Energean shares were up 4.3% to 1,360p in early morning trading on Monday, following a reported gas discovery by the company’s Athena exploration well in offshore Israel.

The discovery was made in block 12, in the A, B and C sands, with preliminary results indicating recoverable volumes of 8 billion cubic metres (bcm) of natural gas on a standalone basis.

Energean highlighted that the discovery also de-risked an additional 50 bcm of mean unrisked prospective resources across the company’s Olympus Area, which includes the Athena exploration well and undrilled prospects on Block 12, and the adjacent Tanin Lease.

The energy group said it would be actively pursuing development options for the commercialisation of the wider Olympus area, including new domestic Israeli gas sales, and export options such as developing the memorandum of understanding signed with the Egyptian Natural Gas Holding Company to supply up to 3 bcm per year into a binding contract.

The firm clarified that the economics of gas extracted and sold from block 12 were not subject to royalties payable to the original sellers of the Karish and Tanin leases, which would lead to an estimated 8% revenue growth for the same volumes sold in comparison to the Karish and Tanin discoveries.

“We are delighted to announce this new gas discovery at Athena and the potential of the wider Olympus Area. We are considering a range of strategic commercialisation options both for a standalone and wider Olympus Area development, including domestic and multiple export routes,” said Energean CEO Mathios Rigas.

“This discovery and the broader de-risking of a number of prospects in the Olympus Area reaffirms the role of the East Mediterranean as a global gas exploration hotspot. It strengthens our commitment to provide competition and security of supply to the region, enables the optimisation of our Israel portfolio and fulfils one of our key milestones for 2022.”

Shaftesbury and Capital & Counties Properties’ (Capco)Boards of directors have taken note of recent news speculation and confirmed that they are in advanced talks over a possible all-share merger on Monday.

Shaftesbury and Capital & Counties’ potential merger would result in a REIT centred on London’s West End, with a portfolio of 2.9m sqft of lettable space in high-profile locations such as Covent Garden, Carnaby, Chinatown, and Soho.

The combined ownership would include 1.8m sqft of retail and hospitality space, as well as 1.1m sqft of commercial and residential space.

According to the proposed terms of the probable merger, Shaftesbury shareholders will own 53% of the new firm, minus the Shaftesbury shares acquired by Capco, and Capco shareholders will own 47% of the combined company.

Capco now owns 97m shares in Shaftesbury, or about 25.2% of the company’s existing share capital, including 38m shares held as security for Capco’s exchangeable bond.

Jonathan Nicholls, Chairman, and Ian Hawksworth, CEO, will oversee the united firm with a defined governance and leadership structure. The CFO will be Situl Jobanputra, while the COO will be Chris Ward.

Norges Bank, a substantial shareholder in both Shaftesbury and Capco, recognises the strategic reason and has expressed its willingness to support a merger in the future, subject to a review of the final terms and conditions of any transaction.

The talks are still underway, and the terms of a potential merger have not been settled. It is impossible to predict whether or not a bid will be received.

The proposed merger is currently planned to be structured as a Capco acquisition of Shaftesbury, subject to terms being finalised.

As a result, the Takeover Panel have agreed that Shaftesbury will be considered as the offeree and Capco will be treated as the offeror for the purposes of the code until further notice.

In connection with the potential merger, Evercore and Blackdown Partners are giving financial assistance to the Shaftesbury Board and Liberum Capital is serving as Shaftesbury’s corporate broker.

In accordance with the potential merger, Rothschild & Co is offering financial guidance to the Capco Board and Capco’s corporate brokers include UBS, Jefferies, and Peel Hunt.

Capco must either announce a firm intention to make an offer for the company or that it does not intend to make an offer by 5.00p.m. on 4 June 2022.

Shaftesbury shares fell 3.9% to 555p and Capital & Counties Properties shares dropped 6% to 155p on news of the possible merger.

Victrex reported a mixed slate of results in its HY 2022 update, including an 8% increase in group sales volume to 2,264 tonnes compared to 2,087 tonnes year-on-year, as a result of double-digit growth in electronics, energy and industrial and VAR.

The company also highlighted a recent improvement in its automotive sector, despite disruptions in its semiconductor chip supply chain, and a 12% uptick in medical revenue with the return of elective surgeries, with a 6% increase in the firm’s core application growth pipeline.

The polymer solutions group announced a 6% growth in revenue to £160.1 million against £150.9 million, alongside a 4% uptick in gross profit to £85 million from £81.4 million.

Victrex mentioned an 80 bps decline to 53.1% compared to 53.9% in the company’s gross margin, with a reported pre-tax profit fall of 6% to £43.6 million against 46.6 million, reflecting a one-off expensed ERP software implementation.

The firm’s earnings per share fell 7% to 43.5p compared to 46.9p since HY1 2021, with an announced dividend per share remaining flat at 13.4p.

Victrex highlighted advances in its polyether ether ketone (PEEK) business for its HY2 2022 outlook, alongside a projected increase in volume growth and a focus on year-on-year revenue growth.

The high performance materials firm added that its gross margin was estimated to decline in the next half year, as a result of currency movements.

The company said its mitigation plans for recovering additional inflation were making good progress, however it caveated that the group remained mindful of the changing global environment going into the remainder of 2022.

“Our attractive and differentiated portfolio includes sustainable products which bring environmental and societal benefit and, reflecting the value PEEK brings to customers, our core application growth pipeline increased by 6%,” said Victrex CEO Jakob Sigurdsson.

“Whilst volumes were strongly ahead and our initial price recovery programme is delivering on plan, we have faced further unprecedented energy, raw material and distribution inflation, as well as FX headwinds.”

“Thanks to significant improvement in operating efficiency and better asset utilisation, first half margin was broadly stable, despite the additional cost inflation, which we are well placed to recover. Without these additional cost headwinds, margin would otherwise have improved closer to our target level.”

Victrex shares were down 3.8% to 1,728p in early morning trading on Monday.

NCC Group announced the appointment of a new CEO, Mike Maddison, and provided a trading update, where the group expects revenue to be significantly better than H1 2022 and H2 2021, on Monday.

NCC Group, a global cyber security firm announced the appointment of Mike Maddison as CEO, following Adam Palser’s decision to step down after more than 4.5 years on the job.

Mike will begin serving on the Board on August 1, 2022. Adam will stay on as CEO until mid-June and will be available to help with the transition. Chris Stone, Non-Executive Chair, will take over as Executive Chair for the 6-week interim period.

Chris Stone, Chair, said, “Meanwhile I am delighted that someone with Mike’s knowledge of the cyber security markets and impressive track record has agreed to join us.”

“With his skills I am confident that NCC Group will be able to build on the momentum it is already seeing across its markets, providing clients with the support and peerless technical knowledge they need in these enormously uncertain times.”

NCC Trading Update

On a constant currency basis, the Board anticipates revenues in H2 of 2022 to be significantly greater than the prior-year period and H1 2022, due to the purchase of IPM and the acceleration of Assurance revenue growth.

NCC Group’s revenue and adjusted EBIT are expected to meet management’s estimates for FY22 and increased volumes and day rates are expected to keep the revenue momentum going into FY23, according to the Board.

The Assurance division is doing well, especially in North America and the United Kingdom and expects H2 revenue growth to be 15% compared to 8.8% in H1 FY22 due to higher volumes in its core business, progressive increases in day rates, and new growth offerings such as Sentinel and Remediation.

NCC paid £3m for Adelard and its assets in April 2022 as its services complement those of NCC since Adelard is a high-value critical system assurance expert.

In H2 FY22, NCC’s Software Resilience business, excluding IPM, is expected to generate revenue again.

In June 2021, NCC purchased IPM for $220m, and the first year’s results have been good and in line with management forecasts.

The company has just begun a complete operational evaluation of its integrated Software Resilience business, which is expected to identify possibilities to increase the NCC’s operating contribution by an estimated £5m through a series of management initiatives, with the entire impact expected in FY24.

NCC expects to release its audited preliminary results for FY22 on September 6, 2022.

Kendrick Resources was formerly AIM-quoted BMR Group, and it has had many other previous names, such as Berkeley Mineral Resources, Tecteon and Dominion Energy. The operations were originally mining, then oil and gas, technology before returning to mining. It left AIM in August 2018 after problems with the progress of the Kabwe project in Zambia, which was then owned by a joint venture with Jubilee Metals (LON: JLP). Alex Borelli was chairman at that time. Jubilee now has full control of Kabwe and Kendrick as a 11% royalty interest.

The company’s Scandinavian assets were acquired from Pursuit ...

Trident Royalties had a monumental start to 2022, with a material increase in revenue demonstrating the long-term potential for the mining royalties company.

Trident Royalties revenue grew 396% to US$2,234,988 in the first quarter, when compared to the same period a year ago. Trident’s Q1 2022 revenue was a 496% increase vs Q4 2021.

The sharp rise in revenue can be attributed to the introduction of revenue from the gold mining royalties that added US$1,577,958 to the quarters top line.

“This has been an excellent start to the year for Trident. Completion of the gold offtakes acquisition coupled with positive advancements at several portfolio assets has significantly enhanced the quality of our portfolio,” said Adam Davidson, Chief Executive Officer of Trident.

“Most notably, Trident’s year-on-year quarterly revenue has increased by almost 400%, with increasing internal cash generation providing us with further flexibility for financing and acquisitions.”

Mining royalties allow Trident to capture the upside of rising metals prices and increased production, without additional capital expenditure.

Trident Royalties progress

Trident also noted progress at the Thacker Pass lithium project which, having received all environment permits from the Nevada state, is now set for the final Federal Record of Decision in Q3 of this year. Thacker Pass is the largest lithium deposit in the US.

The Koolyanobbing iron ore mine recommenced production in Q1 2022 and the Mimbula copper mine royalty earned Trident $500,000 in the period.

“The progress in our assets demonstrates the success of our strategy and the importance of selecting the right assets and operating partners,” Davidson said.

“In addition, we have continued to deliver on growth, with three transactions announced or completed during the quarter. We are confident regarding our outlook, with a strong pipeline of value accretive opportunities across a range of commodities and geographies.”

Petards (Aim: PEG) 13p, Mkt Cap £7m, announced its finals to end December 2021 showing a jump back to a PBT of £0.87m from a loss of £0.53m. PEG, formerly part of Vickers, are a long established- developer of advanced security and surveillance systems initially for rail OMEs, which has become very competitive so increasingly are focused on road transport, and defence clients which significantly reduces the risk profile. Its revenue improved to £13.6m from £13m and reported an order book of £7m and that progress is continuing.

The eye Train order book for its software dri...

“Concern about inflation is the culprit, as ever, and the wild swings we’ve seen this week are a reminder that sentiment is about as fragile as a porcelain doll,” said AJ Bell investment director Russ Mould.

“The other fear is that the cure for inflation, higher rates, could be as bad as the disease if they choke off growth and even lead to recession.”

4imprint Group shares gained 18.6% to 28,950p as the company raised its outlook for 2022 beyond market expectations to revenues of $1 billion.

“New customer acquisition has remained encouraging, and the retention statistics reliably reflect the growing customer file,” the group said in a statement.

Beazley shares rose 5.2% to 427.8p after the insurance firm announced a 27% increase in gross premiums to $1.2 billion and a 17% rise in premium rates on renewal business in its Q1 2022 update.

“The year has started well with gross premiums written increasing by 27% and growth slightly ahead of our expectations across all divisions,” said Beazley CEO Adrian Cox.

SDI Group shares increased 12.5% to 170p following projections that the company would beat market consensus in its annual profits, with an anticipated revenue rise of 40% to £49 million from $35.1 million the previous year.

The firm reported an estimated pre-tax profit increase of 42% to £10.5 million compared to £7.4 million in 2021 and commented that it expected 2023 to be its best year on record.

“We have executed again on all facets of our buy and build strategy, delivering record performance in FY2022 and setting up what looks like another record year in FY2023,” said SDI chair Ken Ford.

Kinovo shares tumbled 46.3% to 18.2p following the company’s loss incurred from the sale of its DCB business.

The firm announced a pre-tax loss of £5 million as a result of the disposal, with the group forced to provide unanticipated working capital support of £3.7 million, and confirmed it expects the amount to increase in the short term.

“Whilst we have incurred a loss on the disposal of DCB, it streamlines our operations and allows us to focus on our core activities of compliance and regulatory work,” said Kinovo CEO David Bullen.

The main UK index slumped on Friday as the FTSE 100 was trading down 1% to 7,424 on the back of concerns over rising interest rates and surging inflation could damage economic growth.

However, rising oil prices were good news for BP and Shell, as it supported the companies’ shares to gain 2.3% and 1.5% to 428p and 2,327p respectively.

The rise in HPI for April marked the 10th consecutive monthly rise in the longest run since 2016.

Halifax also said that rising interest rates and tight household budgets are set to hamper the market in the coming years, which may have resulted in investors fleeing from housing development stocks on the FTSE 100.

Russ Mould, Investment Director, AJ Bell stated, “Despite a 10th consecutive month of growth for house prices the mood music around this number is definitely subdued with growth at least starting to slow and warnings that rising rates and inflation will soon dent demand. The property market may finally be about to be reacquainted with gravity.”

Persimmon, Berkeley and Taylor Wimpey shares were trading down 2% to 2,054p, 1.9% to 4,040p and 1.8% to 124p respectively.

REIT shares fell too, with Segro, Land Securities and British Land shares losing 4.8%, 2.1% and 1.5% respectively.

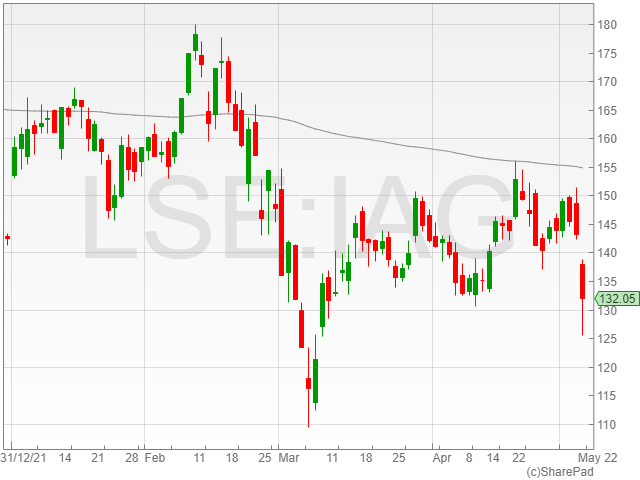

International Consolidated Airlines

International Consolidated Airlines shares plummetted 8% to 132p as the airline company missed market forecasts in its Q1 results despite recovering demand.

IAG reported a post-tax loss of €787m, which decreased from €1.07bn in Q1 2021, as the group noted a 3x fold in total revenue to €3.44bn from €968m.

“After the chaos of the past two-and-a-bit years, most households would love to have a break from everyday life and enjoy a taste of paradise. Travel companies have been patiently waiting for the day when bookings went up and Covid-related restrictions faded away,” said Russ Mould.

“We’re now edging towards this point in many parts of the world. Unfortunately, there’s a new stumbling block in the form of a potential recession.

However, IHG did report a 61% rise in revenue per available room, which is a key metric in the hotel industry in its first-quarter trading update.

“InterContinental Hotels is seeing the average rate per available room creep up versus a year ago and demand has been strong,” added Mould.

“Were it not for the pain of inflation, these travel companies would be singing from the rooftop. As it stands, both still face a fragile trading period ahead and it could be a while before they reach pre-Covid levels of business.”

Mining shares dragged the FTSE 100 down as Glencore, Rio Tinto, Antofagasta and Anglo American all saw their shares fall between 0.2% to 2% on Friday.

The Bank of England (BoE) raised its interest rates to 1% on Thursday. What does the future hold for Lloyds share price as interest rates increase?

Lloyds is the largest mortgage lender in the United Kingdom and Lloyds share price has been erratic since the Bank of England decided to raise interest rates to combat inflation. However, investor may be concerned that future rate hikes may exacerbate the present cost-of-living problem and reduce the number of mortgages taken out, hurting Lloyds’ bottom line.

Mortgages

Lloyds has benefited from a rising property market as the UK’s largest mortgage lender, while higher interest rates mean bigger margins.

While higher interest rates usually mean more money in the bank, more expensive mortgages should keep the property market cool. Recent housing data, fortunately for Lloyds, has shown great strength.

Russell Galley, Managing Director of Halifax, said, “Housing transactions and mortgage approvals remain above pre-pandemic levels, and the continued growth in new buyer inquiries suggests activity will remain heightened in the short-term.”

Given the way investors are continually looking ahead, there’s a risk that this bubble may explode shortly.

Loans

Higher interest rates are beneficial to banks because they allow them to earn more money from the money they lend out.

However, there is always the possibility that if interest rates rise too high, banks may suffer a net negative effect due to consumers borrowing less or defaulting on loans which would lead to pressure on Lloyds’ bottom line.

Lloyds has set aside £178m to cover any customer defaults, according to its most recent Q1 results and since Q4 2021, the share of stage 2 and 3 loans has grown. These are debts whose credit quality has deteriorated dramatically and which may not be repaid.

The company posted pre-tax profits of £1.6bn, exceeding analyst expectations of £1.4bn, however, recorded a decline from £1.9bn in 2021.

Lloyds associated the drop to a £177m charge that it said would safeguard it from inflation-related defaults.

The full-year results from 2021 were also quite promising despite a pre-tax profit which fell just short of experts’ expectations at £6.9bn.

However, FY21 results reported a 9% rise in net income to £15.8bn and a 4% increase in underlying net interest income to £11.1bn.

Outlook

Nonetheless, Lloyds is cautious yet hopeful about the British economy, expressing optimism in its first-quarter results.

Its interim management statement forecasts a 30% gain if the BOE interest rates remain below 1.39% and inflation remains at 7.6%. However, the central bank itself anticipates inflation to peak at 10% later this year.

Lloyds Shares Valuation

The banking group’s shares have a 4.5% dividend yield which is appealing, but that doesn’t change the fact that Lloyds has a track record of underperformance.

Lloyds has a P/E ratio of just 5.7 and a forward P/E of 6.9. That’s a pretty low valuation, especially for a company with significant long-term growth potential.

Unfortunately, Lloyds is still being dogged by a risk premium caused by the financial crisis as investors chose to value banks on their book values rather than the prospects of future earnings.

Nonetheless, brokers have set price goals that are significantly higher than the current 43p share price, and Morgan Stanley recently maintained its 62p price objective.

The targets set by brokers confirm optimism around Lloyds share price, and the move by the BOE could see upside revisions as analyst price in the benefits of higher net interest margins.

Lloyds shares were trading down 1% to 43.5p on Friday afternoon trading, however, YTD the share price has dropped 12.7%.