OPEC+ announced its decision today to increase its monthly oil output by a modest amount in line with its previous agreement, boosting its production by an additional 430,000 barrels per day (bpd) from May 2022.

The coalition resisted calls to increase its output past its current level of 11.7 million bpd to make up for the lack of Russian oil supply since the state’s invasion of Ukraine on 24 February.

“The consensus on the outlook pointed to a well-balanced market,” OPEC said in a tweet. “Current volatility is not caused by fundamentals, but by ongoing geopolitical developments.”

“Saudi Arabia will be keen to avoid falling out with Russia by adding extra barrels at a time when Russian production is struggling,” said Callum Macpherson at Investec via Reuters.

The organisation also suspended its use of International Energy Agency data in favour of reports from consultancies Rystad Energy and Wood Mackenzie, following disagreements within the group over the IEA’s data.

UAE Energy Minister Suhail al-Mazrouei criticised the Agency for allegedly being unrealistic in its recommendations, following the IEA’s statement that no new oil and gas projects receive the green light past 2021.

In contrast, Rystad Energy’s stance argued that hundreds of new oilfields would soon be required to handle the level of fossil fuel demand.

The news follows President Biden’s announcement that the US is currently considering tapping into its 180 million barrel Strategic Petroleum Reserve in a bid to replace a level of the global oil supply lost over Russian sanctions.

The White House confirmed that President Biden will be making an official statement on his decision at 17:30 GMT tonight.

London’s small and mid cap markets traded slightly weaker on Thursday following the release of UK GDP figures and the prospect of the US releasing oil reserves hit energy prices.

Brewin Dolphin’s takeover by RBC made the wealth management company the FTSE 250 top riser with a gain of some 60%.

FTSE 250 Risers

Brewin Dolphin shares soared 61% to 512p as the Royal Bank of Canda agreed to buy the investment advice company for £1.6bn.

Rathbone Brothers gained 11% to 1,968p as a positive read across from the RBC acquistion of Brewin.

Trainline shares bounced back from its slump yesterday with gains of 21% to 240p as the travel ticketing company proposed changes to its commission rates.

“The rail industry is undergoing a lot of changes, and this includes reviewing the cut that third party ticket sellers get when they put bums on seats,” said Russ Mould, Investment Director, AJ Bell.

Provident Financial shares increased 2.6% to 325 as the company swung to profit in 2021. The company saw pre-tax profit of £4.1 compared to a loss of £113.5m, despite a 13% fall in revenue.

A decrease in impairment charges from £312m to £50m helped Provident return to profits in 2021. The company also proposed a 12p dividend for 2021 compared to nil in 2020.

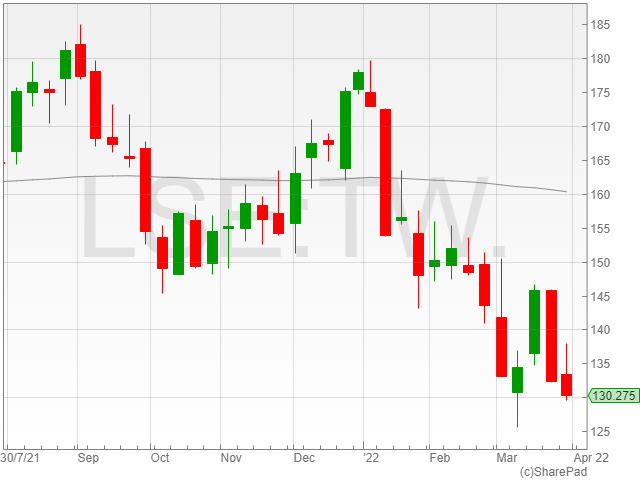

HICL shares gained 0.3% to 177p announced the disposal of its entire interest in the Queen Alexandra Hospital PFI project to InfraRed European Infrastructure Income Fund for £108m.

Retail stocks take the hit as retail spending is at lowest of all time, with Frasers, Pets at Home, WHSmith, M&S, Moonpig and Currys down 2.9%, 1.9%, 0.7%, 0.6%, 0.18% and 0.16% respectively.

However, Vivo Energy and Dunelm Group shares increased 0.22% and 0.27% respectively.

AIM Risers

Mirriad Advertising shares flew 24% to 21.5p when the company announced launch of The Lost Audiences – Regaining Control which highlighted the growth avenue for brands and advertisers to expand their reach via in-content advertising and to engage audiences in an impactful and non-disruptive way.

Renalytix gained 24% to 335p as the company completed a $30m financing package.

AIM Fallers

Xeros Technology shares sank 31% to 61p as the company no longer expects to reach month-on-month EBITDA profitability and breakeven in the first quarter of 2023 due to China restarting lockdowns and India’s slow return to normal operations because of the third wave of the pandemic.

Diamond producer, BlueRock Diamonds fell nearly 30% to 37.5p when the firm raised £2.1m by placing 6m shares at a 35% discount to fund its upgraded mining plans and pay its contractors.

Aukett Swanke shares lost 20% to 1.55p after the company reported a 22% decerase to £8m from £11m in revenues excluding sub consultant costs due to uncertainty in decision making and inevitable delays because of the pandemic.

Business in continental Europe made a profit of £330k exclusding group management charges, however the UK and Middle East business made losses for Aukett.

Kore Potash shares plummeted 15% as the company continues to make losses in 2021, with a pre-tax loss of $2m as opposed to $1m in 2020.

The FTSE 100 was down 0.2% to 7,556 shortly after midday on Thursday after oil prices dropped below $110 per barrel.

The price of Brent Crude was down to $106 per barrel after the US announced a potential release of 180 million barrels of oil from its strategic reserve, in a bid to compensate for the loss of exports from Russia.

Yesterday, the FTSE 100 outperformed European indices helped by stronger commodities. However, the impact of stronger commodities diminished today and London’s leading index joined European shares that were broadly weaker.

“It has felt a bit like the FTSE 100 was singlehandedly being kept afloat by the big oil stocks, BP and Shell,” said AJ Bell investment director Russ Mould.

Shell shares were trading down by 1% to 20,897p and BP shares were down 2% to 374.9p following the developments.

China’s Covid-19 lockdown and Russia’s war in Ukraine are yet to upset the market in a major way, with analysts awaiting the results from crumbling peace talks between the embattled countries and the prospect of advanced lockdowns in China.

The OPEC meeting later today will also bring new developments for the oil market moving into the end of the week.

“Really this is tinkering at the margins. What might put more of a brake on prices is action by OPEC at its meeting later but the extent to which it could increase production, even if it wanted to, is open to question,” said Mould.

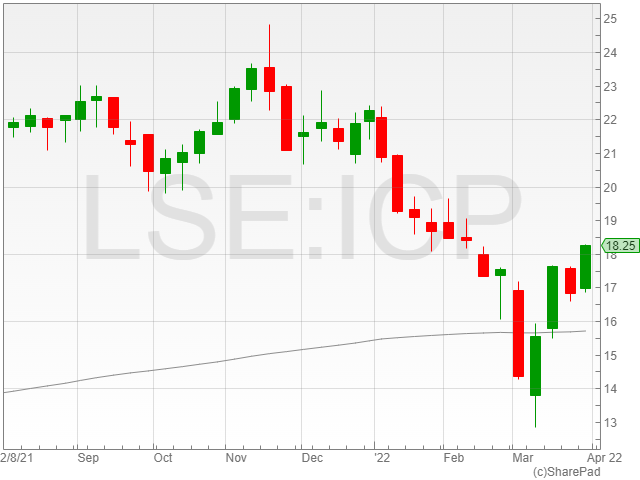

Intermediate Capital Group led the market risers with an increase of 2.9% to 18,232p after the company successfully raised €1.5 billion for its debt Infrastructure Fund, ICG Infrastructure Equity 1.

The group surpassed its initial €1 billion by €500 million as a result of “strong client demand.”

Pearson rose 2.3% to 756.8p as it recovered some ground following Apollo’s withdrawal of interest in the company after the educational services provider rejected its third and final takeover bid.

Halma PLC shares were up 1.8% to 25,340p.

Taylor Wimpey share were trending down 3.5% to 130.1p as Nationwide Building Society said house prices had skyrocketed at their fastest rate of growth in 17 years by £33,000.

Houses are projected to decrease in desirability as inflation spikes and rising energy costs eat into shrinking consumer wallets.

Next fell 3.1% to 60,790p in the retail sector’s decline in sales on the back of rising inflation and falling consumer spending in retail, reported at a 0.3% drop in February by the Office of National Statistics (ONS).

The Royal Mail Group dropped 3% to 335p as it continued its spiral downwards.

Oil prices fell 5% to $107 a barrel, finally dropping from the $110 mark after the Biden administration took steps to control fuel costs by considering a release of 180m barrels of oil from their Strategic Petroleum Reserve.

The Biden administration confirmed that this will be ‘largest-ever release’ since 1974, dating back to when the reserve was created.

For months, global energy supplies have been tightening as economies began to reopen and pandemic lockdown measures were loosened.

However, the global energy markets have been shaken with oil bans and sanctions imposed on Russia for invading Ukraine, as Russia is the second largest global oil exporter after Saudi Arabia.

Biden discussed the potential to supply oil to the EU earlier this month, as EU leaders became wary of their economic progress due to high dependence on Russian oil.

The US is the largest oil producer in the world and currently produces 11.7m barrels per day, which is insufficient to meet global demand.

The US, the UK, and others have already pressed OPEC+ to increase its output, however OPEC+ currently appears unlikely to deviate from its strategy to steadily increase output. Most major energy-producing countries are either at capacity or unwilling to expand output.

It’s uncertain whether other IEA members, including the United Kingdom, France, Germany, and Japan, will follow the US in releasing oil reserves.

Russ Mould, Investment Director, AJ Bell commented, “You can understand why the US leader felt he had to do something, given the political heat he is getting for rising fuel prices, however a speculated release of one million barrels of oil per day over the coming months has to be seen in the context of total global output of around 100 million barrels per day.”

“Really this is tinkering at the margins. What might put more of a brake on prices is action by OPEC at its meeting later but the extent to which it could increase production, even if it wanted to, is open to question.”

HICL Infrastructure announced the disposal of its 100% interest in the Queen Alexandra Hospital Project on Thursday.

The project will reportedly be transferred to InfraRed European Infrastructure Income Fund 4, which is set to pay £108 million to HICL following the transfer.

HICL announced that the £108 million proceeds will represent a 1.5p per share increase on NAV aligned with the company’s valuation on 30 September 2021.

The company invested in the Queen Alexandra Hospital in 2010, and highlighted InfraRed’s active asset management strategy in de-risking and stabilising the project since 2018 as a key factor in contribution to the rising NAV.

The agreement is subject to customary approvals and HICL shareholder approval, however if successful, the disposals are scheduled to be redeployed into the group’s advanced pipeline and to pay down its revolving credit facility.

“The disposal of HICL’s investment in Queen Alexandra Hospital is a tangible example of the Company’s business model in action,” said HICL Chairman Ian Russel.

“HICL, through its Investment Manager InfraRed, seeks to enhance shareholder value in the existing portfolio through active asset management to optimise portfolio performance and composition.”

“The proceeds provide an alternative source of funds to rotate into the Company’s advanced pipeline.”

“The Board unanimously recommends that Shareholders vote in favour of this transaction, as all the Directors intend to do in respect of their own beneficial holdings of Ordinary Shares.”

HICL Infrastructure shares rose 0.5% to 177.9p in late morning trading on Thursday after the announcement.

The UK economy grew faster than expected with GDP growth of 1.3% in the last quarter of 2021 compared to the third quarter, as the health sector saw a boom in business with the arrival of the Omicron variant.

The Office for National Statistics estimated the GDP growth for Q4 2021 to be approximately 1%.

The 1.3% rise in GDP was a step in the right direction for the economy against the 0.9% GDP Growth in Q3 of 2021.

According to the ONS, the household saving ratio reduced to 6.8% in Q4 compared to 7.5% in Q3 2021. Rising customer expenditure in transport, net tourism, clothing and footwear led the increase in household spending as consumers dipped into lockdown savings.

In Q4, real household disposable income dropped by 0.1% whilst nominal households’ gross disposable income grew 1.3%, which was offset by quarterly household inflation of 1.4%.

In Q3, household disposable income adjusted for inflation declined by 0.2% compared to Q2 due to impacts from inflation on household budgets as well as a downward revision of pension contributions.

During the fourth quarter, real household disposable spending increased by 0.5%, underperforming from the initial expectations of 1.2% growth.

However, it was not all bad news, as the UK did manage to shrink its balance of payments to £7.3bn with the help of foreign investments, despite supply chain problems prevailing due to the pandemic.

Government officials monitoring the country’s fiscal condition predicted that with inflation reaching 9%, investors expect the recovery to slow down in 2022 since consumers face a decline in the standard of living.

Danni Hewson, Financial Analyst, AJ Bell said, “It might seem odd, but Omicron actually provided a substantial boost to UK economic growth in the last three months of 2021.”

“Growth was stronger than had been forecast and by the end of the year the UK economy was a hair’s breadth from where it had before the ravages of Covid.”

“But even in the dying days of 2021 inflation was already packing a punch. Household’s disposable income fell, people started to dip into savings as a way to offset those inflationary pressures, put simply people were having to pay more for what they wanted.”

“With the expectation that this year will deliver the biggest fall in living standards since the 1950’s alarm bells are clanging, and damage done to savings and pension contributions in the now will have consequences in years to come.”

“And the squeeze has only just begun, the pressures households were experiencing last year will be nothing compared to what is to come.”

Nationwide chief economist Robert Gardner added that the recent 1.1% month-on-month increase marked the eighth consecutive month of price growth in the housing market.

House prices have hit a 21% rise since the Covid-19 pandemic emerged in 2020, however the market has retained an unexpected level of momentum against the background of rising borrowing costs and shrinking household budgets.

“The number of mortgages approved for house purchase remained high in February at around 71,000, nearly 10 per cent above pre-pandemic levels,” said Gardner.

“A combination of robust demand and limited stock of homes on the market has kept upward pressure on prices.”

“The significant savings accrued during lockdowns is also likely to have helped prospective homebuyers raise a deposit.”

“We estimate that households accrued an extra (around) £190 billion of deposits over and above the pre-pandemic trend since early 2020, due to the impact of Covid on spending patterns.”

Gardner caveated his comment with the insight that older, wealthier households were maintaining the majority of the savings advantage.

However, the housing market is predicted to shrink in coming months as household budgets feel the pressure of climbing credit card debt and short-term borrowing surge on the back of rising inflation and spiking energy prices.

The spy agency head was visiting Canberra, Australia to make a speech at the National Security College on Thursday when he gave his perspective on the current situation in the Kremlin.

Flemming said in a speech on Thursday that Putin’s advisors are “afraid to tell him the truth” about the poorly calculated outcome of his decision to invade the neighbouring state.

The GCHQ head lamented the “barbarity” of Putin’s invasion and the Russian leader’s failure to follow through on his poorly-calculated war.

“Far too many Ukrainians and Russians have already lost their lives. And beyond this toll, many, many more have had their lives shattered.”

“The UN estimate that in just over a month, more than ten million people have already fled their homes. It’s a humanitarian crisis that need never have happened.”

Flemming stated that Putin had over-estimated his military capabilities and under-estimated the effects of sanctions on the Russian economy, alongside the reported refusal to carry out orders and outright incompetence by the Russian army.

“He over-estimated the abilities of his military to secure a rapid victory. We’ve seen Russian soldiers – short of weapons and morale – refusing to carry out orders, sabotaging their own equipment and even accidentally shooting down their own aircraft,” Flemming continued.

He blasted Putin’s poor planning and his inner circle’s overwhelming fear of telling him the reality of his invasion.

US intelligence have commented with similar insights, as officials across the board noted the rising tide of uncertainty within the Kremlin.

US director of White House communications Kate Bedingfield said: “We have information that Putin felt misled by the Russian military which has resulted in persistent tension between Putin and his military leadership.”

“We believe that Putin is being misinformed by his advisers about how badly the Russian military is performing and how the Russian economy is being crippled by sanctions because his senior advisers are too afraid to tell him the truth.”

The war in Ukraine continues to rage on over a month after Russian tanks rolled into the country, however it has become evident that Putin’s military victory is far further from his grasp than he initially predicted.

On Tuesday morning, the Anglo-Russian miner, Polymetal released a statement addressing possible restructures focused on improving shareholder sentiment as the company has faced serious consequences of the Russia-Ukraine war such as heavily imposed sanctions and being booted off the FTSE 100 last Monday.

Russian companies saw investors withdraw from their shares as the tensions grew between Russia and Ukraine and Polymetal was at one pint down over 90% YTD.

Polymetal shares faced serious scrutiny from investors as Russian sanctions were imposed by the West. However, shares have since rebounded and investors will be asking; ‘can Polymetal shares return to 1,000p’?

A Polymetal share price of 1,000p will by no means represent a complete reversal, but it is a significant psychological level for investors.

When the markets started dropping Polymetal shares with the g invasion of Ukraine, the company released a press statement addressing the sanctions and how Polymetal was shielded from the impact.

The company informed investors that Russian sanctions will not disrupt Polymetal’s operations in Russia and Kazakhstan. Apart from the sale of gold bullions being hurt by Russian sanctions, the company’s production guidance is unhindered.

Polymetal assured the markets that they are equipped to handle all liquidity issues that may arise and have stockpiled resources to ensure no disruption is caused to operational activities, at least for the next three months.

The Russian miner’s shares have nosedived 70% to 375p YTD despite their attempts to reassure investors at every stage of the war. Polymetal shares had peaked at 1,729p early June 2021.

Currently, the company has a market cap of £1.1bn with a forward P/E ratio of 1.5, the lowest amongst all LSE listed peers. This alone suggests an inherent value to the shares, despite a heavy discount attributed to Polymetal by the market.

However, Polymetal does have a dividend cover of 30x and a ROCE of 28x, representing the company’s capabilities are in place to handle returns to investors despite times of uncertainty.

On March 2 2022, the miner did announce a proposed final dividend payment of $0.52 will be paid to shareholders in May 2022. The final dividend reduced from $0.89 in 2020 as geopolitical tensions beat up Polymetal’s fiscal position.

Not too long ago, six directors, including chair Ian Cockerill, resigned from the board in an attempt to abandon a potentially sinking ship.

Polymetal have since hired Riccardo Orcel as an independent non-executive chair and installed some stability to the company after a turbulent month. The board now consists of 8 members as Polymetal replace 4 non-executive directors.

Kazakhstan

Polymetal has been analysing the possible divestment of its operations in Kazakhstan as per the request of a group of investors on Monday.

On Tuesday, the mining group addressed ongoing media speculation regarding a possible change in the company’s corporate structure. The group said they are “evaluating various options that could maximise shareholder value.” The statement was meant to relieve investors of their worry and ask them to hang tight while Polymetal figures it out.

On Wednesday, Polymetal reported an increase in net debt from $1.6bn to $1.8bn which it will use towards its seasonal working capital and resource procurement.

Currently the miners have short-term capital financing from Russian banks and is waiting for additional liquidity in Q2 2022.

The company has $0.4bn cash held by institutions which are not subject to Russian sanctions along with a $0.5bn undrawn line of credit.

The company reinterated in the statement that Russian and Kazakhstanian operations are unhindered, and projects in the advance stages of development are back on schedule.

Logistical challeneges having impacted Polymetal’s POX-2 project causing a 3-6 month slippage and early stage projects are delayed by a year.

Pacific POX project is suspended indefinitely while the company look for re-site alternatives for the venture in Kazakhstan.

Junior JVs of the company will suffer due to 50% cuts in the budget of Greenfield exploration.

Polymetal said that its Brownfield explorations schedule and volumes will remain unaffected.

Riccardo Orcel said, “It is my opinion that investors, private and institutional, that collectively control over 75% of this company deserve a Board that will lead the company through this turbulent time, preserving and hopefully rebuilding the value of their investment as well as protecting the livelihood of thousands of employees, contractors, suppliers and other stakeholders.”

The Polymetal share price was up 11% at the time of writing on Thursday.

Sovereign Metals presented its low carbon footprint Kasiya graphite at the UK House of Parliament Roundtable on behalf of the Critical Minerals Parliamentary Group, with the Critical Minerals Association.

The mining group predominantly highlighted the Kasiya graphite’s potential for applications in lithium-ion batteries, which is currently the main market for coarse flake graphite, and traditional industrial applications.

The company noted that the product from its Kasiya mine in Malawi was a quality resource as a result of its high purity and high crystallinity, which is crucial for the material to be upgraded to the minimum 99.95% TGC for lithium-ion battery anodes.

Sovereign Metals estimated that the battery sector is set to be the greatest driver for graphite demand by 2028, with the commodity making up as much as 50% of the average lithium-ion battery composition.

The mining firm said it was capable of producing high-quality coarse flake graphite with a substantially lower carbon footprint than China, where over 75% of the global supply for natural graphite is currently sourced.

The company noted that the graphite from its Kasiya project held an 80% lower greenhouse gas emissions trail than graphite produced in the Heilongjiang Province in China, adding that each tonne of product would produce only approximately 0.2 tonnes of carbon emissions.

“The importance of sustainable supply chains for clean-tech solutions such as lithium-ion battery powered electric vehicles cannot be underestimated,” said Sovereign Metals Chairman Ben Stoikovich.

“As such, Kasiya could become globally strategically important as it has the potential to supply not one, but two, critical raw materials to world economies looking at building a sustainable future and tackling climate change.”

Sovereign Metals shares rose 5.4% to 33.7p in early morning trading on Thursday following the announcement.