“For Christine Lagarde and the gang, increased optimism of an economic recovery in the Eurozone –to be backed up by a new set of forecasts this afternoon – and a region-wide inflation reading that is now beyond the 2% target are the main points of focus,” Campbell added.

That could cause the ECB to begin talks over tapering its €1.85trn bond-buying programme.

“It’s likely that it will be subtle stuff. No policy change announcement, but the removal of certain key phrases in relation to the bank’s bond-buying intentions going forwards. After all, with the Delta variant a threat, the Eurozone is far from out of the covid-woods yet, and the ECB will want to signal to investors that it is still committed to doing what is necessary to support the region,” said Campbell.

“As for the States, this afternoon’s CPI readings could be slightly more market-friendly. Both the standard and core figures are forecast to shrink month-on-month; the former from 0.8% to 0.4%, the latter from 0.9% to 0.5%. It is worth noting, however, that the same was expected last month, and instead we got a pair of recent highs.”

In addition to the inflation numbers is the latest weekly jobless claims reading, which is set to drop to a fresh pandemic-low of 370,000.

Ahead of all the oncoming news, markets were a mixed bag. Sterling’s continued losses against the dollar and the euro allowed the FTSE 100 to clim above the 7,100 mark, while the DAX and CAC fell 0.4% and 0.2% respectively. “The Dow Jones is set to be somewhere in between, currently heading for a 0.1% increase, though that is almost certain to change once the inflation data is out,” said Campbell.

FTSE 100 Top Movers

AutoTrader (6.2%), BT Group (2.91%) and Smith and Nephew (1.78%) are the biggest risers on the FTSE 100 during the morning session on Thursday.

While at the other end, Thungela Resources (-2.06%), Sainsbury (-1.98%) and Just Eat (-1.75%), have seen the biggest falls.

Greatland Gold (AIM:GGP), the precious metals exploration company, provided an update on Thursday regarding the ongoings at the Havieron gold-copper project in the Paterson region of Western Australia.

Drilling activities since the previous report include new results from the current Growth Drilling programme. The latest results from this programme has seen seven new drill holes.

Newcrest has now completed a total of 164,420m of drilling from 190 holes to date, with all the latest holes continuing to intersect significant mineralisation.

Highlights

Excellent results from Growth Drilling continue to support the potential for resource expansion within the Havieron gold-copper mineralised system

High-grade intercepts below the December 2020 Initial Inferred Mineral Resource shell in the South East Crescent Zone and adjacent Breccia Zones, and around the Northern Breccia.

HAD133 returned 85m @ 11g/t Au & 0.29% Cu from 1345m, including 13m @ 32g/t Au & 0.46% Cu from 1363m, and 14.5m @ 32g/t Au & 0.33% Cu from 1396.5m1.

High-grade Crescent Zone remains open at depth.

Additional mineralisation identified in Northern Breccia Zone, highlighting the potential for resource extensions outside the existing resource shell.

New drill intercepts from within the 2020 Initial Inferred Mineral Resource shell support geological and grade continuity

Additional high-grade South East Crescent intercepts from within the December 2020 Initial Mineral Resource.

These results support the delivery of an Indicated Mineral Resource estimate in the South East Crescent Zone.

2021 Growth Drilling is progressing into FY22

North West Crescent and Northern Breccia: Growth Drilling continues to focus on the North West Crescent and Northern Breccia zone and aimed at providing support for the potential expansion of the existing Inferred Mineral Resource Estimate.

Eastern Breccia: Drill testing and interpretation of the geological and mineralisation controls of the Eastern Breccia Zone is ongoing.

South East Crescent and Breccia: Targeting potential resource definition of extensions below the existing resource shell and lateral extensions adjacent to the existing high-grade resource shell.

New Targets: New targets outside of the immediate vicinity of the Havieron deposit, but within the Havieron Joint Venture area, have been identified with the potential to conduct drill testing of these targets in the future.

Early Works Underway: As previously announced, surface earthworks are largely complete, with the box cut complete and decline development commenced:

Excavation of the box cut commenced on 8 February 2021.

Commencement of the underground decline access, from the base of the box cut, was announced on the 12 May 2021.

The Joint Venture is progressing the necessary approvals and permits for the development of an operating underground mine (subject to a successful exploration program, feasibility studies, market and operating conditions, board approvals and a positive decision to mine).

Work continues to investigate the potential to achieve commercial production at Havieron within three years of the commencement of the decline.

Canaccord initiated coverage yesterday with a price target of 25p, calling Greatland ‘unique amongst London-listed gold juniors’:

“Compared to London-listed junior gold mining peers, Greatland Gold stands out to us as a differentiated player with a significant stake in what we believe will become a large scale, top-tier asset, with a tier 1 partner (Newcrest Mining) driving development, in a tier 1 jurisdiction (Western Australia).”

“We believe that Greatland’s flagship Havieron Project could become a 400-700kozpa producer, with a mine life of >20 years, developed at a low capex cost, as a result of taking advantage of Newcrest’s existing processing infrastructure located nearby.”

Shaun Day, Chief Executive Officer of the AIM-listed company, commented: “These latest drilling results add further extensions to the high-grade mineralisation at Havieron while evolving the deposit beyond the existing resource shell. With each new set of excellent intercepts, we demonstrably advance the potential size and value of the gold-copper orebody at Havieron.”

“Development on site continues at pace with surface earthworks nearing completion and the underground decline underway. As the Joint Venture progresses, ongoing exploration continues to enhance the potential scale of the gold-copper mineralised system at Havieron.”

The past decade has witnessed significant shifts in the way that fitness is consumed in the UK & across the globe. The events of 2020 accelerated the trend for digital fitness, creating a range of new market opportunities for challenger brand FLY LDN.

The fitness industry has changed

Since 2010, the UK fitness industry has seen a bifurcation. The growth of the economy gym sector (operators such as Pure Gym, Anytime Fitness) and the premium boutique sector caused a significant squeeze in the mid-market (operators such as Virgin Active, Fitness First).

Boutiques focus on providing a class-based luxury consumer experience in design-led studios with highly specialised class concepts and a high quality of instruction. The boutique price point reflect this, with consumers typically paying between £15 and £23 per class. Monthly memberships are declining with payment per class becoming the accepted pricing model, allowing consumers the flexibility to fit their exercise regime around different product offerings.

London (following the trend in New York, LA and other major US cities) has been the epicentre of the development of the UK boutique market, with more recent growing penetration across the UK. However, the boutique sector currently represents only 4% of the total UK fitness market (compared with 42% in the US) demonstrating significant growth potential for brands domestically and in even more nascent international markets.

HIIT (high intensity interval training) brands were the earliest movers in the boutique space (Psycle, 1Rebel, Barry’s Bootcamp) and established multi-site chains. In 2017, FLY LDN identified low impact training as the next growth sector in the UK fitness market and saw an opportunity to be the first brand to create a low impact boutique experience around yoga, pilates, barre and low impact strength training.

Low impact exercise, meditation and mindfulness are continuing to make the transition into the mainstream – demonstrated by retail brands which are quicker to produce products in response to market trends and demand (e.g. Nike’s yoga collection and the dominance of yoga-inspired brand, Lululemon).

As the first brand to create a low impact boutique experience, FLY has since built and developed significant platforms tracking the trend towards sustainable training, mindful movement, and body positivity.

FLY seized the opportunity to distinguish itself from high intensity and omnivorous fitness brands by building a clear brand identity based on this kinder, more mindful approach to fitness. The brand is focussed on promoting body positivity, selfcare and sustainable fitness as aspirational.

Since launch, FLY has picked up a slew of awards including ClassPass Instructor of the Year, Men’s Health Studio of the Year, and various awards at the Tatler Gym Awards 2018 and 2019.

FLY LDN is now uniquely placed to amplify its strong following and brand identity online and emerge as a leader in this market segment in person and online.

2020

2020 witnessed an explosion in the digital fitness market. The digital fitness market had been growing organically but COVID and the resulting national lockdowns caused significant disruption in the UK fitness industry, providing a challenge and an opportunity to fitness brands. Those with the strongest brand identity, authenticity and customer engagement grew their franchises during 2020.FLY LDN’s social media following increased 400% in 2020.

This presented an even greater opportunity for UK based fitness brands to participate in this $59bn global industry. As with in person fitness, this new growth market has focussed on price, quality and brand appeal.

FLY LDN seized this unprecedented market opportunity to grow the brand profile by launching FLY LDN Online, offering our premium product online to the mass market at an affordable price point.

Almost immediately it became clear that low impact exercise translated well at home. While indoor cycling brands (e.g. Peloton) have grown their sales multiple times year on year, expensive and space consuming hardware remain high barriers to entry for consumers. Low impact exercise disciplines such as yoga and pilates require little to no equipment, are quiet to perform, and are space efficient. FLY LDN Online saw rapid and significant growth scaling to 2.5 million minutes watchedand users in more than 80 countriesglobally with a customer trial conversion rate of 87%and a retention rate of 78%.

The future

2020 has cemented the role of online subscriptions in people’s lives. In 2020, UK spending on digital and subscription services was up 39% YoY. Each household now has an average of 7 monthly subscriptions.

Temporary closure of physical sites and shifting working patterns have also changed people’s fitness consumption patterns. This trend is expected to largely continue as companies look to more real estate light (capital efficient) and flexible forms of working.

“FLY is the beneficiary of some of the key trends witnessed in 2020. The business has a small real estate footprint and significant brand traction and engagement.

FLY’s focus on low impact exercise forms has translated exceptionally well to the at home market and the quality of its offering alongside a well-calibrated pricing strategy has resulted in market leading customer conversion and retention.

The growth of FLY LDN Online allows FLY to achieve global brand recognition in a capital efficient manner, providing opportunities for complementary revenue streams including e-commerce and franchising.

This is our first public fundraising round and a unique opportunity for us to supercharge our growth and welcome you to our shareholder community.

To invest in us and find out more, head to our Crowdcube campaign.” – FLY founder, Charlotte Cox

DFS said that its online business grew during the pandemic

DFS will make an underlying pre-tax profit of £105m for the 2021 financial year.

This is despite a number of disruptions, including issues to do with Covid-19 and supply chains.

In an update released today ahead of its full year results, the furniture seller said its orders for Q4 were up by 92% compared to the same period in 2019, pre-lockdown.

During Q3, when most of its showrooms were closed, online order intake rose by 222.5% compared to the year before, with the company bringing in £178.5m.

DFS said that while the closure of showrooms caused its online business to grow, it was also a result of previous investment in its online business.

Over the past financial year, the sofa seller was hit by two lockdowns. In addition, it came up against various pressures on supply chains, including the availability of raw materials and container shipping delays.

The company said it expects much of its profits and revenues from Q4 will be reflected during the 2022 financial year.

Group chief executive Tim Stacey said: “Our aim is to lead sofa retailing in the digital age by building a truly Integrated retail model that allows us to drive market share gains ahead of the competition.”

“Looking ahead, we will continue to invest in key strategic initiatives such as our digital channels, our showrooms and our Sofa Delivery Company final mile logistics capability, along with new investment in UK manufacturing and capacity and expansion into other home categories.”

CMC Markets believes that it can sustain its existing client levels

CMC Markets (LON:CMCX), the London-listed online trading platform, announced on Thursday that its yearly profits more than doubled as high levels of trading occurred as a result of volatility in the markets.

CMC increased its targets on a number of occasions this year as a flurry of retail trading occurred on Wall Street, brining up trading volumes following big swings last year.

Profit before tax for the year ending in March 2021 was recorded at £224m, a significant increase of 127% from the year before.

For 2022, CMC expects its net operating income to surpass £330m.

Over the course of the year, CMC onboard more than 50,000 new customers, as the public’s interest in retail trading soared.

CMC Markets believes that it can sustain its existing client levels, despite a slight dip.

The trading platform raised its shareholder payout, confirming a final dividend of 21.43p per share . Its total dividend now stands at 30.63p per share.

Chief executive Lord Cruddas said: “The performance in 2021, building on a strong performance in 2020, is a result of the Group’s unwavering focus on our strategic initiatives. This has delivered increased diversification of Group revenues and improved CFD client income retention.”

“Active client numbers have also increased substantially, primarily as a result of COVID-19 related volatility and heightened levels of interest in the financial markets, but our strategy allows us to attract and retain these new clients.”

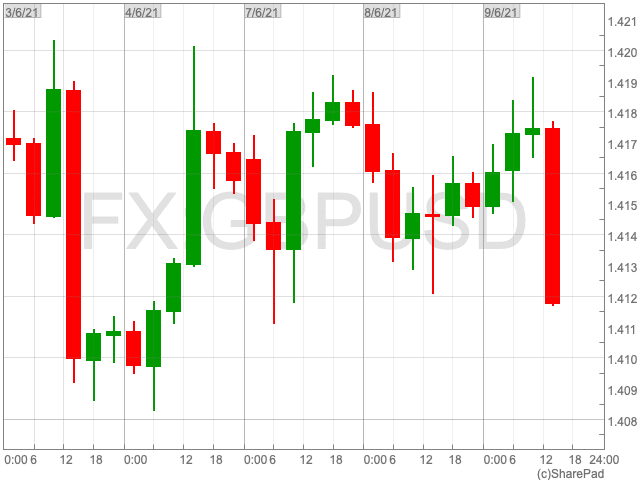

The topic of Brexit made a sudden return on Wednesday in what proved to bad news for the pound.

The UK and EU failed to reach a breakthrough over Northern Ireland Brexit checks, however David Frost, chief negotiator of Task Force Europe, pointed out that talks had not broken down.

“This a new situation, that requires new thinking and new solutions,” said Aodhán Connolly, director of the Northern Ireland Retail Consortium.

“Nevertheless, the lack of progress, and fears over what it would mean if an understanding isn’t reached soon, took a chunk out of sterling as the day progressed,” said Connor Campbell, financial analyst at Spreadex. Against the dollar the pound dipped 0.2%, while against the euro it was down 0.4%, hitting a near-2-week low of €1.1583.

US dollars per GBP

“The pound’s nostalgic decline helped the FTSE 100 cut its own losses from 0.5% to 0.2%, though that wasn’t enough to push it back above 7,100,” Campbell added.

The gains made by the euro, meanwhile, appeared to hurt the DAX, which shed 0.7%, or 115 points, on Wednesday afternoon.

In the States there wasn’t much to report. The Dow Jones was flat at 34,600, likely hesitant to stray from that level until it gets a look at tomorrow’s inflation readings.

“Forecasts would suggest it’ll be good news for the index; the standard CPI figure is set to fall from 0.8% to 0.4%, while the core number is expected to drop from 0.9% to 0.5%. However, similar retreats were expected for April’s readings, and they instead surged to recent highs,” said Campbell.

London’s mid-cap stock index, the FTSE 250, reached an all-time high this month speeding past its previous high of 22,000 in April.

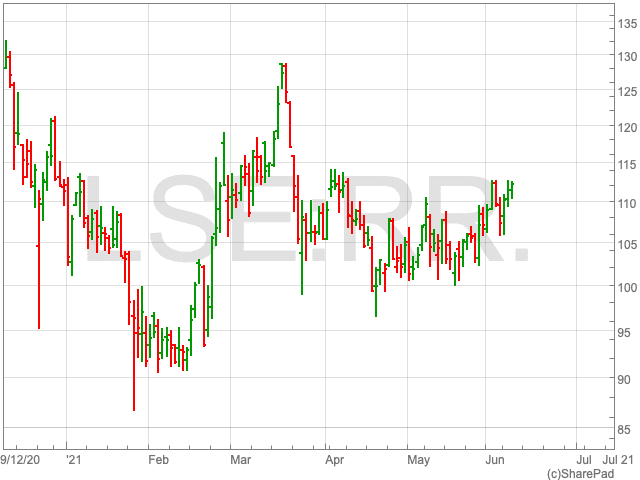

Following a crash in the middle of March, the Rolls-Royce share price looks to have steadied and appears set for a resurgence. Despite coming down from 127.2p in March to to its current level of 112.21p, it is still up by 8.74% since the beginning of the year.

In June the Rolls-Royce share price crept above 110p, having been range bound for much of the preceding months due to uncertainty over the aviation industry. The UK public, as well as the FTSE 100 aviation company, remains hopeful that airports will be opening across the world sooner rather than later.

Aviation Industry and the G7

The ongoing suspension of flights continues to hurt Rolls-Royce, as it earns a significant portion of its revenue from servicing contracts it agrees with airlines that use its engines.

Therefore, any sign that the airline industry is picking up would be good news for the Rolls-Royce share price.

While the government appears to be working on a day-by-day basis, airline executives are continuing to apply pressure on governments to allow them to continue flying. Representatives from major airlines in the UK and US have come together to call on their respective leaders to reopen transatlantic air travel.

While both parties have been fruitlessly arguing for the air corridor for around a year, they will now argue it is more realistic as both countries have high vaccination rates.

“We are going to open up the world,” said Ed Bastian, Delta Air Lines chief executive. “It is going to happen, and this is the corridor to get started.”

Grant Shapps, UK transport secretary, contacted the BritishAmerican Business lobby group in May and stated that restarting travel between the UK and the US was “a priority”.

The G7 meeting later this week could be a turning point for the air travel industry and subsequently the Rolls-Royce share price. However, we have been here before, and investors will know better than anyone that nothing is certain.

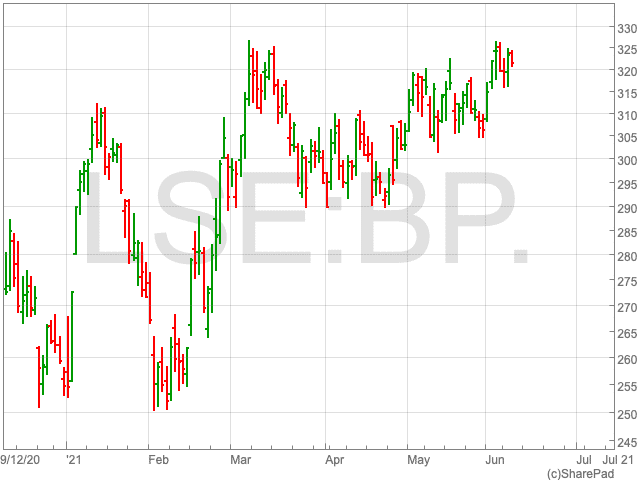

2021 has been a strong year for the BP share price (LON:BP) so far. Since the turn of the year, the BP share price has gained 26.29%. Having dived at the beginning of the pandemic as demand dried up, and again towards the end of 2020 as oil prices dropped, the FTSE 100 oil giant has showed a great deal of resilience. As the world economy has further to go on its path to recovery, and BP continues to plan for the future, now could be an opportune time for investors to buy.

Green Transition

BP, as with a number of its fossil fuel competitors, announced its plans to move towards renewable sources of energy last year. The UK oil company plans to increase its low-carbon investments by 1,000% by 2030. BP also invested in a number of solar projects across the US to the tune of $220m, in addition to renewable assets in Europe.

Additionally, BP is continuing to divest away from oil assets, honouring its commitment to sell up to $15m worth by 2020. By 2025 the oil major could sell $25bn worth of assets.

While BP’s move away from fossil fuels and into renewables appears coherent and is on track. It remains a highly competitive industry, while timing is of the upmost importance.

Barclays

Barclays have high hopes for the BP share price over the coming months. Analysts within the investment banking arm of the UK bank feel that 475p is a realistic price target for BP during 2021. This would bring the oil company back around its levels before the pandemic struck.

Analysts at Barclays feel the oil company’s cash flow is a key strength over its competitors, despite BP easing away from some of its ‘upstream’ activities.

‘Our analysis shows the cash flow generation of the business as having the ability to support a 10% cash return to shareholders in the form of dividends and buybacks in a US$60 per barrel environment, which would be the highest in the sector,” Barclays analysts said in a note.

Of course, this is dependent on the ongoing recovery of the world economy. However, this is something BP can do little to influence. The company appears to be handling its transition well, while its finances are in check and the vaccine roll-out is continuing apace. This, as Barclays argues, bodes well for the outlook of the BP share price.

Private Investors would do well to have a look at the opportunities thrown up within the investment trust sector. Not that many years ago, the sector was the preserve of the traditional stockbroker investing on behalf of their clients. In recent years, those firms have largely been acquired by the vast wealth management chains.

These merged organisations now have assets under management that are so substantial that it is difficult for them to use smaller and medium sized trusts. They simply would not be able to buy enough shares to move the needle within their portfolios.

This has led to a whole raft of these listed funds falling below the radar. Investment trusts are structured in the same way as industrial companies in that their shares are bought and sold on the open stockmarket. Therefore, the price you pay or receive is purely decided by the balance of supply and demand at that moment. Many trusts have become overlooked and unloved, so the market in their shares has often become extraordinarily inefficient.

Therefore, the market price can dramatically vary from the true value of the underlying portfolio. A current example within Miton Global Opportunities plc’s portfolio is private equity specialist EPE Special Opportunities, where the official valuation at the end of March was 448p, yet its shares traded that day at 295p. We have spent the last few years building Miton Global Opportunities plc’s portfolio of exciting opportunities that have been ignored by mainstream investors. For a couple of years, their focus was on a narrow range of very large growth stocks.

This meant that the unloved and overlooked stayed that way. Effective vaccines against Covid are now a reality and this development triggered a broadening of markets. We are now witnessing an influx of investors seeking hidden value amongst trusts. This suggests that it will not be long before the potential of Miton Global Opportunities plc’s portfolio is unlocked.

We look for investment trusts where we are not only confident about the outlook for the portfolio but also where we believe there is a special situation that offers further upside. When we capture a rising asset value and a narrowing discount, this represents a powerful combination. Recent successes include Polar Capital Financial Trust and City Natural Resources.

Polar Capital Financials does what it says on the tin. It specialises in a narrow range of sectors, principally banking, insurance and payment systems. In the aftermath of the Covid crisis there was very little demand for those sectors. Given the poor sentiment, it came as little surprise that the trust’s shares traded at a much wider discount than they have historically.

The market perceived that there were two significant headwinds facing the banking industry. Firstly, it had started to believe that the yield curve would remain flat indefinitely. A flat yield – where there is little difference in yields from the shortest-term bonds to the longest-term – is bad news as borrowing short term and lending long is core to a bank’s profitability – normally the curve steepens the further out in time.

Furthermore, banks made substantial provisions in the expectation that Covid shutdowns would mean that a significant number of customers would not be able to service their debts. Monetary and fiscal stimulus have been thrown at the financial system on a heroic scale, on a par with WW2. This has been a factor behind longer term interest rates increasing and also the buoyant economy has meant that far fewer bank customers have found themselves in difficulty and therefore a significant proportion of the provisions would no longer be needed. The market’s fears were never realised and financials have proved to be a post vaccine rally winner. Despite the positive newsflow, Polar Capital Financial’s discount traded at its widest in late August. Today the shares are trading at a premium having risen nearly 60% since the August low to 14 May 2021, benefitting from the powerful combination of a rising nav and narrowing discount.

Another specialist fund which has come back into favour is CQS Natural Resources, which has bounced 277% from Covid lows on 23 March 2020 to 18 May 2021 on a total return basis. The shares trade close to par to their value at the moment but it has frequently been possible to pick up stock at discounts comfortably wider than 20% in recent years. The trust specialises in small mining companies which were hard hit during the Covid sell off. The sector has bounced sharply with the global economy. Given how long it takes to develop a mine and the lack of capital expenditure in recent years, a number of stocks will benefit from commodity shortages. The “electrification” of our world means that this will be particularly true for metals such as copper, tin and silver.

Being a closed-ended fund itself, we believe that Miton Global Opportunities plc is well positioned to exploit pricing anomalies in this sector. It is protected from daily inflows and outflows, which allows greater conviction. We know that we will not be forced to sell holdings cheaply on a bad day in order to finance a redemption. Therefore, larger positions can be taken with the knowledge that the shares will be held until it is the right time to sell.

The largest holdings in Miton Global Opportunities plc’s portfolio trade at an average discount of a little over 20%. In other words, we are buying these assets at 80% of their latest open market valuation. Our strategy is to focus on situations where we believe the catalyst exists to trigger a narrowing of the discount. There is no point in owning trusts simply because they trade on a wide discount.

We have the luxury of spending our days researching the whole spectrum of investment trusts. Our underlying trusts include everything from shipping leases to residential property in Berlin. Searching for these investment trusts can also be somewhat of a time bandit for the self-directed investor, however Miton Global Opportunities plc provides a one-stop shop access to an area of the market where assets are trading at far below their intrinsic worth.

Source: Morningstar, as at 31.03.2021.

The performance information presented in this document relates to the past. Past performance is not a reliable indicator of future returns.

Diversification chart

Nick Greenwood

Fund Manager

Charlotte Cuthbertson

Assistant Fund Manager

Miton Global Opportunities plc

ENDS

Notes to Editors:

This article has been prepared in response to a request from UK Investor Magazine to be used by the journalist.

Whilst every effort has been made to ensure the accuracy of the information contained within this document, we regret that we cannot accept responsibility for any omissions or errors. The information given and opinions expressed are subject to change and should not be interpreted as investment advice. Reference to any particular stock or investment does not constitute a recommendation to buy or sell the stock / investment.

All data is sourced to Premier Miton unless otherwise stated. Persons who do not have professional experience in matters relating to investments should not rely on the content of this document.

A free, English language copy of the trust’s full Prospectus, the Key Information Document and Pre-investment Disclosure Document are available on the Premier Miton website, or you can request copies by calling us on 01483 306090.

Financial Promotion issued by Premier Miton Investors. Premier Portfolio Managers Limited is registered in England no. 01235867. Premier Fund Managers Limited is registered in England no. 02274227. Both companies are authorised and regulated by the Financial Conduct Authority and are members of the ‘Premier Miton Investors’ marketing group and subsidiaries of Premier Miton Group plc (registered in England no. 06306664). Registered office: Eastgate Court, High Street, Guildford, Surrey GU1 3DE.

This ruling does not mean a change, but rather an acceleration of our strategy, says Shell CEO

Shell (LON:RDSB), the FTSE 100 oil giant, announced on Wednesday its intention to speed up its reduction in carbon emissions following a ruling in a Dutch court.

Last month, a court in the Hague ordered Shell to reduce its worldwide carbon emissions by 45% by the end of 2030.

Chief executive of Shell Ben Van Beurden said in a LinkedIn post:

“For Shell, this ruling does not mean a change, but rather an acceleration of our strategy,” van Beurden said.

“That is likely to mean taking some bold but measured steps over the coming years,” he added.

Previously this year, Shell put forward one of the more ambitious climate plans. This includes a goal of reducing the carbon intensity of its products by at least 6% by 2023, by 20% by 2030 and by 100% by 2050 from 2016 levels.

“Now we will seek ways to reduce emissions even further in a way that remains purposeful and profitable. That is likely to mean taking some bold but measured steps over the coming years.”

Judge Larisa Alwin said last month that oil giant’s current plan was not firm enough and slo that the company was obligated to take further action to avoid violating human rights.

The landmark ruling aimed at bringing the FTSE 100 company in line with the Paris Agreement, was the first of its kind in history.

“The court orders Royal Dutch Shell … to reduce its CO2 output and those of its suppliers and buyers by the end of 2030 by a net of 45% based on 2019 levels,” the court said. “Royal Dutch Shell has to implement this decision at once.”

Shell, the ninth biggest polluter in the world from 1988-2015, was given the right to appeal the judgement.

Half an hour before lunchtime the Shell share price is down by 0.25% to 1,380.40p.