Vodafone shares sank on Tuesday and approached multi-year lows as investors reacted to the telecom group’s preliminary results.

Vodafone shares were down 3.7% to 86.4p at the time of writing. The stock traded around 83p in December 2022, the lowest level since 1997.

The grave state of the telecoms group was reflected in the action taken by the new CEO with the slashing of around 11,000 in an effort to cut costs and boost profits.

Indeed, Vodafone CEO Margherita Della Valle was quite clear in her views of Vodafone’s progress in 2023. “Our performance has not been good enough,” Della Valle said. It’s hard to argue otherwise.

Although operating profit jumped significantly, it was due to the disposal of Vantage Towers. Underlying business performance was poor.

Revenue grew just 0.3% to €45.7bn and service revenue declined to €37.9bn. Adjusted free cash flow decreased to €4.8bn in 2023 from €5.4bn.

“Lacklustre performance has been something markets have come to expect from Vodafone of late, and full-year results didn’t buck the trend. Higher energy costs and continued weakness in Germany meant underlying cash profit came in below the recently downgraded company guidance,” said Matt Britzman, equity analyst at Hargreaves Lansdown.

“New CEO, Margherita Della Valle, has been very vocal about the host of challenges she’s facing in her new role – the honesty is refreshing but not enough to keep shares from falling on the news.

“Today, Vodafone outlined some of its new strategies to combat poor performance, which include cutting around 11,000 jobs over the next three years, streamlining operations and focusing on Vodafone Business. This makes sense on paper, but markets will need to see tangible results over the coming year before they get more excited.”

It is now all about rebuilding profitability and getting back to growth for the boohoo Group (LON:BOO) after the latest set of results.

The £487m capitalised Manchester-based multiple brand-owning retail group, which has built up significantly over the last few years, reported revenues down 11% at £1.77bn (£1.98bn), while its adjusted pre-tax profits fell from £82.5m to a £1.6m loss.

Cost pressures including raw material price inflation, the increased cost of freight, combined with stock clearance and lower sales volumes had significant impact over the year to end February 2023.

Over the last year it spent some £91m on building up its infrastructure to handle efficiently a brand with over £4bn of sales. In so doing it has invested heavily in the automation of its Sheffield site and in its US distribution centre.

It has a clear target of an addressable market of up to 500m potential customers.

The group last year had 18m active customers, which was 10% down from 19.9m the previous year.

Changes in customer behaviour saw it handle 11% less orders at 55.5m (62.4m), while the average order value actually increased 11% to £53.32 (£48.16).

CEO John Lyttle stated that:

“Over the last three years, the Group has achieved significant market share gains.

Looking ahead, we are investing for the future growth of this business with automation, local fulfilment capacity in the US and building global brand awareness.

We will deliver sustainable returns on these investments. We will continue to give our customers the latest trends, outstanding value and a great experience.

Our confidence in the medium-term prospects for the group remain unchanged, and as we execute on our key priorities we see a clear path to improved profitability and getting back to double digit revenue growth.”

Analyst Opinion – 63.5p per share valuation

Rachel Birkett at Zeus Capital expects lower growth this year and next but is impressed with the medium-term guidance in a return to double-digit growth and increased profitability.

Her estimates for the current year to end February 2024 are for £1.72bn sales and a £13.4m adjusted pre-tax loss.

But going into the following year she sees £1.81bn sales giving a profit of £1.2m.

She does, however, have an intrinsic valuation of the group’s implied enterprise value at £801.5m, which equates to 63.5p per share, after net debt.

Conclusion – recovery time is necessary

Cost headwinds have certainly taken their toll, however, given time this group is determined to return to substantial profits and in doing so give its shareholders a meaningful return for their investment.

The return to double digit revenue growth will certainly take time, possibly another three years, so the big question now is just where its shares are going?

After this morning’s news the shares were up 13% at 43.75p.

There were four companies that left AIM during April, plus two reverse takeovers (Beacon Energy (LON: BCE) and Drumz (LON: DRUM), which is changing its name to Acuity RM Group (LON: ACRM)). There were two new companies that joined AIM during the month: Ocean Harvest Technology Group (LON: OHT) and Fadel Partners Inc (LON: FADL).

One company was taken over, one decided to focus on its Nasdaq listing, one was an investment company that ran out of time to find a reverse takeover and the other has become insolvent.

12 April 2023

AdEPT Technology

Managed IT and networking services provider AdEPT Te...

Instem (LON: INS), which provides software and services for drug developers, has boosted its In Silico modelling and simulation operations by acquiring the rights to the ToxHub data sharing platform from eTRANSAFE.

The services help to narrow down the number of potential drug candidates and predict safety, tolerance and other aspects of the potential treatment. The combined service will be rebranded as Centrus.

Thirteen large pharma companies got together and over six years invested €41m to develop the ToxHub platform, where they share research information. This platform speeds up the development of medicines through using artificial intelligence and natural language processing. Around 10,000 non-clinical studies are included on the platform.

Bayer is the first of the companies to take a licence. Others are likely to sign up with discounts provided depending on the level of data provided by the licensee. This will boost group recurring revenues.

There is a serviceable addressable market of £150m. There will be £2.5m of start-up costs in the first year, but there will be limited revenues until 2025.

The fact that these global pharma companies thought that AIM-quoted Instem was a suitable company to take on the platform shows it standing in the sector. It would cost a lot more money for Instem to develop this platform from scratch.

In 2022, revenues improved from £46m to £58.9m, while underlying pre-tax profit jumped from £5.9m to £8.2m. Net cash was maintained at £12.7m. There is an HSBC facility of up to £20m.

A 2023 pre-tax profit of £8.8m is forecast, which reflects good profit growth in most of the existing businesses considering the additional £2.5m of costs. There will also be a higher tax charge that will mean lower earnings. An improvement in pre-tax profit to £11.1m is expected in 2024.

The share price fell 40p to 620p. The shares are trading on 22 times prospective 2023 earnings even after the downgrade. There is potential for further acquisitions.

ON MONDAY, the FTSE 100 was gaining and outperforming European indices with greater exposure to the Turkish economy.

“A weekend of sunshine appears to have put investors in a better mood, with the main UK market indices doing their best to start the new week on the front foot,” said Russ Mould, investment director at AJ Bell.

The good start for UK stocks was an outlier compared to European stocks showing signs of stress due to Turkey’s elections.

A run-off in Turkish elections posed a fresh geopolitical risk to European equities and mainland European stocks suffered early Monday. There is little direct exposure to Turkey among London’s leading indices, and the FTSE 100 rose 0.2%, performing materially better than European indices.

The Turkish Lira sunk on the prospect Erdogan would be re-elected.

“The scattergun of political uncertainty is keeping the Turkish lira on a volatile path, as the country heads for a run-off in the Presidential race,” said Susannah Streeter, head of money and markets, Hargreaves Lansdown.

“Erdogan has led highly controversial monetary policies aimed at increasing exports, rather than tackling painful inflation, and the prospect of Turkey’s ‘strongman’ winning another term has weakened the currency further. There are expectations of a rollercoaster ride in the days ahead, as sentiment waxes and wanes about the prospects for the opposition coalition, which has pledged to pull more conventional levers to restore financial stability.”

FTSE 100 movers

HSBC was among the FTSE 100’s top riser after delivering an upbeat assessment of their Asian business.

“All parts of HSBC Asia are now motoring. In mainland China, we are ideally positioned to facilitate business with the rest of the world; in South and Southeast Asia, we have invested heavily in Singapore, and we have significantly bolstered our growing business in India,” said HSBC Group Chief Executive Noel Quinn.

HSBC shares were 1.6% higher at the time of writing.

British American Tobacco shares were taking the surprise departure of their CEO in their stride with a 0.7% gain.

“It’s never a good look when a company says its chief executive is leaving with immediate effect, and after only four years in the job. This suggests something is not right in the business,” said Russ Mould, investment director at AJ Bell.

“The fact British American Tobacco has promoted its finance director to the CEO role provides some comfort that the new leader already knows the business inside out. However, it raises a lot of questions as to why the change has happened.

“Unlike many companies in this situation, we haven’t had any major clues for problems behind closed doors for British American Tobacco. There have been no profit warnings or activist investors calling for change. The only high-profile calls from shareholders have been a request by GQG Partners to move its stock listing from London to the US in the hope of getting a higher valuation.”

Telecoms billing software provider Cerillion (LON:CER) is one of the most consistent companies on AIM and the share price reflects that. Since floating in March 2016, the share price has risen from a placing price of 76p to 1220p.

There were 29.5 million shares in issue when Cerillion joined AIM and roughly the same number now. So, unlike many companies Cerillion has not been issuing millions of shares to finance growth and this has helped the share price to rise. Admittedly, Cerillion was already a stable and profitable business when it joined AIM, but it has managed to grow organically.

In the six months to March 2023, revenues grew 27% to £20.5m and adjusted pre-tax profit was 46% higher at £9.2m. The interim dividend was raised by 27% to 3.3p a share, while net cash was £23.6m at the end of March 2023.

Margins improved because there were a greater proportion of software sales. Larger contracts are being won and more wins are expected in the second half. Annualised recurring revenues have reached £13.1m as customers take up managed services.

The order book is worth £43m and there is a strong pipeline of potential orders. Telecoms companies are digitising their operations and launching new products and business models. The important thing is to retain customers for longer by improving their engagement.

Full year revenues of £38.5m and pre-tax profit of £13.8m are forecast, but the first half performance suggests that could be beaten – particularly if new contracts are won early enough in the second half.

The share price has remained strong over the past 18 months when many other technology company share prices have slumped. The big difference is the cash generation and winning of large contracts. Net cash could be more than £30m by the end of September 2024.

Cerillion is trading on 32 times prospective 2022-23 earnings, falling to 28 next year. The shares always appear fully valued, but the track record means that they can justify this level.

The upper upscale hotel brand Radisson RED, that presents a playful twist on the conventional, has expanded rapidly in the UK over the past years. The brand is present with bold properties at London’s airports, in lively Glasgow and in buzzing Liverpool, to mention a few. Recently, Radisson Hotel Group announced the signing of Radisson RED Huddersfield, set to open in 2025. The property will undergo an extensive restoration and refurbishment of the historic property The George Hotel, originally built in 1851.

Late last year, the first Radisson RED hotel in the North of England arrived in Liverpool. Located in a thoughtfully renovated Grade II-listed property that first opened as one of the original British railway hotels in the late 1800s, Radisson RED Liverpoolblends history, legacy, and eclectic design. The hotel is also a culinary destination thanks to its modern barbecue and robata grill restaurant, Stoke. It offers classic dishes with a grilled twist paired with unrivalled views of the neoclassical architecture and acclaimed concert venue of St George’s Hall, as well as overlooking the city’s cultural district.

The first Radisson RED property to open in the UK was the award-winning Radisson RED Glasgow. The hotel combines urban style, modern comforts, and a love for the arts with a warm welcome. The hotel is adjacent to the Scottish Event Campus (SEC) as well as close to major local attractions such as Glasgow Science Centre and cultural highlights including Glasgow Royal Concert Hall. The hotel’s RED Sky Bar has won several awards and is ranked among the top 50 best bars in the world*. It is the perfect place for a drink, afternoon tea, DJ sets and snacks with a view.

At Heathrow Airport, Radisson RED London Heathrow opened in 2020, offering 258 bedrooms showcasing the bold and playful design of Radisson RED. The hotel features an executive lounge offering complimentary drinks and refreshments in a vibrant setting and the large conference and events space is flexible to suit a wide variety of group sizes and requirements. It has two multi-purpose conference centres and 41 meeting rooms, including 21 syndicate or breakout rooms. To kick-start or wrap up a long day of travelling or meetings, guests can visit the Pace Leisure Club, featuring a gym, swimming pool, sauna and steam room.

New stunning Radisson RED property on its way

Radisson RED Huddersfield will take over a Grade II listed building, formerly The George Hotel, and will accommodate 91 spacious rooms, including 4 junior suites, which will feature Radisson RED’s signature cutting-edge design as well as references to the history, culture, and the people of Huddersfield, paying homage to the town. Famous for being the birthplace of Rugby League back in 1895, The George Hotel attracted guests from across the world to stay in the iconic landmark.

A full refurbishment will take place across all spaces of the property to restore and enhance the building’s grandeur, while incorporating the unique and distinctive feel of the Radisson RED brand. There will be meeting and events spaces suitable for business gatherings, conferences, and celebrations, located on the ground floor and basement level of the hotel, with a total size of more than 3,000 sq ft. Additionally, the hotel’s first floor is home to the meeting room in which representatives from rugby clubs held a meeting in August 1895 to set up the Rugby Football League.

Radisson RED Huddersfield will be situated in the heart of the town in St. George’s Square and, thanks to the proximity of the train station that is used by millions of passengers every year, provides excellent transport links to its two neighboring cities, Manchester, which can be accessed in 30 minutes by train, and Leeds, which can be accessed in just 20 minutes.

Adela Cristea, Vice President, Business Development UK & Ireland at Radisson Hotel Group, said: “We very much look forward to bringing our fun and vibrant Radisson RED brand to this location. We’re proud to be breathing new life into one of the town’s most iconic buildings.”

The Radisson RED brand launched in the UK five years ago and has been very well received in the market, proving popular with guests, clients, partners and employees. The brand continues its impressive expansion across the UK and the rest of the world. Radisson RED is a brand that incorporates art, music, and fashion into its service to offer an unforgettable stay to all guests.

*Study by Mandoemedia.com that ranked 200 of the world’s rooftop bars

John Wood Group shares plummeted on Monday after US private equity group Apollo said they were halting their pursual of the London-listed energy consulting, engineering, and solutions company.

John Wood Group shares were down over 34% at the time of writing.

Apollo had made a revised 240p cash offer for Wood Group in April – an increase on a prior 230p offer. In February, Wood Group announced they had received three unsolicited bids from Apollo. Wood Group said the initial offers “significantly undervalued the repositioned Group’s prospects.”

Wood Group shares are now lower than their first response to takeover speculation in February.

FTSE 250 constituent Wood Group issued a response to Apollo’s withdrawal and attempted to shift attention to progress in the business:

“The Board remains confident in Wood’s strategic direction and long-term prospects and believes that, following a transformative year in 2022, including new executive leadership and a new strategy, Wood is well placed to deliver substantial value for shareholders.

“Our medium-term targets set out in November 2022 are to deliver adjusted EBITDA growth at mid to high single digit CAGR, with momentum building over time, and to return to positive free cash flow in 2024.

“Furthermore, as set out in the Q1 trading update on 11 May 2023, there is good momentum across all business units which has continued since the end of Q1, with expectations for the full year unchanged.”

Canadian miner SilverCorp Metals Inc is bidding A$0.03 (1.6p) a share in cash and shares for Celsius Resources Ltd (LON: CLA). This values the company at £30.2m. The share price jumped by one-third to 1.3p. SilverCorp Metals is interested in the Makilala-Caigutan-Biyog (MCB) copper gold project in the Philippines. As part of the deal, Celsius shareholders will receive shares in a spin-off that owns the Sagay and Opuwo cobalt projects. This will be on the basis of one share in the new company for every ten Celsius shares. The new company will be quoted on ASX or AIM. Celsius joined AIM in January when it raised £2.4m at 0.8p a share.

Some better news for IOG (LON: IOG). The control event at the Blythe H2 well in the North Sea has been successfully isolated. The first gas from this well should be produced by the end of June. The share price rebounded 15.4% to 6p.

Lexington Gold (LON: LEX) is acquiring White River Exploration, which has five gold projects in the Witwatersrand, which is a major gold region in South Africa. This brings a joint venture with Harmony Gold, which has a non-compliant resource of three million ounces of gold. Lexington Gold will own 76% of White River with the rest owned by black economic empowerment partners. It will loan £300,000 to White River and issue £6.4m of shares to cover loans made to the company. The share price improved 8.82% to 9.25p.

Scotgold Resources (LON: SGZ) has raised £2m from the placing and open offer at 15p a share with excess applications scaled back. Long hole drilling has commenced and a lower than expected average grade of 4g/t gold is reported. The quantity and grade of ore mined is imported for the commerciality of the mine. The share price recovered 10.6% to 18.25p.

The authorities have denied a request by Orcadian Energy (LON: ORCA) to extend phase A of licence P2320 and the licence has expired, which means that potential disposals of sub-areas will not happen. Orcadian Energy plans to make an application for a new licence. More cash is required for working capital and to pay back a £1m loan from Shell. The share price has fallen by one-fifth to 5p. It is down by two-thirds since the beginning of the year. The July 2021 placing price was 40p.

Scientific instruments developer Microsaic Systems (LON: MSYS) says that its audit is taking longer than expected, but the 2022 accounts should be published by the end of June. The share price declined 13.3% to 0.0325p.

Price rises and cost savings are benefiting documents management services provider Restore (LON: RST), while year-on-year sales are 4% higher in the first four months. On the negative side, technology recycling volumes are not recovering as fast as anticipated due to low sales of new IT. This has led to a cut in forecasts. Canaccord Genuity has reduced its 2023 pre-tax profit forecast from £45m to £41m. This knocked 11.2% off the share price leaving it at 261p.

There was a sharp fall in revenues and profit at Caledonia Mining Corporation (LON: CMCL) in the first quarter. Gold production declined by 13% to 16,100 ounces, while unit cash cost rose by 71% to $1,196/ounce. There was a £800,000 loss in the first quarter, but the dividend is maintained at 14 cents a share. Net cash is $3.2m. The share price fell 4.21% to 1025p.

Having enjoyed great success on AQUIS, Marula Mining is seeking to diversify its investor base with an AIM listing.

4. Marula Mining (AQSE: MARU)

Marula is a small-cap mining exploration company focused on battery metals and green-critical commodities in Africa. The company’s diversified portfolio includes four critical minerals in three different countries with strong histories of Chinese investment.

These assets include the Blesberg Lithium and Tantalum Mine in South Africa, the Nkombwa Hill Niobium, Tantalum, Rare Earths, and Phosphate Project in Zambia, and the highly promising Kinusi Copper Project and Bagamoyo Graphite Project in Tanzania.

Marula’s flagship asset remains the 100% owned Blesberg Lithium and Tantalum Mine in South Africa, and the company has spent $1.7 million on increasing its stake from 5% last year. The company also recently announced that it has identified further high-grade lithium deposits at the Blesberg project, with feasibility study work to establish a long-term, hard rock conventional open-pit lithium mining operation to be underway shortly.

In January 2023, Marula announced that the first 1,000 tonnes of lithium ore would be delivered after processing operations began in late November 2022. The company has also entered into a strategic investment and co-development partnership with Q Global Commodities Group, one of South Africa’s leading commodity, logistics, and investment funds, who has subscribed for up to £3.75 million through the issue of up to 100,000,000 new ordinary shares.

Moreover, Marula announced it had entered into a binding heads of agreement with Tanzanian mining company, Takela Mining Tanzania Limited, to secure a 75% interest in ten granted graphite licenses that make up the Nyorinyori Graphite Project for a total consideration of up to £400,000 through staged equity payments. The licenses extend over a combined area of circa 86 hectares and are valid through February 2030.

The company’s CEO, Jason Brewer, is an experienced and hands-on CEO who has been instrumental in the progress made by Marula. The company is scheduled to list on the FTSE AIM in 2023, which should act as a catalyst for further interest and liquidity in the stock.

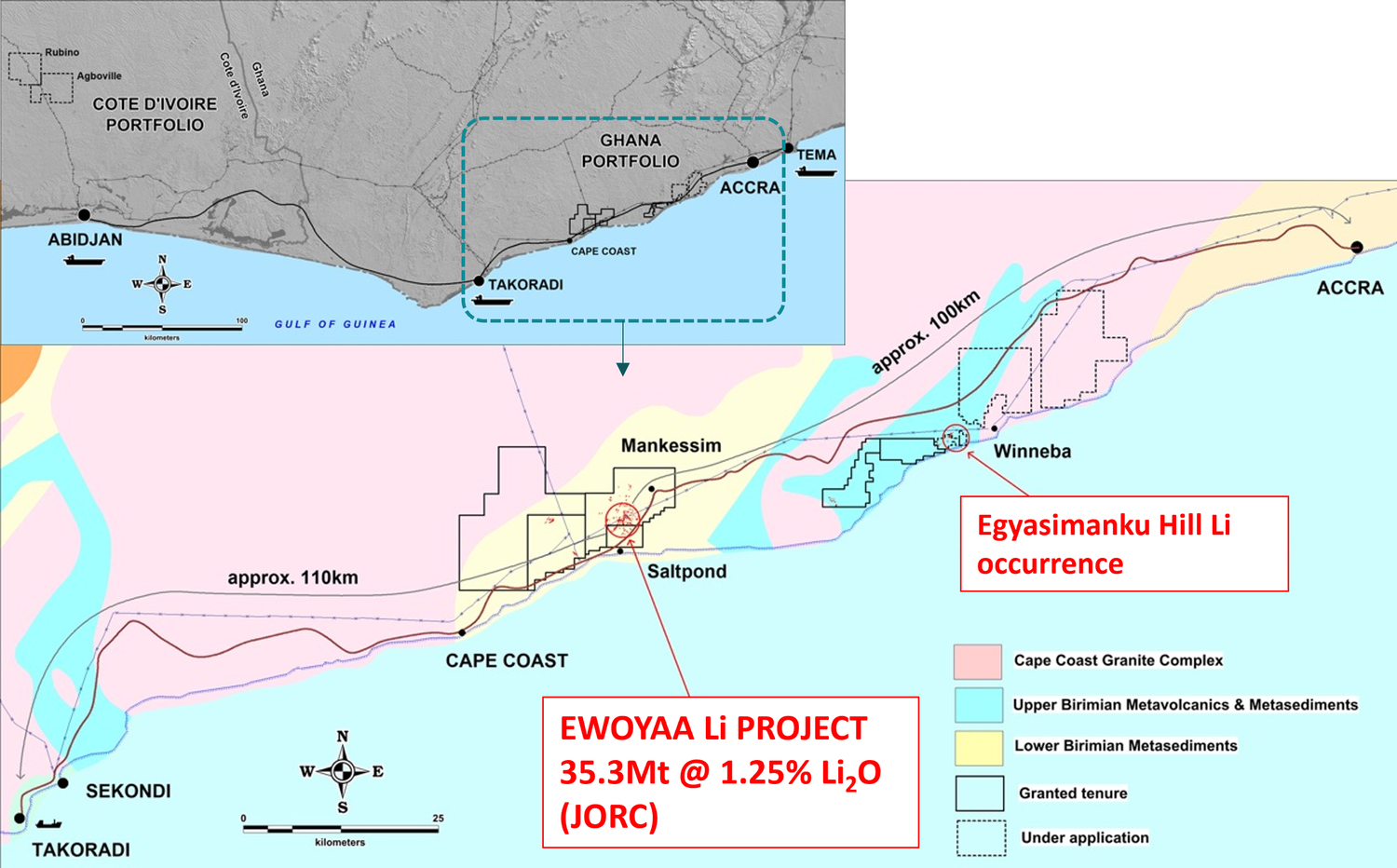

5. Atlantic Lithium (LON: ALL)

The prized possession of Atlantic Lithium is the Ewoyaa Project located in Ghana, which is a vast mine of lithium pegmatite that is likely to be the first lithium-producing mine in West Africa. Piedmont, a strategic investor and a major player in the lithium industry, has provided full funding of $102 million for the project’s production.

The Mineral Resource Estimate for Ewoyaa currently stands at 35.3 million tonnes with 1.25% Li2O. Atlantic Lithium anticipates generating revenue exceeding $4.84 billion throughout the mine’s lifespan, with a post-tax NPV of $1.33 billion.

Atlantic Lithium plans to construct a 2Mtpa DMS plant with the capability to produce 255,000tpa of lithium spodumene concentrate. The company expects to release its definitive feasibility study during the current quarter.

The only downside is the impact of Blue Orca’s short attack in early March. Despite refuted allegations, it continues to have a dampening effect on the company’s stock — but this is a company backed by a billion-dollar titan of the industry.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.