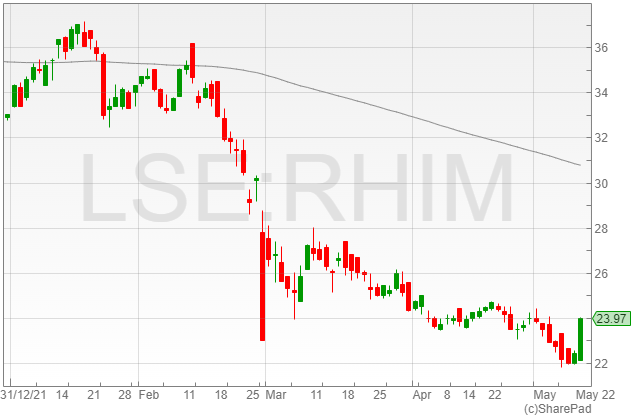

The company confirmed that it successfully passed on price increases to customers, including extra energy and freight surcharges.

Additional price increase are reportedly being implemented by the firm in a bid to offset continued cost growth.

RHI Magnesita issued a caveat that 3.5% of its revenues were based in the Commonwealth of Independent States (CIS) region, with the war in Ukraine putting the sector income at risk.

The group said it was in the process of implementing a slate of contingency measures, such as switching to alternative fuels to avoid energy supply disruption from Russian interference, and an additional capital expenditure of €6 million is set to be incurred to prepare for disruptions.

RHI Magnesita commented that its outlook estimated strong continued demand throughout its key markets over the early part of Q2 2022, underpinning confidence in the group’s outlook for the rest of the year.

The company added that further cost inflation in energy, freight, labour and purchased raw materials was being passed on to consumers in a “timely fashion.”

“In the first quarter we have successfully maintained the business momentum that we delivered in Q4 2021, with margins restored to acceptable levels as we realize the benefits of our price increase programme,” said RHI Magnesita CEO Stefan Borgas.

“Demand conditions continue to be positive, our order books remain full and we have good visibility into the second half. In the midst of ongoing volatility globally we are well positioned to benefit from cost savings in 2022 that will be delivered from our strategic investments in the optimization of our production network.”

“Further growth in new markets supported by acquisitions in Turkey and China and in our new recycling joint venture and new recycling technologies in Europe will also contribute.”

Coca-Cola HBC reported its first quarter trading update on Thursday where the group noted an increase of 24% in net sales revenue on an organic basis and a 31% rise in volumes on a reported basis as the group managed inflationary pressures and manufacturing suspensions in Russian and Ukraine which sent shares to gain 5% to 1,677p.

Strong performance was secured by effective delivery in the out-of-home channel to harness the potential of returning to markets, as well as additional shelf space in the at-home channel and faster development in e-retail.

Coca-Cola HBC said out-of-home channels regained traction as restrictions eased in certain locations across the globe supporting volume growths of 22.9% in Coca-Cola’s Adult Sparkling brands and 13.5% in Still drinks.

Coca-Cola HBC reported that its Sparkling portfolio performed well in the first quarter due to targeted campaigns and successful launch of the the new Coke Zero recipe which rose volume growth of Trademark Coke by 10.6%.

The group’s low and no sugar variants noted a 45.3% rise contributing to 27.1% of CCHBC’s Sparkling portfolio. Under Stills, the group’s Water volumes grew by 11.3% with support in all 3 markets.

Price and other revenue growth management activities accelerated revenue per case growth to 11.6% on an organic basis, as pricing remained a significant instrument that the group controlled according to plan in light of rising inflationary pressures, with no negative impact on volumes.

Coca-Cola HBC Segmental Analysis

Established Markets

Volume in established markets increased by 9.6%, driven by double-digit growth in Stills, primarily driven by Water, which benefitted from out-of-home channels gaining traction with the ease of restrictions.

Despite severe comparatives, Sparkling volumes climbed in the high single digits, while Energy volumes grew in the low twenties.

Stills volume growth grew in the mid-teens in Greece, double digits in Ireland, and in the high teens in Switzerland, owing to a solid performance by Water, according to CCHBC.

In Ireland, volumes increased by the mid-teens and Sparkling volumes increased by the low-double digits, thanks to Trademark Coke and Adult Sparkling, whereas in Switzerland, volumes increased by the mid-single digits, owing to strengthening out-of-home trends despite Sparkling volumes falling slightly.

Volumes increased by low-double digits in Italy, driven by Sparkling and Energy, while ready-to-drink tea surged by double digits as limitations were eased in February, benefiting out-of-home channels.

CCHBC benefited from price changes in all of its markets, as well as a favourable package mix and positive channel mix, as organic growth in net sales revenue per case increased by 7.9%.

On an organic and reported basis, the company’s net sales revenue increased by 18.2% and 19.5%, respectively.

Developing Markets

Sparkling volume climbed by 24% in developing markets, led by CCHBC’s great success in low- and no-sugar variations, while both Energy and Stills volumes grew by double digits.

Volumes in Poland climbed by the mid-thirties, in Hungary by the low-twenties, and in the Czech Republic by the low-double digits.

As the firm battled the sugar levy, Trademark Coke, low/no-sugar versions, and Adult Sparkling experienced a high success in Poland. In Sparkling, Hungary and the Czech Republic both had double-digit and mid-single-digit increase.

Organic net sales revenue per case climbed by 13.3%, while reported net sales revenue jumped by 40.2%.

Emerging Markets

The volume of emerging markets increased by 8.5 percent organically and by 28.8 percent on a reported basis, which incorporates Egypt’s consolidation from January.

Against strong comparables, Sparkling volumes increased by the single digits, while Adult Sparkling and Energy increased by the thirties.

Stills volumes increased by high single digits, thanks to strong performances from Water and Juice.

Russia’s volume increased by double digits in the first half of the quarter, boosted by soft comparatives and strong momentum, but Ukraine’s volume plummeted by the high twenties in the quarter.

The conflict has disrupted Coca-Cola HBC’s activities since February 24, and the group has only been selling small amounts where it was safe.

In Nigeria, volume climbed by the low double digits, with Sparkling up by the high single digits and Stills rising by the mid-teens. Predator nearly doubled volumes this quarter, indicating that energy is still performing strongly.

Despite a minor drop in Sparkling volumes, volume in Romania climbed by the low single digits. Water, on the other hand, drove a continuous rebound in Stills, which increased by high single digits.

Despite a more adverse macro background, volume performance in Egypt is moving in line with objectives; nonetheless, integration continues to move well and infront of forecasts.

Due to the consolidation of Egypt from mid-January, net sales revenue per case climbed 13.1% organically and 36.2% on a reported basis, which was only somewhat offset by the lower Russian Rouble.

Coca-Cola HBC Ukraine and Russia Operations

Coca-Cola HBC continues to put its people’s safety first, giving urgent financial assistance and partnering with the Coca-Cola Foundation and the Red Cross to deliver humanitarian aid in the region. The Coca-Cola System has pledged $15m to humanitarian aid organization across the world.

Coca-Cola HBC has ceased operations in Russia and is working to put this decision into effect in close collaboration with The Coca-Cola Company, with whom it has enjoyed a fruitful cooperation for over 70 years. As a result of this choice, the company will have a significantly smaller market presence, focusing on local businesses.

The group said organic revenue increase excluding Russia and Ukraine was 25.9%, owing to the group’s other markets’ continued excellent performance.

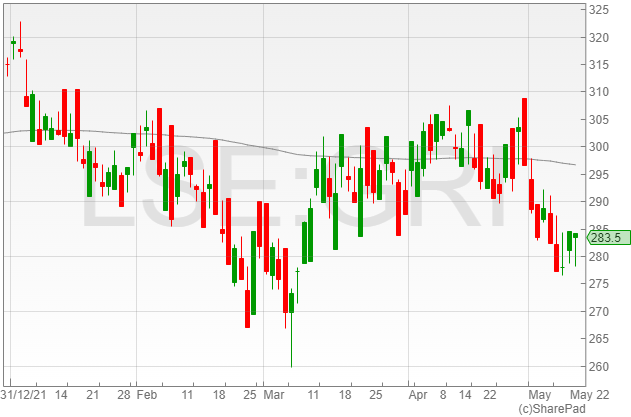

Balfour Beatty shares were down 1.8% to 236.6p in early afternoon trading on Thursday, following a slight decline in the company’s order book in its trading update for the last four months to £15.6 billion compared to £16.1 billion year-on-year.

The order book included the firm’s recently awarded £530 million Fort Meade design and construct contract in Maryland by the US Army Corps of Engineers.

The company reported that it was trading in line with management expectations, with an estimated growth in FY 2022 profits, building on its £181 million delivered by its earnings-based businesses including construction services and support services.

The construction group confirmed an average monthly closing net cash balance rise to approximately £800 million against a FY 2021 average of £671 million.

The group noted that average monthly cash was expected to come in moderately lower than the first four months of 2022 after its share buyback and a level of anticipated working capital normalisation.

Balfour Beatty further said that construction services’ operational performance remained in line with management expectations, despite disruption in Hong Kong as a result of Covid-19 restrictions.

The company’s UK construction sector is set to deliver industry standard margins of 2%-3% over FY 2022, with US construction estimated to deliver a 1%-2% margin for the complete period.

The group highlighted a margin target of 6%-8% in power, road and rail maintenance, however the company added that the sectors were performing on a slightly lower revenue base due to Balfour Beatty’s withdrawal from the gas and water sector.

The firm mentioned that its outlook included several promising asset investment opportunities for infrastructure, alongside a slate of disposals projected to kick off towards the end of HY1 2022 and continue into HY2 2022.

Balfour Beatty confirmed that it had repurchased £19 million of shares as part of its share buyback programme, with the total £150 million in shares projected to close by the end of 2022.

“We remain confident that the Group is well positioned for 2022 and beyond,” said Balfour Beatty CEO Leo Quinn.

“Our business portfolio has been transformed to focus on the growing infrastructure markets of the UK, US, and Hong Kong – each underpinned by strong government investment programmes.”

“The strength of our balance sheet and the higher quality of our order book will enable us to maximise these opportunities for profitable growth while remaining resilient to the current macro-economic challenges .”

Vast Resources is a mining and development company listed on London’s Aim that mines copper, gold, polymetallic ores in Zimbabwe and Romania.

Vast Resources has projects in both Zimbabwe and Romania such as Chiadzwa Diamond Fields located in Marange, Baita Plai and Manaila-Carlibaba facility which we will discuss in-depth later in the article.

In late April, the group announced a fundraise of £420,000 at a premium to the previous closing price to buy mechanised equipment to help the increasing mining volumes planned at the Baita Plai Polymetallic Mine.

In its latest operational update, Vast Resources noted a 236% jump in total gross revenue to £2.29m from £970,000 in the first quarter of 2022, which also included contributions from Tajikistan despite working with limited financial resources.

However, potential pipeline revenue prospects are underway in the attempt to keep the business well-funded. The group generated £1.67m in total revenues from other projects between the fourth quarter of 2021 and the first quarter of 2022.

The business is also in the process of refinancing the Atlas bond facility, while it continues to arrange concentrate sales from Baita Plai to provide additional cash flow.

Vast has a level of debt that should not be ignored but may become insignificant should the company deliver on their plans to develop, and increase production from, its portfolio of assets.

Vast Resources is a high-risk junior miner and is not for the faint of heart. However, with a market cap of just £9.3m, the adventurous may want to pay the stock closer attention.

Projects

Romania

Baita Plai

Baita Plai is located in Transylvania’s Apuseni Mountains, which is home to Romania’s largest polymetallic and uranium mines.

The mine has a complete infrastructure, comprising underground, surface, and processing equipment, as well as a fully working EU-registered tailings facility.

Baita Plai Mine focused on copper output in Q1 2022, with a 24.2% increase in tonnes milled and a 16.8% increase in Dry Metric Tonne production from the fourth quarter to the first quarter of 2022.

Mining was mostly low-grade ore during the quarter as the ramp down to sub-level 3 under level 18, which has now just intersected the Antonio skarn, was being built.

The Baita Plai Polymetallic Mine has a $107m NPV at 10%, before any improvement to the project’s economics including a possible increase in the resource and capacity at the mine. Vast

Vast Resources has a 49% of the 50% stake in Central Asia Minerals and Metals Ore Trading (CAMM) which already holds a relationship with Takob, and Vast has an effective indirect interest in the Takob Project of 24.5%.

Tajikistan Open Joint Stock Company “TALCO” is the owner of Takob which owns the operating Takob fluoride and galena mine in Tajikistan and produces the fluoride concentrate which is sold to TALCO’s chemical division for the production of essential raw materials for primary aluminium production.

The mine reported in the past that it contains 30g/t silver and 1-2g/t gold in situ and according to the deal, the mine will have an output of 7,000 tonnes of ore per month with a minimum of 1.5-2% lead, 1.2-1.4% zinc, and 27% fluoride, along with a supply of two months worth of output on-site.

The terms of the deal also state that CAMM will manage and execute the project and supply the equipment, technology, and technical experience to update and optimise the mine’s processing facility for which CAMM has acquired funding. In return, CAMM will receive 50% of net revenue from the sale of non-ferrous concentrate and precious metals.

Vast Resources will also earn a 12.25% royalty on all sales of the non-ferrous concentrate and any other metals generated for its participation in the collective group, in addition to the fees payable under the services agreement with CAMM.

Manaila Carlibaba Project

The Manaila Carlibaba project is an important project for Vast Resources. The aim is to restart the project after Baita Plai and the Chiadzwa Community Concession enter peak production levels.

The 138.6-hectare Manaila-Carlibaba exploration licence has a JORC 2012 compliant Measured and Indicated Mineral Resource of 3.6Mt grading 0.93% copper, 0.29% lead, 0.63% zinc, 0.23g/t gold, and 24.9g/t silver, as well as Inferred Mineral Resources of 1.0Mt grading 1.10% copper, 0.40% lead, 0.84% zinc, 0.24g/t gold, and 29.2g/t silver.

Vast proposes to build a larger mining and processing facility at Manaila-Carlibaba, which will eliminate the need for expensive road transport of mined ore to the existing processing facility at Iacobeni, about 30 kilometres distant and its preliminary studies suggest the prospect of a new open-pit mine to explore mineral resources to a depth of around 125 metres below the surface.

Blueberry Gold Project

Blueberry Project, is a 7.285kmsq brownfield area located in the “Golden Quadrilateral” which is in the area of the Baia de Aries mine, where Vast Resources has 29.41% interest.

Vast’s stake in Blueberry Gold Project is held through EMA Resources, which is a subsidiary company of Vast, which is expected to become a sole entity eventually to qualify for an IPO.

Vast will be in charge of future mining operations at Blueberry, as well as the exploration programme and the IPO process, in exchange for a fee of 10% of pre-IPO costs.

The Golden Quadrilateral offers strong polymetallic prospects and is said to have generated almost 55m ounces of gold in the past with soil samplings supporting sample values of up to 22.4g/t gold.

A drilling and assaying campaign is now ongoing, and it is expected to yield enough data to support an Inferred JORC Mineral Resource for gold and other polymetallic minerals such as silver, copper, lead, and zinc in one or more separate breccia pipes.

Zagra Licenses

Piciorul Zimbrului and Magura Neagra are collectively known as Zagra.

The 10km2 Piciorul Zimbrului prospecting permit is located in the Zagra-Telciu area in Bistrita-Nasaud County of Romania and lies adjacent to Vast’s 21km2Magura Neagra prospecting permit.

After the initial exploratory work, Vast completed the drilling programme in the Piciorul Zimbrului licence, focusing on six previously detected veins with linked copper and gold mineralisation along an underground route constructed for 820m at a level of 835m above main sea level.

IPEG Cluj, the former state exploration corporation, has conducted 1,200m of underground development and diamond drilling, as well as 862m of surface diamond drilling and geological mapping over a 4km region.

Vast has also begun drilling in the Magura Neagra licence, to find polymetallic veins and regions of scattered sulphide deposit.

Zimbabwe

Vast Resources signed a partnership agreement with Chiadzwa Mineral Resources which is a company that represents the Chiadzwa Community interests which led to the creation of Katanga Mining. Katanga Mining and Zimbabwe Consolidated Diamond Company also aim to enter into a joint venture and will be announced at the same time as the details of the Chiadzwa JV.

The Chiadzwa Diamond Fields in Marange is one of the richest alluvial diamond deposits worldwide.

Vast Resources Shares

Vast Resources shares have given up 10% this year and trade at just a fraction of their 2018 levels. The company is producing revenue and has a number of assets under evaluation that may provide a catalyst for a re-rating. Their financial position will need careful consideration, but the need to raise capital and refinance is common place within the sector.

The FTSE 250 and AIM tracked global equites with sharp decline following a report from the Office of National Statistics that the UK economy shrank by 0.1% in March, shaking investor confidence.

Investors were also spooked as the prospect of surging US inflation heightened fears of an economic slowdown across international markets.

“The FTSE 100 tumbled after weak UK GDP numbers and higher than expected US inflation figures stoked fears about a global economic slowdown,” said AJ Bell investment director Russ Mould.

RHI Magnesita shares increased 6.5% to 2,388p after the refractory products supplier announced an EBITDA rise of 50% in Q1 2022 as a result of continued high demand for steel and industrial products.

Grainger shares were up 0.4% to 232.3p following a profits rise to £98.8 million in HY1 2022 from £44.5 million year-on-year.

“We are delivering on our growth plans which will see us double in size in the coming years, providing exceptional earnings growth and attractive high single digit total returns to shareholders,” said Grainger CEO Helen Gordon.

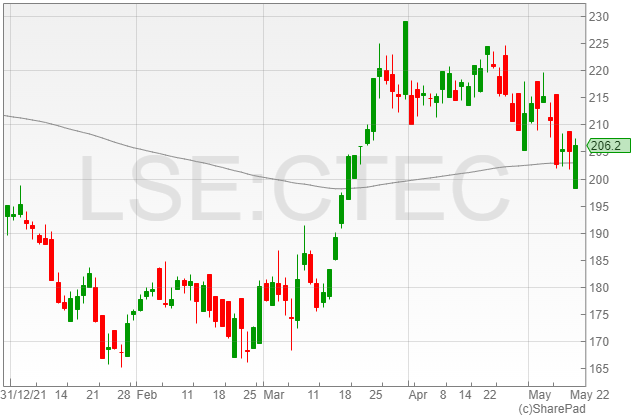

ConvaTec Group shares gained 0.7% to 206.6p after the group reported revenue for the four months to 30 April 2022 of 4.1% on a reported basis, with a 7.5% growth on a constant currency basis and a 6% rise on an organic basis.

Anglo-American is set to buy 70% ownership of the operation for an aggregate investment of up to $88.5 million, including cash consideration of up to $14.5 million.

“This agreement represents a major turning point for Arc and follows many months of negotiations. I am delighted to be signing this agreement with Anglo American which will, upon execution and completion of the definitive agreements, result in the potential for significant investment by a reputable major mining company in the tenements in north west Zambia and a very exciting time ahead for us,” said Arc Minerals executive chairman Nick von Schirnding.

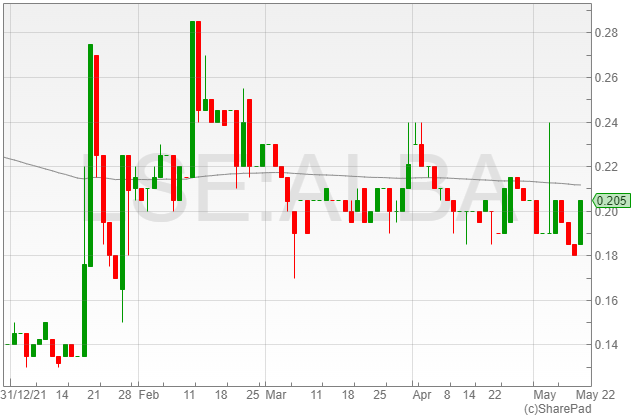

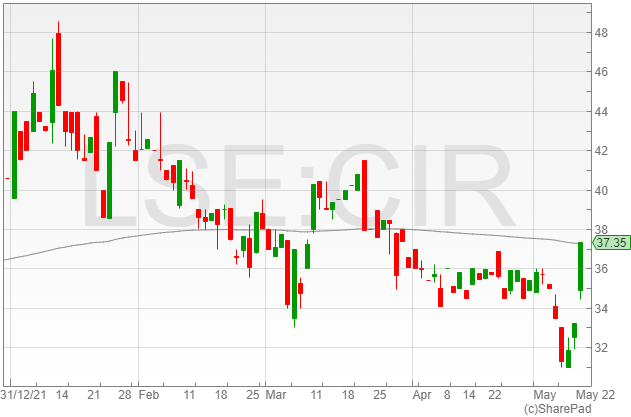

Circassia Group shares increased 12.5% to 37.3p following a reported revenue ahead of market expectations for the initial four months of 2022, with clinical revenue rising 17% year-on-year and trading growth up 23% against the same period last year.

The company said it expects its EBITDA for FY2022 to come in “materially ahead of its expectations” based on strong growth in the year-to-date.

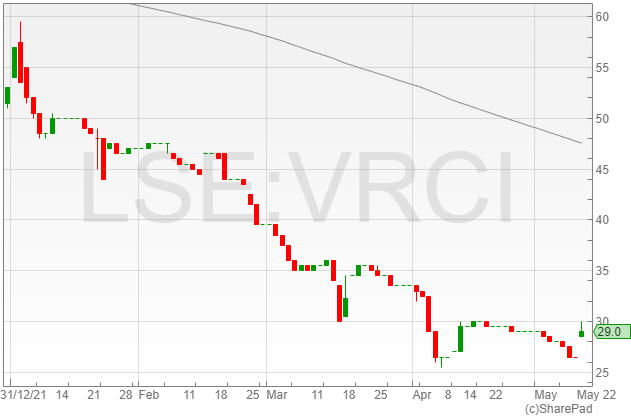

Verici Dx shares were up 11.3% to 29.5p following the successful results of its blinded, international, multi-centre validation study for blood test product Tuteva.

The product is reportedly a next-generation RNA sequencing assay, which demonstrated positive performance in detecting acute rejection after a kidney transplant.

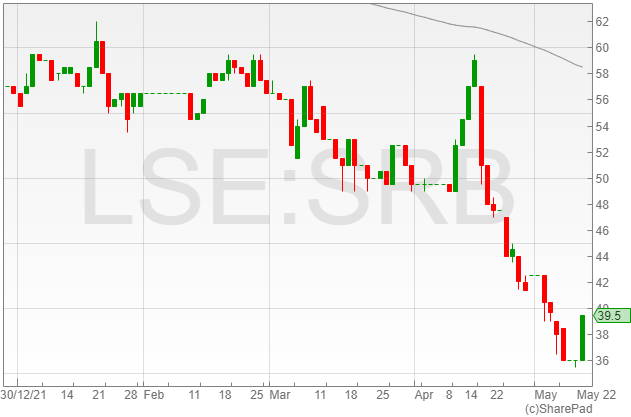

Serabi Gold shares gained 9.7% to 39.5p in light of a production of 2,919 ounces of gold from its Palito Complex, its highest level so far this year.

“It is very pleasing and a testament to the hard work of the team at the Palito Complex that we have managed to produce 2,919 ounces in April,” said Serabi Gold CEO Mike Hodgson.

“As investors will recall we experienced production challenges in the first quarter on the Julia Vein at Sao Chico, and this resulted in us moving away from sublevel long-hole mining method, for the more selective, albeit slower shrink stoping method. So it is really pleasing to see this change bearing fruit coupled with continued excellent performance at Palito.”

GreenRoc Mining shares increase 6.3% to 6.7p following the firm’s revised resource estimate for its Amitsoq graphite deposit to 5-15 million tonnes (mt) at a grade range of 18%-22% graphitic carbon (cg) compared to its initial estimate of 1.7-4.5 mt at a grade range of 24%-36%.

Serinus Energy shares plummeted 21.6% to 1.4p following a 47% plunge in production in Q1 2022.

Titon Holdings shares dropped 16.6% to 75p after the Titon swung to a pre-tax loss in FY1 2022 of £250,000 from a profit of £550,000 year-on-year.

“We are disappointed with the trading performance of the Group over the six months period to 31 March 2022, which, despite good levels of sales in the UK has resulted in a loss for the period,” said Titon Holdings CEO Keith Ritchie.

“We continue to be impacted by the constraints in supply of raw materials and components but are hopeful that some of these supply chain pressures will reduce in H2.”

Concurrent Technologies shares dropped 11.4% to 77p on the back of company warnings over component shortages impacting ship product capabilities and a subsequent expected delay in recognised revenues.

Global stock markets were rocked on Thursday as the growing threat of inflation and slow growth sent equities deep into the red.

The FTSE 100 as sank over 2% as UK GDP fell by 0.1% in March, raising fears of a global recession after US GDP contracted 0.4% in the first quarter.

“The FTSE 100 tumbled after weak UK GDP numbers and higher than expected US inflation figures stoked fears about a global economic slowdown. Investors were quick to dump commodity producers on the grounds that demand could fall in the coming months,” says Russ Mould, Investment Director, AJ Bell.

The price of oil fell 2% to $105 barrel as fears of a recession lead to oil giants Shell and BP shares falling 3% to 2,246p and 4.2% to 402p, respectively.

BP shares remained down despite the oil company making a bid for two individual offshore wind leases in the Netherlands in line with its plans to generate €2bn worth of clean energy investments in the country.

FTSE 100 Risers

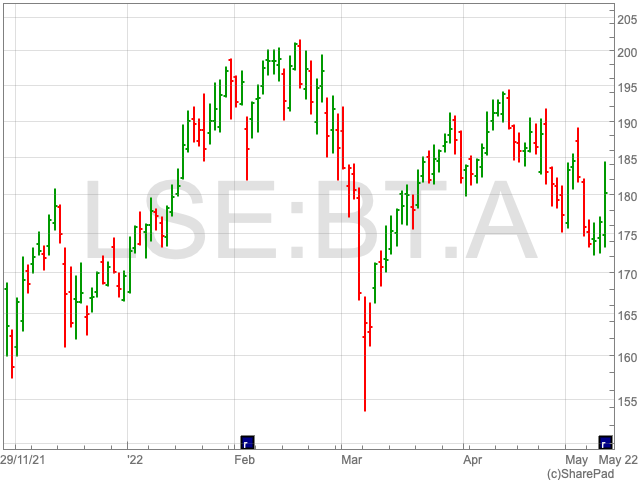

BT Group rose 0.3% to 177p after the telecommunication announced a 9% rise in pretax profit and its joint venture with Warner Bros Discovery to combine its sports broadcasting units.

JD Sports shares rallied 2.4% to 121p as the sports fashion company said it had combated supply chain pressures with a sales growth of 5% YoY in the first few weeks of its financial year, leading to the group raising its profit guidance.

“Sentiment towards JD has soured this year due to worries about consumer spending. JD’s latest trading update implies it is holding up well in a difficult market, but that wasn’t enough to win over investors, with the share price only nudging up 2% on the news,” stated Mould.

Coca-Cola HBC shares gained 1.4% to 1,620p after the company reported group revenue growth of 31% to €1.8bn with established markets up 20%, developing markets gaining 40% and emerging markets increasing 36%.

Compass Group shares were trading up 0.3% to 1,699p following its momentum gained on Wednesday when the group reported a 36% rise to £11.5bn in revenue and a 375% jump to £632m in pretax profit.

FTSE 100 Fallers

Engine maker Rolls Royce saw its shares fall 0.3% to 80.3p despite the company reiterating its guidance for the year with its YTD performance in line with management expectations.

Rolls Royce shares are “another stock struggling to get a break” even though the group reported a “reassuring trading update,” said Mould. He said “investor sentiment is poor” in a recovering aviation sector and an opportunistic defence sector, and would need a “barrage of good news to trigger a strong share price rise in the current environment.”

Mining shares tumbled on Thursday as investor confidence was shaken from commodity stocks dragging the FTSE 100. Glencore and Fresnillo shares fell 7% to 443p and 719p, Anglo American and Antofagasta shares dropped 6.5% to 3,189p and 1,325p and, Rio Tinto and Endeavour mining shares lost 5.5% to 5,067p and 1,827p.

Hargreaves Lansdown shares lost 6.7% to 834p after the group recorded a fall of 16% in group revenue in the first quarter, which was in line with management expectations. The group also stated that assets under administration for the quarter dropped by £600m due to adverse market movements.

Tech-heavy Scottish Mortgage Investment Trust shares sunk 6.7% to 729p as “investors feared portfolio company valuations would be worth less based on discounted cash flow models because of rising interest rates” according to Mould.

Not for onward distribution. Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser. This is a marketing communication. Please refer to the AIFMD Disclosure document and Annual Report of the AIF before making any final investment decisions. Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the law change. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Henderson Management S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

BP’s bids complement BP’s vast and transformative goals for a range of additional integrated clean energy investments in the Netherlands, using the company’s diverse businesses and expertise to underpin the country’s decarbonization targets.

BP has entered bidding for the rights to build sites VI and VII of the Hollandse Kust Wind Farm Zone (HKW) which is located 53km off the west coast of the nation and has two wind farm sites totalling 176 kmsq.

The bid contains an “unprecedented level of innovation”, with nearly €75m committed to improving the marine environment, supporting advanced ecosystem data analysis, and establishing a new Netherlands North Sea Offshore Wind Ecological Innovation Hub to facilitate further studies and collaboration.

Bids for Site VII will be assessed on its ability to integrate systems, and BP’s offer emphasizes connecting offshore wind power supply with adaptable demand in the Rotterdam area.

If BP wins the bids, the group proposed the integration of wind farms with 500MW electrolysis which will create 50,000 tonnes of green hydrogen per year to fulfil BP’s Rotterdam refinery requirement and 10,000 barrels per day of sustainable aviation fuel generation.

BP’s Rotterdam refinery will get a new electric-powered boiler and superheater, as well as a utility-scale battery to help with asset integration.

BP said it will also equip the wind farms with demand shifting solutions, as well as newly designed flexible electric vehicle charging stations with integrated batteries and low-carbon multi-energy logistics hubs.

Additional advanced digital grid optimisation and stability technologies will be used to match demand for electricity to the HKW wind power production as part of these initiatives and BP will create a skills incubator to help workers obtain the skills they need to work in these new sectors.

BP expects to invest up to €2bn in the decarbonization of flexible demand apart from the additions to the wind farms.

Anja-Isabel Dotzenrath, BP’s Executive VP of gas and low carbon energy, said: “Delivering a net zero future demands more than just generating renewable power offshore – we need to create an integrated energy system with renewables at its centre. We plan on doing just that in the Netherlands.”

She said the group will apply its integrated energy company strategy to meet the green energy supply with the demand in the energy system through utilising offshore wind power to electrify industry and mobility and renewable power to produce green hydrogen, to help to decarbonize hard-to-electrify sectors.

“In addition, we will deploy innovative technology in support of an unprecedented scale and scope of monitoring and analysis to create a step change in collaborative marine ecology research in line with our aim to have a positive impact on the North Sea’s ecology,” added Dotzenrath.

The Amitsoq Graphite Project is one of the highest-grade graphite deposits in the world, and was updated to a tonnage range of 5-15 million tonnes (mt) at a grade range of 18-22% graphite carbon (cg), compared to its maiden resource estimate of 1.7-4.5 mt at a grade range of 24-36% gc.

The Greenland-focused company reported a Maiden Resource estimate for the deposit on 8 March 2022 of 8.2 mt of combined and inferred JORC Resource at an average grade of 19.7% cg, providing a complete graphite content of 1.6 mt.

GreenRoc said the deposit was open along strike, predominantly to the north, and down dip in the west, with testing scheduled in the upcoming phase two drilling programme later in 2022.

The firm added that there was considerable upside potential from the undrilled Kalaaq deposit to the south of the Amitsoq Island, with a revised exploration target calculation currently being undertaken for the operation.

The company highlighted the use of graphite in Electric Vehicle (EV) manufacturing, which it pointed out as a major driving factor behind rising graphite demand and prices.

GreenRoc commented that UBS estimated a natural graphite deficit of 3.7 mt by 2030, representing approximately 37% of the global market.

The mining group confirmed that the Amitsoq graphite has the potential to be upgraded to over 99.95% pure graphite product, a specific requirement in EV battery production, which would position GreenRoc to capitalise on the international transition to net zero carbon.

“Amitsoq is one of the highest-grade graphite deposits globally, and our graphite has been shown to be amenable to the production of the high purity graphite, which is the requirement for EV batteries,” said GreenRoc interim CEO Lars Brünner.

“Our focus now is on building our Resource tonnage to a level that will support a detailed feasibility study. The current Maiden Resource of 8.28Mt at an average grade of 19.75% Cg, giving a total graphite content of 1.63 Mt, is a fantastic result but we are confident we can improve this further and in so doing strengthen the commercial value of the Project.”

“More than half of the Exploration Target area for Amitsoq Island remains undrilled and the upcoming drill programme will focus on unlocking this Resource potential. We look forward to sharing further details in due course.”

BT Group addressed a sports broadcasting joint venture with Warner Bros Discovery and noted a 9% rise in annual pretax profit in its full-year results earlier today.

BT Group reported a 2% decline in revenue to £20.85bn from £21.33bn as revenue growth from its Openreach business was offset by a fall in Enterprise and Global, while Consumer, which is its biggest unit remained flat.

The group stated its Openreach broadband infrastructure arm “continues to build like fury”.

The telecommunication company said pretax profit rose 8.8% from £1.8bn to £1.96bn as larger finance expenses were offset by increased EBITDA.

Operating costs declined 4.2% to £18bn in 2022 and the group generated gross annualised cost savings of £1.5bn and rose the target to £2.5bn to be achieved by the end of FY25.

The group’s adjusted EBITDA rose 2.2% to £7.6bn which was in line with guidance of £7.5bn to £7.7bn.

The group noted a 25% rise in Capex to £5.3bn and a 14% rise in Capex excluding spectrum summing up to £4.8bn as BT spent more money on its fibre infrastructure and mobile networks.

BT reinstated dividend payout and added 5.4p as a final dividend resulting in 7.7p as the total dividend for the year. Yearly guidance remains despite difficult economic conditions said the group.

“By bringing together the sports content offering of both BT Sport and Eurosport UK, the JV will have one of the most extensive portfolios of premium sports rights,” said BT Group.

On completion of the deal, the production and operational assets of BT Sport will become a wholly-owned subsidiary of Warner Bros, where BT will receive £93m from Warner and around £540m as an earn-out.

The partnership will also enter into a new agreement with Sky extending beyond 2030 to look after the distribution of the joint venture’s sports content.

Partnership negotiations were first disclosed by BT in February. It hoped to wrap up talks by June 30. Discovery has completed its merger with WarnerMedia, an AT&T spin-off since the talks started. Discovery+ is a streaming service.

“Brave experiment or overly ambitious folly? BT’s participation in the sports rights battle has moved to a new phase as it completes its joint venture with Warner Bros. Discovery,” said Russ Mould, Investment Director, AJ Bell.

“BT entered the fray in 2012 by securing rights to Premier League matches and made a splash a year later by capturing Champions League and Europa League games from under the nose of Sky.

“The promise of top-level sports action was seen as a way of securing subscribers for its wider TV and broadband services.”

There were various positive indications for 2022 such as low Ofcom complaints and BT’s highest ever NPS results.

BT anticipates a 4.2% rise in adjusted revenue growth and adjusted EBITDA, amounting to £7.9bn in the next financial year.

Cash flow is expected to be normalised and within the range of £1.3bn to £1.5bn, where capital expenditure, excluding spectrum work, is forecasted to be £4.8bn.

Mould added, “The results which accompanied news of the tie-up were solid enough – crucially customers seem to be sticking with BT despite the cost-of-living crisis and the company has made decent progress on the roll-out of 5G. The dividend is also in line with what was promised, and free cash flow is, critically, better than expected.”

“BT still has plenty of issues to deal with, not least the complex and costly investment in broadband infrastructure and a big pension deficit, but at least it seems to be laying the platform to address these challenges.”