Savills profits rise after “resilient” performance during the year

International real estate giant Savills (LON:SVS) reported a 3.5 percent increase in profit on Thursday, after a “highly resilient” in their UK residential business.

Profit at the group £140.5 million, with revenues rising by 11 percent to £1.6 billion. Statutory profit before tax increased by 13 percent to £112.4 million, increasing its total dividend for the year by 4 percent to 30.2 pence per share.

The group saw a particularly strong performance from its investment management business, with assets under management rising 5 per cent to £14.6 billion, as well as its UK residential business.

Jeremy Helsby, group chief executive, said: “Savills has delivered another strong performance in 2017. Revenue and profits grew in each of our global Transaction Advisory, Consultancy and Property Management businesses despite challenging conditions in a number of markets. The strength of our business in key transactional markets across the globe, including a highly resilient performance in our UK residential business, were key to this result.

“Throughout the year we maintained our focus on delivering exceptional service to our clients and continued to build on our global network through complementary acquisitions and new team hires.

“We have made a solid start to 2018 with a pipeline of business carried over from last year in many markets, although this is against the backdrop of heightened market uncertainty, geopolitical risks and rising interest rates. We anticipate a tempering of the strong transaction volumes of recent times in some markets; however, at this early stage in the year our expectations for 2018 remain unchanged.”

Shares in Savills (LON:SVS) are currently trading down 0.15 percent at 974.50 (0831GMT).

Cineworld shares rise on strong 2017 figures

Shares in cinema chain Cineworld (LON:CINE) rose over 2 percent on Thursday morning, after an increase in demand had a positive effect on revenue.

Revenues rose 11.6 percent over 2017 to hit £890.7 million, with admissions growing by 3.5 percent to £103.8 million.

Pre-tax profit also rose 22.7 percent on a statutory basis to £120.5 million, while adjusted pre-tax profits rose by 14.5 percent to £127.5 million.

Anthony Bloom, Chairman of Cineworld called 2017 an “exciting year” for the group – “the most momentous since its formation in 1995”.

“For the financial year ended 31 December 2017, the Group’s operations in the UK and ROW once again posted record results and then in December we announced the proposed acquisition of Regal Entertainment Group for $3.4 billion which has successfully completed on 28 February 2018.”

The group added that it was “confident” that the acquisition would be a success.

Adjusted diluted EPS increased by 12.3 percent to 17.3p and the group declared a final dividend of 15.4p per share.

Shares in Cineworld rose 2.41 percent at market open to 246.00 (0823GMT).

Morrisons reports 17 per cent rise in profits

Morrisons (LON:MRW) reported a 17 per cent rise in profits on Wednesday, reaping the results from a turnaround initiative, in spite of a difficult trading environment.

The UK’s fourth largest supermarket pointed in particular to strong sales of local suppliers’ foods, which has risen 50 percent across the last few years.

Morrisons has agreed deals with more than 200 farmers and UK based suppliers, in a bid to counteract restricted food supplies in light of uncertain political circumstances, climate change and adverse weather conditions.

Overall, the supermarket posted a 5.8 percent increase in total annual sales to £17.3 billion. Sales at established locations, excluding fuel revenues, rose 2.8 percent.

This was driven in part by deals with Amazon (NASDAQ:AMZN) and McColl’s convenience store chains, alongside the expansion of smaller locations with later opening times.

Morrisons said it was pay 4p a share special dividend on top of its 4.43p final dividend, in light of underlying pretax profits growing by 11 percent to £374 million in the year to February.

Andrew Higginson, chairman, commented: “Morrisons is now entering its third consecutive year of growth, which is a credit to the whole team. We will continue to prioritise consistent, meaningful and sustainable growth, which I am confident we are well placed to keep delivering.”

Despite the promising performance, shares fell as much 3.7 percent on Wednesday morning.

Investors remain cautious of sustained growth in light of political uncertainties and a difficult retail environment.

The larger supermarkets such as Tesco (LON:TSCO) and Sainsbury’s (LON:SBRY) are also facing pressure from emerging competitors such as Lidl and Aldi, who continue to grow their market share.

In the past month, various U.K high street restaurant chains and stores have been announcing closures, in light of difficult circumstances and shifts in consumer spending levels and trends.

Notably, both Toys R Us and Maplins fell into administration in recent weeks, with both retailers failing to locate a potential buyer.

Shares in the supermarket are currently trading -4.64 percent as of 14.00PM (GMT).

Hostelworld defends its niche

Online travel agent (OTA) Hostelworld is focused on helping travellers book hostel accommodation. Hostelworld’s saw bookings increase by 6% in 2017 with this driven by a strong performance in the first half of the year.

The backdrop in prior years has been mixed with bookings down 1% in 2016 and up by 1% in 2015. Europe makes up half of Hostelworld’s bookings and in 2016 was impacted by a number of terrorist events.

Travel is still a growth area and hostel accommodation offers a uniquely social travel experience. Modern hostels typically include communal lounges and bars while some even feature outdoor swimming pools.

The modern, social hostel experience: some even have pools

Source: Hostelworld

Another attraction of hostel accommodation is that room sharing makes it relatively cheap. Sector bed capacity increased 3% in the 12 months to 30 June 2017 and a number of large hospitality groups are investing in hostel expansion.

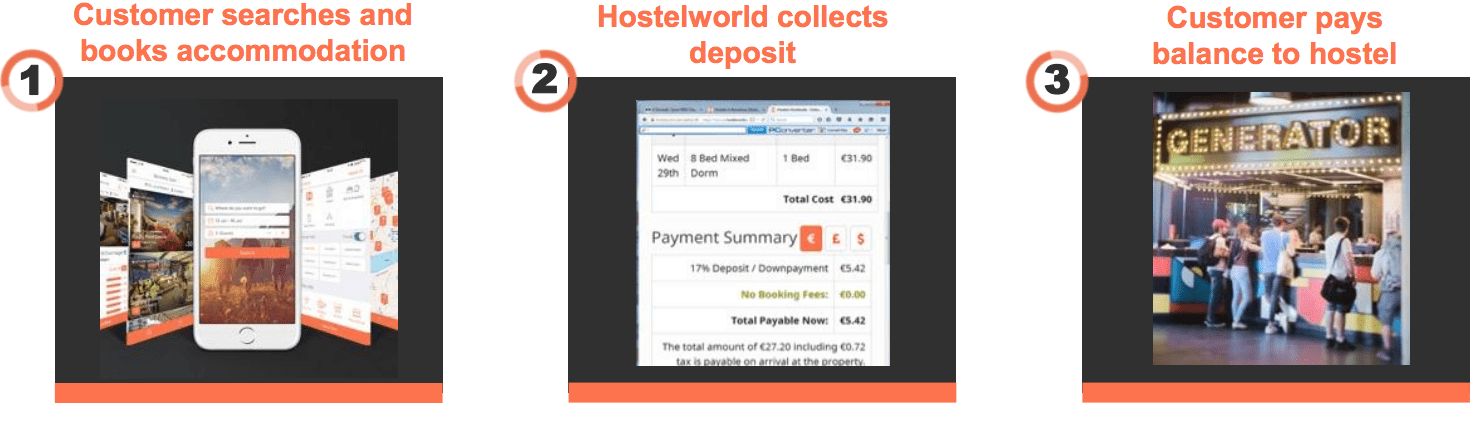

Against this backdrop the future appears to be bright for online travel agent Hostelworld. The company makes hostel booking relatively easy but does charge an additional fee versus booking directly with a hostel.

Hostelworld’s business model: as easy as 1, 2, 3

Source: Hostelworld

Hostelworld is, however, a relative minnow in the online travel agent (OTA) with a market value of circa £400m. The US group Booking Holdings has a market value of £75bn and has a range of heavily marketed brands.

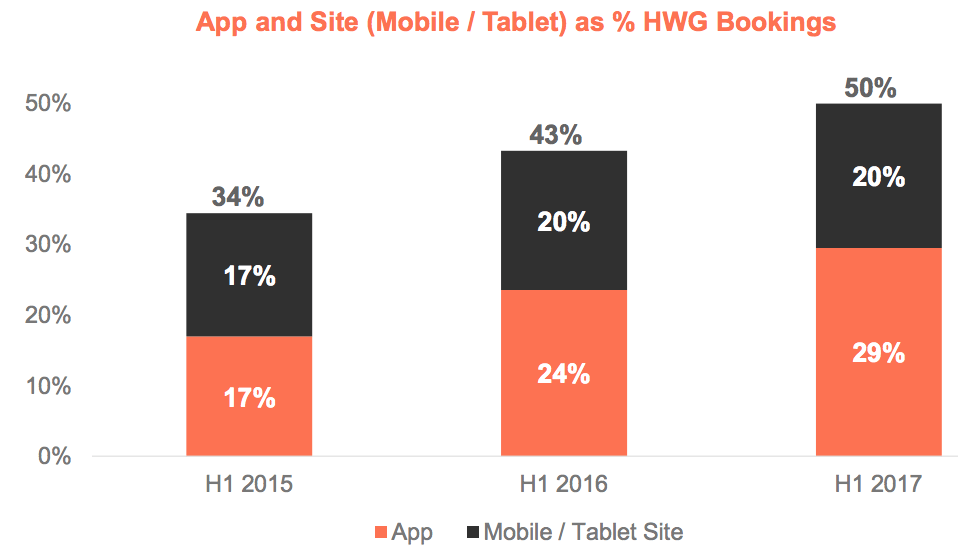

A key issue for Hostelworld investors, therefore, is whether it can successfully defend its niche. New features to improve loyalty include an online Hostel Noticeboard (launched December 2016) and a language translation service.

Hostelworld’s mobile application (app) was used in 29% of bookings in the first half of 2017. This compares to only 17% in the first half of 2015 and suggests that customer loyalty is improving.

Hostelworld’s customers go mobile

Source: Hostelworld

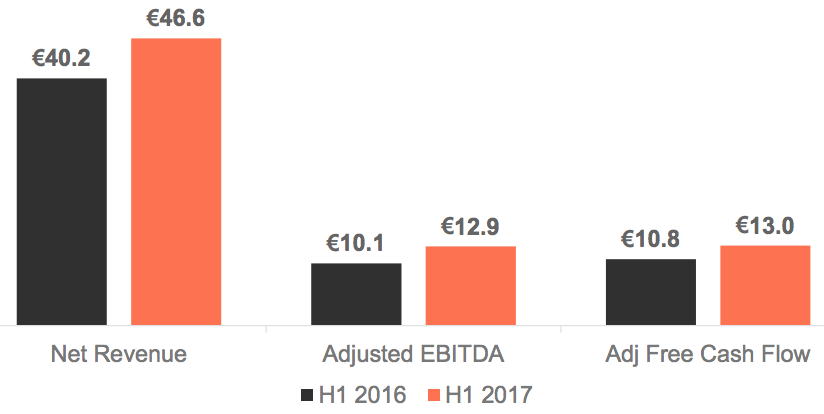

If Hostelworld continues to grow in popularity then profitability should also improve. This is because bookings from paid channels, such as search engines, will decline as more users go directly to Hostelworld.

Marketing investment as a percentage of revenue was 50% in the first half of 2015 but had fallen to 41% in the first half of 2017. This trend has a significant impact on the bottom line with marketing the largest single cost for Hostelworld.

Looking at the numbers and in the first half of 2017 the group generated €46.6m net revenue and adjusted EBITDA came in at €12.9m. This compares to net revenue of €40.2m the first half of 2016 and adjusted EBITDA of €10.1m.

Hostelworld in the first half of fiscal 2017

Source: Hostelworld

Hostelworld will report results for 2017 on 10 April and may announce a special dividend. The forecast dividend yield for 2017 is 3.4% (excluding special dividends) and cash on the balance sheet was €17.7m at mid-2017.

The consensus forecast P/E for 2018 is now 21.7X with share price appreciation having increased the multiple. Investors have brushed aside issues that hit trading in 2016 and the weak momentum seen in the second half of 2017.

Hostelworld’s financial backdrop: growth is expected to continue

Source: SharePad

If Hostelworld can defend its niche then it is well placed to benefit from long-term growth in the travel sector. The increase in mobile application (app) usage suggests that the company has a reasonable chance of seeing off competitors.

Risks include the possibility that a larger rival will develop a branded hostel booking service. Travellers could also increasingly book hostels directly, to save money, or move to alternative booking platforms such as Booking.com.

Disclosure: The writer holds shares in Hostelworld.

Source: Hostelworld

Another attraction of hostel accommodation is that room sharing makes it relatively cheap. Sector bed capacity increased 3% in the 12 months to 30 June 2017 and a number of large hospitality groups are investing in hostel expansion.

Against this backdrop the future appears to be bright for online travel agent Hostelworld. The company makes hostel booking relatively easy but does charge an additional fee versus booking directly with a hostel.

Hostelworld’s business model: as easy as 1, 2, 3

Source: Hostelworld

Hostelworld is, however, a relative minnow in the online travel agent (OTA) with a market value of circa £400m. The US group Booking Holdings has a market value of £75bn and has a range of heavily marketed brands.

A key issue for Hostelworld investors, therefore, is whether it can successfully defend its niche. New features to improve loyalty include an online Hostel Noticeboard (launched December 2016) and a language translation service.

Hostelworld’s mobile application (app) was used in 29% of bookings in the first half of 2017. This compares to only 17% in the first half of 2015 and suggests that customer loyalty is improving.

Hostelworld’s customers go mobile

Source: Hostelworld

If Hostelworld continues to grow in popularity then profitability should also improve. This is because bookings from paid channels, such as search engines, will decline as more users go directly to Hostelworld.

Marketing investment as a percentage of revenue was 50% in the first half of 2015 but had fallen to 41% in the first half of 2017. This trend has a significant impact on the bottom line with marketing the largest single cost for Hostelworld.

Looking at the numbers and in the first half of 2017 the group generated €46.6m net revenue and adjusted EBITDA came in at €12.9m. This compares to net revenue of €40.2m the first half of 2016 and adjusted EBITDA of €10.1m.

Hostelworld in the first half of fiscal 2017

Source: Hostelworld

Hostelworld will report results for 2017 on 10 April and may announce a special dividend. The forecast dividend yield for 2017 is 3.4% (excluding special dividends) and cash on the balance sheet was €17.7m at mid-2017.

The consensus forecast P/E for 2018 is now 21.7X with share price appreciation having increased the multiple. Investors have brushed aside issues that hit trading in 2016 and the weak momentum seen in the second half of 2017.

Hostelworld’s financial backdrop: growth is expected to continue

Source: SharePad

If Hostelworld can defend its niche then it is well placed to benefit from long-term growth in the travel sector. The increase in mobile application (app) usage suggests that the company has a reasonable chance of seeing off competitors.

Risks include the possibility that a larger rival will develop a branded hostel booking service. Travellers could also increasingly book hostels directly, to save money, or move to alternative booking platforms such as Booking.com.

Disclosure: The writer holds shares in Hostelworld.

Source: Hostelworld

Another attraction of hostel accommodation is that room sharing makes it relatively cheap. Sector bed capacity increased 3% in the 12 months to 30 June 2017 and a number of large hospitality groups are investing in hostel expansion.

Against this backdrop the future appears to be bright for online travel agent Hostelworld. The company makes hostel booking relatively easy but does charge an additional fee versus booking directly with a hostel.

Hostelworld’s business model: as easy as 1, 2, 3

Source: Hostelworld

Another attraction of hostel accommodation is that room sharing makes it relatively cheap. Sector bed capacity increased 3% in the 12 months to 30 June 2017 and a number of large hospitality groups are investing in hostel expansion.

Against this backdrop the future appears to be bright for online travel agent Hostelworld. The company makes hostel booking relatively easy but does charge an additional fee versus booking directly with a hostel.

Hostelworld’s business model: as easy as 1, 2, 3

Source: Hostelworld

Hostelworld is, however, a relative minnow in the online travel agent (OTA) with a market value of circa £400m. The US group Booking Holdings has a market value of £75bn and has a range of heavily marketed brands.

A key issue for Hostelworld investors, therefore, is whether it can successfully defend its niche. New features to improve loyalty include an online Hostel Noticeboard (launched December 2016) and a language translation service.

Hostelworld’s mobile application (app) was used in 29% of bookings in the first half of 2017. This compares to only 17% in the first half of 2015 and suggests that customer loyalty is improving.

Hostelworld’s customers go mobile

Source: Hostelworld

Hostelworld is, however, a relative minnow in the online travel agent (OTA) with a market value of circa £400m. The US group Booking Holdings has a market value of £75bn and has a range of heavily marketed brands.

A key issue for Hostelworld investors, therefore, is whether it can successfully defend its niche. New features to improve loyalty include an online Hostel Noticeboard (launched December 2016) and a language translation service.

Hostelworld’s mobile application (app) was used in 29% of bookings in the first half of 2017. This compares to only 17% in the first half of 2015 and suggests that customer loyalty is improving.

Hostelworld’s customers go mobile

Source: Hostelworld

If Hostelworld continues to grow in popularity then profitability should also improve. This is because bookings from paid channels, such as search engines, will decline as more users go directly to Hostelworld.

Marketing investment as a percentage of revenue was 50% in the first half of 2015 but had fallen to 41% in the first half of 2017. This trend has a significant impact on the bottom line with marketing the largest single cost for Hostelworld.

Looking at the numbers and in the first half of 2017 the group generated €46.6m net revenue and adjusted EBITDA came in at €12.9m. This compares to net revenue of €40.2m the first half of 2016 and adjusted EBITDA of €10.1m.

Hostelworld in the first half of fiscal 2017

Source: Hostelworld

If Hostelworld continues to grow in popularity then profitability should also improve. This is because bookings from paid channels, such as search engines, will decline as more users go directly to Hostelworld.

Marketing investment as a percentage of revenue was 50% in the first half of 2015 but had fallen to 41% in the first half of 2017. This trend has a significant impact on the bottom line with marketing the largest single cost for Hostelworld.

Looking at the numbers and in the first half of 2017 the group generated €46.6m net revenue and adjusted EBITDA came in at €12.9m. This compares to net revenue of €40.2m the first half of 2016 and adjusted EBITDA of €10.1m.

Hostelworld in the first half of fiscal 2017

Source: Hostelworld

Hostelworld will report results for 2017 on 10 April and may announce a special dividend. The forecast dividend yield for 2017 is 3.4% (excluding special dividends) and cash on the balance sheet was €17.7m at mid-2017.

The consensus forecast P/E for 2018 is now 21.7X with share price appreciation having increased the multiple. Investors have brushed aside issues that hit trading in 2016 and the weak momentum seen in the second half of 2017.

Hostelworld’s financial backdrop: growth is expected to continue

Source: Hostelworld

Hostelworld will report results for 2017 on 10 April and may announce a special dividend. The forecast dividend yield for 2017 is 3.4% (excluding special dividends) and cash on the balance sheet was €17.7m at mid-2017.

The consensus forecast P/E for 2018 is now 21.7X with share price appreciation having increased the multiple. Investors have brushed aside issues that hit trading in 2016 and the weak momentum seen in the second half of 2017.

Hostelworld’s financial backdrop: growth is expected to continue

Source: SharePad

If Hostelworld can defend its niche then it is well placed to benefit from long-term growth in the travel sector. The increase in mobile application (app) usage suggests that the company has a reasonable chance of seeing off competitors.

Risks include the possibility that a larger rival will develop a branded hostel booking service. Travellers could also increasingly book hostels directly, to save money, or move to alternative booking platforms such as Booking.com.

Disclosure: The writer holds shares in Hostelworld.

Source: SharePad

If Hostelworld can defend its niche then it is well placed to benefit from long-term growth in the travel sector. The increase in mobile application (app) usage suggests that the company has a reasonable chance of seeing off competitors.

Risks include the possibility that a larger rival will develop a branded hostel booking service. Travellers could also increasingly book hostels directly, to save money, or move to alternative booking platforms such as Booking.com.

Disclosure: The writer holds shares in Hostelworld. Get a year’s worth of investment insights at Master Investor Show

The stock market is often portrayed by the media as a casino where folks are just as likely to lose money as to make it. Although it’s true that many a private investor underperforms the markets, for those willing to put in the time and effort to “DYOR” – Do Your Own Research – it is often a different story entirely.

After all, no other asset class offers access to a broader spectrum of investments than the companies listed on a stock market. Easy to buy and sell via any bank or broker, low transaction costs, and strict transparency rules that protect investors. In Britain alone, there are over 2,000 public companies you can invest into at the touch of a button. Look at Europe and the number rises to over 10,000. Globally, there are over 50,000 public companies.

But where can investors find trustworthy information about these companies to aid their investment decisions? For those looking to get up close and personal with their investments, there is no better option than Master Investor Show.

The hands-on approach

Master Investor Show is by far and away the UK’s largest event for private investors. Each year more than 4,000 delegates descend on London’s Business Design Centre, to interact with the CEOs, founders and senior management of around 100 companies and listen to the insights and predictions of some of the best minds in the business. What better way to take control of your financial future than to meet the people you’re entrusting with your hard-earned cash?

Showcasing star performers again and again

Master Investor Show doesn’t issue buy or sell recommendations, but takes great pride in giving visitors early access to investment opportunities that can outperform the broader market.

The show has gained a reputation for repeatedly working with winners:

Learn about alternative asset classes

Master Investor Show introduces visitors to a wide-ranging selection of investments that can complement their portfolios.

Showcasing star performers again and again

Master Investor Show doesn’t issue buy or sell recommendations, but takes great pride in giving visitors early access to investment opportunities that can outperform the broader market.

The show has gained a reputation for repeatedly working with winners:

Showcasing star performers again and again

Master Investor Show doesn’t issue buy or sell recommendations, but takes great pride in giving visitors early access to investment opportunities that can outperform the broader market.

The show has gained a reputation for repeatedly working with winners:

- Blue Star Capital was trading at 14.5p when introduced to the show audience last year. It is now trading at 51p (+252 per cent), and had been as high as What made it gain so much? Master Investor Show caught early wind of Blue Star being a cryptocurrency-related opportunity!

- Critical Elements exhibited at the show in 2016. Its shares were trading at C$0.17 and were recently trading as high as C$1.86, an increase of 994 per cent.

- Avation is presenting at the event for the fifth time. The share traded at 60p in 2013 and is now 241p (+302 per cent). Is the growth opportunity still worth buying into? At the show, visitors get to speak to their CFO and make up their own

- Vox Markets: Investor relations information from a broad range of sources, aggregated into a single platform.

- Selftrade: Execution-only brokerage accounts for 130,000 UK investors.

- Edison: Free access to over 400 equity research reports.

- QuotedData: Research on investment trusts, financial stocks, property companies, REITs and mining shares.

Learn about alternative asset classes

Master Investor Show introduces visitors to a wide-ranging selection of investments that can complement their portfolios.

Learn about alternative asset classes

Master Investor Show introduces visitors to a wide-ranging selection of investments that can complement their portfolios.

- Property lending: LendInvest offers investors the opportunity to earn 5.25% p.a. from their publicly traded bond.

- Gold: EVR Bullion explains why purchasing the investor’s ‘safe haven’on the spot markets represents the best deal.

- High-growth businesses: Show regular SyndicateRoom connects ambitious investors with trailblazing companies.

- The Main Stage forms the epicentre of the event. Presentations bring together an exceptionally broad selection of investable opportunities from around the world. How does a 6,733% return from a Hungarian share sound? The Budapest Stock Exchange will showcase Hungarian investment opportunities that are much cheaper in terms of valuation and now easily accessible to UK private investors. High-calibre speakers also include gas and oil giant Total and Tom Stevenson, Investment Director for Personal Investing at Fidelity International.

- The Rising Stars Stage, co-hosted with investor portal London South East, features companies that are traded on a stock market – i.e. anyone with a brokerage account can easily buy or sell these shares. The line-up of companies presenting in 10-minute slots includes Auxico Resources, Condor Gold plc and Cadence Minerals plc.

- The Auditorium is heavily geared towards educational presentations. Companies presenting include Fidelity International, VectorVest and Avantis Wealth. It will be standing room only for “The Panama Papers”, this year’s explosive talk by Simon Cawkwell (aka Evil Knievil) – Britain’s most feared bear-raider, and the man who made £1 million off the collapse of Northern Rock.

- The Gallery Suite gives presentation slots to companies that are active in alternative asset classes, such as Avation plc, Netwealth Investments and Nova Financial. The Gallery Suite also hosts billionaire Jim Mellon for an exclusive, ticketed talk that sees the Master Investor share his latest investment predictions and left-field ideas.

Zara owner Inditex reports strong results for 2017

Zara owner Inditex (BME:ITX) reported a 41 percent jump in online sales over the course of 2017, after a year of “solid growth”.

It was the first time the group had reported its online sales, which were a key driver of the group’s performance for the year, which saw net profits rise 7 percent to €3.37 billion.

Like-for-like sales, which excludes new store openings, rose 5 percent, with net sales up 9 percent. The group reported revenues of €25.34 billion for the full year.

Pablo Isla, Inditex’s CEO, saifd the group had seen “solid growth” throughout the year, with recent investment in technology and logistics leaving the company well placed for continued progress.

During the year the company spent €1.8 billion, spent largely on integrating the online and physical businesses.

Shares in Inditex, who also own Massimo Dutti, Bershka and Pull & Bear, are currently down 2.27 percent at 23.71 (1017GMT).

Profits double at Marshall Motor Holdings, despite warning on 2018

Car retailer Marshall Motor Holdings said profits doubled over the course of 2017, pleasing investors with a 16 percent dividend increase.

The groups’s strong results were largely due to the sale of its leasing business as well as a hike in revenue, despite recording lower like-for-like new and used car unit sales.

Pre-tax profit rose to £53.1 million, up from £22.2 million the year before, with revenue rising by 19.5 percent to hit £2.27 billion. Underlying pre-tax profit increased by 14.4 percent as gross profit margin expanded by eight basis points to 11.7 percent.

The company declared a dividend for the full year of 6.4p per share, up 16.4 percent on-year.

“Despite the more challenging market backdrop, the board is pleased to announce another record financial performance which was ahead of our previously upgraded expectations,’ chief executive Daksh Gupta said.

“During 2017 we took a number steps, including the strategic disposal of Marshall Leasing, to prepare the group for the future.

“We are now focused exclusively on our motor retail business and with a significantly strengthened balance sheet remain ideally positioned to exploit future opportunities.”

The company warned on the state of the car market going forward, with Gupta drawing on the latest forecast from the Society of Motor Manufacturers and Traders UK which warned of a decline of 5.6 percent in the new vehicle market for 2018.

However, Gupta said trading performance in the current financial year to date is “in line with our expectations and our outlook for the full year remains unchanged.”

Shares in Marshall Motors (LON:MMH) are currently trading up 3.89 percent at 173.50 (0944GMT).

Balfour Beatty shares up as profits jump in 2017

Construction giant Balfour Beatty (LON:BBY) saw shares rise in early trading on Wednesday after reporting a jump in profits in 2017.

The group, who are currently running the London Crossrail project, saw underlying operating profit more than double to £19 million. Pre-tax profit hit £165 million, up from £62 million in 2016.

The group’s order book fell during the year, however, down 8 percent to £11.4 billion as the group made a concerted effort to take on projects aligned with their capabilities.

Its troubled UK construction division moved into profit during the year, reporting a £16 million profit compared to a loss of £65 million the previous year.

Leo Quinn, group Chief Executive, said:

“These results clearly demonstrate that our Build to Last programme is transforming Balfour Beatty. The Group has been repositioned to drive sustainable growth in profits, underpinned by a strong balance sheet. It has the right culture and capabilities to capitalise on the rising tide of infrastructure spend in our chosen markets.

“As a result of Build to Last, and the governance and controls now in place, we remain on track to achieve industry-standard margins in the second half of 2018. In the medium term, we are building a Group capable of delivering market-leading performance.”

Shares in Balfour Beatty (LON:BBY) are currently trading up 2.71 percent at 282.91 (0903GMT).

Petards Group shares down despite record profits

Security and surveillance systems developer Petards Group (LON:PEG) recorded record profits in 2017, with revenue recording an increase for the fourth year in a row to hit £15.6 million.

The group posted a 30 percent rise in annual profit after enjoying “another good year” in 2017. Pre-tax profit rose to £1.21 million, with revenue increased by 2 percent to £15.6 million.

Petards invested heavily in its eyeTrain hardware and software over the course of the year, with gross margins expanded to 38.6 percent, from 36.3 percent.

“The group’s order book at 31 December 2017 was over £18m, of which £12m is expected to be taken to revenue during 2018,” chairman Raschid Abdullah said.

“We are also engaged in on-going discussions for new projects across all areas of our business, many of which our customers have themselves already been awarded.

“This coupled with a strong balance sheet provides the board with confidence for the group’s prospects in 2018 and beyond.”

Shares sunk in early trading, however, and are currently down 2.04 percent at 23.02 (0841GMT).

Prudential profits up 45pc alongside demerger

Wealth management and insurance company Prudential (LON:PRU) announced a 45 percent increase in profit over the course of 2017, alongside the announcement that it would demerge its UK and European investment management businesses.

The company also announced that it would demerge its UK and European investment management business, splitting them in two separately-listed companies. The shareholders would hold interests in both Prudential and the new European business, M&G Prudential.

The group’s results were buoyed by “positive inflows” into its managed fund products and growth in Asia. Pre-tax profit rose to £3.30 billion, up from £2.28 billion a year earlier, with operating profit increasing by 10 percent to £4.70 billion.

“Our clear, consistent strategy, high-quality products and constantly improving capabilities have enabled us to deliver excellent progress across the group, led by double-digit growth in our Asia business,” chief executive Mike Wells said.

“We have also achieved all of our 2017 objectives, which we set in December 2013. This represents the third set of objectives successfully achieved within the last 10 years.”

Prudential shares are currently up 4.66 percent at 1910.50 (0831GMT).