{kind=link}

Dumping Frame, Infrastructure Reality: While the market sees Chinese EV makers as dumping excess capacity overseas, they are actually making strategic investments in Europe. BYD is building a 3,000-station flash charging network to accelerate EV adoption, while Chery, SAIC, and others are investing in European factories.

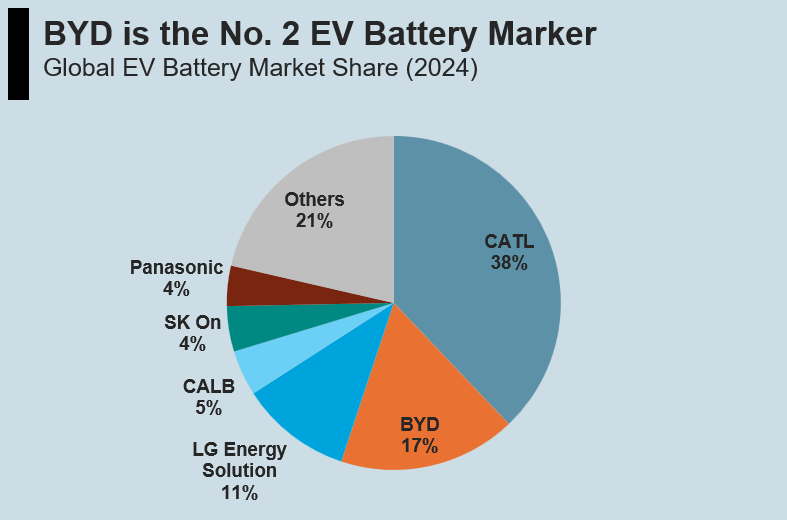

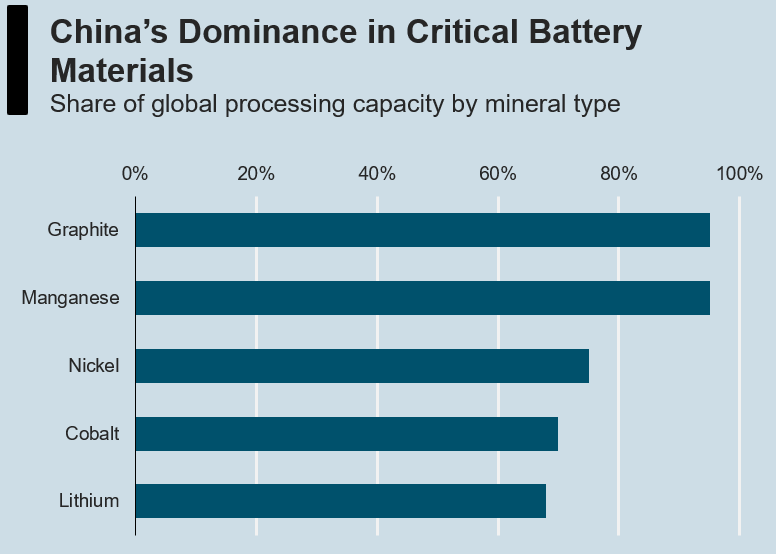

BYD’s Battery Advantage: BYD not only produces vehicles — it is also the second largest EV battery maker globally, backed by China’s dominance over battery mineral processing: over 90% of graphite and manganese, 70% of cobalt and lithium, and 75% of nickel.

Infrastructure Beats Tariffs: The EU’s tariff and MIP regime targets finished vehicle imports. China’s EV infrastructure strategy turns trade policy into a sideshow.

The market frames Chinese EV expansion in Europe as dumping tactics — excess capacity seeking outlets, containable with tariffs.

The reality is that Chinese EV makers are making strategic investments in Europe. BYD is planning to build an extensive fast charging network across Europe, while various brands including Chery and SAIC are investing in factories.

This indicates these brands are implementing a long-term EV strategy instead of short-term dumping of domestic capacity.

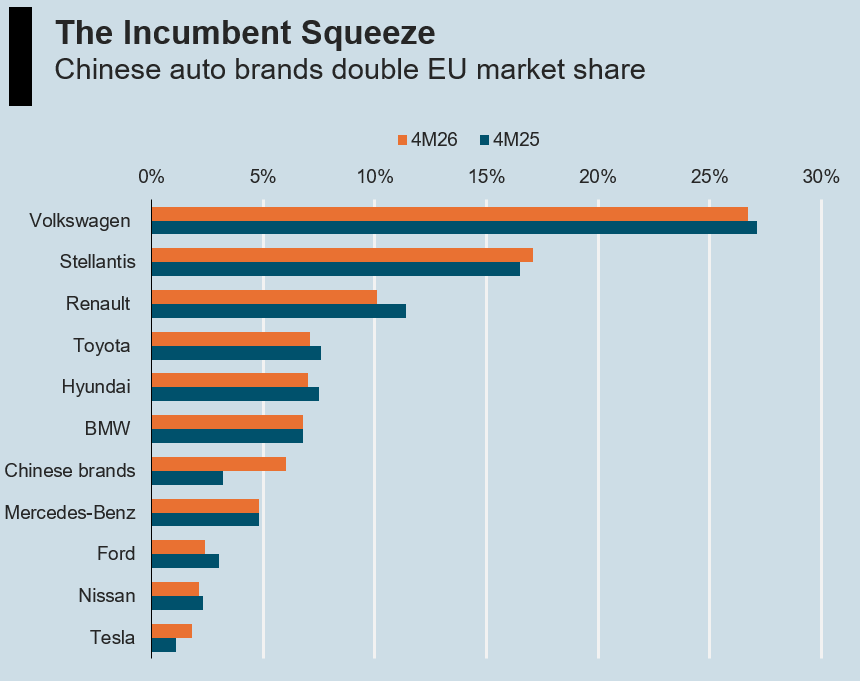

Chinese Auto Brands Gaining Strength in Europe

Chinese auto brands doubled their combined EU market share to 6% in the first four months of 2026, according to ACEA, ahead of Ford, Tesla, Nissan, Mercedes, and approaching BMW.

Among Chinese brands, SAIC/MG led with 2.0% market share, followed by BYD (1.9%), Chery (1.3%), and Leapmotor (0.8%).

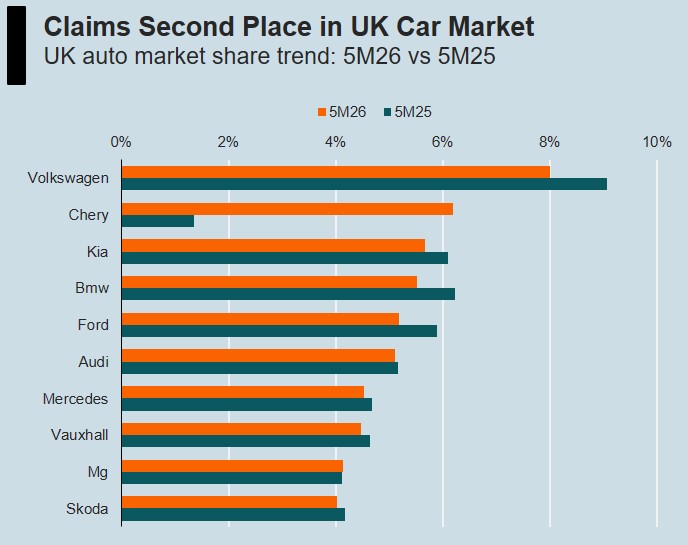

In the UK, the situation is more dramatic. In the first five months of 2026, Chery has become the No. 2 automaker in the UK with 6.2% market share, just behind Volkswagen. Its premium SUV, Jaecoo 7, which offers the look and feel of a Range Rover for less than half the price, has become a major success.

Unlocking the Full EV Potential

Despite strong sales growth, the majority of Chinese EVs sold in Europe today are plug-in hybrids (PHEV), not pure battery electrics (BEV). Mileage anxiety remains the primary reason, hindering the EV adoption curve.

The biggest barrier to EV adoption in Europe is not vehicle price. It is charging infrastructure.

Chinese EV makers are now addressing this directly, not through lobbying or policy, but through infrastructure investment.

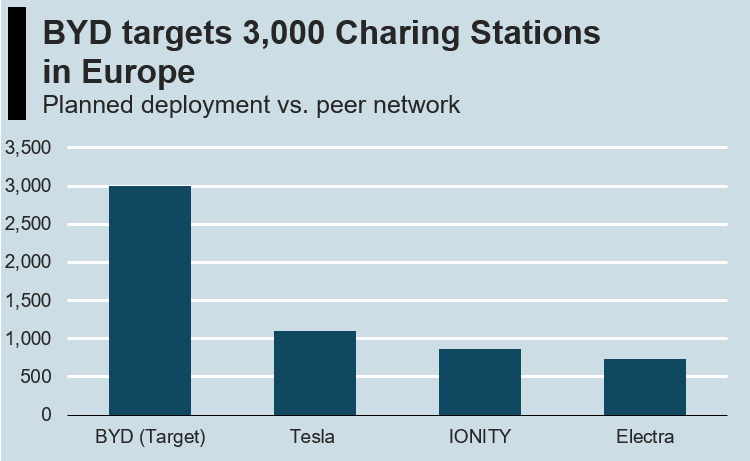

The most ambitious plan belongs to BYD.

BYD plans to build 3,000 flash charger stations across Europe. Each station delivers 3x the power of Tesla’s V4 Superchargers (1,500kW versus 500kW).

In June 2026, its first flash chargers went live in Germany and the UK, which take a compatible vehicle from 10% to 70% in five minutes. BYD reportedly targets pricing 34-38% below IONITY and roughly 17-28% below Tesla’s Supercharger network.

A structural detail: BYD equips each flash charging station with on-site battery storage — not to bypass the grid, but to bypass the grid upgrade. A 1,500kW charger needs peak power most sites cannot supply. The battery trickle-charges at 100-200kW from the existing connection and delivers the burst during a five-minute flash session. No utility upgrade is required.

BYD’s plan represents Europe’s largest EV charging network, beyond the scale of Tesla or IONITY. Existing networks operate at lower power levels, resulting in longer charging times than BYD’s 1,500kW flash chargers.

The Hidden Edge in Battery

The key question is why BYD can build a massive EV charging network at low cost.

The answer lies in China’s hidden dominance in the EV battery supply chain.

BYD not only produces vehicles. It is also the second largest EV battery maker globally.

This is supported by China’s dominance over battery mineral processing — over 90% of graphite and manganese, 70% of cobalt and lithium, and 75% of nickel.

This gives BYD access to essential raw materials for EV batteries at low cost, helping it build a leading position in the global EV battery market.

On the flip side, European battery production costs nearly 50% more than in China, according to the Central European Institute of Asian Studies.

This is illustrated by the bankruptcy of Northvolt, the continent’s flagship battery maker, in 2024.

Local Production Strategy

Chinese EV makers are strategically building new manufacturing capacities overseas instead of dumping domestic capacity.

- BYD’s Hungary plant begins serial production with the Dolphin Surf compact EV. The company is also securing an existing factory for a second European plant, with a third factory under discussion.

- SAIC/MG is investing €200m in a Ferrol, Galicia factory with 120,000-unit capacity, scheduled to commence operation in 2028.

- Chery is producing vehicles through its Barcelona joint venture with Ebro at the former Nissan plant, and is separately in collaboration talks with Nissan for broader cooperation.

- Xpeng and GAC Aion use contract manufacturing through Magna Steyr in Austria.

- Leapmotor has deepened its partnership with Stellantis for dual-plant European production. One plant will produce Leapmotor’s own B10 SUV for the European market; the other will build a new Opel EV on Leapmotor’s platform.

In addition to regulatory hedge, local design and production can be better tailored to European consumer preferences, safety standards, and regulatory requirements.

On the supply side, some European car makers are under financial pressure, creating acquisition and partnership opportunities. The Chery-Nissan collaboration talks signal that Chinese makers can access existing European manufacturing capacity, which offers a faster route to local production than greenfield construction.

The Incumbent Challenges

European automakers struggle to replicate BYD’s charging infrastructure due to lack of a battery supply chain.

No European OEM has in-house battery production that matches Chinese cost structures.

They need to coordinate across separate suppliers for cells (CATL, LG, Samsung), charger hardware (ABB, Alpitronic, Siemens), and network operation (IONITY, or their own fragmented efforts), adding business friction.

The IONITY consortium (BMW, Ford, Hyundai, Mercedes-Benz, and Volkswagen) illustrates the problem. Five OEMs with different strategies funding a shared charging network cannot match the decision velocity of a single vertically integrated operator. BYD can decide to build 3,000 stations and execute. IONITY must negotiate pricing, vendor selection, and market prioritisation across five headquarters.

The Tesla Benchmark

Tesla wrote the playbook for entering the European EV market. First, build the charging network. Then, build the local factory. Then, sell the vehicles at scale.

Tesla’s first European Superchargers went live in Norway in 2013. Gigafactory Berlin began production in 2022 — nine years later. The strategy was infrastructure first, then production once scale was reached.

BYD is following the same sequence but compressing the timeline. First flash chargers went live in June 2026, and Hungary factory production starts the same year.

BYD has two structural advantages Tesla never had. First, Tesla buys battery cells from CATL and Panasonic. BYD manufactures its own cells — the second largest EV battery maker globally. Second, Tesla’s V4 Superchargers deliver 500kW. BYD’s flash chargers deliver 1,500kW — matched to its own Blade Battery 2.0 architecture.

Not All Chinese Makers Are the Same

The market may treat Chinese EV makers as a group but their European strategies differ significantly.

- BYD is the full-stack player. Batteries, vehicles, charger hardware, network operation, factory construction — it controls the entire chain. This makes it the most formidable competitor for European incumbents.

- SAIC/MG and Chery are pure-play EV makers with no vertical integration. They are investing in European manufacturing facilities via greenfield projects as well as partnerships with existing plants.

- Xpeng and GAC Aion are the asset-light players, via manufacturing contracts through Magna Steyr.

- Leapmotor leverages its Stellantis partnership to access two European plants (Zaragoza and Madrid) and an established dealer network. In return, Stellantis gets access to Leapmotor’s EV platform for its own models, including a new Opel EV.

Each strategy has a different risk/reward profile. BYD’s full-stack model is the one European incumbents cannot match structurally. The others are manageable through conventional competition — price, brand, and dealer networks.

This article is a “periodical publication” for information only and is not investment advice or a solicitation to buy or sell securities. This article does not constitute a “personal recommendation” or “investment advice” under UK FCA regulations. Investing in equities involves significant risk. The author holds NO position in the securities mentioned. There is no warranty as to completeness or correctness. Please do your own due diligence or consult a licensed financial adviser. Please read the Full Disclaimer before acting on any information. Images created with the assistance of AI.

Article provided by Asia Pulse.