Equipmake Holdings has developed electric vehicle drivetrain technology that has won some initial contracts. It is still early days and the cash raised will help to increase capacity if additional work is won.

The share price ended the first day at 5.875p (5.5p/6.25p). There were five trades at between 5.65p a share and 6.1p a share. Just over 69,000 shares were traded.

Revenues are currently modest, but there are more than £400m of opportunities that are being negotiated. These include active discussions, soe with existing customers, or proposals that have been sent.

Positive news about this ...

Keller (LON: KLR) is the largest geotechnical company in the world, and it is growing strongly. On 2 August it is publishing its interim figures. These should show that Keller is on course

At the end of 2021, there was a record order book of £1.3bn, with £787m of this in North America. Since then, significant orders have been won. Keller has gained a contract in Saudi Arabia, that could end up generating hundreds of millions of pounds. The NEOM project involves constructing a new city and there will be an initial £50m in revenues generated in the next 12 months.

The first half is normally less...

Full year figures from AIM-quoted Hargreaves Services (LON: HSP) were better than previously upgraded expectations. Profit is forecast to fall this year, but they will still be significant.

In the year to May 2022, pre-tax profit improved from £21.2m to £32.7m. That included a £27.3m contribution from German associate HRMS, up from £13.6m in the previous year. Higher commodity prices and increased volumes of minerals traded continued to boost the HRMS performance. The steel waste recycling business moved into profit, while the carbon pulverisation plant is fully operational and broke even.

The...

Waste plastic to hydrogen business Hydrogen Utopia International (LON: HUI) was the best performing Aquis-quoted share last week. There was a 38.9% rise to 9.375p, which took the share price back above the 7.5p placing price. The shares started trading on the US OTCQB Venture Market on 26 July. Executive director Howard White bought 55,500 shares at 9p each, taking his stake to 3.89%.

Coinsilium Group Ltd (LON: COIN) has been appointed adviser to Metalinq Labs Inc and it has a token purchase agreement to acquire $200,000 of future Metalinq tokens, which should be issued in 2023. Metalinq is a next generation Layer 3 protocol solution enabling interoperability between metaverses. Existing Indorse token owners (Coinsilium holds 5.35 million Indorse tokens) are eligible to receive Metalinq tokens. The share price jumped 20.4% to 2.95p.

==========

Fallers

Shares in Lekoil Ltd (LON: LEK) returned from suspension after the publication of interim results. The share price fell 18.4% to 0.775p. Thanks to finance income Lekoil reported a pre-tax profit of $836,000. Olapade Durotoye is leaving the board to take up a role at Savannah Energy. Lekoil is continuing its litigation with the former chief executive and Lekoil Nigeria.

TECC Capital (LON: TEC) shares fell 9.37% to 2.9p prior to their suspension. TECC Capital is subscribing for £300,000 of convertible loan notes in EDX Medical Ltd, with a reverse takeover expected to eventually happen. This is subject to due diligence. EDX Medical was founded by Sir Chris Evans to develop digital diagnostics products and services. It owns a laboratory in Cambridge and offers testing and genomic sequencing research.

AQRU (LON: AQRU) shares declined 6% to 1.175p, having floated as a shell in April 2021 at 5p a share. The decentralised finance company lost £2.32m in the six months to April 2022 and still had net cash of £6.1m.

In the year to March 2022, Oberon Investments (LON: OBE) increased its revenues by 75% to £6.7m. That includes an initial contribution from financial planning business Smythe House. The big increase in revenues came from corporate finance. The pre-tax loss was £581,000, after a £212,500 gain on investments. Funds under management increased by 80% to more than £1bn. The share price fell 5.05% to 4.7p.

Greencare Capital (LON: GRE) is still seeking a suitable cannabis-related acquisition. There is still £679,000 in the bank. The share price fell 1.64% to 30p, which values the company at more than five times its net assets.

Macaulay Capital is run by an experienced investment team that has worked at Chelverton Asset Management, so it has expertise in the smaller end of the market. It is focusing on smaller companies with solid businesses that are too small to attract institutional investors. The flotation will provide access to additional cash and increase the profile of the company.

An initial investment has been made in a food manufacturer, which has also provided income for the company.

The shares ended the first day of trading at 21p (20p/22p), although there were no trades. All shares have all been issued at...

Cyber security services provider Shearwater Group (LON: SWG) is growing rapidly on the back of increased demand for cyber security. New contracts worth £25m were won in the fourth quarter of the year.

In the year to March 2022, Shearwater revenues increased from £31.8m to £35.9m. Two customers account for more than two-thirds of those revenues. The overall growth was held back by a decline in software sales, while the products are re-engineered so that they are part of one integrated platform. The main growth was in security solutions. US revenues grew 26% to £1.5m.

Shearwater moved from breakeven to an underlying pre-tax profit of £900,000. Higher depreciation and amortisation charges mean that pre-tax profit is expected to fall to £500,000 this year, although EBITDA should be higher. Historically, there tend to be upgrades later in the financial year.

There are already £14m of revenues secured for this year, which is 37% of the forecast of £37.7m. There is potential for software contracts, although there may be more SaaS-based revenues meaning that it will take time for these revenues to build up.

There are increasing numbers of cyber attacks and they can be highly costly to corporates. This is making them more aware of the requirement for good cyber security services and software to be in place.

Tintra (LON: TNT) has fast-tracked development of its banking platform and is six months ahead of the roadmap. Tintra intends to raise $25m to fund further development and it believes that it can be done for no more than 10% of the company. It is not clear how this will be done. The shares jumped 78.9% to 170p at the end of the week and they are more than treble the level at the beginning of the year.

Gas and electrical services provider Kinovo (LON: KINO) shares have risen on the back of Jersey-based Tipacs2 Ltd increasing its stake from 13.9% to 25.7%. The company is related to Thomas and Nikolaus Wilheim. The stake first went above 3% in September 2020. MI Sterling Select Companies Fund sold its 9.93% stake. Kinovo is growing its revenues, but it has potential liabilities relating to the DCB business it sold and subsequently got into financial difficulties.

John Selaschi has acquired a 5.13% stake in Active Energy Group (LON: AEG) and the share price rose 62.7% to 6.8p on the week. He also owns an 8.34% stake in Verditek (LON: VDTK).

Coal miner MC Mining (LON: MCM) shares rose 61.3% to 12.5p. MC Mining is finalising a debt and equity funding package for the hard coking coal Makhado project. The bankable feasibility study is being extended to include alternative development plans to enhance th4e value of the project. Performance improvement initiatives are underway at the Uitkomst colliery.

The share price of battery technology developer Ilika (LON: IKA) continues to recover following the recent results. It is 40.5% higher on the week at 78p.

==========

Fallers

Professional services provider Ince (LON: INCE) is the worst performer in the past week after it raised £7m at 5p a share, which was a 58% discount to the previous market price. The share price fell 65% on the week to 5.3p. Ince is also taking on an additional £1.6m loan. Ince has been operating at the limit of its debt facilities following the recent acquisition of broker Arden Partners. There was a cyber attack which management estimates cost £4.9m in cash. An insurance claim has been lodged for this amount, but that could take 12 months to settle. Insurance proceeds would be used to pay off loans. Annual cost savings of up to £5m are being targeted. Revenues are recovering, although Arden had a quieter than expected first half.

Parsley Box (LON: MEAL) floated at 200p at the end of March 2021 and it has fallen to a new low of 11.25p, down 37.5% on the week. Trading is poor and marketing spend is being reduced due to low response rates. First half revenues slumped from £14m to £9.6m. finnCap has reduced its full year revenues forecast to £19m and the expected loss increased to £4.6m. The loss could continue for at least two years and cash could be run out by the end of 2024.

Payment services provider Cornerstone FS (LON: CSFS) continues to decline following the exit of chief executive Julian Wheatland. The share price fell a further 21.4% to 8.25p.

The FTSE 100 was buoyed by shining corporate results from several companies in a busy week for the market, with the blue chip index closing 1.1% higher at 7,428 at close of trading on Friday.

US markets enjoyed a boost with Amazon and Apple reporting sales ahead of market expectations and hopes that the US Federal Reserve might ease back on interest rate hikes, given the US has already entered a technical recession.

The Dow Jones was 0.1% higher at 32,586.1, with the S&P 500 rising 0.5% to 4,093.5 and the NASDAQ up 0.5% to 12,233.5.

“The FTSE 100 continued to grind upwards on [Friday], putting it on course to end a pivotal week in positive territory,” said AJ Bell investment director Russ Mould.

“Also helping sentiment was good news from Amazon and Apple, with both managing to deliver better-than-expected sales despite rising prices and a weakening consumer outlook.”

“It says something about the looking glass nature of investing right now that seemingly bad news in the shape of the US meeting the technical conditions for a recession – even if the ultimate arbiter the National Bureau of Economic Research is still to deliver its verdict – is seen as a positive development as it might lead the Fed to ease back on rate hikes.”

NatWest

NatWest shares gained 8.2% to 248.9p as the banking giant exceeded market expectations with a £2.6 billion operating profit in the interim.

The firm announced a 13.1% return on tangible equity and a cost:income ratio of 58.3% from 67.6% in the previous year.

NatWest reported a total dividend of 20.3p for the HY1 2022 period.

“In a mixed UK bank reporting season so far, there’s no question who is getting the gold star,” said Mould.

“Natwest has knocked it out of the park with its latest results. It’s hard to see what more it could have done to impress the market.”

— UK Investor Magazine (@UKInvestorMAG) July 29, 2022

Croda

Croda shares increased 5% to 7,498p on the back of a tripled HY1 profit linked to high demand in its Consumer Care business.

The company saw a pre-tax profit spike to £636.5 million against £204.1 million the last year.

Croda reported an 8% rise in its interim dividend to 47p from 43.5p in the previous year.

Rightmove

Rightmove shares fell 0.5% to 639.6p, despite a 9% revenue growth to £162.7 million in HY1 2022 from £149.9 million the last year as a result of increased digital products used by customers.

The property site confirmed a 6% operating profit rise to £121.3 million compared to £114.9 million year-on-year.

“This is another decent set of results from Rightmove, helped by a housing market that has remained robust,” said Wealth Club head of equities Charlie Huggins.

“How long can that last with interest rates rising and inflation at a 40-year high? Only time will tell. However, even if the housing market stalls, there are reasons to think Rightmove could prove resilient.”

— UK Investor Magazine (@UKInvestorMAG) July 29, 2022

AstraZeneca

AstraZeneca shares dipped 0.2% to 10,844p after HY1 2022 revenues climbed to 48% to $22.2 billion, reflecting growth in all divisions, except for Other Medicines.

The pharmaceutical giant saw a 71% spike in operating profits to £1.4 billion, excluding the impact of its Alexion acquisition, exchange rates and one-off expenses.

“Drug maker AstraZeneca is something of a stock market rarity right now – a company trading at fresh record highs in 2022,” said Mould.

“But it appeared to fall victim to profit taking this morning as it beat expectations for the second quarter and raised its full-year guidance, yet got only raspberries in response from investors.”

AstraZeneca revenue grows to $22.2bn, raises FY guidance on Covid-19 treatmentshttps://t.co/1KiqTxSaxJ

— UK Investor Magazine (@UKInvestorMAG) July 29, 2022

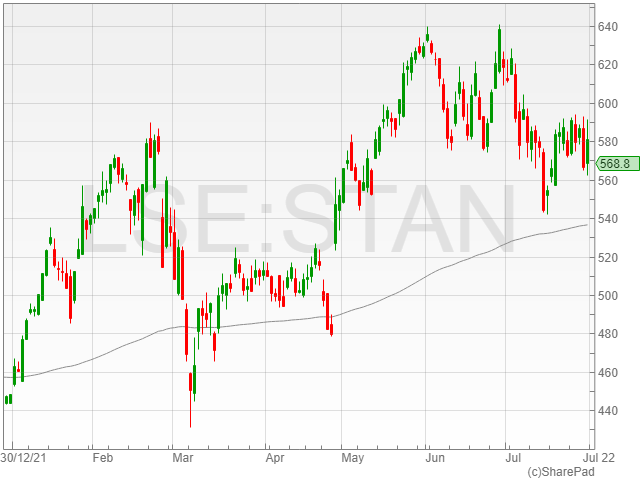

Standard Chartered

Standard Chartered shares fell 0.4%% to 564.2p as its pre-tax profits grew 8.2% to $2.7 billion against $2.5 billion year-on-year in HY1 2022.

The banking firm reported an operating income climb of 7.7% to $8.2 billion compared to $7.6 billion the last year.

The group mentioned a dividend of 4c per share in the period.

Standard Charted also announced the launch of a $5 billion share buyback over the next three years, after its recent $750 million buyback in the interim term.

Glencore

Glencore shares climbed 2.7% to 461.8p following a mixed bag of production results, with rising output of cobalt, nickel and ferrochrome and coal.

However, the mining group announced falling copper production as a result of geotechnical constraints in Katanga, the basis change from its Ernest Henry sale in January 2022, Collahuasi mine sequencing and lower copper units produced from the miner’s zinc sector.

Glencore further mentioned falling zinc, gold, silver and lead production across the interim term.

The company reported its unchanged FY production guidance remained unaltered, with the exception of a lowered copper production expectation.

“Our full year production guidance remains unchanged with the exception of copper, where the ongoing geotechnical constraints relating to Katanga’s open pit and continued management of higher levels of acid-consuming ore, largely account for the reduced guidance of 1,060kt (previously 1,110kt),” said Glencore CEO Gary Nagle.

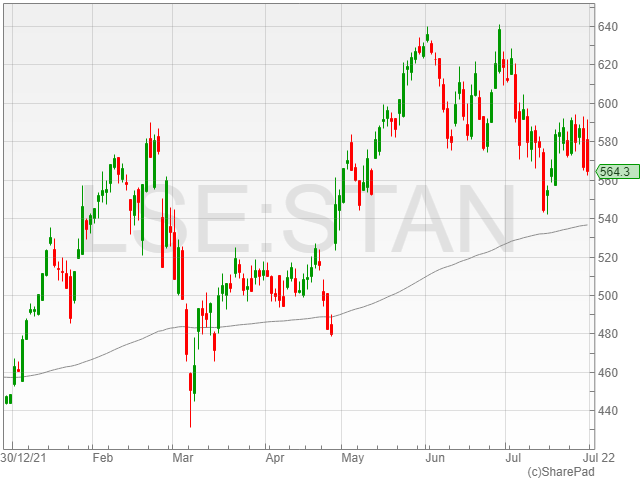

Standard Charted shares fell 0.5% to 563.7p in late afternoon trading on Friday following an announced HY1 2022 pre-tax profit growth of 19% to $2.8 billion, beating market expectations.

The banking firm benefited from rising interest rates, with the latest Bank of England meeting hiking rates 1.25% in a move to tackle soaring inflation.

Analysts projected a $2.4 billion profit for the group in the interim term, along with a CET1 ration of 13.9%.

Standard Chartered confirmed it was on track to reach a 10% return on tangible equity by 2024 at the latest.

Meanwhile, the banking giant reported a higher dividend of $119 million, representing 4c per share.

Standard Charted also announced the launch of a $500 million share buyback, which is scheduled to kick off imminently.

“We remain disciplined on expenses, with significant savings delivered and maintained a strong capital position, with a CET1 ratio of 13.9%,” said Standard Chartered CEO Bill Winters.

“We are also announcing today a new $500 million share buy-back to start imminently. We remain confident in the delivery of the financial targets we set out in February.”

Octopus Renewables Infrastructure Trust shares rose 0.9% to 114.1p in late morning trading on Friday after the group announced an unaudited NAV rise of £40 million to £627.5 at 30 June 2022, representing a growth of 7.1p to 111.1p per share.

Octopus Renewables attributed the rise to increases in short-term wholesale energy price forecasts, especially across the UK, Sweden, Poland and Finland.

The valuation reportedly includes an increased discount to baseload forward prices on revenue not fixed in each market of 30% for 2022 and 2023, and 20% for 2024 and 2025.

The company confirmed a 20% discount for 2022 and 2023 for Nordic markets only at 31 March 2022.

Octopus Renewables commented the impact of updating wholesale energy price forecasts was over £17.2 million.

The group said it had a fixed pricing on a substantial portion of output for the rest of 2022 and 2023 at the Saunamaa and Suolakangas wind farms in Sweden and Finland, and the Penhale solar farm in the UK.

The company added its fixed power price agreements were secured at prices over forecast, resulting in a valuation climb of £1.8 million.

Meanwhile, 60% of ORIT’s forecast revenue at 30 June 2022 to 30 June 2024 was fixed, with approximately 51% of Octopus Renewable’s forecast revenues to be received by its current asset portfolio was confirmed to be explicitly inflation linked.

The firm noted a gain of £3.9 million recognised on the completed construction at the Kuslin wind farm in Poland, along with the completion of civil works and the installation of seven out of eight turbines at the Cerisou French wind farm.

Octopus Renewables announced all its assets under construction were scheduled to achieve operational status by the end of Q2 2023.

The group said it continued to see strong appetite for renewable energy assets in its target regions and no alterations to market discount rates made over Q2.