{kind=link}

Managers of MIGO Opportunities Trust, Nick Greenwood and Charlotte Cuthbertson presented the MIGO Opportunities Trust at the UK Investor Magazine Investment Trust Conference in early May.

MIGO is a ‘trust of trusts’ investing in Investment Trusts they feel are unfairly discounted to the NAV. During the presentation, Charlotte and Nick discuss the trust’s investment strategy and how it selects trusts.

According to Bloomberg on 31 March 2022, there are 428 London listed funds with an aggregate market value of £199bn. Out of the 428 funds, 267 have a market cap of less than £400m. This is the universe of trusts available to MIGO’s portfolio.

Overview of MIGO

MIGO looks for investment trusts trading at a discount with the aim of their discount to NAV reducing over time.

The close-ended trust aims for diversification to achieve maximum global exposure and invests in trusts of mixed asset classes such as equity, private equity, commodities and property.

Greenwood said that the trust thrived in the volatile markets over the last couple of years, when compared to 2019 when tech stocks were high in demand.

MIGO has a total net asset of £95.2m and a NAV of 362.55p with a discount of 4.98% as of 31 March 2022.

MIGO Holdings

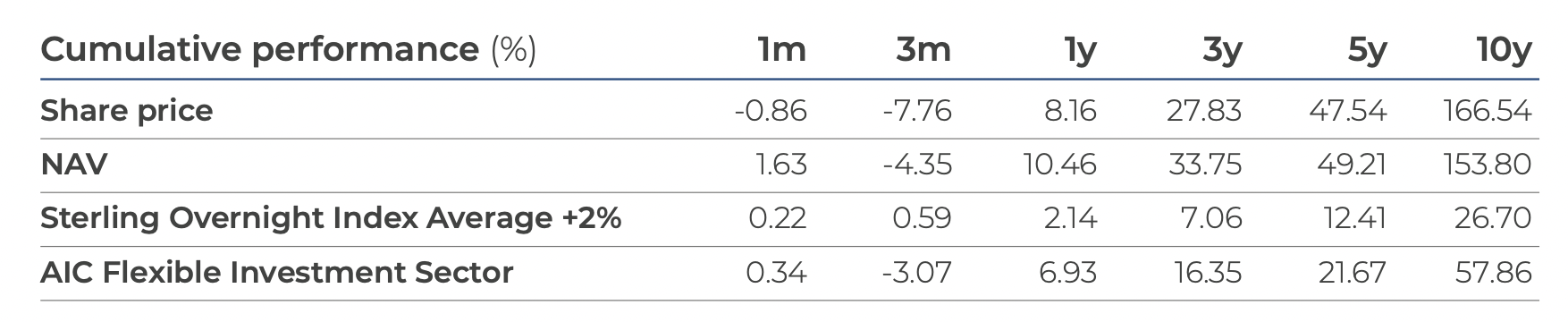

Over the last 1,3, and 5 years, the trust has outperformed both the benchmark and the sector based on NAV and Share Price.

MIGO has many holdings in equity trusts, however, the portfolio is deeply diversified with investments in sectors such as forestry, shipping, India, and Berlin residential.

Trust Returns

MIGO Opportunities Trust’s top holdings included the VinaCapital Vietnam Opportunity Fund with a weightage of 5.7% and a discount of -21.6%.

Nick explained that Vietnam became a popular location in 2005 for investments and stated that investors wanted to diversify from China during the Covid era which impacted the manufacturing industry due to coronavirus restrictions.

MIGO holds the Baker Steel Resources Trust with a weight of 5.4% and a discount of -20.3%, along with Dunedin Enterprise having a weight of 5.3% and a discount of -11.4%, followed by Georgia Capital with a weight of 3.3% and discount of -56.3%.

The average discount of the holdings of MIGO Opportunities Trust was -23.7%, across the top 12 holdings.

The trust notes positive contributions to returns from CQS Natural Rescourses Growth and Income, Geiger Counter, Georgia Capital and Yellow Cake.

On the other hand, the trust generated the worst returns from EPE Special Opportunities and Schrodger UK Public Private, both with a return of -0.3%.

MIGO Investment Themes

The MIGO team outlined how they seek out investment themes for the portfolio and target trusts in that sector. For example, MIGO recently sold its exposure in shipping and began investing in biotechnology, which is one of its core themes.

Uranium

Uranium is increasingly being accessed as nuclear power and COP26 highlighted that though wind and solar are important contributors to power generation, nuclear power will have an important role in the expansion of nuclear power.

The COP26 conference highlighted that whilst wind and solar are important contributors to power generation, nuclear power will have to assume an ever-increasing role.

Greenwood said that “nobody is looking for uranium” and after the price languishing at $25 per 250 Pfund U308, Uranium is now trading above $50.

He added this was an opportunity for the trust because if demand for nuclear power spikes in the future, MIGO are well placed to benefit from a scramble to bring Uranium production online as prices jump.

Biotechnology

s Covid emerged, focus on developments in Biotechnology were hindered when medical firms began streamlining their resources to develop a cure for the pandemic.

However, the profits anticipated from the Biotechnology sector are expected to rise again as the focus shifts back to research in Biotechnology after the temporary detour towards Covid projects.

Investment Process

Core to the MIGO investment strategy is the identification of discounted trusts that sit within favourable sectors. There is then an assessment of the trust’s leverage.

In terms of leverage, Charlotte describes assets with leverage as “very risky” and stated that the trust behaves as if it’s “allergic to leverage” and steers clear. Should a trust pass the leverage test, the MIGO team will then look for catalyst to spur investment.

MIGO also seeks out arbitrage opportunities in the case of a trust wind-up.

A good arbitrage opportunity described by Charlotte is where at the end of the trust, the share price is equal to NAV due to a takeover or a windup.

Move to Alternative Investment

Paul Simon, American Economist, said, “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas,” which Nick Greenwood says he agrees with.

This is particular fitting for the alternative instrument trusts MIGO seeks out that do indeed provide exposure to assets such as forestry.

Over the past ten years, new issues have shifted from equity to alternative assets, as the close-ended nature of Investment Trusts are more suited for less liquid asset classes.