Imagine a ride-hailing service that always arrives on time. It is clean, electric, and intelligently optimised.

That’s Odysse: an AI-powered fleet-as-a-service model already transforming urban transport in London. By combining artificial intelligence with an all-electric fleet, Odysse is pioneering a fleet-as-a-service model designed to make urban transport smarter, cleaner, and more reliable.

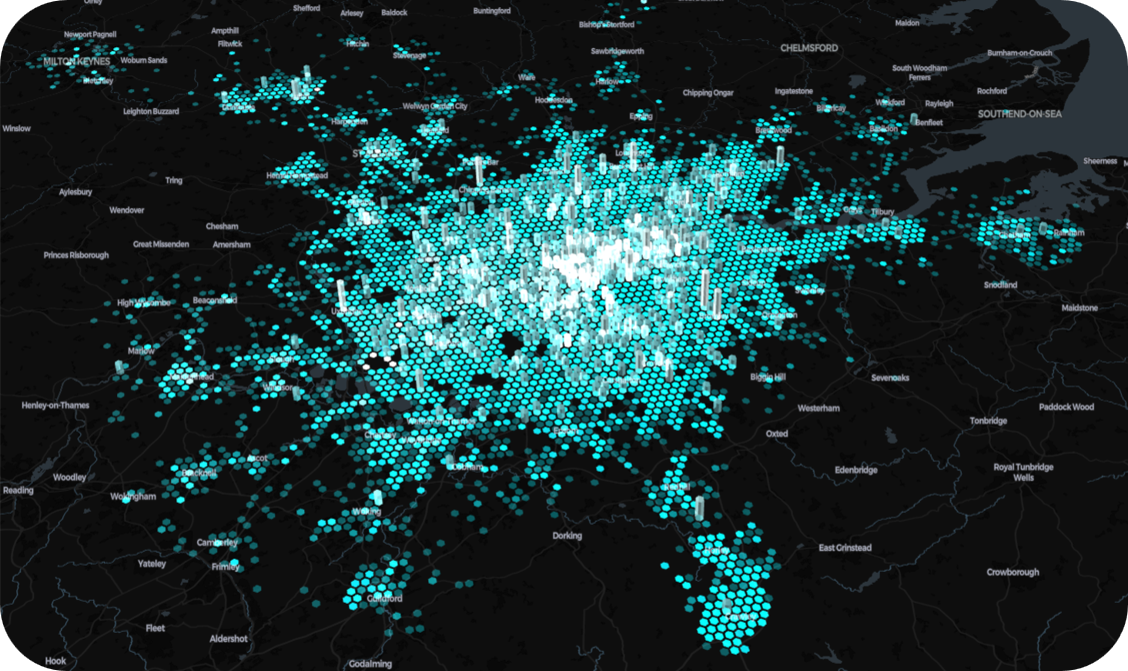

Their proposition is simple but bold: deploy electric vehicles where passenger demand is.

This approach solves a major pain point for ride hailing customers by reducing their wait time and offering a more reliable service. It also reduces idling time, and increases earnings for drivers. For cities, reduction in idling time reduces congestion, and all electric service reduces emissions.

Now, Odysse is inviting investors to join its journey through a live crowdfunding campaign. Explore the campaign here: https://europe.republic.com/odysse

The Challenge Ride-Hailing Faces

London’s streets tell a familiar story: Commuters waiting, gazing at their smart phones, ride-hailing apps buzzing with trip requests and cancellations, and drivers sometimes idling at the wrong place, at the wrong time. The convenience that once defined ride-hailing has, in many ways, eroded. The challenge is systemic as ride hailing struggles to match supply with demand.

Amid these cracks in the system, one start-up is rewriting the rulebook.

Odysse’s Solution

Odysse’s mission is clear: to build the most intelligent, all-electric ride-hailing fleet for urban transport, powered by AI, data analytics, and advanced operations.

Their proprietary Intelligent Demand Response model uses machine learning to analyse rider demand and directs cars to the right place at the right time.

“We’re proving that data-led fleet operations can make ride-hailing profitable, sustainable, and reliable — all at once,” says founder and CEO Anant Prakash.

Intelligent Demand Response: From Data to Deployment

Odysse operates on a continuous feedback loop analysing every pickup and drop-off. It is building systems where AI will detect demand clusters and predict surges across time and geography, allowing fleet deployment to match real-world demand patterns. This analysis will uncover frequently used routes across different hours and days, enabling Odysse to proactively align fleet supply with both high-demand zones and priority travel corridors.

Odysse doesn’t just produce insights, they operationalise insights.

Data analytics is only the first part of what makes Odysse achieve sector leading utilisation.Operationalising insights is the second.

Driver shifts and vehicle deployments are pre-planned, to align with demand across the city. In simple terms, operations aim for vehicles being at the right place, at the right time. Drivers are being equipped to respond in real time, closing the gap between data and action. This bridge between analytics and execution is what sets the company apart from traditional ‘gig divers’ on ride-hailing platforms.

The Market Opportunity

London is one of the world’s largest markets in ride hailing. As the first EV fleet service for Bolt in the UK, Odysse is already tapping into the demand side of that opportunity and demonstrating traction. Looking ahead, Odysse has ambitious plans to scale 100x: from around 30 vehicles today to 3,000 by 2030, with revenues targeted at £100 million annually. With a proven model delivering top-tier utilisation today, Odysse’s next phase is pure scale.

Why Investors are Getting Excited About Odysse

- c£1m annualised revenue (+500% YoY)

- 1m+ electric miles

- 5-year Bolt partnership

- £1.6m raised from VCs and corporates

An investment in Odysse is EIS pre-approved, offering potential tax relief opportunities* for UK investors.

This mix of proven traction, contracted revenue streams, and scalable technology makes Odysse a compelling investment opportunity.

The Next Chapter of Urban Mobility

The first wave of ride-hailing transformed how cities move. The next wave will make it smarter, cleaner, and more reliable. And that’s where Odysse comes in. By combining machine learning-optimised efficiency with an all-electric fleet, Odysse sits at the crossroads of two unstoppable trends: AI and sustainability.

Odysse’s core strength in placing vehicles where they’re needed is an edge that will become even more critical in an autonomous future, where utilisation of self-driving cars will separate early winners from loss leaders in self-driving fleet operations.

Backed by multi-year, high-value partnerships, proven revenues, and an ambitious growth path, Odysse is inviting investors to be part of its next phase. Odysse is already over 90% funded. Momentum is strong and space in the round is limited. Investors can join this next-generation mobility venture today at Republic Europe

* Please note that tax treatment is dependent on individual circumstance and subject to change. Odysse has completed advanced assurance for EIS and has issued compliance certificates for EIS relating to subscriptions for eligible shares (EIS2) within the last 6 months.

Investment risk warning: Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. Take 2 mins to learn more.