UK GDP grew 0.5% in February before the Iran war started, as strong services and production offset weakness in construction.

UK growth of 0.5% in February was much higher than the 0.1% recorded in January, showing the UK economy was getting itself on a better footing before the US and Israel launched attacks on Iran.

Luke Bartholomew, Deputy Chief Economist at Aberdeen, said: “The UK economy grew much faster than expected in February after a period of very sluggish growth.”

Bartholomew continued to explain that although the data for February was strong, the world was a very different place now and that upcoming data points, such as unemployment figures, would be a better guide to the health of the UK economy.

“While it is no doubt of some interest that the stronger survey data from earlier this year did indeed translate into stronger hard data, ultimately this report feels very dated given all that has happened since February,” he said.

“As the IMF recently pointed out, the UK economy was very exposed to the shock from the Iran war as a large energy importer with weakly anchored inflation expectations and an already very soft labour market. So next week’s inflation and employment data will provide an important early sign of how this shock is playing out, and have much more influence on the path of interest rates than this report. But with energy markets having stabilised recently, we think the Bank of England is unlikely to hike interest rates in the near term.”

Audioboom has kicked off 2026 in style, delivering its strongest-ever first quarter, with revenue climbing 30% to $22.5m and adjusted EBITDA more than doubling.

The AIM-listed podcast group reported adjusted EBITDA of $1.4m for the three months to 31 March, up 118% on the same period last year, with the margin expanding to 6.2% from 3.7%. Gross profit rose 41% to $4.8m, reflecting what management described as a continued focus on higher-quality revenue and improved creator contracts.

The standout performer was Showcase, Audioboom’s tech-driven global advertising marketplace, where revenue surged 63% year-on-year, driven by stronger demand and expanded inventory. With operating costs held flat at an average of $1.1m a month, the business is now seeing more than 20% of every marginal dollar of revenue drop straight through to EBITDA.

Average monthly downloads and video views hit 170 million in the quarter, up 79% year-on-year, helped by last summer’s Adelicious acquisition and fresh signings including Crooked Media, RedHanded and Hear Me Out.

Those tier one deals alone are adding more than 20 million monthly downloads and YouTube views to the network, plus over 200 million monthly impressions to Showcase.

Average revenue per thousand downloads and views came in at $45.10, down from $60.83 a year ago, as expected given the growing mix of lower-yielding video and UK inventory.

Stuart Last, CEO of Audioboom, said: “2026 is off to a flying start for Audioboom with new major podcast signings, the launch of commercial partnerships in video, and excellent financial performance by all metrics.

“In February we signed Crooked Media to the Audioboom Creator Network. Crooked is a leader in political podcasting, and will be part of our network through this year’s US midterm election and the 2028 Presidential election. Together with other newly signed top tier podcasts like RedHanded and Hear Me Out, more than 20 million new downloads and video views have been added to the platform as we achieved record monthly distribution of 170 million during the quarter – up 79% on the same period last year.

“Optimising the yield from those new downloads and video views will be key to our future growth. Our new partnerships with Spotify and Apple provide us with enhanced monetisation options for our video creators, ensuring we are the go-to platform for podcasters whether in audio or video form.”

The FTSE 100 was little changed on Wednesday despite the S&P 500 closing just shy of a record high overnight, fueled by a tech rally.

But Europe’s lack of technology shares meant the optimism in the US didn’t translate to a higher FTSE 100 with European indices dragged lower by the luxury sector.

Hopes of a ceasefire and the IEA cutting its 2026 global demand growth forecast amid a weakening demand picture weighed on oil prices and helped provide some support for the FTSE 100, which was up 5 points at 10,615 at the time of writing.

“The optimism that had been fired up on hopes that fresh talks could end the Iran conflict has begun to seep away,” said Susannah Streeter, chief investment strategist, Wealth Club

“Stocks on Wall Street nudged fresh record levels as oil prices dipped back. But given the hurdles to cross, this could be interpreted as a dose of irrational exuberance. In Europe there’s a lot more caution around as companies count the cost of the conflict.

“The FTSE 100 has struggled to hold onto early gains while the CAC 40 in Paris is deep in the red, dragged down by luxury goods giants.”

Burberry was among the FTSE 100’s top fallers, declining in sympathy with French luxury names that reported lower sales, driven by a lack of Middle Eastern buyers.

Antofagasta is often among the FTSE 100 top gainers or losers and has one of the highest betas of the index. Today, it released production figures that show copper production falling but gold strengthening. The net result

Alex Pugh, Investment Writer at Freetrade, said: “Gold saves the day for Antofagasta. The mining firm’s Q1 was a softer production quarter but a stronger net cost quarter. Copper production fell 8% year on year to 143,000 tonnes, but net cash costs dropped to $1.08/lb thanks to a surge in by-product credits from gold and molybdenum.”

“Management is sticking to full year guidance and expects production to improve quarter on quarter as grades and processing rates recover at Los Pelambres copper mine. So the question now is whether Q1 was simply a planned soft start, or whether the second-half ramp will need to do more of the heavy lifting than investors might like.”

Barratt Redrow shares were 2% higher after the company reaffirmed its completions outlook for the year, despite warning of a potential impact from the war in Iran.

“The conflict in Iran and the implications it has for inflation and interest rates have shaken the foundations of the housebuilding sector, so there will be a modicum of relief after Barratt Redrow’s third-quarter update,” Russ Mould, investment director at AJ Bell, explained.

“The company is sticking with guidance, albeit for a financial year which ends in a matter of weeks. Demand is holding up for now, with sales rates ticking higher and the order book in reasonable shape, but the company’s decision to materially scale back land purchases feels instructive as it reacts to limited forward visibility.”

Standard Life’s proposed acquisition of Aegon UK in a deal that would create the UK’s largest pensions and savings group helped firm the stock up by 1.7%.

Oracle Power (LON: ORCP) has announced assay results from another 31 holes at the Northern Zone Intrusive Hosted gold project in Western Australia. They are some of the best intercepts for grade and width drilled at the project. The tenement is being converted to a mining lease. The share price jumped 35% to 0.0675p.

Silver Bullet Data Services (LON: SBDS) is continuing its strong momentum into 2026. First quarter revenues are 22% higher and are better than the digital advertising services company budget. Margins are improving. Cost savings helped the company to report its initial EBITDA quarterly profit, and the company should be cash flow positive by the end of the second quarter. The share price gained 18.4% to 22.5p.

LiDAR wind sensor and software developer Windar Photonics (LON: WPHO) has secured a record number of test orders in the first quarter of 2026 and full year revenues are expected to be €7.8m, up from €6.4m in 2025. That assumes 50% of the ten active test orders are converted into contracts. A £20m share subscription facility has been agreed with GEM Global Yield LLC. The company is near to appointing a new chief executive. The share price increased 12.7% to 31p.

Iodine producer Iofina (LON: IOF) generated record production of 179 tons in the first quarter from a combination of new capacity and higher brine temperatures improving recovery. First half guidance is being upgraded to 325-355 tons. Iodine prices are still above 70/kg. Canaccord Genuity has raised its revenue forecast from $69.5m to $71.6m and earnings from 3.7 cents/share to 3.9 cents/share. The share price rose 6.78% to 31.5p.

Bow Street Restaurants (LON: BOW) has made progress with improving the performance of its existing stores and has identified potential acquisitions. Full year revenues fell from £36.6m to £31.3m following the closure of some sites. There was a swing from an underlying operating profit of £400,000 to a £500,000 loss. There was an impairment charge of £7.3m following a review of assets. Refurbishments are helping to boost income. The number of restaurants has been reduced to 29 and the refurbishments are continuing. Net cash was £11.1m at the end of 2025. This will also fund acquisitions of restaurant groups, with the initial purchase potentially an Asian style brand. Trading has improved so far this year with like-for-like growth of 6.1% in March. A 2026 loss is still expected from the current operations. The share price improved 1.69% to 0.3p, having reached 0.31p earlier.

FALLERS

Trellus Health (LON: TRLS), which developed the Trellus Elevate platform to manage complex chronic conditions, has issued another 48.7 million shares on conversion of £50,000 of loan notes. That takes the number of shares in issue to 371 million. The share price is one-fifth lower at 0.2p.

Anglo Asian Mining (LON: AAZ) produced 3,711 tonnes of copper, 42,796 ounces of silver and 6,062 ounces of gold in the first quarter. Cash was $37.2m at the end of March 2026, while debt was $19.5m. The share price declined 3.85% to 250p.

Thor Explorations (LON: THX) had cash of $154m at the end of the first quarter of 2026 and it could reach $351m by the end of the year. It produced 23,397 ounces of gold at the Segilola ming, which was better than expected due to the high recovery rate, and is well on the way to the 2026 target production of 75,000-85,000 ounces of gold for the full year at an all in sustaining cost of up to $1,200/ounce. There is further drilling at the Douta project. The share price fell 1.23% to 80p.

This morning the near £214m-capitalised ASA International (LON:ASAI) has announced its Final Results for the year to end-December 2025 – they were excellent.

The group, which has a strong commitment to financial inclusion and socioeconomic progress, is one of the world's largest international microfinance institutions, providing small, socially responsible loans to low-income entrepreneurs, most of whom are women, across Asia and Africa.

This morning’s results showed a doubling of profits and the impact of its scaling opportunities. ...

Barratt Redrow has reported a resilient third quarter, with private reservation rates ticking up and the housebuilder reaffirming full-year guidance despite growing economic uncertainty.

The group’s net private reservation rate rose 3.2% to 0.64 per outlet per week, up from 0.62 a year earlier. Including contributions from the private rental sector and multi-unit sales, the rate climbed 6.3% to 0.67.

Barratt’s shares were 2% higher at the time of writing.

Total home completions in the period came in at 3,274, down from 3,717 in the prior year.

Barratts attributed the decline to a particularly strong comparable quarter last year, when buyers rushed to beat the end of stamp duty relief. Strip this out, and they aren’t doing too badly considering the current climate.

Year-to-date completions stand at 10,718 homes, and Barratt Redrow remains on track to deliver between 17,200 and 17,800 completions for the full year, including around 600 through joint ventures.

The order book is in good shape. Total forward sales jumped 11.2% to 11,395 homes, worth £3.54bn, while the private order book edged 2.5% higher to 5,643 homes. The group is now 94% forward sold for FY26.

On costs, management is sticking with guidance of around 2% build cost inflation for the year, rising to roughly 3% in the second half, though it flagged that higher energy costs could feed through into material prices in FY27.

Like many other listed housebuilders, land purchases have slowed markedly, with just 4,010 plots approved year to date, compared with over 15,000 in the same period last year. The group said this reflects both its disciplined approach and a lack of attractive opportunities, as it works towards a target of 3.5 years of owned land supply.

Year-end net cash is now expected to come in between £550m and £650m, around £150m ahead of previous guidance, helped by the timing of building remediation payments and lower land spend.

In terms of guidance, there was an element of cautiousness. While FY26 adjusted profit before tax remains on track with consensus, the group warned that Middle East conflict is adding to economic uncertainty and could prolong the higher interest rate environment. Visibility beyond the current year, it said, remains limited.

SpaceX has confidentially filed for what could be the largest initial public offering in history, targeting a valuation of up to $1.75 trillion with a roadshow expected to kick off in June.

The listing will be a landmark moment for the space economy, and a rising tide that could lift other publicly traded space companies already delivering real revenue and winning serious contracts.

Here are three Space shares to put on your radar:

BlackSky Technology (NYSE: BKSY)

Rocket Lab (NASDAQ: RKLB)

Intuitive Machines (NASDAQ: LUNR)

BlackSky Technology (NYSE: BKSY)

BlackSky operates a constellation of low-earth-orbit satellites and its proprietary Spectra platform to deliver real-time, AI-enhanced geospatial intelligence. Essentially, on-demand eyes in the sky. The company can task satellites and return analysed imagery in under 90 minutes, serving defence, intelligence and national security customers including the NGA, NRO and Department of Defense.

The investment case centres on BlackSky’s transition to its next-generation Gen-3 satellites, which are already delivering very-high-resolution imagery and exceeding performance expectations.

Full-year 2025 revenue hit a record $106.6 million, with Q4 revenue up 16% year-on-year to $35.2 million. Backlog stood at $345 million, bolstered by over $130 million in new contract bookings during Q1 2025 alone.

Recent wins include an eight-figure international contract for a sovereign Gen-3 intelligence solution and expanding relationships in India. The company is guiding 2026 revenue of $120–$145 million and adjusted EBITDA of $6–$18 million, a meaningful step toward sustained profitability. For a small-cap with deep ties to government intelligence budgets and a genuine technology edge, BlackSky looks well-placed to benefit from increased space spending.

Rocket Lab (NASDAQ: RKLB)

Rocket Lab is arguably the most credible pure-play space company on the public markets and has been gaining investor attention. It operates two business lines: Launch Services (its workhorse Electron rocket and the hypersonic HASTE vehicle) and Space Systems (satellites, components and spacecraft). The company is also developing Neutron, a medium-lift launch vehicle designed to compete more directly with SpaceX’s Falcon 9.

The numbers speak for themselves. Full-year 2025 revenue hit a record $602 million, up 38% year-on-year, with Q4 revenue of $180 million.

Backlog surged 73% to $1.85 billion, underpinned by an $816 million prime contract from the Space Development Agency to design and build 18 missile-tracking satellites.

Rocket Lab flew 21 missions in 2025 with a 100% success rate and posted record gross margins of 44% (non-GAAP) in Q4. Q1 2026 guidance points to revenue of $185–$200 million, maintaining strong momentum. With proven launch capability, a growing satellite manufacturing business and Neutron on the horizon, Rocket Lab is the closest thing to a SpaceX proxy that public market investors can actually buy.

Intuitive Machines (NASDAQ: LUNR)

Intuitive Machines made history as the company behind the first commercial lunar landing (IM-1 in 2024) and has rapidly evolved from a lunar lander startup into a broader space infrastructure and services business.

Its revenue comes primarily from NASA contracts: Commercial Lunar Payload Services (CLPS), the Near Space Network Services (NSNS) programme and engineering services under OMES III. But it is actively diversifying into national security and commercial orbital services.

Full-year 2025 revenue came in at $210.1 million, with the company executing across lunar delivery, satellite communications and orbital transfer vehicle development. The real story is what’s ahead: management is guiding for $900 million to $1 billion in 2026 revenue and expects positive adjusted EBITDA for the full year, a roughly fivefold jump driven by contract ramp-ups and recent acquisitions including KinetX, a space navigation software firm. Combined backlog stands near $943 million. The company has also won work on the Missile Defense Agency’s SHIELD programme.

Customer concentration (NASA accounts for the bulk of revenue) remains the key risk, but this is understandable in the early stages of the space industry life cycle. The pipeline and the company’s ambitions are hard to ignore.

Standard Life has agreed to acquire Aegon UK, the British insurance and pensions arm of Dutch group Aegon, for £2 billion in a transaction that will create the UK’s largest retirement savings and income business.

The combined group will serve 16 million customers with approximately £480 billion in assets under administration, moving Standard Life to the number two position in both UK workplace pensions and UK retail.

The deal significantly scales up the company’s pension and savings capabilities, adding advice, distribution and digital capacity across both channels while securing an established adviser platform.

Andy Briggs, Group CEO of Standard Life, said: “Our agreement to acquire Aegon UK significantly accelerates our vision to be the UK’s leading retirement savings and income business.”

“We will be in an even stronger position to meet the evolving needs of our 16 million customers with enhanced digital, advice and distribution capabilities across Workplace and Retail, strengthening our standing in one of the world’s most attractive markets. Furthermore, the transaction accelerates our shift to capital-light whilst strengthening our cash, capital and earnings position to create increased value for shareholders.”

The acquisition will be funded through a mix of debt, cash and newly issued Standard Life shares representing around 15.3% of the enlarged group’s share capital. Aegon will become a strategic shareholder and asset management partner in the combined business.

Standard Life pointed to £0.8 billion of total net synergy value, comprising £110 million of run-rate pre-tax cost synergies and roughly £340 million in one-off capital synergies.

The deal is expected to add £190 million in adjusted operating profit and £160 million in operating cash generation, with mid-single-digit accretion to adjusted operating earnings per share by 2029.

Made Tech has secured a three-year contract worth £19m with the Government Digital Service, reinforcing the digital consultancy’s position at the centre of Whitehall’s technology agenda.

Under the deal, Made Tech will serve as GDS’s strategic IT and security delivery partner, supporting the rollout of next-generation technology for staff across the department.

The work focuses on improving collaboration, boosting productivity, and reducing cyber risk exposure.

GDS, which sits within the Department for Science, Innovation and Technology, has been a Made Tech client since 2018. The new contract builds on an existing relationship and is expected to be felt in the group’s revenues from FY27 onwards.

MadeTech posted revenue of £27m for H1 2026, making today’s win a notable contribution going forward.

Rory MacDonald, CEO of Made Tech Group, said: “Being selected by GDS, a long-standing client, as its Strategic IT and Security Delivery Partner is an important win for Made Tech.”

“As the centre of digital government, GDS plays a critical role in shaping technology across government, and this award strengthens our position in one of the most important parts of the UK public sector technology market. We are particularly pleased to see the Sales Booking conversion of the pipeline we referenced at the Interim Results, further increasing our confidence in the outlook.”

The win gives a significant lift to the group’s sales bookings, which have now reached £54m year to date. Of that, roughly £41m has been secured in the second half alone, spanning both new and existing clients across a range of contract sizes.

This year, Temple Bar celebrates its centenary. One hundred years is a long time in any walk of life – long enough to have witnessed the Wall Street Crash, two world wars, the dot-com bubble, a global financial crisis, a pandemic, and today, fresh conflict in the Middle East. In our view, through all of it, the principles first set down by Benjamin Graham, the father of value investing – that paying less than something is worth is the most reliable path to long-term investment returns – have proved their worth. They represent the foundation of how we manage the trust today.

To mark the occasion, it seems a good moment to ask what a century of evidence actually tells us about the discipline. The answer is rather compelling.

Proof, not promise – what a century of data shows

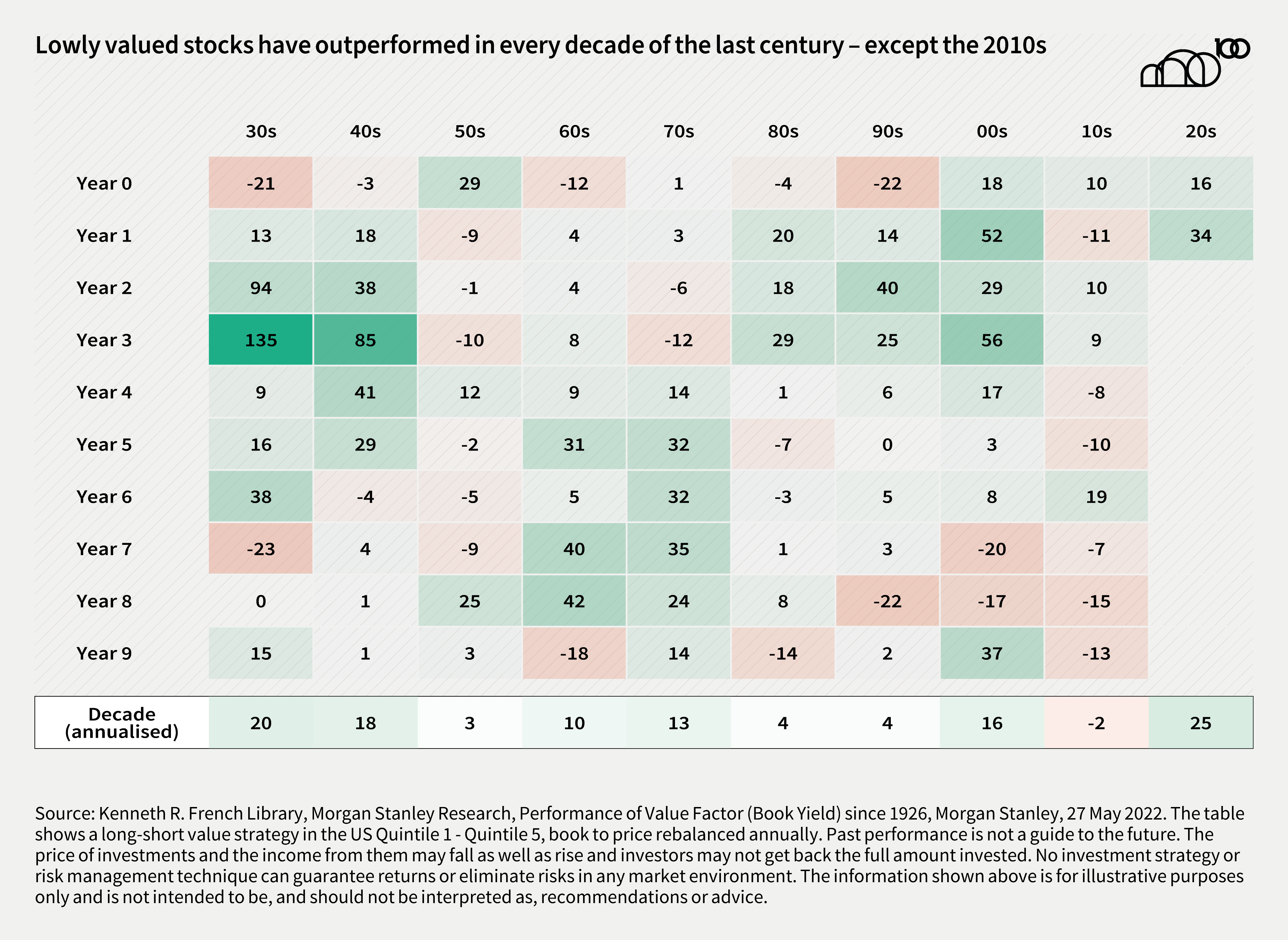

The chart below tracks the performance of lowly valued stocks relative to more expensive ones across every complete decade since the 1920s. The picture it paints is striking – in nine out of ten decades, value investing has outperformed. The one exception – the 2010s – is the subject we will return to shortly.

What the data shows is not that value investing works every quarter, or every year. It does not. What it shows is something more durable and, we would argue, more useful – that over a long enough time horizon, the discipline of buying assets priced below their intrinsic worth has been rewarded with remarkable consistency. Crashes, recessions, wars, bubbles – none of these has been sufficient to break that relationship. Only one decade in a century has managed it, and as we will explain, the conditions that produced that exception were historically unusual.

This conclusion is also supported by the UBS Global Investment Returns Yearbook – one of the most authoritative long-run studies of financial market returns, with data stretching back to 1900. Its long-term factor research shows value delivering positive premiums across most decades in both the US and UK, with the 2010s as the clear outlier. It is reassuring, if not surprising, to find the evidence from independent academic studies pointing to exactly the same conclusion.

Price, value, and the gap in between

Why should this be? The answer lies in a combination of how businesses are valued and how investors behave.

The intrinsic value of a business is determined by its long-term earning power – a figure that moves slowly and is largely indifferent to the noise of day-to-day markets. Share prices, however, move constantly, driven by sentiment, short-term news flow and the collective tendency of investors to extrapolate recent experience into the future. When pessimism takes hold – as we explored in our last newsletter – prices can fall well below intrinsic value. When enthusiasm turns to euphoria, and investors crowd into fashionable areas, they can run well ahead of it.

It is this wedge between price and value that value investors seek to exploit, and it cuts in both directions. The discipline applies as much to knowing what to avoid as to knowing what to own.

The reason this opportunity persists is that the behavioural tendencies that create it keep recurring. The specific mis-pricings they produce are temporary – that is the whole point. But the human instincts that generate them – the discomfort of buying what others are selling, the allure of crowding into what everyone else is buying – are not. That discomfort is real. But historically, it has been the source of consistent outperformance.

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.” — Benjamin Graham

The decade that proved the rule

Which brings us to the exception. The 2010s were, by any historical measure, an unusual decade for financial markets. In the aftermath of the global financial crisis, central banks around the world held interest rates at historically low levels for an extended period, while successive rounds of quantitative easing flooded markets with liquidity. These conditions had a profound effect on investor behaviour.

When the cost of money is close to zero, the present value of future cashflows – even very distant ones – appears to rise dramatically. This mechanical effect made growth companies, whose investment case rests heavily on earnings expected many years into the future, look extraordinarily attractive. The steady, cash-generative businesses that value investors tend to favour looked comparatively dull. Capital flowed accordingly – not because the underlying economics had changed, but because the unusual monetary environment had distorted the lens through which investors were looking.

The result was a decade in which the normal relationship between price and value was suspended. Not broken – suspended. Investors were not wrong to observe that growth was outperforming – we assert that they were wrong to conclude that this represented a new and permanent state of affairs. A century of evidence suggested otherwise, and so it has proved.

“The four most dangerous words in investing are: ‘This time it’s different.’” — Sir John Templeton

Value reasserts itself

Since around 2021, as inflation returned and central banks began to raise rates, the conditions that had suppressed value’s relative performance have gradually unwound. As we explored in some detail in our October 2024 newsletter, value stocks have reasserted their historical dominance across the UK, Europe and Japan – and since that piece was written, the evidence suggests the US has begun to follow suit.

None of this should be surprising. The conditions of the 2010s were historically unusual. Their unwinding was always likely to restore the longer-run relationship between price and value that a century of evidence describes. What is perhaps most notable is how little attention this restoration has received – a reminder, if one were needed, of how quickly markets move on from the narratives they were once certain about.

“Value investing will always be relevant. To succeed, always buy for less than what it is worth, and be smarter than the market. It will never go out of style.” — Charlie Munger

The next hundred years

As Temple Bar enters its second century, the world looks, as it always does, uncertain. Conflict in Iran is weighing on markets, inflation has proved stickier than many had hoped, and the interest rate cuts that investors were anticipating at the start of the year look less certain than they did. These are not trivial concerns.

But they are also not new ones. The history we have traced in this article is, in large part, a history of uncertainty – of investors navigating wars, crashes, bubbles and crises, and of a simple discipline repeatedly vindicating itself on the other side. It is worth noting that Temple Bar itself was founded at a moment of considerable economic turbulence, and that Nick and I were appointed as managers at what proved to be the peak of growth’s dominance. In both cases, the principles of value investing provided a reliable compass.

The lesson is not that uncertainty doesn’t matter. It is that uncertainty, and the anxiety it produces, is often precisely what creates the conditions in which value investing thrives.

“It is largely the fluctuations which throw up the bargains and the uncertainty due to the fluctuations which prevents other people from taking advantage of them.” — John Maynard Keynes

One hundred years of evidence is a rare thing in financial markets. We do not take it lightly, and we do not think it should be dismissed. The principles that Benjamin Graham first set down in the 1930s remain, in our view, the most intellectually coherent framework for navigating whatever comes next. At Temple Bar, they remain the foundation of everything we do.

Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so.

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Nothing in this document should be construed as advice and is therefore not a recommendation to buy or sell shares. Information contained in this document should not be viewed as indicative of future results. The value of investments can go down as well as up.

This article is issued by RWC Asset Management LLP (Redwheel), in its capacity as the appointed portfolio manager to the Temple Bar Investment Trust Plc. Redwheel is authorised and regulated by the UK Financial Conduct Authority and the US Securities and Exchange Commission.

The statements and opinions expressed in this article are those of the author as of the date of publication.

Redwheel may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. Redwheel seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is directed only at professional, institutional, wholesale or qualified investors. The services provided by Redwheel are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.

The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by Redwheel; or (iv) an offer to enter into any other transaction whatsoever (each a Transaction). No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party. Redwheel bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction.