After weeks of uncertainty and speculation whether the Uk government would U-turn of their radical tax changes, the new Chancellor today confirmed many of the mini-budgets tax cuts would be binned.

Jeremy Hunt has wasted no time in his mandate to bring stability to UK assets by scrapping almost all of the measures first proposed by Kwarteng in his mini-budget.

“The simplest way to adjust the fiscal plan was always going to be to just reverse it and by and large that is what has happened,” said Guy Foster, chief strategist at wealth manager RBC Brewin Dolphin.

The FTSE 100 rallied on the news with housebuilders, banks, insurers and asset managers surging.

The housebuilders produced the most notable gains with Barratts, Taylor Wimpey and Persimmon all gaining more than 4%. Changes to stamp duty are one of Kwarteng’s mini-budget measures likely to remain.

Fears about bond market complexities for pension funds subsided with benchmark 10-year gilt yields falling below 4%. Legal & General, Phoenix Group, Aviva, M&G and Prudential were among the FTSE 100’s wealth management and insurance providers cheering Hunt’s roll back.

Short term reprieve

Despite investors stepping in to pick up bargains in sectors most heavily hit by the doomed mini-budget in September, questions still remained about the longer-term trajectory of the UK economy.

Hunt’s rollback has remedied market volatility in the short-term, but the decision to end current energy bill measures in April brings the health of the UK economy back into the spotlight.

“Markets have reacted positively to the news. However, with taxpayers back to footing the bill, it means little has been done to address the cost of living, except for a temporary cap on energy bills,” said Will Stevens, Head of Financial Planning at Killik & Co.

Today’s announcement will also do little to avert a 75 – 100 bps hike in UK rates at the Bank of Englands’s next meeting in November, piling more pressure on UK households.

The UK Investor Magazine was delighted to welcome Oliver Goffe, the co-founder of the Marloe Watch Company, for a discussion around the UK’s watchmaking industry and how Marloe are targeting a revival in UK watch manufacturing.

The Marloe Watch Company designs and assembles ‘refreshing, heirloom-quality’ watches here in the UK and are at the forefront of a resurgent UK watchmaking industry.

Oliver describes a company that is as focused on the service they provide as the mechanical watches they design. Marloe are a community oriented watch designer and it is evident they want their customers to be involved in every step of their journey.

We discuss how the company was established, the industry they operate in, Marloe’s future expansion, and how they plan to deliver shareholder value.

Jeremy Hunt, the fourth UK chancellor in four months, marked his first full working day in office with an astounding move to scrap almost all of the measures outlined in Kwasi Kwarteng’s catastrophic mini-budget.

Hunt’s first – and primary – job as chancellor was to calm markets and early signs from GBP/USD and UK gilts were he was enjoying a notably more successful reaction than his predecessor.

In a thumbs up from the markets, GBP/USD rose 0.8% to 1.1272 and UK 10-year gilt yields fell below 4% to 3.97%.

The chancellor said his measures were designed to bring ‘confidence and stability’ and reiterated the word stability numerous times in his speech.

Hunt tore up all tax measures announced in September apart from the changes to stamp duty and reversal of national insurance increases made under Johnson’s leadership.

There was also amendments to energy bill support with the current measures now set to end in April. In total, Hunt’s announcement would save £32 billion.

“Perhaps the largest news is the earlier cut off to the energy price cap to April next year. This is a significant development both financially and politically,” said Joshua Raymond, Director at online investment platform XTB.com.

“Financially, the energy price cap is one of the largest contributions to the black hole in the fiscal budget and gives the government more headroom for tighter fiscal cuts especially should a global recession force energy prices lower than expected in the medium term.”

Oil and gas company ADM Energy (LON: ADME) has agreed a £500,000 subscription at 1.2p a share and a $250,000 loan with Tennessee Black Gold. This is more than double Friday’s closing price and the shares jumped 22.7% to 0.675p. There will be a strategic review of the company’s assets, so that it can focus on cash generating assets. The Tennessee Black Gold loan will be drawn down in five tranches of $50,000 and matures on 28 October 2024. The interest rate on the loan is 6%. The cash will pay off creditors and fund working capital while costs are being reduced. Osa Okhomina is stepping down as chief executive when the money is received. Tennessee Black Gold can appoint two directors.

Mosman Oil & Gas (LON: MSMN) announced a quarter-on-quarter decline in net production from 8,815 to 6,958 barrels of oil equivalent, but that was due to there being no contribution from Falcon. Production was halted prior to the latest period. Otherwise, the net production is higher. Oil sales prices were lower, but gas prices increased. Production should increase in the fourth quarter. The share price is 15.4% higher at 0.075p.

Third quarter trading figures from CentralNic (LON: CNIC) sparked a further upgrade for the online marketing and internet domains supplier. Zeus has increased its 2022 pre-tax forecast from $57.8m to $68.7m, while net debt is expected to be lower than previous forecasts at $47.6m. There could be net cash by the end of 2023. So far this year, organic growth has been 66%, which is up from 62% at the half-way stage. The current forecast assumes that the rate of growth slows in the fourth quarter. Debt facilities of $250m have been secured to finance any suitable acquisitions that are found, and the interest rate will be lower than on the bonds currently in issue. The share price is 7.1% higher at 128.5p.

Floorcoverings supplier Victoria (LON: VCP) says interim revenues were more than £700m and EBITDA £100m, which is in line with forecasts. Cash flow should be stronger in the second half following the integration of recent acquisitions. The full interim figures will be published on 29 November. The share price edged up 3.1% to 414.5p, which is around nine times prospective 2022-23 earnings.

Gold and base metals explorer Rockfire Resources (LON: ROCK) has raised £375,000 at 0.125p a share with senior management contributing one-fifth of the funds. That is a big discount to the previous market price and there was a 48% slump to 0.1325p. The cash will fund a geophysical survey and initial drilling at the Molaoi zinc, lead and silver deposit in Greece.

Revenue recognition disagreements over a multi-year contract between auditor EY and MJ Hudson (LON: MJH) mean that the full year EBITDA of the asset management services provider will be lower than anticipated. EY is also questioning cost allocation and capitalisation. Management is positive about current trading. The shares dived 29.8% to 16.5p.

PipeHawk (LON: PIP) shares have fallen 11.3% to 13.75p because a contract with Ventive will be delayed because the customer is still trying to raise development funding. This means that revenues from the contract are not likely to be booked in the year to June 2023.

Naked Wines (LON: WINE) confirmed that an operational and financial update will be held on 20 October. The shares fell a further 5.8% to 79.65p, which is near to the recent low and the lowest the price has been for more than two decades.

Hargreaves Lansdown revenues grew in last quarter after rising interest rates helped boost the wealth manager’s net interest margin.

Revenue grew to £162.9 million in the quarter end September, up from £142.2m in the same period last year. Hargreaves Lansdown’s increase in revenue reflected rising interest on cash that mitigated the impact of falling share dealing transaction.

Hargreaves Lansdown are now operating in a world where competitors are offering share dealing services for free, meaning Hargreaves have had to broaden their offering to remain competitive.

This is evident in the upcoming launch of the new HL US Fund, scheduled to open to investors 1st November. The fund will be managed by external fund managers and is aimed at long term growth in US mega caps. Investors are able to invest in the fund from £100. They also plan a similarly managed UK-focused fund.

Net inflows for the period were £0.7 billion, but assets under administration (AuA) fell £1.8 billion due to adverse market conditions. Hargreaves also warned of an ‘uncertain economic environment’ which may put further pressure on clients’ assets.

“The impact of the challenging macroeconomic and geopolitical backdrop on asset values, client confidence and propensity to invest has been seen across our industry. Against this backdrop we have delivered £0.7 billion of net new business and welcomed a further 17,000 net new clients in the quarter, reflecting both the diversified nature of our platform and also the trust clients place in us,” said Chris Hill, Hargreaves Lansdown Chief Executive Officer.

“Our focus remains on helping new and existing clients navigate these tough times and engaging with them to help improve their financial resilience. Cash savings are high on the agenda for clients and we have seen a further £0.7 billion of net flows into Active Savings leading to a record £5.3 billion of assets. Although flows into risk based investments remain subdued, both client and asset retention rates remain strong and in line with last year.”

Woodford legal case

The trading statement comes days after Hargreaves Lansdown were targeted by 3,200 former Woodford investors seeking £100m for Hargreaves involvement in recommending the failed Woodford Equity Income Fund.

The fund held a number of illiquid investments that were central to the funds collapse and claim alleges Hargreaves Lansdown knew the problems with Woodford’s fund, but continued to encourage investors to invest.

Hydrogen Utopia International (LON: HUI) has signed a memorandum of understanding with Poland-based Elkard in relation to a plastic waste processing plant producing energy. They will start looking for a suitable site and the two companies will share the costs. Hydrogen Utopia International was the best performer on the week with a 34.9% increase to 7.25p.

Invinity Energy Systems (LON: IES) is having a good week. Early in the week it announced a sale of a a 0.8MWh Invinity VS3 flow battery system to Equans Belux and then it won a California Energy Commission project as part of a consortium developing a large solar-plus-storage microgrid. Invinity Energy Systems will provide a 10MWh vanadium flow battery system. Delivery is expected in 2023. There is also a new relationship with US Vanadium, which could lead to a joint venture. The share price is 31.2% higher at 30.5p.

Rural Broadband Solutions (RBBS) edged up 0.4% to 2.32p following the announcement the previous Friday that Tiger Infrastructure Partners Fund III is investing in its two operating subsidiaries. It will invest up to £75m, £16m initially, and own 85% of a new company that will acquire the subsidiaries. Rural Broadband Solutions, which is changing its name to Global Connectivity, will receive £825,000 over three years as a partial repayment of loan to one of the subsidiaries. The existing warrants are being extended to 21 April 2024 and the exercise price reduced to 3p a share.

==========

Fallers

Valereum (LON: VLRM) has appointed First Sentinel Corporate Finance as corporate adviser and the share price declined by 17.2% to 13.25p.

Oscillate (LON: MUSH) has appointed Steve Winfield as a non-executive director. He is a previous colleague of Professor Sir Chris Evans, and he is a director of fellow Aquis company Igraine (KING). The shares fell 5.5% to 0.605p.

EPE Special Opportunities Ltd (LON: EO.P) had net assets of 242.3p a share. The share price was down 3.57% to 135p.

Arbuthnot Banking Group (LON: ARBB) has completed the sale of Arbuthnot Latham’s West End office. The offer was previously indicated as £60m. Chairman and chief executive Sir Henry Angest bought 25,000 shares at 820p each. The share price slipped 0.6% to 820p.

It has been a good week for drug developer Evgen (LON: EVG), which is partnering with Swiss biotech Stalicia for the potential use of SFX-01 for the treatment of autism spectrum disorder and other CNS disorders. This deal could generate up to $160.5m in milestone payments and double-digit royalties, although that is a long way away. The upfront payment is $500,000 with a further $500,000 once a volunteer study is completed in the first half of 2023. If the FDA approves an investigational new drug admission that will spark a $5m payment – possibly next year. Evgen is also undertaking an additional early-stage study for the treatment of glioblastoma using SFX-01. This could de-risk a phase II study and help to secure a partner. It will help to better target brain tumours. R&D costs will be lower and cash resources should lase best performer on the week with a 77.2% jump in the share price to 5.05p.

Identity management software provider Intercede Group (LON: IGP) says trading is in line with expectations and it is acquiring password security management software company Authlogics for an initial £2.5m, plus up to £3m depending on growth in annualised recurring revenues. This broadens the scope of the Intercede business. Net cash will still be £7.9m. The share price rose by 47.4% to 56p.

Powerhouse Energy (LON: PHE) rose 42.7% to 1.384p after it said that it expects to finalise the agreements for special purpose vehicle for the plastics-to-hydrogen project on the Protos Plastics Park before the end of the year. A new site for the company’s headquarters is under negotiation.

Tanfield Group (LON: TAN) has agreed a settlement for UK proceedings with Foulston Siefkin for £3.98m. This relates to the disposal of the Snorkel work platform business. It is continuing its proceedings against Ward Hadaway in the UK and US. The UK trial starts on 7 November. The share price rose 37.5% to 2.75p.

Escape rooms and bars operator XP Factory (LON: XPF) shares have been rising since the beginning of October and the improvement has accelerated this week with a 36.9% rise to 19p. In the first half of 2022, revenues were £8.12m and it is on course to be profitable next year. Finance director Graham Bird bought 100,000 shares at 13.25p each. John Story has reduced his stake from 8.7% to 4.88%.

==========

Fallers

Shares in DeepVerge (LON: DVRG) slumped 62.9% to 2.875p after the company admitted that it was seeking to raise cash via a share issue to repay a loan facility agreed in March with Riverfort Global Opportunities PCC and YA II. A £500,000 repayment was due on 16 October, but this can be delayed if the whole loan and interest is repaid immediately after a fundraising. DeepVerge also needs more cash for working capital. There are no firm details and management is still trying to secure the funding.

Europa Oil & Gas (LON: EOG) fell by 50% to 1.1p because the Serenity SA02 well in the North Sea was not oil bearing. The gross well cost is forecast to be £10.4m with £4.8m paid by Europa Oil & Gas and £5.6m by i3 Energy (LON: I3E). WH Ireland has reduced its estimate for i3 Energy from 66p a share to 49.35p a share. The i3 Energy share price fell 15.5% to 23.2p. John Festival, chair of i3 Energy bought one million shares at C$0.355 each and chief executive Majid Shafiq acquired 206,607 shares at 24.2p each.

Bion Holdings (LON: BION) has returned from suspension following the publication of results for the 16 months to April 2022. The operating business was sold at the end of the period and the company is a shell. Bion raised £1m in a placing at 0.3p a share and the cash was received after the balance sheet date. There was a two-fifths drop in the share price to 0.15p. It will not complete a reverse takeover by 20 October, so the shares will be suspended again.

Sierra Oncology Inc is returning the rights to SRA737, which was jointly developed by Sareum Holdings (LON: SAR) and the Institute of Cancer Research, to the CRT Pioneer Fund. It is a treatment that targets cancer cell replication. Sierra Onclology was acquired by GSK in July. The share price fell by 37.2% to 135p.

Property lending platform operator Lendinvest (LON: LINV) fell on the back of a trading statement. The share price declined 36.4% to 62p. Platform assets under management are one-third higher at £2.4bn, but finnCap has downgraded its full year forecast. Interest rate volatility is hampering margins. Chief executive Rod Lockhart bought 27,111 shares at 67.5p each and chief investment officer bought 60,000 shares at 63.75p each. The July 2021 placing price was 186p.

Investment manager Premier Miton Group (LON: PMI) reported assets under management of £10.6bn at the end of September 2022. That is £3.3bn lower than one year earlier. There were net inflows for fixed income funds. Full year results will be published on 2 December. The share price fell 5.6% to 92.5p.

Faron Pharmaceuticals (LON: FARN) shares fell 7.14% to 162.5p following the completion of the placing raising €8.4m at €1.85 each. The share price is still above the Euro equivalent. The cash will be used for the acceleration of the bexmarilimab, which is an immunotherapy treatment for difficult-to-treat cancers, clinical development programme and manufacturing.

Spirits supplier Distil (LON: DIS) continues to decline after yesterday’s interims. It is 11.8% lower at 0.75p. Sareum Holdings (LON: SAR) is also continuing its decline after Sierra Oncology Inc announced earlier in the week that it is returning the rights to SRA737. There was a further 11.5% fall to 135p.

Tanfield Group (LON: TAN) has agreed a settlement for UK proceedings with Foulston Siefkin for £3.98m. This relates to the disposal of the Snorkel work platform business. It is continuing its proceedings against Ward Hadaway in the UK and US. The UK trial starts on 7 November.

Lebanese restaurants operator Comptoir Group (LON: COM) has appointed former Leon boss Nick Ayerst as its chief executive. The former chief executive resigned last month after pressure from founder Tony Kitous, who still owns 48% of the company. The interim chief executive will return to a non-executive capacity on the board.

The FTSE 100 breathed a sigh of relief in Friday’s session on reports the Chancellor has been sacked, igniting hopes of a broad reversal in the damaging mini-budget proposals and recovery in UK assets.

The FTSE 100 was trading at 6,908, up 0.85% at the time of writing while gilt yields fell.

Investors were attempting to price an increasing fluid situation on Friday with the Chancellor’s sacking raising questions about the future of the Prime Minister. Speculation was also mounting about who the next Chancellor would be, and what their approach would be to rethinking economic plans.

It was later confirmed Jeremy Hunt would step into Kwartengs shoes.

A group of senior Tories have been holding discussions + have decided the following: the sacking of @KwasiKwarteng will prompt them to come out publicly next week + call on @trussliz to resign. My source: “These are serious people. The PM will find it difficult to survive.”

Some investors will be questioning whether today’s gains are simply a bear market rally and whether losses are set to resume as we move towards key central bank meetings in November.

The Bank of England is also set to end bond purchases today, risking potential choppiness in the very near term.

“There will be a long way to go and significant bridge building ahead before the UK risk premium disappears. The cost of government borrowing fell further earlier, with gilt yields dropping as speculation swirled that there would be a change at the Treasury, an indication that investors in the UK might welcome this change to the front seat line up,” said Susannah Streeter senior investment and markets analyst, Hargreaves Lansdown.

As we reported earlier this week, the FTSE 100 UK banks and housebuilders are traders’ equity proxies for the UK’s economic and political outlook. Both sector rose following the sacking of Kwasi Kwarteng but are likely to remain volatile in the coming sessions.

Lloyds, Natwest and Barclays gained as did housebuilders Persimmon, Barratt Developments and Taylor Wimpey. A reversal in the mini-budget proposals has the power to ease pressure on the mortgage market and household spending.

After significant weakness earlier in 2022, both onshore and offshore Chinese equity markets have recently bounced back strongly.

In the period from the end of April to July 22, the Shanghai A-share Index outperformed the S&P 500 Index by 11% and the MSCI Emerging Markets Index by 15%. This rebound came after Chinese equities had underperformed for much of the previous year, following the Common Prosperity drive, which began in summer 2021.

The important question for investors now is: Can this improvement be sustained?

Drivers of earlier weakness

A challenging economic backdrop has weighed on Chinese equities since late 2021. The latest consensus expectation is that China’s economic growth will halve to 4.2% in 2022 from 8.4% in 2021.1 This slowdown reflects the country’s ongoing real estate downturn and its zero-Covid policy, which has resulted in economically damaging lockdowns in major commercial centers including Shanghai and Shenzhen. China equity investors have also had to contend with unhelpful regulatory conditions, both home and abroad.

Easing headwinds

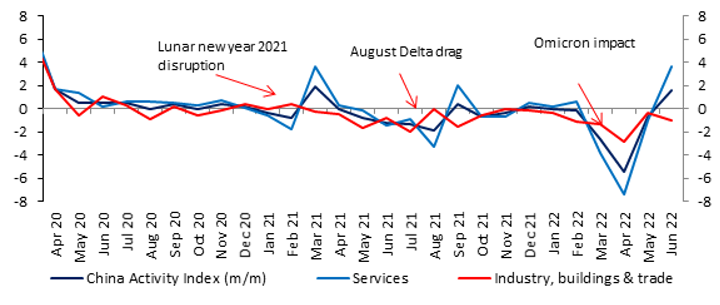

Moderation of some key headwinds has driven the the recent rally in China equities. On the Covid front, China’s zero-tolerance approach has been effective in reducing the number of new cases very significantly. The seven-day average of daily new cases was less than 1,000 as of July 24 — a small fraction of earlier this year, in mid-April, when there was a high of nearly 30,000 cases. This has enabled some controls to be relaxed, including less stringent quarantine rules. This has given way to an uptick in Chinese economic activity lately (Chart 1).

Chart 1: Recovering China economic activity

Source: Research Institute, abrdn, July 2022

On the regulatory side, there have also been clear signs of the new regime bedding down, allowing some easing of pressures. For example, in June, the government gave tentative approval for Ant Group, an affiliate of e-commerce giant Alibaba, to revive its initial public offering in Shanghai and Hong Kong.

Comparatively helpful policy backdrop

Another contributor to improved performance lately has been China’s comparatively much more helpful monetary and fiscal backdrop. Unlike virtually all other major central banks, the People’s Bank of China has not felt the need to join the global trend of sharply raising policy interest rates. On the contrary, since the start of 2022, it has eased policy on multiple occasions through a combination of interest-rate and reserve-requirement cuts. China has been able to adopt this markedly different monetary stance because, compared to the rest of the world, it’s experienced very low inflation, which was running at just 2.5% year-over-year in June.

On the fiscal front too, policy in China is more supportive compared to the rest of the world. For example, our economists think infrastructure spending especially could get a significant boost from efforts to bring forward local government bond issuance.

Valuations not prohibitive for further outperformance

Despite the recent rally, the valuation of China equities remains more attractive compared to many global equity markets. For example, the MSCI China Index forward price-earnings (PE) ratio of 11.1 suggests significant cheapness compared to the MSCI US Index and MSCI All Countries World Index, which have forward PE ratios of 16.3 and 14.2, respectively.2

Despite the recent rally, the valuation of China equities remains more attractive compared to many global equity markets.

At the same time, the forward earnings projections for China corporates seem more than adequate. For 2023, consensus estimates are for 7% revenue growth and 4.7% net margin, which would produce 15% earnings-per-share growth, relative to the expected lower base of 2022.3

Risk factors

However, optimism regarding the outlook for China equities should be qualified by respect for some weighty risk factors. First, while restrictions have been incrementally easing in the past two months, the dynamic zero-Covid policy has not been discarded. This means that new restrictions are still possible, although we think that future lockdowns are likely to be much more targeted and adaptive.

Second, the important property sector, which by some estimates, together with related services, accounts for around 25-30% of China’s GDP, remains a headwind. Until further deleveraging is completed, the sector will probably remain vulnerable to adverse news flow. Recently for example, concerns have been rising that mortgage defaults could rise owing to a wave of homeowners joining a nationwide mortgage payment boycott for unfinished homes. However, given potential contagion risk, we expect the authorities to be very proactive in addressing this issue.

Putting everything together

Putting everything together, we think there are enough reasons to be relatively optimistic regarding the outlook for Chinese equities. In particular, the combination of these factors suggests scope for continued outperformance:

Easing Covid restrictions

easing regulatory pressures

Accommodative monetary and fiscal policy

Relatively undemanding valuations

However, investors would be wise to temper their optimism with due appreciation of the risks, especially regarding the dynamic Covid policy and unresolved stresses in the key real estate sector.

Overall, we think the present environment underscores the need for a selective investing approach that favors Chinese companies with attractive fundamentals, low exposure to the macro risk factors and undemanding valuations.

1 Consensus Economics, 11 July 2022 2 Global Index Briefing: MSCI Forward P/Es, Yardeni Research Inc., 19 July 2022 3 China Equity Strategy – Bullish 2H22 outlook on macro & micro, J.P.Morgan, 22 June 2022

IMPORTANT INFORMATION

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Past performance is not an indication of future results.

Projections are offered as opinion and are not reflective of potential performance. Projections are not guaranteed and actual events or results may differ materially.

Other important information:

Issued by Aberdeen Asset Managers Limited which is authorised and regulated by the Financial Conduct Authority in the United Kingdom. Registered Office: 10 Queen’s Terrace, Aberdeen AB10 1XL. Registered in Scotland No. 108419. An investment trust should be considered only as part of a balanced portfolio. Under no circumstances should this information be considered as an offer or solicitation to deal in investments.