the persistence of the high grade and coarse gold bearing mineralisation to the east of the old underground workings is quite clear. We are now well into the new diamond drilling programme at Abu Marawat and we are liking what we are seeing so far. We are also making progress at Hamama, with the establishment of Abu Marawat Gold Mines.”

FTSE 100 storms higher after dovish Federal Reserve minutes

The FTSE 100 was in a buoyant mood on Thursday as the UK headed to the polls to vote in the general election.

However, the biggest driver of UK stocks on Thursday was not the prospect of Keir Starmer making a victory speech outside Downing Street tomorrow but the Federal Reserve minutes released last night.

“The FTSE 100 made a strong start on election day but its gains had far more to do with events on the other side of the Atlantic,” said AJ Bell investment director Russ Mould.

The Federal Reserve released minutes last night that suggested US monetary policy makers saw financial conditions easing to a point conducive to reducing borrowing costs.

“Participants highlighted a variety of factors that were likely to help contribute to continued disinflation in the period ahead,” the Federal Reserve wrote in their minutes.

“The factors included continued easing of demand–supply pressures in product and labor markets, lagged effects on wages and prices of past monetary policy tightening, the delayed response of measured shelter prices to rental market developments, or the prospect of additional supply-side improvements. The latter prospect included the possibility of a boost to productivity associated with businesses’ deployment of artificial intelligence–related technology.”

The mention of possible deflation as a result of AI is interesting for the long-term path of monetary policy and what it will do to US AI stocks when they reopen tomorrow.

US markets are closed for Independence Day today, so the true impact of The Fed’s dovishness on global markets may not be felt until tomorrow, by which time we will have received data from June’s Non-Farm Payrolls.

190,000 jobs are thought to have been created last month. Should the headline figure miss estimates, the case for a rate cut becomes much stronger. In such a scenario, one would expect a sharp rally in stocks.

FTSE movers

Gains were broad on Thursday, with 83 of the FTSE 100 constituents trading higher at the time of writing.

UK housebuilders were well bid as traders positioned for a Labour victory and the promise of planning reforms and a boom in housebuilding.

Smith & Nephew was the FTSE 100’s top riser on Thursday after activist investor Cevian Capital took a 5% stake in the firm. The Smith & Nephew share price has had a dismal run, and investors will hope the activist shakes the firm up. Shares were 9% higher at the time of writing.

Next was the biggest faller as the retailer traded ex-dividend.