Direct Line shares were down 27% on Wednesday after the insurance group scrapped their dividend due to higher than expected claims due to bad weather.

Total claims are now expected to be £140m, significant higher than the previously estimated £73m. Claims associated with the cold weather are expected to be around £90m.

Having paid out £1.5bn of capital over the last 5 years in dividends to investors, the sharp jump in claims meant Direct Line are being forced to scrap their final dividend for 2022.

Direct Line also said they were writing down the value of their property portfolio by £45m due to a softer property market.

“News that Direct Line won’t be issuing a final dividend this year has rattles markets, with shares down around 27% in early trading. December’s cold spell has caused a significant increase in bad weather claims, with the estimated cost somewhere in the region of £90m,” said Matt Britzman, Equity Analyst at Hargreaves Lansdown.

“To make matters worse, motor claims ticked higher as well as third party claims inflation. All in, the fourth quarter presented some serious challenges, and the end result is a weaker capital position with the dividend on the chopping block. It’s not too surprising to see the dividend some under pressure though, the forward yield’s been trending above 10% for most of the second half of 2022 and looked likely to be revised lower at some point.”

Despite pressures from bad weather, train strikes and the like it was apparent that the customers of the Nightcap (LON:NGHT) bars continued to increase its cheer.

The thirteen weeks leading up to and just after the Christmas festivities saw the portfolio of 36 cocktail and late-night bars across the country report a 60.9% increase in revenues.

Expansion through a programme of organic growth aided by new strategic openings has been impressive.

Revenues for the 26 weeks to 1 January 2023 were £23.2m (£15.9m), the improvement clearly showing that the Nightcap group bars have proved popular with its target customers.

CEO Sarah Willingham stated that:

“To achieve quarterly growth of 60.9% in revenue and 4.7% growth on a like-for-like basis represents a monumental effort, not least during a time when rail unions deliberately chose a number of the biggest most important weeks and weekends for hospitality, for their series of significant rail strikes, including the incredibly important Christmas weeks.

During the first half of our current financial year we also successfully opened another six phenomenal bars across the country, while also delivering record breaking amounts of corporate Christmas parties and a New Year’s Eve which was sold out across most of our 36 sites.

This result is a testament to the resilience of our high disposable income Millennial and Gen Z customers, who continue to enjoy social interactions in a fun party atmosphere in our bars across the country.”

Second Half confidence

Looking forward to the second half of the financial year, the group’s Board has confidence that, in the absence of further rail strikes or other major interruptions, the group will trade in line with management’s expectations.

Analyst Opinion

Matt Butlin at the group’s brokers Allenby Capital currently has estimates out for the year to end June 2023 for takings rising to £49.3m (£35.9m), with adjusted EBITDA of £3.67m (£3.31m), pre-tax profits of £399,000 (£24,000), taking earnings up to 0.55p (0.23p) per share.

For the coming year his figures suggest an increase in takings to £58.0m, EBITDA £5.0m, a leap in profits to £1.67m, with earnings almost doubling to 1.04p per share.

Conclusion – looking for price recovery

The shares of this £18.1m capitalised bars group offer significant price recovery prospects.

Since the group’s IPO in early 2021 they have been up to 35.5p and have subsequently been down to 6.5p.

Now at just 8p they have good upside potential as the group pushes forward into 2023.

AT85 Global Mid-Market Infrastructure Income (LON: AT85) is the first investment fund to launch an offer in 2023. The initial issue is 300 million shares at 100p each and that could be topped up with the issue of a further 700 million shares after flotation.

The initial placing and offer for subscription has opened and the subscription closes on 22 February. The expenses will be £6m, so the NAV will be 98p a share. Subsequent issues can happen from 2 March.

Winterflood Securities is the sponsor, while the investment manager is Astatine Advisors LLC, which will receive 1% of the lesser of group NAV and market capitalisation up until £500m – excluding uninvested cash and money invested in related funds. The annual percentage will then reduce as the company gets bigger until it is 0.8% above £1bn. There will be 85% paid in cash and the rest in shares.

The focus is capital growth and increasing dividends. Total return should be 8%-10%/year over the medium-term. Dividends of 5p a share are targeted for 2024. Money can be borrowed but it cannot exceed 25% of gross asset value.

Infrastructure assets

The company will invest in essential infrastructure or infrastructure-related assets – some of which have inflation-linked income. They should have a steady operating record and predictable cashflow. These could be in North America or Europe.

The three main areas are transport and logistics, utilities and digital assets and they will be under the control of the company’s investment manager. There should be a potential exit for these assets. By diversifying between different areas, it reduces the risk of regulatory change in any particular sector. Investments in hydrocarbon-related assets are likely to be avoided.

There are £92.1m of assets that can be acquired once the cash is raised. There are a further £449m of potential acquisitions.

One-fifth of the initial proceeds will be invested in Alinda Infrastructure Fund IV (AF4) as part of a $1bn fund raising by the fund. Investments include air freight Unit Load Device (ULD) leasing company ACL Airshop and AT85 Global may also invest directly. Waste management vehicles provider BTR and Kansas City data network owner Everfast Fiber Networks are other investments.

Marks Electrical(LON: MRK) continues to outperform its electrical retail rivals and is taking market share. The share price has been on an upward trajectory since last October.

Revenues in the third quarter to December 2022 were one-third ahead at £29.8m and margins are improving. More customers are taking advantage of the installation service offered by the company. Nine-month revenues are 22% higher at £72.9m. The interim growth rate was 15%.

Profit is still likely to be lower this year and earnings certainly will because of the additional shares in issue after the 2021 flotation. Marks Electrical raised £5m at 110p a share when it joined AIM in November 2021. However, Marks Electrical has been able to maintain a good level of profitability even in tougher times.

Full year pre-tax profit is expected to decline from £6.44m to £5.67m, but the strength of the third quarter revenues means that there I a chance that this figure could be beaten. A pre-tax profit of £8m is expected next year.

Although inventories levels are higher, net cash is forecast to improve to £3.87m by the end of March 2023. A full year dividend of 0.67p a share is forecast.

AO World

In contrast, AO World (LON: AO.) third quarter revenues were 17% lower. That was in line with expectations, although full year profit guidance has been raised. The reduction was partly down to eliminating unprofitable business.

Margin improvements mean that AO World should return to profit in the year to March 2023. A full pre-tax profit of £1.8m is expected on revenues of £1.13bn. Pre-tax profit could recover to £20.3m in 2023-24. Even so, the share price fell 5.4% to 65.85p. That is equivalent to 24 times prospective 2023-24 earnings.

In contrast, the Marks Electrical share price rose by 3.9% to 93.5p, which means it is trading on 22 times forecast 2022-23 earnings, but that multiple falls to 16 the following year.

AO World already has a large market share and growing revenues will be difficult – particularly profitably. In contrast, Marks Electrical has scope to grow existing product ranges and move into new areas. Marks Electrical is a much more attractive investment.

Higher utilisation levels and growing order books have combined to give this group confidence that 2023 will help to mitigate any external pressures, while seeing the group strengthen its prospects.

The £47m capitalised Gulf Marine Services (LON:GMS) is a world leading provider of advanced self‐propelled self‐elevating support vessels (SESVs).

The group’s fleet of 13 vessels serves the oil, gas and renewable energy industries from its offices in the United Arab Emirates, Saudi Arabia and Qatar.

The SESVs are used in a broad range of offshore oil and gas platform refurbishment and maintenance activities, well intervention work and offshore wind turbine maintenance work, as well as in offshore oil and gas platform installation and decommissioning and offshore wind turbine installation.

The group has given higher guidance for the current year to end December 2023 for its EBITDA to range between $75m to $83m – which is quite positive.

Executive Chairman Mansour Al Alami stated that:

“Our markets continue to show signs of strength. Vessel utilisation and day rates are continuing to remain resilient amid high demand for our vessels.

As we progress in to 2023, we aim to mitigate the impact of external pressures, including continued high inflation and higher worldwide interest rates, on our margins and maintain our focus on deleveraging and delivering on operational efficiencies.”

Analyst Opinion – Target Price of 20p a share

Daniel Slater at Arden Partners has a Buy rating out on the group’s shares, with a Target Price of 20p, over four times the current market price of just 4.6p.

His estimates for the year to end December 2022 are for sales of $128.1m ($115.1m) while adjusted pre-tax profits could rise to $25.2m ($20.7m), giving earnings of 1.9c (2.7c) per share.

After this Trading Statement the group has given guidance from which Slater assesses $139.9m sales in the current year, lifting profits up to $29.1m and generating 2.2c in earnings per share.

Conclusion – these shares could easily double

With an order backlog of $369m the demand for the group’s vessels has continued, while improvements in operating efficiencies and strengthening markets will certainly boost the bottom line.

The group’s shares were up to almost 8.7p each ten months ago, they could so easily return to trade at those levels.

Currently trading at only 4.6p each, these shares have the ability to more than double in the next year.

Attention shifted to the macro environment on Tuesday as markets began to prepare for key inflation data from the United States and China, as well as a speech by Fed chair Powell later on Tuesday.

A strong European session on Monday was met by concerns about interest rates in the US session overnight and sparked a wave of caution early on Tuesday. The FTSE 100 was down 0.2% at 7,710 at the time of writing.

“After a Devon Loch style collapse for US stocks late on Monday, the FTSE 100 and other European indices started Tuesday on the back foot,” said AJ Bell investment director Russ Mould.

“Sentiment soured on Wall Street as two members of the Federal Reserve indicated rates would need to move above 5% in 2023 to curb inflationary pressures and this helped erase earlier gains.”

Jerome Powell is due to speak Monday afternoon and will be closely watched for any confirmation of the comments by the Fed members.

Markets will also begin to position for US CPI data on Thursday which has the potential to cause sharp swings in markets. US inflation is expected to fall to 6.5% after dipping to 7.1% last month. A further drop in inflation will be a major positive for risk assets and a precursor for a slow down in rate hikes.

Goldman’s forecasts were not market moving in themselves, but if more economists join Goldman in making more optimistic predictions, it may provide support for risk assets.

Indeed, there is a consensus building that the second half will be considerably better than the first half, and this could provide the impetus to buy into equities.

Katoro Gold (LON: KAT) has appointed Beaumont Cornish as nominated adviser and the share price recovered by two-thirds to 0.175p. Previous nominated adviser RFC Ambrian resigned, and a replacement needed to be found by 11 January or trading in the shares would have been suspended. The minerals explorer requires cash to fund its iron ore project in Namibia.

Subsea cable protection services provider Tekmar Group (LON: TGP) has won several significant contracts worth more than £8m. These will be delivered in the first half of 2023. The share price moved up 32.1% to 17.5p, which is the highest it has been since June.

Industry intelligence provider GlobalData (LON: DATA) says 2022 revenues are at the higher end of expectations. They increased from £189.3m to £242m, with a one-third increase in EBITDA to £86m. Net debt is £252m. Current year forecasts have been upgraded. There is 80% revenue visibility for 2023. There was a 12.7% jump in the share price to 1335p.

Zenova Group (LON: ZED) has received a US order for 7,500 units of the FX500 mini fire extinguisher. The share price rose 11.9% to 11.75p.

Supreme (LON: SUP) had a better than expected Christmas trading period. Vaping revenues continue to grow, while lighting revenues are recovering. The other products are trading steadily. The consumer products supplier is on course for market expectations of 2022-23 earnings of 9.6p a share. The share price is 11.3% ahead at 113p.

Biopesticides developer Eden Research (LON: EDEN) expects 2022 revenues to increase by 50% to £1.8m. New authorisations have boosted product sales. The loss will be slightly lower at around £2.8m. There is still cash of £2m, but this will reduce further this year. The share price improved by 9.4% to 4.65p.

A heavily discounted placing by Nanosynth (LON: NNN) has knocked 23.6% off the share price to 0.21p. The £400,000 was raised at 0.18p a share. This cash will provide additional working capital.

Model railways supplier Hornby (LON: HRN) says that its third quarter sales were ahead of the same period last year. Sales in the first nine months of the financial year are 6% ahead, but management is cautious about the future. Net debt has increased to £7.6m. The share price fell by 19% to 23.5p.

Braveheart Investment Group (LON: BRH) says sales of investee company Phasefocus were lower than expected due to the loss of a distributor. A £300,000 cash raising is planned to fund sales activity. Life sciences subsidiary Paraytec is undertaking a clinical study for rapid diagnostics tests in Sheffield. A lack of NHS staff has delayed the trial and the initial results have been delayed to February. The Braveheart Investment share price declined by 14.5% to 8.125p.

Games Workshop shares dipped on Tuesday after the table-top gaming company said their profit in the six months to 27 November 2022 dropped as a result of external cost pressures.

Despite the drop in profit, Games Workshop achieved record sales in the period of £226m.

“Another rewarding and successful period for the global team with core sales for the six months of over £200 million for the first time,” said Kevin Rountree, CEO of Games Workshop.

External cost pressures put pressure on margins with Brexit costs and the ongoing impact of COVID-19 causing gross margin compression of 4.5% to 64.1%. The company said they now saw Brexit costs as an ongoing cost of doing business.

“First half results for Games Workshop reveal some growing pains for the business. The company has admitted the level of global sales achieved in recent times is a new development and inevitably that creates challenges,” said AJ Bell investment director Russ Mould.

“In many ways it is a positive that management are willing to be so open about the need to learn and improve the way its range of brands and new releases are brought to market. An upgrade to its IT systems is also taking longer and costing more than it previously expected. It is crucial that it gets the basics like this in place if it is to thrive as a global business.”

The Warhammer operator added 20 new jobs in the period as the company prepares for increased demand in the future.

Licensing revenue did fall in the period as a result a recording revenue when a deal was signed, but investors will look forward to further news on potentially lucrative deal with Amazon Studios. In December last year, Games Workshop said they were exploring opportunities with the streaming company but didn’t comment further in today’s update.

Games Workshop have a generous dividend policy and are increasing their payout to 295p per share, up from 165p in the year prior.

It may well be some time until any real value comes back into the shares of the ‘Fridays’ UK operator.

The group’s CEO Robert Cook has decided to step down with immediate effect.

A number of management changes for various reasons has seen the top team being reshaped.

Will it be good enough to handle the current headwinds, bad weather and train strikes?

Red and White-striped

The £15m capitalised Hostmore (LON:MORE) operates ‘Fridays’, the American-themed casual dining brand, and ‘63rd+1st’ the cocktail bar and restaurant chain, as well as the fast casual dining brand ‘Fridays and Go’ – a total of 91 sites across the country.

Situated mainly in locations where footfall is generally high, like shopping centres, city centres and retail parks – the group’s sites gave the group some trade protection, despite the impact of the Quuen’s passing, rail strikes, the Football World Cup and the bad weather.

Analyst Opinion

Following the latest Trading Update analysts Nigel Parson and Michael Clifton at finnCap, the group’s broker, have almost halved their Target Price for the group’s shares from 80p to just 45p.

Their latest estimates for the year just ended see takings up from £159.0m to £196.8m, while the group’s EBITDA will slip from £43.5m to £31.7m.

Pre-tax profits could have swung from a £7.2m positive to a £5.0m loss for the 2022 year, with earnings collapsing from 7.2p to a negative 3.2p per share.

For the current year now underway the brokers are looking for some £213.9m takings, £36.6m EBITDA, and just £0.9m losses pre-tax.

The analysts have pencilled in £232.1m revenues for the group in 2024, with an EBITDA of £41.4m, a pre-tax profit of £2.8m, with earnings of 1.8p per share.

Following the CEO departure and the Update the group’s shares eased 20% to 11.25p.

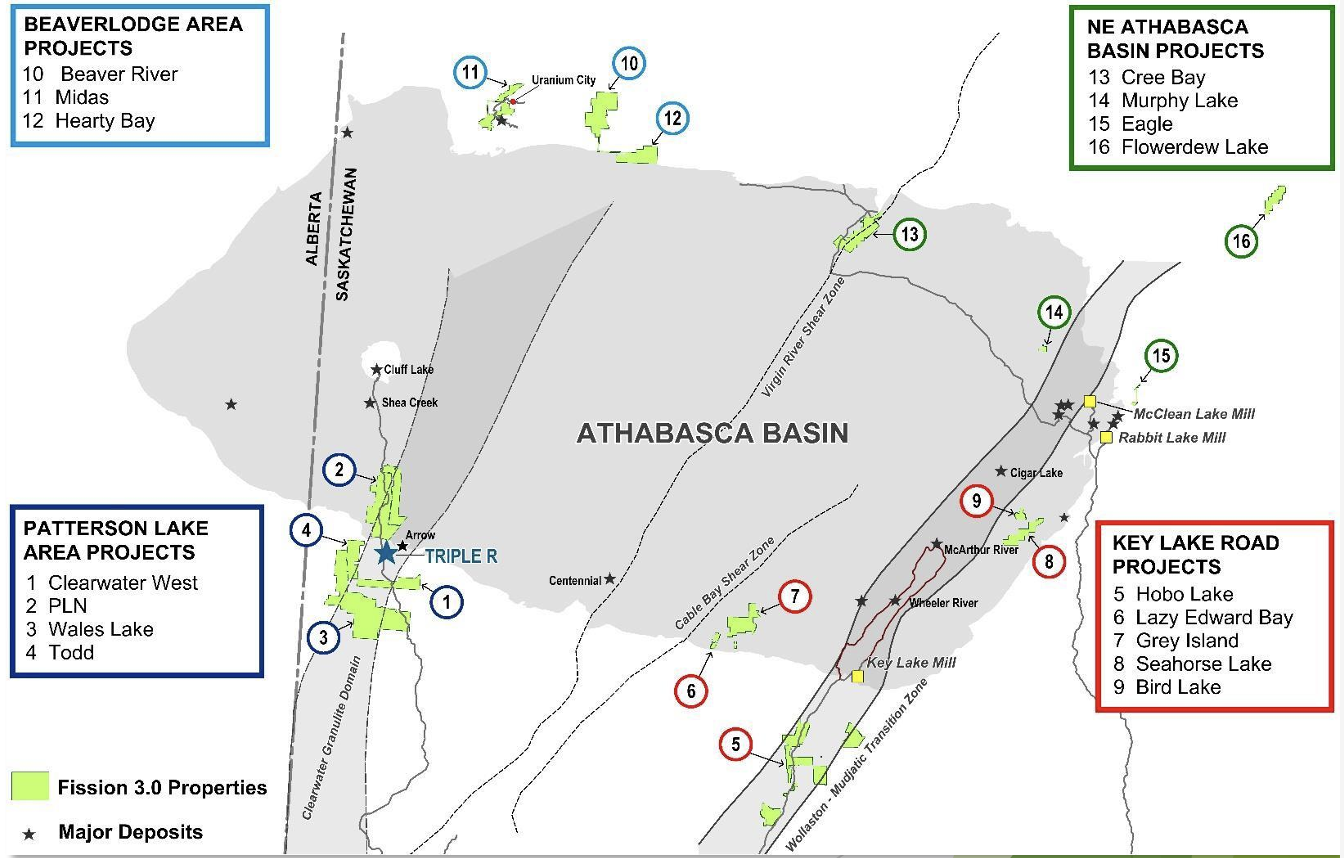

Fission 3.0 Corp (TSX.V:FUU) has established a substantial portfolio of 16 uranium projects across four defined areas in the Athabasca Basin in Canada. The region holds some of the world’s largest uranium deposits and accounts for a significant proportion of global uranium production.

With major uranium producers such as Cameco and Orano as their neighbours in the Athabasca Basin, Fission’s projects sit in close proximity to the world’s top producing high-grade uranium mines.

Fission 3.0 is project generator and exploration company and aims to develop and de-risk uranium projects ready for sale.

Of paramount importance is their Patterson Lake North project which recently produced high-grade shallow depth assays of 15.0 m @ 6.97% U3O8 including a high-grade 5.5 m interval averaging 18.6% U3O8.

PLS Area Projects

The PLS area holds the world class Triple R discovery, Athabasca’s highest grade uranium deposit with mineralisation starting from 50m below the surface.

Fission 3.0 have four projects in the area; Clearwater West, Patterson Lake North (PLN), Wales Lake and PLN A1.

In late December 2022, Fission 3.0 announced assay results at the PLN project that encountered one continuous 15.0 m interval averaging 6.97% U3O8 including a high-grade 5.5 m interval averaging 18.6% U3O8. In addition, the assay revealed a ultra high core of 59.2% over 1.0 m.

Further assay results from the project are due in early 2023.

The prevalence of high grade uranium at the Tripe R discovery substantiates early evaluations at the PLS area making this project area Fission 3.0’s primary concern in the near future.

The Fission 3.0 technical team undergoing the assessment of PLN project have deep experience operating and defining resources the region, having been at the forefront of Fission Uranium’s Triple R discovery at Patterson Lake South. The Fission 3.0 technical team will count the discovery at Patterson Lake South as their third significant uranium discovery.

The Clearwater and Wales Lake projects are considered to be highly prospective and will undergo evaluation in due course.

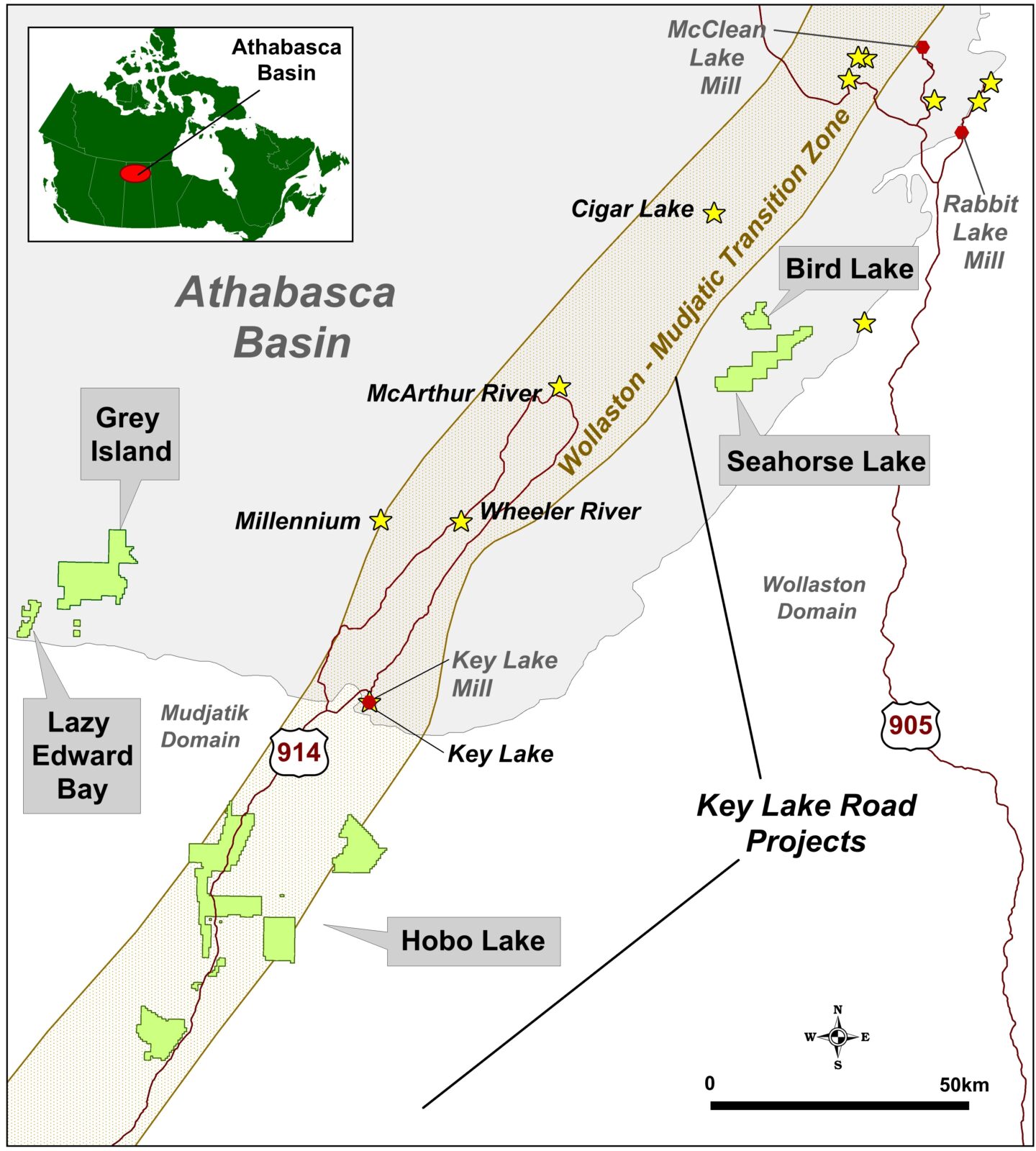

Key Lake Road Projects

The Key Lake Road project group consists of Hobo Lake, Lazy Edward Bay, Bird Lake and Seahorse Lake.

The area previously produced 208M lbs @ 2.32 U3O8 from shallow depth resources and Fission’s project all have confirmed uranium encounters from historical studies.

The project group is located close to refining mills and other uranium mining infrastructure which supports their economics.

Beaverlodge Area Projects

The Beaverlodge Area was once home to 12 open pit mines in the 1950s and 1960s and Fission’s recent survey’s have identified additional areas warranting further exploration.

The four projects in the area are Beaver River, Midas, Hearty Bay and North Sore.

Beaver River was subject to assays in 2007 that yielded results of 3.66% U3O8 (over 0.61m), 3.37% U3O8 and 2.93% U3O8 in the central area of the project. The project consists of 21 mineral claims totaling 19,474 ha.

Midas straddles the Black Bay fault, which is associated with the deposits of Uranium City and Beaverlodge areas. Midas is home to historical uranium mines.

Hearty Bay and North Shore sit in close proximity to uranium encounters and have undergone early stage evaluation.

Northeastern Athabasca Basin

The Northeastern Athabasca region is home to two operating uranium mines including Cameco’s Cigar Lake mine.

The Cigar Lake mine produces 15-million pounds of uranium concentrate per year and is one of the world’s highest grade uranium mines.

Fission’s four Northeastern Athabasca projects are situated on geological structures known to hold high grade uranium. The four projects are Murphy Lake, Cree Bay, Eagle and Flowerdew Lake.