India’s Energy Transition: Capitalising on the Solar Revolution

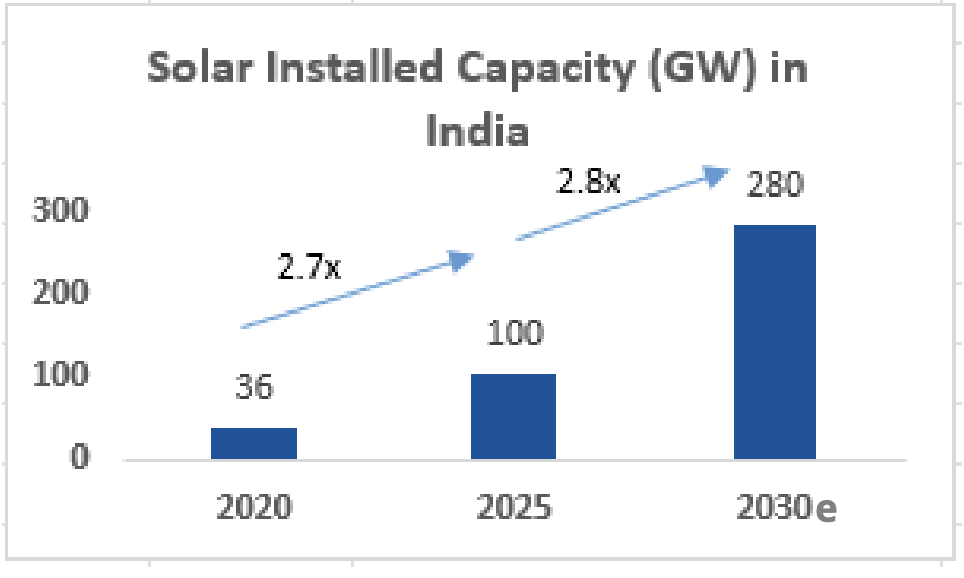

India stands at the cusp of an energy transformation. Once plagued by power shortages, the country now aims to become a global leader in renewable energy, targeting a massive 500 GW of renewable capacity by 2030, with solar energy contributing 280 GW to this ambitious goal. To give some context, UK’s renewable energy capacity stands at 60 GW in 2024. Traditionally a coal-driven energy market, this solar-first approach leverages India’s natural advantage of abundant sunshine and the continuously declining cost of solar power generation. With solar renewable energy cheaper than coalfired power, it presents a win-win positioning for India to simultaneously address climate change concerns while meeting the country’s growing demand for power.

Source: Govt of India – Press Information Bureau MNRE: Year End Review, Dec 20. MNRE: Press Release: 2100603, Feb 25. Grant Thornton Report, Achieving 500 GW of renewable energy capacity by 2030, 2024. e indicates estimate.

The Solar Value Chain in India

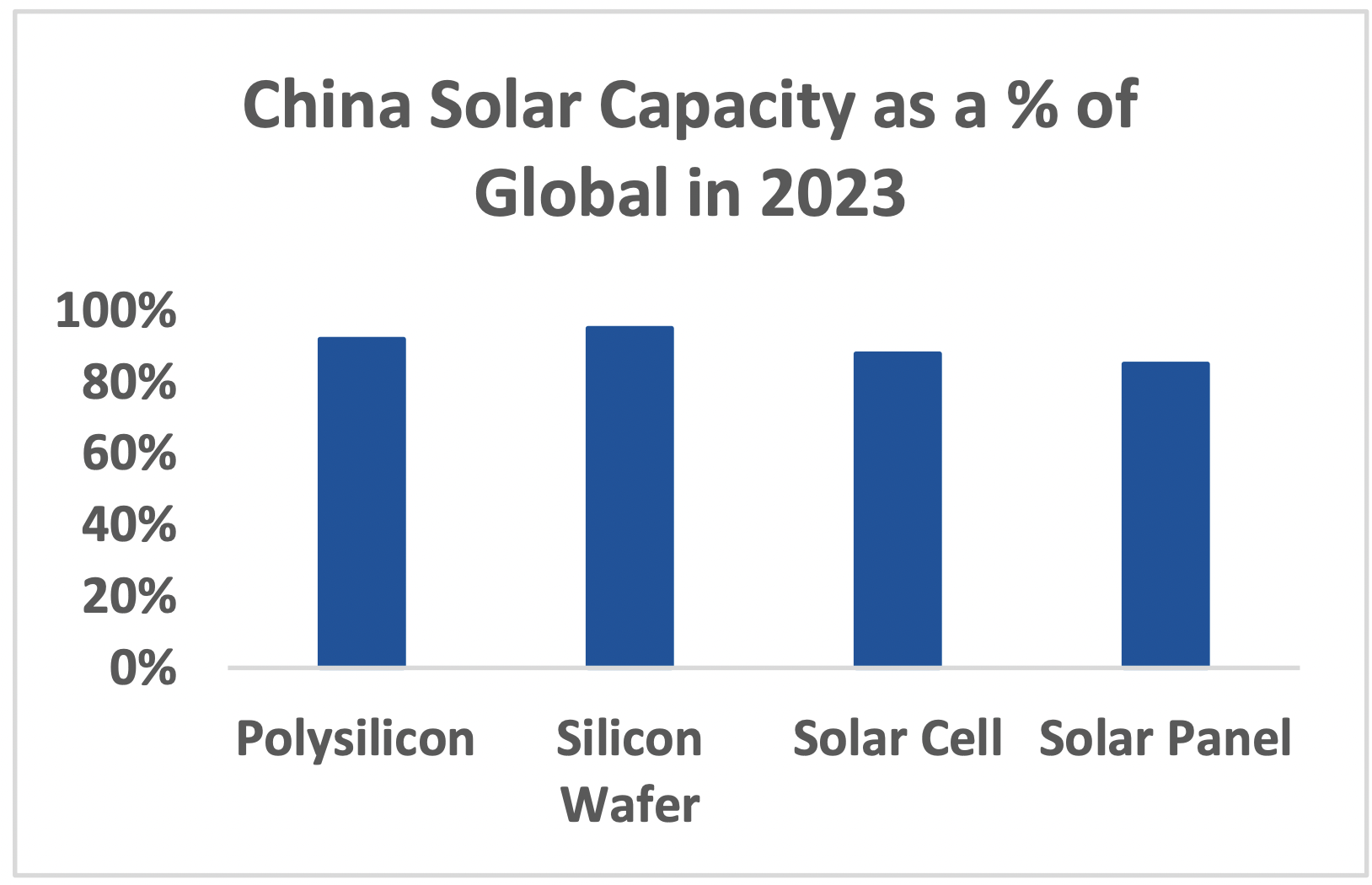

The solar industry value chain consists of multiple stages: polysilicon production, ingot and wafer manufacturing, solar cell production, and finally, panel assembly. Currently, most Indian companies operate only in the final stage of solar panel assembly—the least technologically and capital-intensive part of the manufacturing process. This limited participation in the value chain creates significant vulnerability and dependence on imports, particularly from China, which controls approximately 80% of the global solar supply chain.

This dependence is now changing with backward integration into silicon wafer and solar cell manufacturing becoming the new buzzwords among Indian companies. With companies having achieved scale and profitability in panel manufacturing along with end product prices stabilising, companies no longer see price declines as a risk to their capital investment and are thus investing in capital expenditure. This vertical integration process is accelerating thanks to the government. Not only has the government provided a long-term vision on the size of the opportunity, but it has also actively incentivised the growth of the industry through various initiatives such as domestic content requirements for government projects, substantial import duties (40% on imported solar panels and 25% on imported solar cells), and Production Linked Incentives (PLI) to encourage manufacturing scale-up. New market opportunities have also been created by incentivising solar pump and rooftop solar projects in both rural and urban India.

In an effort to understand Indian companies’ positioning, we visited the plants of two leading companies, Adani Solar and Waaree Energies and were amazed by the sheer scale and size of the state-of-the-art fully automated plants. Their investments demonstrate the seriousness with which Indian players are approaching vertical integration and technological advancement in this sector.

From an investor’s perspective, the Indian market offers diverse investment opportunities across the solar ecosystem with pure-play manufacturers, independent power producers (IPPs) that develop and operate solar plants, as well as engineering,= procurement, and construction (EPC) companies that implement solar projects. This variety allows investors to participate in different segments of the value chain according to their risk appetite and return expectations.

The story doesn’t stop here. India’s vision is to not only be self-reliant but also become an important export hub for renewables in the world for those looking for an alternative source to Chinese solar products. The US is one of the biggest importers of solar cells and panels. With restrictions on China, this opens up a great avenue for India and it is highly profitable too. In FY24, India’s solar products exports to the US were almost $2bn.

So, is it all Sunshine?

Having interacted with a dozen of the listed companies across the ecosystem, our main concern remains China and its dominance across the value chain ranging from polysilicon to cells.

Source: CLSA, CPIA, Companies, Dec 23

Irrational behaviour can have a domino effect. The dependency is not only in the supply chain but also in technological know-how where China is a leader and innovator. As Indian companies backward integrate, the capital intensity also increases, putting at greater risk the investment whenever there is a change in technology, which typically happens every five years. Our other concern stems from domestic competition. The entry barrier in module manufacturing is low, with the capital expenditure for 1GW of solar module manufacturing capacity at approximately $31 million (INR 2.5 bn). This has attracted a lot of companies, including first-time entrepreneurs, to set up capacities. Hence, it is a highly competitive industry. With the entire ecosystem backward integrating, the buyer/seller equation is itself undergoing a change. Supply is catching up with demand quickly. Consolidation seems inevitable.

The key question remains how we participate in this theme of renewables. We have absolutely no doubt that solar renewable energy is the answer to meeting India’s rising power demand of 6-7% per annum. Solar addresses all the fundamental requirements of cost, time, ease of usage, scalability and, of course, ample sunshine. As the industry evolves, we are in a wait-and-watch mode, closely tracking the business models and leaving no stone unturned to identify the eventual winners. There also remains an extended ecosystem of transmission, battery, glass and other inputs riding piggyback on the solar growth story.

Important Information:

The information in this document does not constitute or contain an offer or invitation for the sale or purchase of any shares in the Fund in any jurisdiction, is not intended to form the basis of any investment decision, does not constitute any recommendation by the Fund, its directors, agents or advisers, is unaudited and provided for information purposes only and may include information from third party sources which has not been independently verified. Interests in the Fund have not been and will not be registered under any securities laws of the United States of America or its territories or possessions or areas subject to its jurisdiction, and may not be offered for sale or sold to nationals or residents thereof except pursuant to an exemption from the registration requirements of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and any applicable state laws. While all reasonable care has been taken in the preparation of this document, no warranty is given on the accuracy of the information contained herein, nor is any responsibility or liability accepted for any errors of fact or any opinions expressed

herein. Past performance is not a guide to future performance and investment markets and conditions can change rapidly. Emerging market equities can be more volatile than those of developed markets and equities in general are more volatile than bonds and cash. The value of your investment may go down as well as up and there is no guarantee that you will get back the amount that you invested. Currency movements may also have an adverse effect on the capital value of your investment. Investing in a country specific fund may be less liquid and more volatile than investing in a diversified fund in the developed markets. This Fund should be seen as a long term investment and you should read the London Stock Exchange Listing Prospectus published in December 2017 (the ”Prospectus”) whilst paying particular attention to the risk factors section before making an investment. Please refer to the Prospectus for specific risk factors. Where reference to a specific Class of security is made, it is for illustrative purposes only and should not be regarded as a recommendation to buy or sell that security. This document is issued by RGI Fund Management (referred to as River Global) and views expressed in this document reflect the views of River Global and adviser Saltoro Investment Advisors Pvt Ltd as at the date of publication. This information may not be reproduced, redistributed or copied in whole or in part without the express consent of River Global and River Global Investors LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. River Global Investors LLP is a signatory to the UN Principles of Responsible Investment.

Aquis weekly movers: Incanthera takes direct to consumer approach

Smarter Web Company (LON: SWC) has raised a further £6.83m at 49p/share. It has purchased a further 39.51 Bitcoin for £3.13m. The total holding is 58.71 Bitcoin at a total cost of £4.54m. The additional funds will be used to buy more Bitcoin. The share price jumped 123% to 69p.

Coinsilium Group Ltd (LON: COIN) subsidiary Forza! will be transferred an initial 15 Bitcoin. Coinsilium will announce purchase of Bitcoin by Forza! Institutional investors are interested in investing in Forza! The Coinsilium share price improved 18.9% to 5.35p.

Res Privata NV has raised its stake in WeCap (LON: WCAP) from 11.3% to 13.6%, while Peel Hunt has a higher shareholding of 19%. The share price rose 11.6% to 0.96p.

Newbury Racecourse (LON: NYR) director James Richardson bought 2,878 shares a 625p each and his total shareholding is 5,515 shares. The share price increased 10.6% to 625p.

Global Connectivity (LON: GCON) says that the value of its 2.8% stake in Rural Broadband Services has fallen to £3.9m, which is equivalent to 1.3p/share. The share price is 9.09% higher at 1.2p.

Mendell Heloum (LON: MDH) has an option to acquire M3 Helium, which is continuing work on the Rost 1-26 well recompletion project. The share price improved 9.09% to 3p.

Arbuthnot Banking Group (LON: ARBB) stated at the AGM that trading was in line with expectations in the first four months of the year. Activity is showing signs of picking up. There were loan and lease assts of £2.36bn at the end of April 2025. Deposits rose 3% to £4.26bn. There was an annualised 17% increase in assets under management in the wealth management division. Shore Capital forecasts a dip in full year pre-tax profit from £35.1m to £28.5m. That assumes a further 0.25 of a percentage point cut in interest rates. The share price edged up 2.72% to 942.5p.

FALLERS

Dermatology treatments developer Incanthera (LON: INC) is finalising an agreement with a global direct to consumer and it will launch the Skin + CELL product range in return for royalties on sales. There are 100,000 units in stock ready for sale, and they should be sold by March 2026. This will improve gross margins and provide positive cash flow. The share price dipped 9.09% to 5p.

Valereum (LON: VLRM) is investing $1.35m in DigiShares in four tranches up until July. DigiShares owns a real estate tokenisation platform called RealEstate Exchange. The share price fell 5.37% to 4.85p.

AIM weekly movers: Norman Broadbent rises after share consolidation

Executive search firm Norman Broadbent (LON: NBB) revealed at its AGM that second quarter trading is materially ahead of the same period last year. Recent appointments are helping to enhance growth, and the company is moving into the Middle East market. This should ensure a return to profit this year. The £96,000 CBILs loan has been repaid. Shareholders approved the 35-for-one share consolidation, and it was well-timed considering the good news. The adjusted share price improved 45.3% to 147.5p.

TheWorks.co.uk (LON: WRKS) improved sales and margins in the fourth quarter and guidance has been upgraded. EBITDA for the year to April 2025 has been raised by £1m to £9.5m on flat revenues compared to £6m in the previous year, while the 2025-26 figure is increased to £11m despite the National Insurance headwinds. Net cash has improved to £4m. The share price rebounded 41.4% to 38.6p.

Ironveld (LON: IRON) says sales of DMS grade magnetite from its Bushveld project to offtake partner Sable Platinum should commence shortly. Production ramp-up from stockpiles is underway and the product meet market requirements. Demand is exceeding expectations. Ironveld is set to shift from a development company to fully operational business. The high purity iron, vanadium and titanium project is on the northern limb of the Bushveld Complex in Limpopo, South Africa. The share price increased by two-fifths to 0.0525p.

Chain manufacturer Renold (LON: RNO) has received two bid offers one is 77p/share in cash from Webster Industries and the other is 81p/share in cash from a consortium comprising Buckthorn Partners LLP and One Equity Partners IX, L.P. The share price rose 38.6% to 74p.

FALLERS

Healthcare services provider Totally (LON: TLY) is considering offers for subsidiaries. This is the only practical way to pay off liabilities. However, the proceeds may not be enough to meet all liabilities. The share slumped 79.3% to 0.3p.

There was significant disappointing news from Pantheon Resources (LON: PANR) during the week. First, an initial unstimulated flow test from Megrez-1 in Alaska showed production dominated by water, which was consistent with the previous test in the area. Management will assess the data, but it currently says no recoverable oil resource should be associated with the Lower Prince Creek interval. Second, the flow testing of the Lower Sag 3 reservoir level in the Megrez-1 well was also disappointing. The well is suspended. The focus will switch to Ahpun West, and the Dubhe-1 well will drill this year. Final investment decision on Ahpun West should be in 2027. The share price dipped 41.6% to 24.75p.

Ascent Resources (LON: AST) is acquiring a 49% interest in oil and gas leases in Colorado operated by Locin Oil Corporation and a 10% in oil and gas leases in Utah operated by ARB Energy. US-based geologist David Patterson will take over as chief executive and there will be cost savings. The first purchase costs $2.5m, including shares at 0.5p each and a $1.9m convertible loan note. The second purchase costs $750,000 in shares. The deal includes rights to earn a 50% economic interest in incremental production from these leases. There is an option to acquire a further 23% interest in the leases. A fundraising will generate £1.35m at 0.5p/share with £224,000 used to pay back part of the RiverFort secured loan with $100,000 converted into shares at 0.7245p/share. The share price decreased 38.2% to 0.525p.

Cybersecurity software company Acuity RM (LON: ACRM) raised £421,000 at 1p/share. This will finance sales and marketing, plus further product development. The share price slipped 25.9% to 1.075p.

FTSE 100 sinks as Trump recommends 50% tariff on EU

The FTSE 100 was heading for another positive week as London’s leading index notched up marginal gains in early trade on Friday. That was before Trump posted on social media that he was recommending a 50% tariff on the EU starting 1st June.

The FTSE 100 gains evaporated, and the index sank over 1% after Trump fired his latest shot in the trade war with the rest of the world.

Despite gyrations in global equities caused by concerns around US debt this week, the FTSE 100’s resilience and weighting towards defensive ‘safe-haven’ stocks overcame the worst of the concerns.

However, the threat of such a large tariff on the EU blew this out of the water, and the index was down 1.1% at the time of writing on Friday.

Trump’s social post undid strong gains recorded on Friday morning, with the FTSE 100 trading down 150 points from the highs.

“The FTSE 100 was propelled by AstraZeneca and Rolls-Royce which made the biggest contribution in terms of index points. The more domestic-focused FTSE 250 also nudged ahead, driven by a range of sectors including financials and real estate,” said Russ Mould, investment director at AJ Bell.

Miners were stronger on Friday morning with Anglo American topping the leaderboard as shares gained more than 4%. The sector was mostly negative following Trump’s post.

easyjet was higher as it rebounded from a sell-off yesterday on the back of its half year report. A number of positive broker price target upgrades would of helped attract interest in the stock. Bernstein raised its target to 575p and Barclays now has a 730p target. Goldman Sachs reduced their target slightly to 624p.

Games Workshop was the top faller after the tabletop gaming firm said they didn’t expect the sharp increase in licensing fees to continue into the next year.

“Games Workshop has enjoyed terrific success with licencing assets for the Warhammer 40,000: Space Marine 2 video game,” Russ Mould explained.

“There’s a warning that licencing gains seen over the past 12 months won’t be matched in the new financial year, which explains why the shares have pulled back on the trading update. However, the pipeline looks strong enough to keep most investors on side. In addition to another Space Marine game being developed, it has all the licencing income from a deal with Amazon to look forward to.”

Games Workshop shares were down 4.8% at the time of writing.

AIM movers: Tekcapital increases NAV and Benchmark to leave AIM

Tekcapital (LON: TEK) is the largest riser of the day following publication of 2024 results. NAV has improved from $0.27/share to $0.33/share. The company intends to pay a special dividend when “material levels of capital are monetised” from its portfolio. Autonomous vehicle software developer Guident is set to list on Nasdaq this year. The Tekcapital share price increased by one-eighth to 9p.

Diagnostics company Cambridge Nutritional Sciences (LON: CNSL) says sentencing has been announced for four past health and safety breaches at a former subsidiary. There were mitigating circumstances, and the fine was £35,000. This has already been provided for. The share price rose 9.8% to 2.8p.

Aquaculture company Benchmark (LON: BMK) is asking for shareholder approval to leave AIM and Euronext Growth Oslo. There should be annual savings of £2.4m and there should also be overhead savings of £5.6m following the sale of the genetics business. Benchmark is launching a tender offer at 25p/share. The total amount of cash available through the tender is £56.7m out of the current net cash of £117m. The share price improved 8.18% to 23.8p.

A prospectus has been lodged by Greatland Gold (LON: GGP) for the flotation of its new holding company Greatland Resources on ASX. There are plans to raise £24.2m, while Newmont Corporation is selling 50% of its shareholding. The new company will also be admitted to AIM, and there will be a UK retail offer to raise up to £6.7m. This will close on 17 June. The share price increased 3.79% to 13.7p.

FALLERS

Healthcare services provider Totally (LON: TLY) is considering offers for subsidiaries. This is the only practical way to pay off liabilities. However, the proceeds may not be enough to meet all liabilities. The share price dived 77.2% to 0.325p.

OptiBiotix Health (LON: OPTI) has raised £750,000 at 14p/share. Every two shares come with a warrant to subscribe to one share at 21p. A US institution with experience in investing in weight management businesses has invested £500,000. A new subsidiary has been set up and a warehouse will be leased. There will also be investment in other regions and in social media advertising. The share price fell 12.3% to 16p.

Nostra Terra Oil and Gas (LON: NTOG) says 2024 oil and gas production fell by 27% to 77 barrels/day. Revenues were $2m and the loss was $1.5m. Current production levels are 140 barrels/day. If the Fouke 3 well is successful in the third quarter, then that could generate cash inflows of $200,000 each month. The share price slipped 8.82% 0.0155p.

Seascape Energy Asia (LON: SEA), which was formerly Longboat Energy, increased its 2024 loss from £3.86m to £5.69m following the refocusing on south east Asia. That is before a £10.8m loss on discontinued operations. Net cash was £2.8m at the end of 2024 and since then there has been an inflow of $11m. By the end of the year, there should be a decision on a preferred gas evacuation option for a DEWA cluster development (working interest of 28%) of 12 shallow water discoveries in Malaysia. The share price declined 7.46% to 31p.

Tekcapital shares jump as net assets surge

Tekcapital shares were firmly higher on Friday after the technology investment company announced a dramatic increase in the value of its portfolio and touched on plans to focus its future investment strategy on artificial intelligence.

The group’s investment portfolio valuation increased 49.6% to US$61.5m in 2024, while Net Assets increased 46.3% to US$70.1m.

Tekcapital shares were 14% higher at the time of writing.

“We are excited to provide this 2024 summary report which describes a few of our portfolio company achievements and their contribution to our profitability and growth. In 2024 our net assets reached US $70.1m, an increase of ~46%, over the previous year, an annual record since the Company’s inception. NAV per share was US $0.33,” explained Dr. Clifford Gross, Executive Chairman of Tekcapital.

Gross continued to outline the progress of its portfolio companies – the driving force behind the sharp rerating of the group’s net assets in 2024.

“Our performance reflects strong commercial progress through the completion of two AIM listings (MicroSalt plc & GenIP plc), and as a result, four of our five portfolio companies are now listed,’ Gross said.

“Additionally, we observed significant commercial traction for Innovative Eyewear Inc. as they achieved several new product and go-to-market milestones.

“We were also pleased to note MicroSalt has received new and follow-on B2B orders from a major snack food manufacturer. Further, we believe that Guident Corp’s commercial advancements, coupled with improving performance and market traction in the autonomous vehicle industry, have created a fertile opportunity for Tekcapital to potentially further crystallise its balance sheet in 2025.”

The fertile opportunity mentioned by Gross relates to Guident’s proposed NASDAQ IPO. Tekcapital recently announced that Guident had filed confidentially for its IPO, an increasingly popular way of listing in the US that allows companies to undergo preparations away from the public eye.

Listing portfolio companies has been hugely successful for Tekcapital in terms of asset value creation, with the IPOs of GenIP and MicroSalt crystallising a combined £18.3m of portfolio value in 2024. The value of Tek’s stake in MicroSalt increased substantially after its February 2024 IPO as shares rallied through the year.

The Guident IPO promises another uptick in Tekcapital’s net assets as the autonomous vehicle safety company seeks to list amid a wave of increasing adoption of AVs.

Artificial intelligence investment strategy

While investors will be encouraged by net asset growth in 2024, Tekcapital doesn’t appear to be resting on its laurels and provided a fascinating insight into things to come.

After the successful IPO of AI analytics firm GenIP in 2024, Tekcapital’s outlook hinted at increased investment in AI companies that are transforming workflows across various sectors.

“We intend to aggressively pursue further investments in pre-existing generative artificial intelligence companies (GenAI). Our potential targets are expected to include companies that are focused on the transformative impact of GenAI on business workflows across a number of sectors,” the Tekcapital report read.

In addition to hints at the group’s future investment strategy, Tekcapital reaffirmed its strategy to return cash to shareholders through special dividends, once significant capital growth is achieved.

“Once material levels of capital are monetized from our portfolio companies, we will seek to provide a special dividend. We remain committed to this long-term objective, and our portfolio companies’ progress in 2024 is a good step in that direction,” Tekcapital Executive Chairman Clifford Gross said.

Totally shares plummet after warning of total shareholder value destruction

Troubled Totally has issued a warning to investors that shareholders may recover nothing from their investment as the company desperately attempts to sell off subsidiaries to prevent financial collapse.

The healthcare outsourcing company launched a strategic review three weeks ago to strength its balance sheet through asset sales. After appointing Ernst & Young to advise on the disposals, Totally said it has now received multiple offers for various business units but directors have painted a grim picture of the likely outcomes.

In a brief statement released today, the board made clear that asset disposals represent “the only realistic route” for meeting the group’s obligations.

Unfortunately for investors, the solution to meeting these obligations will leave little or no value in the company’s shares which fell over 30% on Friday. Totally shares have lost 95% of their value since the beginning of the year.

What began as a strategic review has evolved into what appears to be a fire sale of assets, with the company racing to raise cash.

The major issue for Totally is that even if the company successfully completes the disposal programme, the expected proceeds will fall well short of covering all future liabilities.

The group’s trading statement released in early May highlighted they were trading profitably on a monthly basis. This will be of little consequence if these income generating assets are sold to cover debts.

Totally may well be one of the next firms to leave London’s AIM.