Swedish growth investor Verdane has agreed a recommended cash deal to take Augmentum Fintech private at 111p per share, valuing the London-listed fintech fund at approximately £185.7 million.

Augmentum Fintech has several leading UK Fintechs in its portfolio, including Tide, Zopa, and Iwoca, but the vehicle has struggled to narrow the deep discount to the portfolio valuation.

The favoured solution to this, as announced today, is to take it private.

The offer represents a 27% premium to Augmentum’s closing price of 87.4p on 24 February and a 29.6% premium to the three-month weighted average.

Augmentum’s board has unanimously backed the deal, advised by Cavendish, which considers the terms fair and reasonable.

The acquisition is being made through Frontier Bidco, a newly formed vehicle controlled by Verdane through its Freya XII fund.

“Since our IPO in 2018, Augmentum has been at the heart of the UK and European fintech sectors, backing high-growth companies such as Tide, Zopa, Iwoca, Cushon and Interactive Investor,” said William Reeve, Chairman of Augmentum.

“However, we recognise that for our shareholders, this portfolio’s potential has not been reflected in Augmentum’s market valuation.

Over several years, we have faced a persistent and widening discount to Net Asset Value, compounded by low levels of liquidity. This has made it difficult for shareholders to realise the true value of their holdings or for Augmentum to raise the capital necessary to support our ambitions.

To address this, the Augmentum Board has run a process to consider a range of strategic options. We are now recommending the Verdane offer, the best we received. This offer provides an immediate solution: it offers full liquidity at a 27.0% premium to the prevailing share price as at the Latest Practicable Date.

Diageo’s results were never going to make for good reading, and they weren’t. They confirmed that key markets of China the US are still facing pressures, and there are few reasons to be optimistic.

If one were to take the glass half full approach, one could point to reasonably stable sales growth in Europe, LATAM, and Africa, but this was more than offset by weakness in the US and China.

US net sales fell 7.4% and struggles in China culminated in net sales in Asia Pacific sliding 13%.

Overall, net sales were down 4% and operating profit fell 1.2%. The poor performance led to the drinks giant revising its fiscal 2026 sales growth guidance to negative 2-3%.

The reduction in alcohol consumption in the developed world is well documented, but that appears to have done nothing to soften the blow of today’s results, which sent shares down 6% at the time of writing.

Most punishingly for investors, Diageo’s challenging environment has led the group to slash its dividend by more than half.

“Dave Lewis is going to need a stiff drink after presenting his first set of results as the new Diageo boss,” said Dan Coatsworth, head of markets at AJ Bell.

“The business is not doing as well in the once lucrative North American market and China is not lining its pockets with riches either. Most of the key metrics in the results are in negative territory, with sales, operating profit and cash flow all in decline.

“Shareholders have also been delivered the sucker punch of a big cut to the dividend. That might come as a surprise to many investors who thought they would be paid to wait for the business recovery.”

EQTEC PLC has confirmed significant copper and gold potential at its Green Rock Project in Western Australia’s Ashburton Basin, following a comprehensive review of historical exploration data.

The review identified high-grade surface mineralisation with historical grades reaching up to 46.7% copper and 5.31 g/t gold, associated with major structural features and dyke margins across the 31.5 km² exploration licence.

Multiple prospects have been flagged across the site, with geological interpretation pointing to several possible mineralisation styles — yet remarkably, no modern drilling has ever been carried out.

The project sits roughly 160 km west of Paraburdoo and 35 km southwest of the Paulsens Gold Mine, placing it within a proven mineral district with established infrastructure access.

“Our detailed review of the historic data has reinforced both the quality of historic work, and the high tenor of copper and gold mineralisation observed to date. We are also delighted the mineralisation appears to be structurally controlled and both the copper and gold anomalies are overlapping spatially,” said James Parsons, CEO of EQTEC.

EQTEC’s geological consultants are expected to mobilise to site in the coming weeks, once the summer wet season ends, for what will be the first systematic modern exploration programme at Green Rock.

Fieldwork will focus on validating outcropping mineralisation on the ground, assessing geophysical techniques suited to the malachite-hosted copper-gold systems present, and building broader structural models to explain how mineralisation is distributed across the licence area.

EQTEC had previously been a waste-to-energy specialist and has undertaken a major pivot to gold mining.

Biotech Avacta (LON: AVCT) has undertaken AI-driven analysis to assess differences between its pre|CISION peptide drug conjugate platform and a cleavable linker antibody drug conjugate. This showed that the AVA6103 pre|CISION based treatment was more rapid in penetrating the tumour and the tumour selectivity index (ratio of payload in the tumour vs that in plasma) is three times that of the rival treatment. The share price increased 7.08% to 60.6p.

Governance, risk and compliance software provider Acuity RM (LON: ACRM) has won a contract with Sopra Steria worth £75,000. The ultimate customer is the British government. This is for a programme that has already generated £250,000 for Acuity RM. This follows a £178,000 contract with the British government. The share price improved 5.88% to 0.9p.

Concierge technology platform provider Ten Lifestyle (LON: TENG) has won a multi-year contract with a financial services provider in the AMEA region. The service will be offered to high net worth and ultra-high net worth clients. This has been won from an incumbent provider, and the transition will start in the second half of the year to August 2026. The share price gained 5.11% to 72p.

One Health Group (LON: OHGR) shares rose 4.29% to 243p following yesterday afternoon’s announcement that planning approval had been obtained for the new surgical hub in Scunthorpe. The facility could be completed within 12 months, and it will cost up to £9m. Some of this has already been spent and there is cash to cover the rest. The surgical hub could generate revenues of £6m-£9m at a potential gross margin of 30% – forecast 2026-27 revenues are £30.7m without a contribution from the surgical hub.

Digital transformation services provider TPXimpact (LON: TPX) has followed up the recent contract wins with a third quarter trading statement that has sparked a forecast rise. Margins continue to improve, so although forecast full year revenues are maintained at £76.2m, the operating profit forecast has been raised from £5.5m to £6.2m. Earnings have been upgraded from 3.4p/share to 3.9p/share. Forecast growth in 2026-27 revenues has been raised from 5% to 10% and operating profit is expected to be £7.5m. The share price is 3.955 higher at 39.5p.

FALLERS

RC Fornax (LON: RCFX) full year figures were in line with previously downgraded estimates. Revenues fell 37% to £4.1m, while the pre-tax loss was £1.4m. The defence contractor says activity has improved since the MoD review. This increases confidence in the 2025-26 forecast revenues of £5.8m and a loss of £2m. In November, cash was raised at 6p/share. The share price slipped 10.5% to 9.625p.

Essensys (LON: ESYS) is recommending a 17p/share cash offer by a bid vehicle backed by founder Mark Furniss that values the flexible workspace software provider at £11.3m. there is a one-for-one share alternative for shareholders that want to retain an interest in the business. The original indicative offer was 20p/share. The share price was already trading below the indicative offer, and it fell a further 9.17% to 16.35p.

Fiinu (LON: BANK) says Conister Bank is delaying the launch of the Plugin Overdraft until the second quarter of 2026. Testing has commenced and a third-party payment interface is being developed for Conister Bank by Fiinu. The share price declined 7.58% to 7.625p.

Alien Metals (LON: UFO) says joint venture partner West Coast Silver reports that assay from the Elizabeth Hill silver project show significant results and extend silver mineralisation away from the historic mine workings both to the north and south. There are multiple near-surface, high-grade silver intersections. The share price dipped 8.11% to 0.17p.

Sylvania Platinum (LON: SLP) has more than doubled interim revenues and declared a 2p/share interim dividend. The outlook for platinum group metals production and prices remains positive. There was a small contribution from the Thaba chrome joint venture, which should make a larger contribution in the second half.

The AIM-quoted tailings processor and minerals explorer, which has six platinum group metal processing plants in the Bushveld complex in South Africa, produced 49,164 4E platinum group metals (PGM) ounces in the six months to December 2025, up from 39,398 ounces in the corresponding period last year. The first chrome and PGM products were produced by the Thaba joint venture.

Interim revenues were 110% higher at $99.8m due to a combination of increased production and a 55% rise in platinum group metals prices. There was a $600,000 contribution from chrome sales. Pre-tax profit jumped from $9.7m to $36.7m, which was after a $12.3m write-down of the Hacra exploration project.

The centralised PGM filtration plant was commissioned late in the period, and it will enable a more stable quality of concentrate to be produced, which will help to prevent penalties from buyers.

Cash was $54m at the end of December 2025. Management has set aside $2.5m for share buybacks. That still leaves plenty of cash to invest in the existing business. There is another potential chrome joint venture, as well as two remaining exploration projects.

Full year production guidance is 90,000-93,000 4E PGM – seasonally lower second half – and there is a chrome concentrate target of 60,000-90,000 tons.

The chrome target has been reduced due to plant optimisation issues that were more complex than expected. A review of the mine plan is being undertaken. The plant could still ramp up to full capacity by the summer.

Panmure Liberum forecasts a full year pre-tax profit of $90.5m, although it anticipates a decline to around $71m in 2026-27. The share price edged up 1p to 121p, which is around six times prospective 2025-26 earnings. The forecast yield is nearly 2.5%.

Cash can be invested in new projects that will further enhance revenues and profit.

Diageo will report results on Wednesday and provide insight into how the drinks giant is navigating faltering demand in key markets amid changing consumer behaviors.

Diageo shares have more than halved since their peak in 2022 as a series of setbacks in China, the US, and Africa have raised questions about the company’s growth prospects.

Morningstar analysts have highlighted that the pressures that have dogged Diageo in recent years haven’t gone away, but the company has a much tighter grip on its management.

Verushka Shetty, equity research analyst at Morningstar, said: “In its first-quarter results last year, Diageo lowered its full-year guidance, which makes sense given the current environment.”

“The company now expects a slight decline in organic revenue year on year and low- to mid-single-digit operating profit growth. Previously, it had guided to organic net sales growth in line with fiscal 2025 and mid-single-digit organic operating profit growth. We do not expect a meaningful change here.”

“We continue to see the US and China as the main drags on performance. Pernod also reported softness in both markets last week, while performance was mixed in other regions.”

Shetty continued to explain that much of the focus will be on the action Diageo is taking to control costs and maintain margins:

“Diageo has been progressing with cost-cutting initiatives and divesting non-core assets (including the Bangalore cricket team and East Africa Breweries) to support cash generation and protect margins. There is now increasing discussion that the new CEO, Sir Dave Lewis, plans to restructure the organisation – something that would not be surprising given his reputation.”

Despite ongoing constraints, Morningstar still sees value in the stock.

“Diageo is a four star stock, trading at roughly 18% discount to our Fair Value Estimate,” Shetty said.

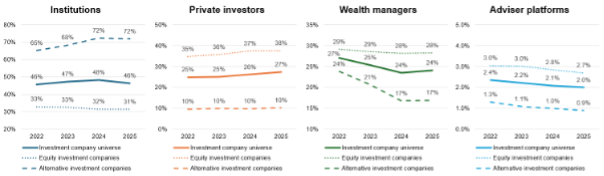

Private investors now hold more than a quarter of all investment company shares, with their share climbing to 27%, worth £57 billion, according to a new report from the Association of Investment Companies (AIC).

That’s up from 26% and £55 billion the year before, a measured but meaningful increase in the ownership of investment trusts by private individuals.

One pound in every six of investment company shares is now held through just three platforms: Hargreaves Lansdown, interactive investor and AJ Bell. Hargreaves Lansdown alone accounts for £14.5 billion, with interactive investor close behind at £13.7 billion and AJ Bell at £5.1 billion.

Wealth manager shares, meanwhile, has stablised. After two years of declining share, wealth firms including Rathbones, Evelyn Partners and Brewin Dolphin held steady at 24% of investment trust shares at the end of 2025, with holdings worth £50 billion.

Rathbones is now the single largest wealth management holder at 4.9% of all investment company shares by value, bolstered by its merger with Investec.

Institutional investors still command the biggest slice of the pie at 46%, though their share has fallen. Adviser platforms hold a modest 2%.

Richard Stone, Chief Executive of the AIC said: “During a tumultuous time for investment companies, it is good to see that wealth managers’ share of the industry has held steady and that private investors have continued increasing their share. We are not quite at the point where every headwind is turning into a tailwind, but there are some positive signs, such as the narrowing of the discount from 19% in 2023 to 11% today, and the partial resolution of the cost disclosure issue that has been a cloud over the sector for some years.”

The AIC’s report, based on analysis of £187 billion in holdings, roughly 90% of the sector’s £208 billion market capitalisation, also reveals an interesting insight into international participation. UK investors hold 74% of investment company shares overall, but that drops sharply to just 58% for trusts investing in alternative assets. US investors pick up much of the difference, holding 23% of alternatives-focused trusts compared to 13% of the broader sector.

The FTSE 100 was trading in the red on Tuesday after AI worries hit US stocks overnight, dragging the S&P 500 lower and hitting sentiment in Europe.

The market is still showing signs of concern around the potential for AI disruption, evident in a sell-off in US financials overnight – the latest sector to be hit by targeted selling, which is seemingly moving from sector to sector.

AI-related selling spilled over into the UK session and put AI beneficiary software stocks on the back foot in early trade, although losses here were partially offset by strength in commodities and strong earnings from Croda and ConvaTec.

“While investors looked a bit dazed from a wobbly start to the trading week, market movements on Tuesday would suggest they’re regaining their balance rather than falling over,” says Dan Coatsworth, head of markets at AJ Bell.

“European indices were down a touch amid weakness in financials and pharma, yet the FTSE 100 was propped up by strength in oil and consumer goods sectors. Futures prices imply small gains on Wall Street when trading opens later today, which is important as that could help repair investor sentiment.

“Investors have plenty to worry about, and Nvidia’s results on Wednesday have the potential to make or break the market depending on what it says about AI.”

The FTSE 100 was trading 0.3% lower at the time of writing as strong corporate results limited losses elsewhere.

“That’s offset continued falls in software and data-focussed companies such as Sage, RELX, Experian and the London Stock Exchange Group as herd mentality stokes anxiety around the threats from Artificial Intelligence. Warren Buffett’s mantra of being greedy in times of fear could serve investors well here, as long as they’re prepared to hold for the long-term,” said Derren Nathan, head of equity research, Hargreaves Lansdown.

RELX was down 1.8% while Sage lost 0.7%.

Croda was among the gainers after the specialty ingredients and chemicals group posted a 4.4% increase in sales and a 4.8% rise in adjusted EBITDA. Shares were 2% higher.

ConvaTec was the FTSE 100’s top riser, surging 8%, after increasing its guidance amid an improving pipeline and outlook.

Jonny Mason, Chief Executive Officer of ConvaTec, said: “Convatec performed strongly in 2025, demonstrating further resilient growth. We delivered broad-based organic revenue growth across all categories, supported by new product launches, operating margin expansion, mid-teens growth in adjusted earnings per share and strong cash conversion.”

“Looking ahead, we are increasing our medium-term revenue growth target to 6-8% from 2027. This acceleration follows the successful implementation of our strategy and is underpinned by our rich innovation pipeline.”

Melten Energy & Metals led the charge in the commodities sector, posting gains of 3%. Rio Tinto rose 0.6%.

ConvaTec shares surged to the top of the FTSE 100 leaderboard on Tuesday after lifting its outlook amid strong earnings growth and a ‘rich innovation pipeline’.

ConvaTec has reported a solid set of full-year results for 2025, with revenue rising 6.5% to $2,439m and adjusted operating profit climbing 12.1% to $544m. Adjusted diluted earnings per share grew 16% to 17.6 cents, comfortably in the mid-teens range the group had guided towards.

The adjusted operating margin widened by 110 basis points to 22.3%, whilst the company generated $362m in free cash flow to equity before growth capex. This was broadly flat year-on-year, but reflecting a step-up in capital investment to $185m as the group backs its pipeline.

This was all good news for investors, who were happy to bid the stock higher on Tuesday, sending shares up 7.4% as of the time of writing.

Growth across the board

All four divisions delivered organic revenue growth. Infusion Care led the way at 12.5%, driven by strong demand for infusion sets in both diabetes and non-diabetes treatments.

Continence Care grew 6.6% on US volume gains and expanding international sales, whilst Ostomy Care added 4.5%, supported by new patient starts and the well-received Esteem Body launch. Advanced Wound Care grew 4.1% excluding InnovaMatrix, which fell 30% to $69m following a $72m impairment charge on the Triad intangible asset.

2026 outlook

Management expects organic revenue growth of 5-7% excluding InnovaMatrix. The adjusted operating margin is guided to at least 23.0%, taking into consideration tariff costs in the first half. The group is confident it can replicate its double-digit adjusted EPS growth again in the coming year.

“Convatec performed strongly in 2025, demonstrating further resilient growth. We delivered broad-based organic revenue growth across all categories, supported by new product launches, operating margin expansion, mid-teens growth in adjusted earnings per share and strong cash conversion,” said Jonny Mason, Chief Executive Officer of ConvaTec.

“Looking ahead, we are increasing our medium-term revenue growth target to 6-8% from 2027. This acceleration follows the successful implementation of our strategy and is underpinned by our rich innovation pipeline. These results are also testament to our great team of Convatec colleagues who bring our promise of forever caring to life daily for the millions of people around the world who rely on our trusted medical solutions.”

The group returned $300m through share buybacks and is recommending a full-year dividend of 7.244 cents, up 13%.

Analysis for informational purposes only. Capital at risk.

The Brand Illusion: Store aisles suggest plentiful choice, but the market has flipped. Chinese challengers (Haier, Midea) have absorbed or outcompeted many legacy Western labels (GE, Toshiba, Fisher & Paykel), while Korean firms (Samsung, LG) now mainly defend the premium tier. This consolidation is most visible in fast‑growing categories like robot vacuums, where the top five Chinese manufacturers account for roughly 70% of global shipments.

Hidden Component Dominance: Control sits below finished goods. Midea and Gree together produce an estimated 70–75% of the world’s AC compressors, and Sanhua holds roughly 45% of key AC control components (valves, heat exchangers). As a result, many Western brands effectively fund their competitors by sourcing high-margin internal parts from them.

How Chinese Incumbents Keep Growing: Despite a weak domestic property cycle, Haier and Midea have sustained high‑single‑digit revenue CAGRs via overseas expansion, commercial and non‑appliance products, and moving into premium segments.

China’s Win in Home Appliances

The home appliance market looks full of choice—premium Western heritage brands, mid‑range Korean brands, and low-cost Chinese labels. But beneath the badges, competition has become more cosmetic. Chinese manufacturers now control volume, components, and scale, effectively “buying the pyramid” and reshaping industry economics.

The white goods industry has now evolved into a “three-tier” ecosystem:

• The Attackers (China) — Haier, Midea, Gree: These firms combine vertical integration, component ownership and massive OEM/ODM scale. That lets them undercut incumbents on price, win volume globally, and pull ahead on revenue compared with peers like LG, Panasonic and Whirlpool.

• The Defenders (Korea) — Samsung, LG: Rather than competing on cost, they are leaning into software, services and smart features to protect margins and maintain premium positioning.

• The Retreaters (US/EU/Japan) — Whirlpool, Toshiba, GE: Many legacy Western and Japanese firms are pulling back from global volume plays, focusing instead on home markets or profitable niche segments.

Source: Companies, AP

The Fall of The Old Guard

Western and Japanese brands increasingly ceded manufacturing control to Chinese firms, often keeping the brand while outsourcing (or selling) production and supply chains.

Sanyo: White goods business acquired by Haier (2012).

Fisher & Paykel: Acquired by Haier (2012).

GE: Sold to Haier (2016). Haier now leverages the GE brand to sell premium appliances in the US while sharing global manufacturing and distribution.

Toshiba: Midea acquired Toshiba’s appliance business (2016), retaining patents but replacing the supply base.

Gorenje: Acquired by Hisense (2018).

Candy: Acquired by Haier (2019).

Philips: Domestic appliances sold to Hillhouse Capital (2021).

Whirlpool: Pulled back from Europe, spinning EMEA operations to Beko Europe (2024) and shifting focus to North America.

Teka: Acquired by Midea (2025).

The New Big 3: Haier, Midea, and Gree

• Midea (300 HK) — World’s largest appliance maker by volume, capturing ~24% of the global volume in residential air conditioners and ~14% in laundry. Broad OEM/ODM business (c.60% of overseas revenue), dominant in AC compressors (c.45%).

• Haier (6690 HK) — #1 global major‑appliance brand for 17 years; strong in refrigerators and washing machines; grows through acquisitions and brand rollouts (GE, Candy, Fisher & Paykel).

• Gree (000651.SZ) — Specialist in air conditioning with deep domestic exposure and market leadership in compressors (c.25–30% share).

Midea is the largest of the three by revenue driven by a diversified product mix and a substantial overseas OEM/ODM business. Gree is the smallest, due to its narrower focus on air conditioners and heavy dependence on the domestic market.

Source: Companies, AP

Despite a weak domestic property cycle that weighed on appliance demand, Haier and Midea have delivered high‑single‑digit revenue CAGRs in recent years, driven by overseas expansion, product diversification into commercial/non‑appliance segments, and premium products.

Source: Companies, AP

Gree’s growth has lagged because of its exposure to residential ACs (which track the property market). In response, Gree has leaned on higher dividend payouts and channel reforms to improve margins while pursuing gradual diversification. As a result, and because room ACs generally carry higher margins than other appliance products, Gree now reports the highest net margin of the three.

Source: Companies, AP

Category Highlights and Implications

Air Conditioning: The Triopoly and the Hidden Dominance

The Triopoly: Haier, Midea and Gree produce roughly 50% of residential ACs globally. Including OEM production for legacy brands, China accounts for ~70% of room ACs.

Source: AP estimates

The Hidden Dominance: Midea and Gree together make 70–75% of global AC compressors. Key control components (valves, heat‑exchangers) are dominated by Chinese suppliers such as Sanhua (2050 HK) with ~45% share.

Source: AP estimates

Daikin: The “Last Samurai”: Daikin remains the major non Chinese player with strong position in the premium and commercial segment.

Refrigeration: The “Cold Chain” Consolidation

The Rise of Haier: Haier controls an estimated 20–23% of global refrigerator volume via acquisitions and OEM scale — near double the next competitor.

The Fall of Whirlpool: Whirlpool has ceded significant global ground, exiting Europe and selling China operations.

Koreans’ “Smart” Defense: Korean players defend the premium tier with “smart” features; LG now leads the US fridge market on share (c. 24%) via premium positioning.

The “Silent” Challenger: Midea, which owns the Toshiba appliance brand, captures roughly 10% of the branded global refrigerator market and operates a large OEM/ODM business.

Source: AP estimates

Washing Machines: A Tight Race

A tight race: Haier leads with ~16% share, but LG, Samsung and Whirlpool each retain over 10% shares, limiting a full Chinese monopoly.

Whirlpool’s stronghold in the US: Whirlpool maintains a dominant US position (~46%) due to brand loyalty and channel strength.

Korean players’ tech moat: Samsung and LG defend premium pricing with tech-led differentiation (AI sensors, auto dosing).

Source: AP estimates

Smart Robotics Cleaner: Pioneer dismantled

Chinese dominance: Five Chinese makers (Roborock, Ecovacs, Dreame, Xiaomi, and Narwal) control nearly 70% of the global shipment volume. They won by deploying advanced R&D, such as LiDAR navigation and AI object avoidance, at fast speed.

The Fall of the Pioneer: iRobot, which invented the Roomba, filed for Chapter 11 bankruptcy in December 2025 and is being acquired by its own Chinese manufacturer, Picea Robotics.

Source: AP estimates

This article is a “periodical publication” for information only and is not investment advice or a solicitation to buy or sell securities. This article does not constitute a “personal recommendation” or “investment advice” under UK FCA regulations. Investing in equities involves significant risk. The author holds NO position in the securities mentioned. There is no warranty as to completeness or correctness. Please do your own due diligence or consult a licensed financial adviser. Please read the Full Disclaimer before acting on any information. Images created with the assistance of Gemini AI.