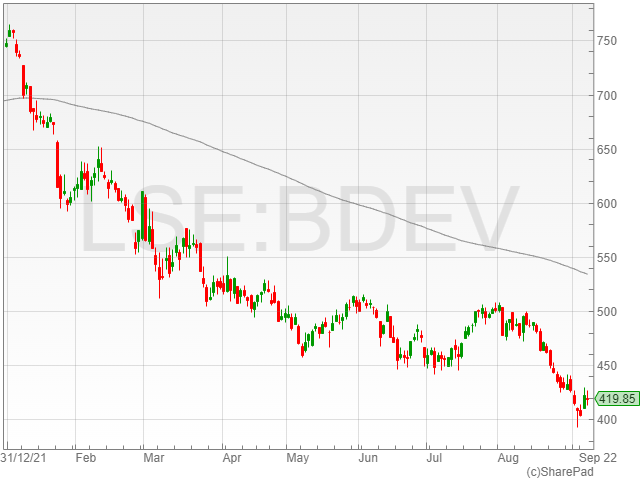

Barratt Developments shares dipped 0.8% to 418.6p in early morning trading on Wednesday, after announcing a statutory pre-tax profit of £642 million in FY 2022 against £812 million the last year.

The company highlighted revenues of £5.2 billion in FY 2022 against £4.8 billion the last year.

Barratt Developments reported total home completions of 17,908 compared to 17,243, marking a recovery to pre-pandemic levels. The group confirmed a targeted 3% to 5% growth in total home completions in FY 2023, representing between 18,400 and 18,800 houses.

The firm mentioned a statutory profit from operations decline to £646 million from £811 million, along with an operating margin slide to 12.3% compared to 16.9%.

Barratt Developments announced an adjusted profit from operations rise to £1 billion from £919 million, alongside an adjusted operating profit margin of 20% compared to 19.1%.

The group noted a basic EPS fall to 50.6p against 64.9p year-on-year, and an adjusted EPS of 83p compared to 73.5p.

The company also highlighted a ROCE of 30% against 27.8% in FY 2022.

Barratt Developments confirmed net cash of £1.1 billion from £1.3 billion the year before.

“This has been a year of fantastic progress, with completions recovering to pre-pandemic levels and excellent productivity across our sites,” said Barratt Developments CEO David Thomas.

“Our financial strength and operational excellence position us well to navigate the macro-economic uncertainties ahead.”

“I’d like to thank our employees, sub-contractors and supply chain partners for helping us to continue to deliver the industry-leading, sustainable homes and developments our customers want and the UK needs.”

Barratt Developments hiked its dividend 25.5% to 36.9p against 29.4p in the previous year.

House prices rose 11.5% per year in August 2022, according to the latest report from Halifax.

The average UK house price hit a record £294,260, raising the rungs on the property ladder further out of reach for home buyers as the cost of living crisis continued to bite.

The figure represented a 0.4% rise month-on-month, recovering from a slight drop in July. However, the climb was a noted slowdown from the average monthly increase of 0.9% over the past 12 months.

Halifax confirmed annual house price growth had been easing gradually, after reaching 12.5% in June this year.

“The property market is looking relatively rosy, but that’s largely because we’re looking in the rear view mirror.” said Hargreaves Lansdown senior personal finance analyst Sarah Coles.

“Prices rose by double-digits again in August, to a new record high, and monthly price rises returned to positive growth again.”

London prices hit new record

The month saw the London property market hit its highest annual price rise in six years at 8.8%, with average prices soaring to a record £554,718.

“Wales saw annual price rises of 16.1% – which is something we haven’t seen in the region for 17 years. Even London, which has been a laggard for years, posted the highest price growth in six years,” said Coles.

Cost of living crisis signals market slowdown

“It looks like everything in the property market is rosy. But this reflects the market two or three months ago, because of the lag between sales being agreed and completions, and in the intervening months, the world has started to look a bit different.”

“Back in May, when interest rates were at 1%, talk of recession was much more subdued and while we had seen the energy price cap rise in April, future rises weren’t at the forefront of people’s minds,” said Coles.

“We had seen demand start to come off the boil, but the RICS report at the time highlighted that prices were still being driven up by a shortage of properties on the market.”

“Now the cost-of-living crisis has hit home, and while we may not be forced to face the full impact of rises in energy prices, we’re still having to cope with rampant inflation across the board. At a time of rising rates and higher house prices, this is going to push property out of reach for desperate buyers.”

However, the housing market decline will come as a bumpy ride, rather than a straightforward downward trajectory.

“As we go through the rest of the year. higher interest rates and runaway inflation are only going to make life harder,” said Coles.

“However, we won’t see annual house price rises fall in a straight line. This is partly because of the echoes of the stamp duty holiday last year which created really lumpy price changes a year ago.”

“However, it’s also because the property market is driven to a huge extent by sentiment, and right now, that’s a bit of a rollercoaster ride.”

Trump’s social media platform hit a roadblock on Tuesday, after the former Apprentice star and the blank-check acquisition firm which agreed to merge with his company were denied shareholder support for a one-year extension to complete the transaction, according to Reuters.

The businessman currently stands to lose a $1.3 billion cash injection for the Trump Media & Technology Group, which runs Trump’s Truth Social app, from Digital World Acquisition Corp, the special purpose acquisition company (SPAC), which was set to take the media company public.

The agreement is currently at a standstill as civil and criminal probes investigate the deal, with the process exceeding Digital World’s initial timeline due to the Securities and Exchange Commission (SEC) review.

Regulators are currently investigating Digital World documents on due diligence of potential targets other than Trump Media and Technology Group, links between Digital World and other entities, the identity of a series of investors, Digital World board policy meetings and trading procedures.

Digital World reportedly needs 65% of its shareholders to vote for the agreement to extend its lifespan by a year for the move to become effective. However, far fewer shareholders than required voted in favour of the deal.

Sources close to the matter said executives did not believe Digital World would muster sufficient support in time for the special meeting of shareholders on Tuesday.

The sources commented one option under consideration was to delay the vote in a move to rally additional support. Without a sufficient number of shareholder votes, the SPAC is set to liquidate on Thursday and return the cash raised in its IPO back in September 2021.

On the other hand, Digital World have the option to extend its life by up to six months without shareholder approval. Sources did not clarify if the company would pursue this option, however.

Investment companies reported a strong level of demand in Q2 despite the volatile market environment, according to the Association of Investment Companies.

Purchases of investment firms amounted to £700 million in HY1 across the sector, representing the highest figure on record.

“The healthy level of demand for investment companies during some difficult months in the market shows that advisers and wealth managers are taking a long-term perspective,” said Association of Investment Companies head of intermediary communications Nick Britton.

“Historically, market downturns have been great times to buy investment companies, though that’s not to say things won’t get worse before they get better.”

Advisor platforms logged £361 million in purchases, representing a 20% growth year-on-year and the second-highest quarterly figure ever recorded.

Net demand earned a further silver medal record at £151 million for the industry.

Market volatility showed its impact on the flexible investment sector as demand surged, accounting for more than any other AIC sector with 17% of purchases.

Flexible investments stole the crown from previous sector victor Global, which held the winning spot for purchases over the past 20 quarters. Global dropped to second place with 13% of overall purchases.

“It’s noteworthy that the Flexible Investment sector proved so popular last quarter. This sector contains investment companies that can invest in a range of assets, including a few well known ‘capital preservation’ mandates,” said Briton.

“It doesn’t take too much imagination to guess why these might have been popular this year.”

Smaller companies gained ground over Q2 with 7% of purchases, while UK commercial property gained 6%, UK equity income won 5% and infrastructure secured 5% of the investment pie.

“[A] strong showing for sectors trading on wider-than-usual discounts, such as UK Smaller Companies, suggests that some buyers may have been shopping for bargains,” said Briton.

“The resilient demand for investment companies in the second quarter of the year bucked a broader decline in total platform purchases.”

“Purchases of all products on adviser platforms fell to £48.93bn in Q2, 5% lower than the same quarter last year.”

The price of oil suffered a dramatic fall on demand fears, with benchmark Brent crude dropping 3.2% to $92 per barrel.

The move comes on the heels of the US Federal Reserve’s hawkish interest rates stance, with the latest positive jobs report adding fuel to the fire for Fed chair Jerome Powell to hike rates to prompt a softening in the jobs market.

US inflation currently stands at 8.5%, representing a decline from its 9.1% figure the previous month. However, the one-month drop provided little incentive for Powell to change course, with the chair confirming his intention to continue rate hikes until inflation fell far closer to the organisation’s 2% target level at last month’s Jackson Hole convention.

Meanwhile, continued lockdowns in Chinese city Chengdu and tech hub Shenzhen prompted increased demand fears, as the country’s zero-Covid policy continued to see its production hubs shut down for extended periods.

The OPEC+ decision to roll back its September production rise of 100,000 bdp on Monday did little to stop prices falling, after the cartel cited market price volatility as its motive to cut production, although its minor alteration was essentially symbolic in nature, representing approximately 0.1% of total international demand.

“The OPEC+ news is now in the market and the focus has temporarily shifted to economic and inflationary concerns amongst which the two relevant factors are the extended COVID lockdowns in China and Thursday’s ECB rate decision,” said oil broker PVM representative Tamas Varga.

“Undoubtedly, they raise fears of demand destruction.”

Orosur Mining Inc (LON: OMI) says assays from one of the three drill holes at the Pepas prospect in Colombia have shown substantial high-grade gold intersection. More holes are being drilled. Joint venture partner Minera Monte Aguila has operational control and has spent $4m in the financial year. This sparked a 37.9% jump in the share price to 16.55p.

Ethernity Networks (LON: ENET) has recouped some of last week’s losses with a 24.3% gain to 11.5p. The shares have commenced trading on the OTCQB Venture Market in the US, but it is difficult to see this being of much benefit to the share price in the short-term.

RAB Capital has taken a 4.02% stake in Strategic Minerals (LON: SML) and the shares are one-fifth higher at 0.3p.

Verici DX (LON: VRCI) has revealed positive initial results from its validation study for pre-transplant prognostic test Clarava. This has shown to be effective in identifying patients that are likely to reject a transplant. There will be an extended study for a further six months. The share price rose 8.57% to 19p. Interim figures will be published tomorrow.

Building products supplier Alumasc (LON: ALU) reported improved pre-tax profit on continuing activities following the sale of the loss-making Levolux business. Revenues increased from £77.8m to £89.3m, while underlying pre-tax profit improved from £10m to £12.7m. Demand for water management and building products remains strong in the new financial year, although finnCap is being cautious with its forecast and assuming a decline in operating margin and pre-tax profit in 2022-23. The share price edged up 8.55% to 165p. That means that Alumasc is valued at seven times prospective earnings and has a forecast yield of 6%.

Trading is holding up well at building and plumbing products distributor Lords Group Trading (LON: LORD) even though problems with boiler supply hampered the plumbing division in the first half. First half revenues were one-fifth ahead at £214.2m and they are set to hit £435m for the full year. Interim pre-amortisation profit improved from £9m to £11.3m. The interim dividend is 0.67p a share. The share price moved 7.14% higher at 75p.

Ondine Biomedical Inc (LON: OBI) has announced results for its US phase 2 trials of its nasal photodisinfection treatment, which eliminated or significantly decreased Staphylococcus aureus in 92% of carriers treated. The treatment was safe and well tolerated. The full results will be published in November. There will then be multi-site phase 3 trials to move towards FDA approval. The share price improved by 7.14% to 41.25p.

Brownfield land developer Inland Homes (LON: INL) says delays in receiving planning consents and selling sites mean that it will make a loss in the year to September 2022 and a strategic review is underway. There are also problems with poor margins in the partnership housing and housebuilding operations. There will be £19.4m of cost and design provisions related to these operations as well as £4.7m of credit loss provisions. The total loss is expected to be £37.1m. If a land sale is made before the end of the month then that could generate a profit of £25m to offset against the loss estimate. A subsidiary’s borrowings will breach their interest covenant, although management believes it can negotiate a waiver. The share buyback will be ended. Founder Stephen Wicks is retiring as chief executive and finance director Nish Malde will become interim chief executive. NAV is estimated to be 65p a share. The share price slumped by one-third to 18.25p.

Chaarat Gold (LON: CGH) has fallen % to p after a fatality at the Kapan mine. Production guidance is unaffected. The share price fell 4.15% to 10.4p.

Markets perked up in late morning trading on Tuesday, after entering Prime Minister Liz Truss finalised a £130 billion energy bills relief plan for struggling UK households, according to Bloomberg.

The FTSE 100 increased 0.3% to 7,312.6 after enduring a tough start to the week before Truss’ appointment to the UK’s highest office.

The Pound picked up after falling to a 37-year low yesterday, after news of the energy plan sent the currency rising to 1.1586 from its bottom of 1.1474.

“After yesterday sinking to a 37-year low against the dollar, the pound perked up on Tuesday, rising 0.2% to $1.1586 as the UK prepared for the changing of the guard at number 10,” said AJ Bell investment director Russ Mould.

“Reports so far suggest energy providers will be able to use government-backed loans to subsidise bills, meaning there could be some near-term relief on energy costs for consumers and businesses.”

“While not expected to be confirmed until Thursday, the messages clearly being fed in from Liz Truss’ team do help to remove some uncertainty and that has translated into a stronger day for UK stocks.”

Good news from housebuilder Berkeley sent the company to the top of the blue chip index.

The company’s shares gained 4.6% to 3,605.5p after it announced trading on track to meet its FY 2023 profit guidance of £600 million and FY 2024 guidance of £625 million.

Berkeley Group credited the strong housing market for its high performance, with persistent demand covering rising 5% to 10% cost inflation.

“Berkeley Group has put in a resilient showing, despite soaring cost inflation which is marring the entire sector. The reason profits have been left without too much bruising is because sale prices are high enough to offset the housebuilder’s fatter bills,” said Hargreaves Lansdown lead equity analyst Sophie Lund-Yates.

Taylor Wimpey, Barratt Developments and Persimmon rode the wave of renewed optimism across the housing market, with shares rising 3.8% to 108p, 3.6% to 423.5p and 3.7% to 1,505.7p, respectively.

Consumer Stocks

Consumer stocks rose as the prospect of an energy price cap freeze helped assuage fears of atrophied consumer spending over the winter season.

Investors fled consumer stocks in recent weeks on fears of lower spending due to spiking energy prices.

Next shares gained 4% to 6,280p and JD Sports Fashion shares climbed 4.3% to 128.1p.

Meanwhile, Kingfisher shares rose 3.9% to 249p and Howden Joinery picked up 3.9% to 575.1p.

“Some of the top risers on the blue-chip stock index included retailers Next and JD Sports, kitchens seller Howden Joinery and DIY store chain owner Kingfisher,” said Mould.

“These stocks have all suffered this year as earnings expectations were cut and investors priced in the likelihood of a recession. Now we might be at the stage where investors take the view that shares in retailers have been oversold, hence the big recovery rally today.”

“How long it will last is another matter, as the general cost of living crisis is still punishing for households, whether energy bills go up further or not.”

DS Smith

DS Smith shares climbed 3.1% to 271.4p after the packaging firm reported trading in line with expectations, with its savvy cost control measures mitigating rising cost inflation.

The company said it expected a “significant improvement” in business performance during FY 2023.

“We have started the financial year very strongly, despite the current macro-economic conditions,” said DS Smith CEO Miles Roberts.

“We are focusing on ensuring the highest levels of security of supply and customer service and are very pleased with the ongoing support we receive from both our customer and supplier base.”

“Whilst the industrial sector is showing some weakness, our FMCG business remains resilient.”

DS Smith trading in line with expectations, company mitigates energy cost inflationhttps://t.co/C3DIkrVIen

Shell and BP shares tumbled to the bottom of the FTSE 100, dropping 2.1% to 2,297.5p and 1.8% to 454.6p, respectively, after oil prices fell following demand fears on the US Fed’s aggressive stance to interest rate hikes.

Lockdowns in Chinese city Chengdu and continued lockdown measures in tech hub Shenzhen spurred further fears of lowered demand across the sector.

The price of benchmark Brent crude dropped 3.1% to $92 per barrel, despite a surge in prices yesterday after OPEC+ cut production by 100,000 bpd to calm market price volatility. However, the essentially symbolic move did little to stem falling prices.

Ashtead

Ashtead Group shares slid 1.4% to 4,250p after the rental equipment company announced its Q1 2022 outperformance was mitigated by rising interest costs.

The firm noted a 25% revenue growth to $2.2 billion and a 22% EBITDA climb to $1 billion, with trading confirmed in line with management expectations.

“Very strong levels of growth in sales and profits weren’t enough to drive Ashtead’s shares forward,” said Mould.

“The construction equipment rental group hit a sour note with the market by saying that better than expected performance is being offset by higher interest costs, which means there isn’t an upgrade to earnings forecasts today.”

The Pound Sterling picked up in early morning trading on Tuesday following Bloomberg’s report that new Prime Minister Liz Truss had shored up plans for a £130 billion energy relief package for struggling UK households.

The Pound rose from 1.15646 just after 06:00 to 1.15894 after Bloomberg broke the scoop, with the Sterling trading at 1.16027 in late morning trading.

Truss is apparently set to eradicate the looming 80% price cap rise to £3,548 in October, instead either freezing the current price cap of £1,971 or reducing energy costs to families across the country.

The entering Conservative leader is also set to provide a £40 billion relief package for businesses, with many small business owners likely breathing a sigh of relief, after facing an approaching winter of skyrocketing energy prices.

The Pound regained ground after its 37-year low tumble on Monday before the Prime Minister’s appointment, reaching depths of 1.1443 in morning trading due to the joint strains of a weakening UK economic outlook and a strengthened dollar.

The Pound has been picking up speed over Tuesday, however, with the potential price cap freeze providing the first light among a gloomy horizon for the country.

Liz Truss is set to announce a new £130 billion plan to freeze energy bills for UK households as the cost of living crisis sends costs soaring for families across the country.

Bloomberg reported the price tag would be spread over the next 18 months, which would see a new price cap set either at or below the current price cap of £1,971.

The energy price cap had been scheduled to rise 80% to £3,548 in October, snowing families under thousands of pounds in spiking costs.

However, the new proposal would apparently see the price cap alteration ditched.

Funding now stands as the next issue, with the Financial Times reporting that Truss is attempting to persuade nuclear and renewable energy generators to accept new 15-year contracts at fixed prices on a voluntary basis below the current rates, which tie their profits to surging gas prices.

Business secretary Kwasi Kwarteng, who has been the favourite to take on the chancellor role under the Truss administration, is allegedly seeking to fund the initiative via general tax or a future consumer bills levy.

Meanwhile, Truss is also said to be eyeing a £40 billion business relief plan to assist struggling businesses with rising energy costs.

Bloomberg said the new Prime Minister was undecided between a guaranteed unit price for companies to pay, or a percentage or unit price reduction for energy suppliers to offer firms.

Ashtead Group shares dropped 3.3% to 4,169p in early morning trading on Tuesday after its outperformance in Q1 2022 was mitigated by rising interest costs, resulting in a pre-tax profit projection in line with previous expectations.

The firm reported a 25% revenue growth to $2.2 billion from $1.8 billion the year before, alongside a 26% rental revenue increase to $2 billion against $1.6 billion.

“Our end markets remain strong and we continue to execute well across all actionable components of our strategic growth plan, Sunbelt 3.0. In the quarter, we invested $699m in capital across existing locations and greenfields and $337m on 12 bolt-on acquisitions, adding a combined 33 locations in North America,” said Ashtead CEO Brendan Horgan.

“This significant investment is enabling us to take advantage of the substantial structural growth opportunities that we see for the business as we deliver our strategic priorities to grow our general tool and specialty businesses and advance our clusters.”

“We are achieving all this while maintaining a strong and flexible balance sheet with leverage near the bottom of our target range.”

Ashtead Group confirmed a 22% EBITDA rise to $1 billion compared to $860 million, and a 26% operating profit climb to $594 million against $477 million.

The rental company highlighted a 29% adjusted pre-tax profit growth to $555 million from $437 million and a 28% pre-tax profit climb to $527 million against $416 million.

The firm noted a 33% adjusted EPS rise to 94.4c compared to 71.5c and a 33% reported EPS growth to 89.7c from 68c the last year.

“Our business is performing well with clear momentum in supportive end markets. We are in a position of strength and have the experience to navigate the challenges and capitalise on the opportunities arising from the market circumstances we face, including supply chain constraints, inflation, labour scarcity and economic uncertainty, all factors which we are convinced are drivers of ongoing structural change,” said Horgan.

“The business is performing strongly, with revenue and operating profit ahead of our previous expectations. This performance is offset by increasing interest costs and therefore, we expect adjusted profit before taxation for the year to be in line with our previous expectations and the Board looks to the future with confidence.”