US stocks hit refresh highs after Non-Farm Payrolls

US shares hit fresh highs on Friday driven by a jobs report that signalled pressure in the retail sector but expansion in construction.

The US created 148,000 jobs in December, missing estimates of 190,000.

While the number of jobs created missed estimates, average wages came inline with economists prediction at at annualised growth rate of 2.5%.

“A little bit of a disappointment when you only get 2,000 jobs out of the government and get retail at the absolute busiest time of the year losing 20,000 jobs. It just goes to show the true struggle that traditional brick and mortar is having now…Outside of that I actually thought it was a good report.” said JJ Kinahan, of TD Ameritrade.

US stocks took the release as enough reason to break to new highs with the S&P 500 trading above 2731 in early trade.

Shares in the US have had a solid start to the year as investors price in the potential benefits of Trump’s much anticipated tax reforms.

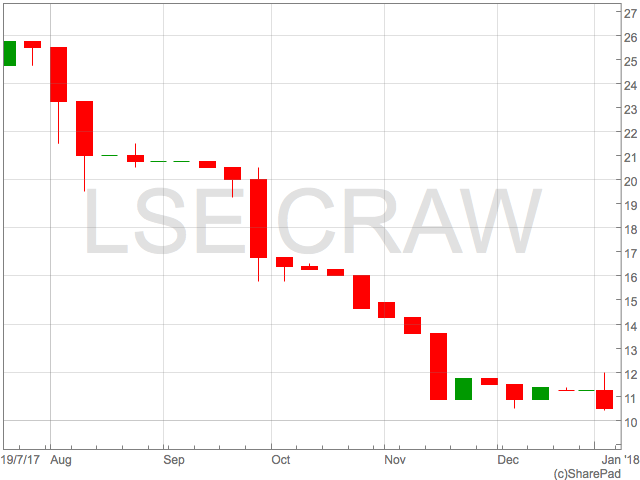

Crawshaw shares slump after slow festive sales

Crawshaw, the UK’s leading value butcher, suffered meaty fall in it’s share price after annoucing its Christmas trading figures.

Shares in the group were down over 7% on Friday after the group revealed like-for-like sales were down 6.1% in the 15 week period to 24th December.

The group blamed lower footfall and weak consumer sentiment for the drop in sales.

CEO, Noel Collett, said of the results:

“On balance, this was a solid core Christmas trading performance against what remains a very tough high street environment. Our biggest ever Christmas week and the record number of meat hampers sold clearly demonstrates the trust our customers place in us for their most important meat spend of the year. This gives us a solid platform to improve trading momentum going into 2018.

CEO, Noel Collett, said of the results:

“On balance, this was a solid core Christmas trading performance against what remains a very tough high street environment. Our biggest ever Christmas week and the record number of meat hampers sold clearly demonstrates the trust our customers place in us for their most important meat spend of the year. This gives us a solid platform to improve trading momentum going into 2018.

CEO, Noel Collett, said of the results:

“On balance, this was a solid core Christmas trading performance against what remains a very tough high street environment. Our biggest ever Christmas week and the record number of meat hampers sold clearly demonstrates the trust our customers place in us for their most important meat spend of the year. This gives us a solid platform to improve trading momentum going into 2018.

CEO, Noel Collett, said of the results:

“On balance, this was a solid core Christmas trading performance against what remains a very tough high street environment. Our biggest ever Christmas week and the record number of meat hampers sold clearly demonstrates the trust our customers place in us for their most important meat spend of the year. This gives us a solid platform to improve trading momentum going into 2018.

“We continue to focus on strengthening Crawshaws’ position as the country’s best value butcher. We are excited by the performance of our factory shops and by the progress of our 2Sisters supply agreement and, while there is much to do, we remain confident that this combination will be transformational for the long-term growth of the company.”

Crawshaw results add to the mixed picture of consumer health during the Christmas period following the release of results from Next and Debenhams.

Next shares jump on positive Christmas update

Shares in UK retailing group Next soared on Wednesday morning following their Christmas trading statement.

Next sales figures for the 54 day period to 24th December revealed the company had successfully offset weaker retail sales with a bumper online sales increase.

Online sales rose 13.6% offsetting a disappointing 6.1% drop on sales in the retail unit.

Investors cheered the results sending Next shares as much as 9% higher in early trade on Wednesday.

Next predicted that profit would slow slightly in the coming year to £705m as operating cost rose at a faster pace than sales which were expected to rise 1%.

The results were not only good news for Next, but the wider retail space; shares in Marks & Spencer and Sainsbury’s rose 1% and 1.2% respectively.

Next predicted that profit would slow slightly in the coming year to £705m as operating cost rose at a faster pace than sales which were expected to rise 1%.

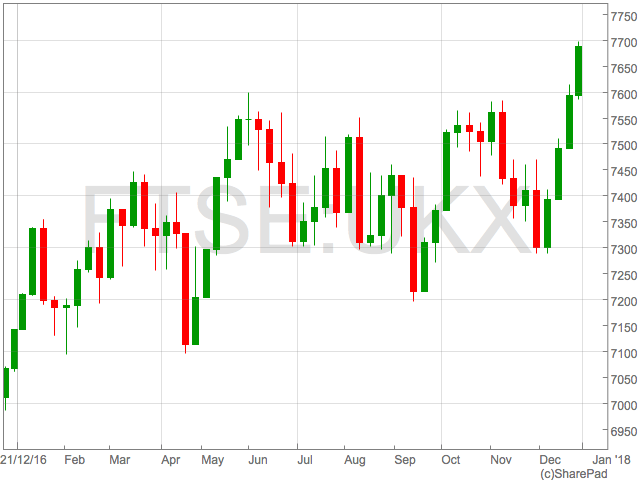

The results were not only good news for Next, but the wider retail space; shares in Marks & Spencer and Sainsbury’s rose 1% and 1.2% respectively. UK shares start 2018 in the red

The FTSE 100 fell on Tuesday, kicking off the new year with losses following a record close on the last day of 2017.

The losses were broad with 44 constituents of the FTSE 100 in negative territory. The biggest losers were Land Securities, Standard Life and Johnson Matthey, down between 1%-1.1%.

The biggest riser was easyJet, up 3% following an announcement from rival IAG saying it was to acquire NIKI assets of air Berlin.

Next was also weaker following a note from Deutsche Bank that called Next and peer group retailers Marks & Spencer’s and Debenhams ‘value traps’.

A value trap is traditionally the name given to a share that appears cheap but could have underlying problems.

The biggest riser was easyJet, up 3% following an announcement from rival IAG saying it was to acquire NIKI assets of air Berlin.

Next was also weaker following a note from Deutsche Bank that called Next and peer group retailers Marks & Spencer’s and Debenhams ‘value traps’.

A value trap is traditionally the name given to a share that appears cheap but could have underlying problems. FTSE 100 closes the year at record high; this year’s winners and losers

The FTSE 100 closed on Friday at 7687 as London-listed stocks added to gains throughout the festive period enjoyed in a so-called ‘Santa’s Rally’.

The FTSE 100 closed 2017 up around 7% in a year that was characterised by extremely low volatility throughout a persistent backdrop of political uncertainty and high equity valuations.

The best performer in the FTSE 100 this year was NMC Healthcare, the middle eastern healthcare company who joined the index in Q$ 2017. The stock enjoyed an impressive 80% gain in 2017 following strong growth in their hospital business based in Abu Dhabi.

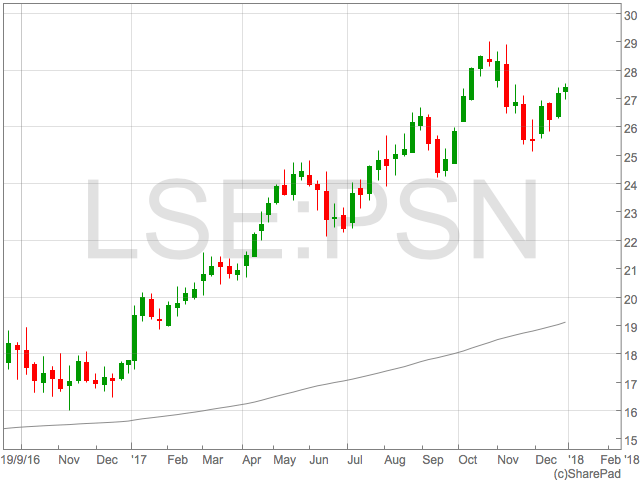

Other string gainers this year included Persimmon and Berkeley Group Holdings who were up 54% and 50% respectively. The housebuilders posted significant profit increases despite fears over a Brexit induced UK economic slowdown.

A major contributor to their success was the governments support for first-time buyers in the form of the Help to Buy Scheme which some have blamed for creating artificially high house prices.

Miners also posted respectable gains this year after commodity prices rallied, ending years of decline. Copper miner Antofagasta was up 49% while Glencore rose 41%.

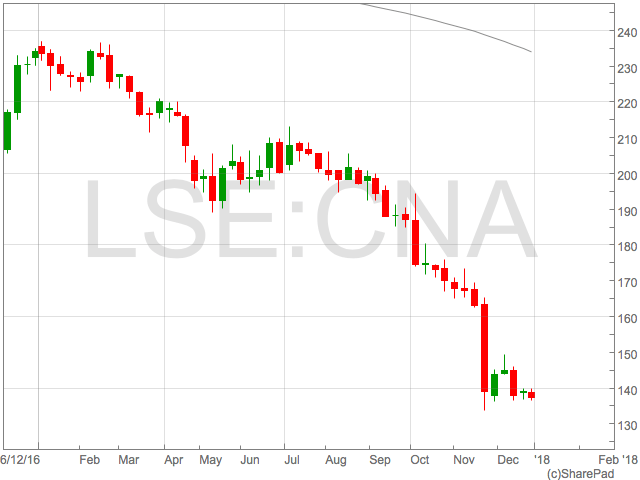

Bottom of the FTSE 100 for 2017 was Centrica, down around 40%. Fears of a price cap for energy suppliers hit the entire sector with National Grid and SSE down between 15%-16%, but news that Centrica were shedding large numbers of customers led to investors dumping shares.

Other causalities of 2017 include WPP and ITV who felt the pain of slowing advertising revenues and failed to realign their businesses with digital content consumption trends.

BT Group shares also suffered after they failed to recover from and Italian accounting scandal and analysts questioned the investment in TV rights as opposed to their core broadband business.

The best performer in the FTSE 100 this year was NMC Healthcare, the middle eastern healthcare company who joined the index in Q$ 2017. The stock enjoyed an impressive 80% gain in 2017 following strong growth in their hospital business based in Abu Dhabi.

Other string gainers this year included Persimmon and Berkeley Group Holdings who were up 54% and 50% respectively. The housebuilders posted significant profit increases despite fears over a Brexit induced UK economic slowdown.

A major contributor to their success was the governments support for first-time buyers in the form of the Help to Buy Scheme which some have blamed for creating artificially high house prices.

The best performer in the FTSE 100 this year was NMC Healthcare, the middle eastern healthcare company who joined the index in Q$ 2017. The stock enjoyed an impressive 80% gain in 2017 following strong growth in their hospital business based in Abu Dhabi.

Other string gainers this year included Persimmon and Berkeley Group Holdings who were up 54% and 50% respectively. The housebuilders posted significant profit increases despite fears over a Brexit induced UK economic slowdown.

A major contributor to their success was the governments support for first-time buyers in the form of the Help to Buy Scheme which some have blamed for creating artificially high house prices.

Miners also posted respectable gains this year after commodity prices rallied, ending years of decline. Copper miner Antofagasta was up 49% while Glencore rose 41%.

Bottom of the FTSE 100 for 2017 was Centrica, down around 40%. Fears of a price cap for energy suppliers hit the entire sector with National Grid and SSE down between 15%-16%, but news that Centrica were shedding large numbers of customers led to investors dumping shares.

Miners also posted respectable gains this year after commodity prices rallied, ending years of decline. Copper miner Antofagasta was up 49% while Glencore rose 41%.

Bottom of the FTSE 100 for 2017 was Centrica, down around 40%. Fears of a price cap for energy suppliers hit the entire sector with National Grid and SSE down between 15%-16%, but news that Centrica were shedding large numbers of customers led to investors dumping shares.

Other causalities of 2017 include WPP and ITV who felt the pain of slowing advertising revenues and failed to realign their businesses with digital content consumption trends.

BT Group shares also suffered after they failed to recover from and Italian accounting scandal and analysts questioned the investment in TV rights as opposed to their core broadband business.

Other causalities of 2017 include WPP and ITV who felt the pain of slowing advertising revenues and failed to realign their businesses with digital content consumption trends.

BT Group shares also suffered after they failed to recover from and Italian accounting scandal and analysts questioned the investment in TV rights as opposed to their core broadband business.

Future of Toys R Us hangs in balance as creditors vote

The future of troubled toy retailer Toys R Us will be decided on Thursday, as creditors prepare to vote on whether to back the proposed rescue plan.

The Pension Protection Fund (PPF) had already said it will vote against the plan, after Toys R Us failed to secure £9 million, but both parties have been in talks throughout the night to secure a deal. The pension scheme currently has a deficit of over £25 million, and an outline of the agreement between the two parties is said to include a ten-year commitment to wiping out the deficit.

If Toys R Us cannot secure the support of the PPF in the vote, the company will fall into administration and around 3,200 staff across its 105 stores. The talks are part of Company Voluntary Arrangement (CVA), a last minute step which could save the company but needs the backing of 75 percent of investors.

Earlier this week, Toys R Us told shoppers that “there will be no disruption for customers shopping through the Christmas and New Year period.”

Government borrowing falls but public debt soars

Government borrowing has fallen to its lowest November level since 2007, according to the latest figures from the Office for National Statistics.

Public borrowing for the year-to-date fell to £48.1 billion, £3.1 billion lower than the 2016 April – November period. A spokesperson for the ONS said:

“This is the best year-to-date borrowing in a decade, but there is still further to go to repair the public finances.

“We continue to build an economy fit for the future by taking a balanced approach, getting debt falling while investing in our vital public services and keeping taxes low.”

The figure puts chancellor Philip Hammond on track to meet the Office for Budget Responsibility’s expectation of £49.9 billion for full-year borrowing to the end of March 2018.

However the same set of figures showed an increase in public sector net debt, which has risen by £72.2 billion to £1.7 trillion. The total figure is equal to 84.6 percent of Britain’s gross domestic product. UK car production on track for first annual fall in 8 years

UK car production fell in November, setting the industry on track for its first annual fall in eight years.

Production at UK factories fell by 4.6 percent in November, putting the total number of cars produced at 161,490. Whilst the number of cars destined for the domestic market fell, the figures were offset by a boost in exports, which saw a 1.3 percent rise.

If the weak figures continue into December, the UK car industry will have suffered its first annual fall since the financial crisis. The figures will come as a blow to Brexiteers, who have relied on the strength of the UK’s car manufacturing industry to support Britain’s exit from the European Union.

Commenting on the data, SMMT chief executive Mike Hawes, said: “Brexit uncertainty, coupled with confusion over diesel taxation and air quality plans, continues to impact domestic demand for new cars.”

IMF downgrades UK economic growth in wake of Brexit

The International Monetary Fund has warned that the UK may lose out in the wake of Brexit, downgrading growth prospects in its latest report.

The IMF now expects growth of 1.6 percent this year, down from its previous forecast of 1.7 percent. Growth is expected to slow further in 2018 to 1.5 percent.

The report highlighted the negative impact of the weak pound on the domestic economy, as well as its effect on UK trade. It said:

“The sharp depreciation of sterling following the referendum pushed up consumer price inflation, squeezing household real income and consumption.

“Business investment growth has been lower than would be expected in the context of strong global growth and high levels of capacity utilisation, owing to heightened uncertainty about economic prospects.”

Christine Lagarde, the IMF’s chief, also said it was clear that the UK was “losing out” from the impact of Brexit.

Post Office to be given extra £370m funding

The Post Office is to be given an extra £370 million by the government, after the postal service announced it had made a profit for the first time in to get 16 years.

The money will be used largely to protect Post Office services in rural areas, as well as to modernise the existing 11,600 Post Offices. The Government has already committed £2 billion to the group since 2010, with £160 million of this round going towards rural branches and £210 million to modernise services.

Business Secretary Greg Clark announced the extra funding on Wednesday, saying the Post Office was “at the heart of communities across the UK, with millions of customers and small businesses relying on their local branch every day to access a wide range of important services”.

He said: “With the network at its most stable in decades, this £370 million of government funding will ensure it can continue to modernise and bring further benefits to customers across the UK.”