United Oil and Gas (LON: UOG) has raised £500,000 at 0.2p/share. This will provide cash while the company continues with the farm out of the Walton-Morant licence in Jamaica. The share price rebounded 27.8% to 0.23p.

Celsius Resources (LON: CLA) has executed a binding sale agreement with Chinalco (Xiong’an) Mining Corporation for the disposal of 95% of the Opuwo cobalt copper project in Namibia for $15m. The mineral resource estimate is 225.5 million tonnes at 0.12% cobalt, 0.43% copper and 0.54% zinc. The disposal will allow Celsius Resources to focus on Philippine assets. The share price increased 27.3% to 0.35p.

Hercules (LON: HERC) chief executive Brusk Korkmaz bought 140,000 shares at 28.14p each, taking his stake in the staffing business to 22.4%. The wife of finance director Paul Wheatcroft bought 37,000 shares at 27p each. The share price recovered 23.4% to 29p..

Video games producer tinyBuild (LON: TBLD) chief executive Alex Nichiporchik bought 200,000 shares at 9.3p each. He owns nearly 58% of the company. The share price rose 22.2% to 11p.

FALLERS

River Global (LON: RVRG) has issued D shares to the holders of the A shares. The D shares will be entitled to receive a distribution of Liontrust Asset Management shares issued for the sale of the fund management business. The company will retain some shares in Liontrust and more than £2m in cash to help fund annual running costs of £400,000. Rover Global will remain on AIM for the time being and will decide whether to seek a reverse takeover transaction. The remaining interest in Parmeni9on is estimated to be worth £75m-£90m. The share price reflected the distribution and dived 62.5% to 2.25p.

Shares in ADM Energy (LON: ADME) have been suspended because the 2025 accounts have not been published. They are expected before the end of August. Working capital is constrained. Prior to suspension the share price slumped 44.4% to 0.0125p.

Huddled Group (LON: HUD) raised £1.24m at 0.4p/share via subscription and the retail offer at 0.4p/share was nearly three times subscribed and the online retailer decided to accept £200,000, which was double the amount sought. That takes the total raised to £1.51m. The cash will be spent on increasing stock levels and on marketing activity. Management believes that this should take the business to cash flow positive. The share price dipped by two-fifths to 0.45p.

Mercantile Ports & Logistics (LON: MPL) says the hearing before the National Company Law Tribunal relating to Karanja Terminal & Logistics has been adjourned. There will be a further hearing on 7 August. The port handled 1.2 million MT of cargo in 2025, compared to 1.33 million MT in the previous year. Net debt is £49.6m. The share price fell 36.6% to 1.3p.

Lift Global Ventures (LON: LFT) has bought a 2.18% stake in FourJaw Manufacturing Analytics, which is developing AI and machine learning technology for manufacturing, for £150,000 in shares at 1.5p each. The share price jumped 64.3% to 0.575p.

WeCap (LON: WCAP) investee company WeShop has been added to the US Russell 3000 index. The WeCap share price increased 15.4% to 0.375p.

Coinsilium Group (LON: COIN) chairman Malcolm Palle bought 750,000 shares at 2.05p each. He has a 3.43% shareholding. The share price gained 15% to 2.3p.

Healthcare IT supplier DXS International (LON: DXSP) says full year revenues will be slightly lower than the previous year at around £3.4m. There should be a small profit this year. Ten pilot deployments of the NextGen referral service are active. NHS decisions are still being delayed. The share price improved 8% to 1.35p.

FALLERS

Ormonde Mining (LON:ORM) had cash of €1.09m at the end of 2025 and since then it has received the final deferred consideration for La Zarza. In 2025, cash used in operations was €679,000. The share price declined 12.7% to 0.24p.

Advanced technology developer Vault Ventures (LON: VULT) reported a non-cash impairment of £2.12m for its Dubai activities. There was a cash outflow from operating activities of £2.85m. Cash was £766,000 at the end of 2025. The share price slipped 11.8% to 0.375p.

Vaultz Capital (LON: V3TC) is convening a general meeting on 21 July to gain shareholder approval to end the Bitcoin buying and to sell the remaining holding. The share price dropped 3.92% to 2.45p.

Tomahawk Metals (LON: TMHK) has entered into an advisory agreement with Sven Honig and Voytech Sesulka for new projects for the company to consider. They will also analyse the information on the antimony and gold licences in Slovakia. Sampling will be conducted at the Saturn gold project in Western Australia. The share price decreased 3.7% to 1.3p.

Wishbone Gold (LON: WSBN) had cash of £3.4m at the end of 2025. There was a cash outflow from operations of £2.62m and capital investment of £2.05m. The share price dipped 1.06% to 23.25p.

Dan Higgins, Investment Manager of Majedie Investments, joins UK Investor Magazine to explain how the trust’s ‘liquid endowment strategy’ is built to deliver inflation-beating returns without locking up investors’ capital.

Managed by Marylebone Partners, now part of Brown Advisory, the portfolio is structured around three core strategies: Direct Investments, a concentrated selection of quality stocks managed in-house; External Managers, allocations to hard-to-access boutique specialists operating in inefficient niches of the market; and Special Investments, episodic opportunities alongside some of the world’s leading investors in their highest-conviction ideas.

Higgins explains why the trust deliberately avoids benchmark-driven investing. With so much capital crowded into index heavyweights, he argues that today’s benchmarks carry risks, distortions and biases that are unnecessary for an absolute return mandate and that differentiated assets are increasingly where genuine absolute returns are likely to be found.

The FTSE 100 dipped on Friday, with US cash markets closed for the Independence Day holiday and no fresh catalysts for UK stocks.

London’s leading index was down 0.33% at the time of writing.

After a strong session yesterday, Friday brought a higher degree of choppiness, with the index opening on the front foot before the gains evaporated and turned to losses.

But given that the FTSE 100 hit its highest level since April yesterday, the pullback looks like nothing more than a bout of profit-taking.

Thursday’s rally was sparked by a strong US jobs figure, easing fears of an interest rate hike that could sap confidence among equity bulls.

“Yesterday’s US jobs data pointed to a softer labour market which has raised hopes that the Fed won’t put up interest rates,” said Dan Coatsworth, head of markets at AJ Bell.

“The shift in rate expectations led to a drop in US Treasury yields, meaning the opportunity on fixed income was slightly diminished and thereby dampening one of the drivers that’s taken money away from gold this year. Investors might have seen this market shift and decided it was time to add back some more gold.”

In London, St James’s Place was the best FTSE 100 performer of the session after UBS increased its price target on the stock.

Financials generally were stronger on Friday, with ICG, Aberdeen, and Lion Finance in the top ten risers.

Consumers facing stocks acted as the main drag on the FTSE 100 index. IHG was the top faller, losing 2.3%. Tesco, Diageo, Unilever and Games Workshop were also lower.

Touchstone Exploration (LON: TXP) chief executive Paul Baay bought 183,800 shares at $C0.135 each in the oil and gas company. The share price increased 7.41% to 7.25p.

United Oil and Gas (LON: UOG) has raised £500,000 at 0.2p/share. This will provide cash while the company continues with the farm out of the Walton-Morant licence in Jamaica. The share price gained 4.445 to 0.235p.

Strategic Minerals (LON: SML) has gained local government approval for the expanded drilling programme on the Redmoor tungsten tin copper project in Cornwall. This should be completed in the second quarter of 2027. Drill hole CRD044 has been completed and it intersected the full thickness of the Redmoor Sheeted Vein System.

FALLERS

Hospital charging software provider Craneware (LON: CRW) says that there has been an unexpected slowdown in 340B transactions revenues. This provides discounted drug prices for some people in the US. There were also delays in some contracts. Expected revenues have been trimmed to between $205m-$208m, while EBITDA has been reduced to $65m to $67m. The Craneware share price slipped 18.1% to £11.97.

Oracle Power (LON: ORCP) has raised £500,000 at 0.04p/share. This will predominantly finance the mining projects in Australia and help the move towards gold production in the Northern Zone. There will also be investment in projects in Pakistan. The share price declined 15% to 0.0425p.

Litigation Capital Management (LON: LIT) has been unsuccessful in seeking permission to appeal a competition claim loss. The related value of £800,000 will be written off. The share price dipped 13.65 to 1.72p.

Helix Exploration (LON: HEX) has raised £16m at 22p/share and up to £1.6m more could be raised by a retail offer. The helium producer is spending $11m on the Keyes helium complex. This will enable Helix Exploration to benefit from the full margin on its production from wellhead to the delivery of liquid helium. The range of buyer is broader for liquid helium. The share price fell 10.6% to 23.25p.

Digital health company MedPal AI (LON: MPAL) is raising £5m at 3.5p/share to fund the acquisition of Solid State Technologies, an electronic Medicines Administration Record software provider, and boost working capital to finance record NHS dispensing volumes. The company will invest in stock ahead of expected demand from adding new customers. Each additional customer could add recurring revenues of around £2,400 each year. The share price slid 8.75% to 3.65p.

Craneware shares are likely to come under pressure after the healthcare financial software group said full-year results would fall short of market expectations, blaming a late slowdown in 340B revenue conversion and the deferral of several large enterprise contracts.

The AIM-listed company now expects FY26 revenue of US$205-208 million and adjusted EBITDA of US$65-67 million, both broadly flat on the prior year.

The shortfall stems largely from Craneware’s 340B business, where the final weeks of the year proved materially weaker than anticipated.

While the group has identified around $500 million of outstanding qualifying drug purchases for hospital customers, the pace at which these opportunities converted into actual sales slowed sharply as pharmaceutical manufacturers expanded restrictions on the supply of certain 340B-priced medicines.

A small number of significant enterprise contracts have also slipped into FY27.

This is not what investors wanted to hear, and shares were down 20% at the time of writing.

Next Wednesday, 8th July, The Gym Group (LON:GYM) will be issuing a Trading Update covering the first six months of its current year.

The leading low-cost gym operator could well be guiding investors towards a very fit set of revenues, profits and earnings in 2026.

Its current proposition is highly successful and extremely well rated by its members.

I have to say that I do like the look of the group’s share price, despite it having risen well so far this year.

They now trade at 212p, valuing the group at around £376m, and dep...

MedPal AI has raised £5m in a placing, with the proceeds earmarked for the acquisition of care-home software firm Solid State Technologies and a push to capture the UK launch of the first oral weight-loss pill.

The AIM-listed digital health company secured funding at 3.5p per share, a 12.5% discount to Wednesday’s closing price of 4p, but a 40% premium to the 2.5p at which it raised £3m in April.

Around £0.5m of the proceeds will fund the acquisition of Solid State Technologies, a profitable provider of electronic medicines administration record software used at the point of care in the care homes MedPal Pharmacy already supplies. Bolting eMAR onto MedPal’s robotic dispensing hubs and existing supply relationships completes what the company describes as a closed-loop platform for the care-home sector, covering prescribing, dispensing, administration and reconciliation.

The lion’s share of the funds is being deployed ahead of the UK launch of oral Wegovy on 6 July. Since arriving in the US in January, the pill has racked up more than three million prescriptions in just over five months, with over 80% written for patients new to GLP-1 therapy, according to Novo Nordisk.

MedPal, which has a live weight-loss clinic, a Novo Nordisk supply relationship, and low-cost robotic dispensing, plans to invest in stock and patient acquisition to secure a large launch cohort, with each active private patient forecast to generate around £2,400 in recurring revenue per year.

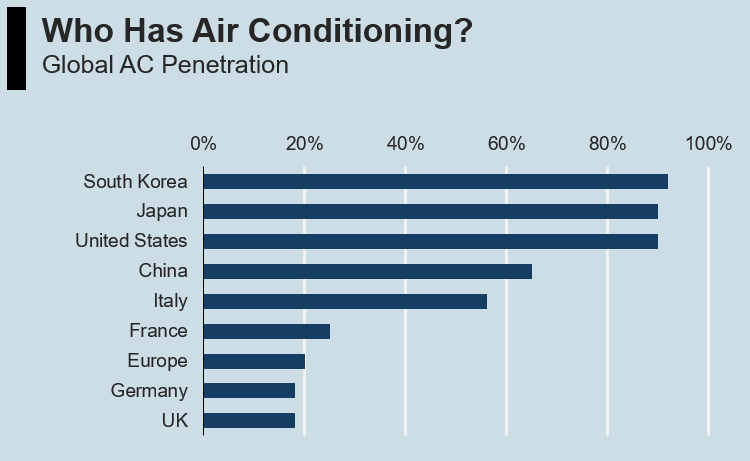

Europe’s AC deficit: Europe sits at roughly 20% air-conditioning penetration, significantly lower than other major economies such as the United States and Japan, which both sit above 90%. A Chinese product innovation is breaking the installation barrier that kept AC out of reach for most households.

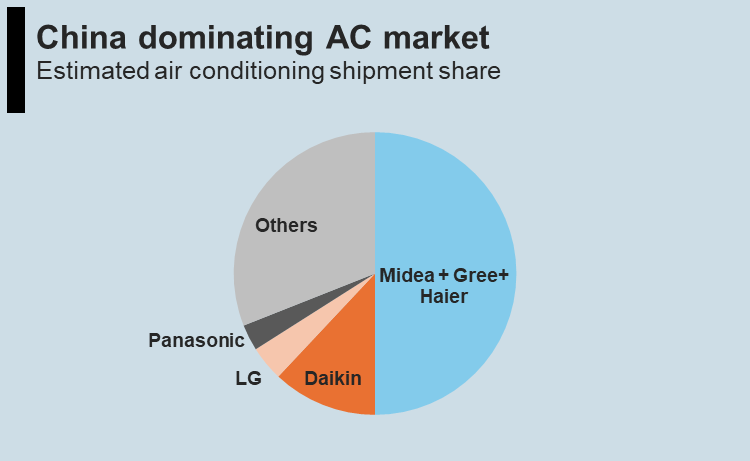

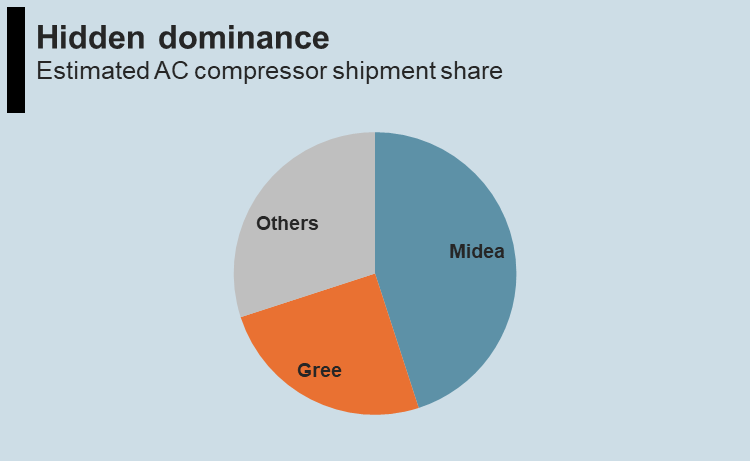

Who Controls the Pyramid: Haier, Midea and Gree produce roughly 50% of residential ACs globally. In addition, Midea and Gree control 70-75% of global AC compressors – a hidden dominance inside every AC and heat pump, regardless of brand badge.

Hidden second wave: Heat pumps are ACs that run in reverse, using the same compressors and valves. Europe’s regulation is accelerating heat pump adoption, effectively adding a second demand stream through the same Chinese supply chain.

An €800 air conditioner selling for nearly €3,000 on Germany’s secondary market.

That is the price of a Midea PortaSplit (split AC), during Europe’s latest heat wave in June 2026. It has been sold out across Germany for weeks. According to braucheklima.de, a Midea PortaSplit tracker site in Germany, only one store out of 1179 branches in Germany has stock on June 30, 2026.

Europe’s AC Deficit

Europe sits at roughly 20% air-conditioning penetration, significantly lower than other major countries such as the United States and Japan, which both sit above 90%.

The deficit is structural, not cyclical. The World Meteorological Organization has documented that Europe is warming at more than twice the global average.

Source: IEA, Statista, various other sources, AP estimates

Europe can be divided into three distinct cooling markets.

Southern Europe — Replacement/upgrade demand: Spain and Italy run at 40-60% penetrations, and Greece is estimated to have a higher penetration rate of over 70%. This represents an established installed base where the primary demand driver is replacement cycles and efficiency upgrades.

Western and Northern Europe — first-time buyer market: France and Germany run at 20-25% penetration. These represent the lowest penetration among major global economies. Heatwaves in recent years have shifted consumer behaviour, stimulating AC demand.

Central and Eastern Europe — price-sensitive growth market: This region is estimated in the 15–30% range. This is the entry point for Chinese brands on price-competitive branded units, competing against incumbents on cost.

Crossing the Installation Hurdle

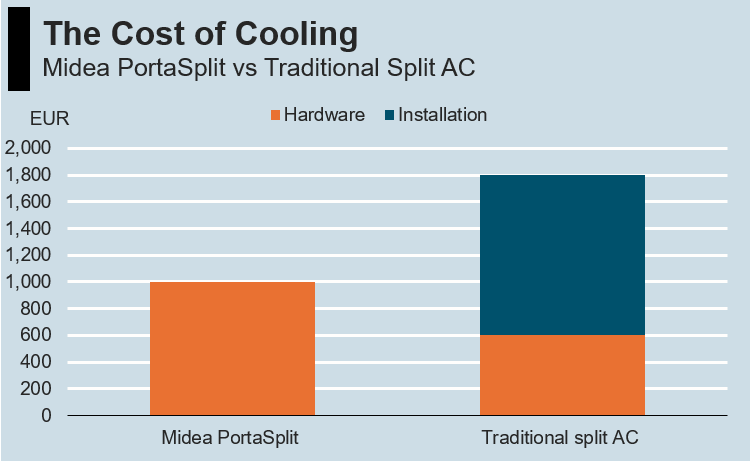

Installing a traditional split AC in Europe is not straightforward.

The installation costs €1,000 to €1,500 in labour alone. For a €500 to €800 hardware purchase, the installation cost multiplies the total.

Source: Companies, AP estimates

In addition, it must meet various country-level regulations:

Spain: the outdoor unit alters the building facade, which is a shared property right. Installation requires a three-fifths majority vote by the owners’ community.

Italy: only certified professional technicians may install split systems.

France: any system with more than 2 kg of refrigerant charge requires a certified inspection. Most traditional split units exceed this threshold.

Switzerland: energy efficiency must reach SEER class A++ or higher, a rating many older or low-cost models cannot meet.

Midea’s innovative product, PortaSplit, addresses this. It is a split AC: an indoor unit connected to an outdoor condenser by a pre-charged refrigerant line with quick-connect fittings.

It is designed around the above installation barriers.

The outdoor unit sits on a bracket that clamps into the open window frame. No drilling or modification is required.

Its 0.62 kg of refrigerant stays under the French 2 kg threshold.

Its energy efficiency fits into the Swiss A++ bracket.

The product category, DIY split ACs, did not exist at scale before. It won TIME’s “Best Inventions of 2025” award.

Midea debuted it in Germany in 2025, and expanded to France, Italy, Denmark, and the Netherlands in 2026. It was met with stockout across Germany by mid-June 2026.

Source: The company, AP

Who Controls the Pyramid

The air conditioning supply chain is dominated by Chinese players.

Haier, Midea and Gree produce roughly 50% of residential ACs globally. Including OEM production for legacy brands, China accounts for ~70% of room ACs.

Source: The companies, AP estimates

Daikin: The “Last Samurai”: Daikin remains the major non-Chinese player with a strong position in the premium and commercial segment.

How did three Chinese companies dominate the world’s AC market?

Japan ruled the 1980s and 1990s: Daikin, Mitsubishi Electric, Panasonic, Toshiba, Sanyo commanded premium pricing and margins.

Korea rose in the 2000s: LG and Samsung added design and marketing and undercut on price.

China’s domestic housing boom: created a 100M+ unit-per-year domestic AC market. Midea, Gree, and Haier scaled on that structural trend. The volume gave them economies of scale.

Brand acquisition: Chinese brands then bought the pyramid: Haier acquired Sanyo (2012), Fisher & Paykel (2012), and GE Appliances (2016). Midea bought Toshiba’s appliance business (2016).

The “Component Toll”

Midea and Gree control 70-75% of global AC compressors. Sanhua controls over 45% of HVAC thermal expansion valves and electronic expansion valves, the precision components that determine inverter-class energy efficiency. These are the bottlenecks inside every AC unit and heat pump, regardless of brand badge.

Source: The companies, AP estimates

For example, Europe’s AC and heat pump makers are largely assembly operations. They import compressors and valves from Asia and assemble branded finished units in European factories.

Europe has almost no domestic compressor capacity at scale.

Capacity concentration: China produces roughly 80% of the world’s AC compressors. Building equivalent capacity in Europe would take three to five years and require a skilled industrial workforce that does not exist at scale.

Cost advantages: Chinese compressor costs benefit from a domestic market that installed roughly 100M AC units per year. European demand, measured in low millions, cannot match this scale economics.

The Hidden Second Wave

China’s dominance in AC compressors and valves positions it to capture the European heat pump market — a market currently riding on the regulatory tailwind.

The technology connection: Every modern AC with a heat mode is already a heat pump. The refrigeration cycle is identical — a compressor circulates refrigerant between two coils, and a reversing valve flips the flow direction. The same Chinese factories that supply AC compressors also supply heat pump compressors.

Cost and efficiency: Heat pumps do not burn fuel. They run at 3-4x efficiency compared with traditional gas boilers. Despite Europe’s high electricity prices, a heat pump’s efficiency advantage makes running costs roughly equal to a gas boiler — and cheaper with subsidies.

Regulatory tailwind: European governments are accelerating heat pump penetration via legalisation.

EU: Targets to double heat pump deployment every 4 years; fossil boiler phase-out by 2040 and ~60M additional heat pumps by 2030.

Germany: New heating must be ≥65% renewable from 2024 — effectively banning gas boilers.

UK: 600K installs per year by 2028; gas boiler ban signalled for 2035 — £7,500 grant per installation.

France: New buildings must have low-carbon heating — heat pumps are default compliance

Netherlands: Gas grid connections banned for new buildings from 2018.

The European Heat Pump Association estimates roughly 25.5M heat pumps installed as of end-2024, while the REPowerEU target requires 60M by 2030. EHPA warns the EU could be 15M units short. Daikin itself projects 250% market growth by 2030.

Who dominates today

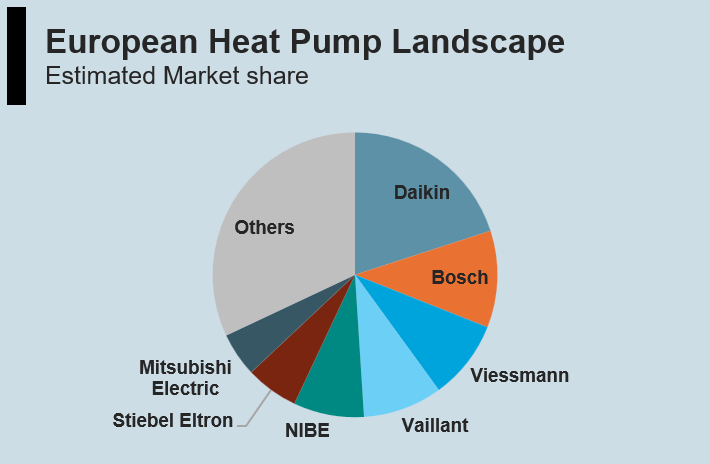

The European heat pump market is led by Japanese and German brands. Daikin is the single largest player. Bosch, Vaillant, Viessmann, NIBE, Stiebel Eltron, and Mitsubishi Electric follow. Chinese brands are not yet major players.

Source: EHPA, JRC, companies, AP estimates

But these market leaders are assembly operations that depend on Chinese components. The compressors inside likely come from GMCC or Gree. The valves likely come from Sanhua.

Midea’s PortaSplit is the bridge. It is marketed as “the first DIY heat pump”. It is currently a minor player in the broader heat pump market, where whole-house hydronic systems generally cost €12,000 to €40,000. The PortaSplit at €900-€1,200 is a room-level solution, not a whole-house replacement, but it demonstrates that the underlying technology does not need to cost five figures.

As heat pumps shift from premium green technology to regulated compliance item, the category could commoditise. Chinese brands, with vertically integrated supply chains and the lowest component costs, are structurally positioned to capture the volume end of this transition.

Daikin: The Last Samurai

Daikin (TYO:6367) dominates European heat pumps through premium branding and installer relationships. But its position is currently under pressure.

Price-sensitive demand: Europe’s fastest-growing AC segment is first-time buyers at the low end. PortaSplit at €800 delivers split-AC performance at a fraction of the €2,000+ installed cost of a Daikin premium split product.

Dependent on Chinese supply: Daikin’s volume models use compressors from GMCC and Gree, leading to higher costs than vertically integrated Chinese players.

Commoditisation by regulation: As heat pumps shift from premium green technology to regulated compliance, customers tend to go for budget options. Premium branding matters less when demand is driven by regulation.

This article is a “periodical publication” for information only and is not investment advice or a solicitation to buy or sell securities. This article does not constitute a “personal recommendation” or “investment advice” under UK FCA regulations. Investing in equities involves significant risk. The author holds NO position in the securities mentioned. There is no warranty as to completeness or correctness. Please do your own due diligence or consult a licensed financial adviser. Please read the Full Disclaimer before acting on any information. Images created with the assistance of AI.

Automated trading is really evolving as more market participants move beyond traditional momentum strategies. Rather than chasing trends that may already be losing strength, many serious investors are paying closer attention to systems designed to identify price exhaustion and potential reversals before they fully develop.

In today’s currency markets, reacting really quickly isn’t always enough. You also need to recognise when a trend is close to running out of steam.

While many algorithms are built to follow momentum, counter-trend systems focus on the moments when markets become overstretched. Automating this process reduces much of the hesitation that can affect manual decision-making while providing a more structured approach to risk management.

Shifting From Trend-Following to Counter-Trend Logic

For years, trend-following has been the dominant approach to forex trading. The idea is simple: identify a market moving in one direction and stay with that move for as long as it lasts. In reality, however, many traders enter too late, just as momentum begins to fade. When the market reverses sharply, those late entries can quickly become costly.

This challenge is one reason automated counter-trend strategies have gained more attention on MetaTrader 4. Instead of joining an established move, these systems search for signs that a trend is reaching exhaustion.

Technical indicators such as the Relative Strength Index (RSI) and Bollinger Bands help identify overbought or oversold conditions, allowing the software to look for the beginning of a new move rather than the end of the old one.

Risk controls are built into the process. Tight stop-loss orders and carefully defined take-profit targets help the algorithms respond consistently to short-term market corrections. Rather than relying on instinct, the system applies the same rules to every opportunity, aiming to identify pricing inefficiencies before broader market participation shifts.

Unlocking Precision in Advanced Trade Execution

Successfully trading reversals depends on far more than a single technical indicator. Markets move quickly and relying on a single signal often creates delays that lead to poor timing. For that reason, many developers build a MetaTrader strategy automation running bidirectional systematic currency entries to analyse multiple market conditions simultaneously.

This type of framework evaluates price action across several timeframes while managing both long and short opportunities. Instead of reacting emotionally to sudden market moves, the software studies live candlestick behaviour and looks for confirmation that a trend is genuinely losing strength before executing a trade.

Institutional-grade order routing also helps reduce slippage during periods of elevated volatility, improving execution quality when market conditions become unpredictable. The result is a rules-based process that replaces guesswork with measurable decision-making and provides a more consistent way to navigate changing currency markets.

Balancing Risk With Quantifiable Drawdown Protection

Counter-trend trading has always carried one obvious concern: entering too early against an existing move. Buying while prices continue to fall or selling into a strong rally can quickly increase losses without disciplined risk controls.

Automated systems address this by embedding protective measures directly into their trading logic.

Fixed Capital Minimums: Operating with defined account baselines, such as a minimum balance of 1,000 USD, helps maintain the intended risk structure.

Historical Drawdown Caps: Higher-tier systems monitor long-term performance data and maintain a maximum historical drawdown of 40.12% across multi-year testing dating back to 2016.

Dynamic Stop Distribution: Instead of concentrating risk in one large position, exposure is spread across multiple smaller entries.

Together, these safeguards help preserve capital during prolonged periods of unusual market behaviour while providing investors with greater transparency in assessing portfolio risk.

The Crucial Role of Specific Timeframes

Timeframe selection plays a significant role in reversal trading. Very short charts, such as one-minute or five-minute intervals, often generate excessive market noise, increasing the likelihood of false signals. At the other end of the spectrum, daily charts may react too slowly to capture shorter-term turning points.

Many systematic strategies therefore prioritise the 30-minute (M30) timeframe. This interval offers a practical balance for highly volatile markets, including gold (XAUUSD), by providing enough price history within each candle to confirm meaningful structural changes while filtering out much of the random intraday movement.

Using the M30 timeframe also helps reduce overtrading, limiting unnecessary transaction costs from spreads and commissions. Under this structure, algorithms typically execute between zero and seven higher-probability trades per day.

This measured pace keeps exposure under control during periods of low liquidity while allowing the system to respond when genuine reversal opportunities emerge.

Integrating Reversal Automation Into Portfolios

Diversification remains an important objective for many investors. If a portfolio relies primarily on equity indices or conventional trend-following currency strategies, adding an automated counter-trend system introduces an approach that behaves differently under changing market conditions.

Because these systems are designed to perform during consolidation phases and market reversals, they may continue generating opportunities when traditional breakout strategies struggle. Capturing shorter-term pricing inefficiencies can add another layer of diversification while helping smooth portfolio performance during periods of heightened volatility.

These systems can also be managed remotely through a secure virtual private server, with performance monitored in real time from mobile devices. This setup allows investors to maintain oversight without constantly watching charts or manually timing every market move.