The UK Investor Magazine Podcast is joined by Alan Green to focus on Lloyds shares, GSK and two London IPOs.

Lloyds released its quarterly trading update which alluded to a slowdown in profit from Q4 2021. We discuss their dividend and what it will take for the Lloyds share price to break through 50p and back up towards 70p. With Net Income dipping from Q4 2021, there is also consideration paid to the impact of actions at the Bank of England to Lloyds shares in 2022.

Despite cutting their full year dividend by 35%, GlaxoSmithKline produced a bumper 32% increase in sales in Q1 2021. Given the strong revenue growth, high valuation and reduced dividend, we question whether GSK is now a value, growth or income stock.

We also look at two upcoming London IPOs in Lift Global Ventures and SpectrumX.

Lloyds (LON:LLOY), GlaxoSmithKline (LON:GSK) and Lift Global Ventures (LON:LFT).

Persimmon shares were down 2.3% to 2,129p in late morning trading on Wednesday, after the housing firm reported rising cost pressures and a lowered level of outlet completions in its Q1 2022 trading update.

The group confirmed that completions would fall short of 2021 levels, and that the timing of outlet openings would result in them being weighted in H2 2022.

However, the company mentioned that private sales reservation rates in the current period increased 2% on 2021 levels, as consumer demand for new build homes continued to outstrip supply and mortgage availability stayed high.

“Persimmon are the second housebuilder this week to point out demand for UK houses remains strong, following Taylor Wimpey’s positive outlook yesterday,” said Hargreaves Lansdown equity analyst Matt Britzman.

The group noted that it was on track to deliver full-year volume growth of 4-7% while maintaining margins, estimating that price growth would mitigate rising levels of building cost inflation.

“Persimmon continues to perform well. We are currently trading in line with expectations, demand remains strong, our private average sales rates are 2% higher year on year and we have a robust forward order book of £2.8bn,” said Persimmon CEO Dean Finch.

“As expected, reflecting the profile of outlet openings, we anticipate that completions this year will be weighted towards the second half, with first half completions being lower than those delivered in the first half of 2021.”

“We continue to expect to deliver volume growth for the full year 2022 of around 4-7% of 2021 levels, with resilient industry-leading margins.”

Persimmon’s £2.8 billion order book represented a decline from its £3 billion result the previous year, along with a £75 million commitment set for the group’s initiative to strip its properties of flammable cladding more than three years after the Greenfell fire disaster.

“As is the case with most of the major housebuilders, the group’s signed the government’s fire safety pledge to fix cladding issues. For Persimmon, unlike many of its peers, the previously set aside £75m is expected to cover the full costs of remedial work so no extra costs are expected,” said Britzman.

Persimmon is set to pay out a dividend of 110p on 8 July 2022, following the firm’s 125p dividend distributed in April.

GlaxoSmithKline reported a 32% rise in revenue in Q1 and noted higher quarterly profit as it announced it is on track to demerge and list its consumer healthcare arm Haleon on Wednesday.

Specialty Medicines recorded £3.1bn which made up almost half of the Commercial Operations £7bn contribution. The segment saw a 98% rise which was driven by consistent growth in all therapy areas including sales of Xevudy. The sale of Xevudy amounted to £1.3bn for GlaxoSmithKline.

Vaccine turnover increased by 36% to £1.66bn, led by Shingrix which is a shingles vaccine for adults aged 50 and over, in the US and Europe, reflecting robust performance and the advantage of a favourable comparative in Q1 2021, when sales were hit by COVID-19-related disruptions in numerous markets and decreased Centers for Disease Control purchases.

GlaxoSmithKline’s General Medicines generated £2.34bn, up 2%, thanks to Trelegy’s growth in all regions, the antibiotics market’s recovery, and the benefit of a favourable prior period returns and rebates adjustment, which helped to offset the impact of generic competition in the US, Europe, and Japan.

The remaining £2.6bn of the group’s revenue came from Consumer Healthcare which rose 14%.

GSK consumer healthcare will become Haleon in July, leaving a biopharma-focused ‘New GSK,’ according to the company’s demerging plans. Since early 2020, the separation has been in the works.

Sensodyne toothpaste, Panadol & Advil pain relievers, and Centrum vitamins will all be available at Haleon.

GlaxoSmithKline’s total operating profit rose 65% to £2.8bn compared to £1.69bn in Q1 2021 which included an upfront settlement from Gilead of £924m.

GlaxoSmithKline will propose a 14p quarterly dividend, down from 19p in the first quarter of 2021.

GSK aims to announce a 27p dividend for the first half-year under its new dividend policy, with 22p going to the new GSK and 5p going to consumer healthcare, soon to be Haleon.

GlaxoSmithKline 2022 Outlook

In 2022, GlaxoSmithKline estimates adjusted operating profit growth of 12% to 14%, excluding any contribution from Covid-19 solutions. GSK stated that the company intends to continue delivering on its strategic priorities.

Covid-19 solutions will generate similar sales in 2021, “but at a substantially reduced profit contribution due to the increased proportion of lower margin Xevudy sales,” according to the pharmaceutical company.

Xevudy is a Covid-19 antibody medication developed by GSK in collaboration with Vir Biotechnology, a San Francisco-based immunology business, however, it is no longer allowed for Covid-treatment in any US region due to the surge of the Omicron BA.2 sub-variant.

Emma Walmsley, Chief Executive Officer, GSK said, “We have delivered strong first quarter results in this landmark year for GSK, as we separate Consumer Healthcare and start a new period of sustained growth.”

“Our results reflect further good momentum across specialty medicines and vaccines, including the return to strong sales growth for Shingrix and continuing pipeline progress. We also continue to see very good momentum in Consumer Healthcare, demonstrating strong potential of this business ahead of its proposed demerger in July, to become Haleon.”

GlaxoSmithKline shares gained 1.15% to 1,774 after the company reported strong financials in its Q1 results.

Sebastian Skeet, Senior Analyst for healthcare sector companies at Third Bridge said, “With a consumer division split off set for July, GSK’s biggest task is to restore investor confidence in their pipeline.”

“All eyes will be on the guidance GSK will issue alongside Q2 results, and how the post-Hal Barron pipeline will tackle the patent cliff edges set for 2028.”

“Key revenue driver Shingrix’s performance was encouraging, with management seemingly upbeat on its prospects, although recent data points to prescription levels still significantly below pre-pandemic volumes. Longer term, mRNA vaccines pose a threat following Pfizer and BioNtech announcing a shingles collaboration earlier in the year.”

Lloyds shares were up 2% to 46.8p in early morning trading on Wednesday, following a positive Q1 update from the company with a 12% increase in net income to $4.1 billion compared to £3.6 billion in Q1 2021.

The firm reported a £1.2 billion statutory profit and against £1.4 billion in Q1 2021 on higher net income and a limited underlying impairment charge versus net credit the previous year.

The company also reported an underlying net profit before impairment increase of 26% to £1.9 billion against £1.5 billion, driven by high net income growth.

The banking firm’s asset quality remained strong, with an underlying impairment of £200,000 reflecting a low incurred charge and restricted impact from revised economic outlook, including higher inflation offset by higher house prices and lower unemployment.

“In the first three months of 2022, we delivered solid financial performance, with strong income growth and capital build,” said Lloyds CEO Charlie Nunn.

“These results demonstrate the consistent strength of our business model.”

The financial giant beat the stormy economic forecast with a £3.2 billion rise in loans and advances to customers at £451.8 billion over Q1 2022, and a £1.7 billion increase in its mortgage book to £295 billion despite rising inflation and surging house prices.

“For banks there is always the risk that a deterioration in economic health could hurt consumer loans businesses and see bad debt pile up, but for now Lloyds Bank is galloping away from these worries,” said Hargreaves Lansdown senior investment analyst Susannah Streeter.

“Despite the uncertain terrain ahead, it’s seen limited impact from the tougher outlook, with the housing market still super-bouyant and unemployment low.”

“While other companies take a sharp intake of breath about more aggressive monetary policy, it’s a boon to banks like Lloyds given rising rates lift net interest margins.”

Lloyds confirmed a higher net interest and a rise in other income, along with low operating lease depreciation as contributions to its increase in revenue.

Lloyds mentioned a £4.8 billion increase in customer deposits to £481.1 billion, with continued inflows to the company’s brands, along with a loan to deposit ratio of 94% providing the group with robust funding and liquidity.

The bank further noted a strong capital build of 50 basis points, which allowed for a boost in accelerated pension contributions, comprising the full 2022 fixed contributions along with 50% of the variable element.

The financial group noted a CET1 ratio of 14.2%.

Lloyds also said it would be enhancing its 2022 guidance for banking net interest margin and return on tangible equity, with banking net margin expected to hit over 270 basis points and the return on tangible equity projected in excess of 11%.

The company predicted operating costs of £8.8 billion on the new reporting basis and asset quality ratio at 20 basis points, with risk-weighted assets at the close of 2022 estimated to be £210 billion.

“Whilst we are seeing continued recovery from the coronavirus pandemic, the outlook for the UK economy remains uncertain, particularly with regards to the persistency and impact of higher inflation,” said Nunn.

“We are proactively contacting customers where we feel they may need assistance and will continue to help with financial health checks and other means of support. We encourage customers, where affected, to get advice early and talk to us.”

Mogford is scheduled to step down from the position in early 2023, after 12 years with the water and wastewater firm.

The group confirmed its appointment of Customer Service and People Director Louise Beardmore as United Utilities’ next CEO, who is set to support Mogford in his role until he officially steps down and retires from United Utilities next year.

The company said that Beardmore would join the Boards of the group as CEO designate on 1 May 2022, and added that she is set to lead the creation of the firm’s PR24 business plan which will cover the next five-year regulatory period.

“It has been a real honour to lead such a wonderful team that has succeeded on so many fronts,” said Mogford.

“We’re acutely aware of the important role we play within our North West community and Louise embodies all of the values to which we aspire.”

“With her boundless energy and commitment, I have no doubt she will lead United Utilities to even greater success.”

Beardmore has extensive experience across the utilities sector, and has worked in regulated and non-regulated environments in the UK and across the global markets.

“I am privileged to have been asked to lead an organisation that cares passionately about the essential service we deliver to seven million people in the North West,” said Beardmore.

“I look forward to working with the team to ensure we continue to provide the service and results our customers and stakeholders deserve and expect; a business where colleagues are proud to work and an organisation that is recognised as delivering for all communities in our region.”

WPP reported revenue less pass-through costs increased 9.5% to £2.57bn on a like to like basis in Q1 2022, leading the company to increase its expectation of full-year growth from “around 5%” to 5.5%-6.5%.

The advertising and marketing firm reported a rise in revenue of 8.1% on an LFL basis to £3.09bn.

WPP Top 5 Markets

The company’s top five markets in Q1 in terms of the LFL revenue less pass-through costs growth were the USA, UK, Germany, China, and India.

Like-for-like revenue, excluding pass-through costs, increased by 8.7% in North America. GroupM, Hogarth, and Brand Consulting drove +8.9% growth in the United States.

Landor & Fitch, H+K, AKQA Group, and Hogarth were the best performers in the UK, with like-for-like revenue less pass-through costs up 8.1%.

Like-for-like revenue in Western Continental Europe increased by 8.9% excluding pass-through charges. Germany, Denmark, and Spain all did well, although France, Italy, and the Netherlands took longer to recover.

Like-for-like revenue less pass-through costs increased 11.9% in Asia Pacific, Latin America, Africa & the Middle East, and Central & Eastern Europe.

Latin America, led by Brazil, experienced the most rapid increase. The Asia Pacific region expanded by double digits as well, thanks to strong performances in China and India.

WPP Top Business Sectors

WPP’s top business sectors in Q1 in terms of the LFL revenue less pass-through costs growth were Global Integrated Agencies, Public Relations and Specialist Agencies.

Global Integrated Agencies’ like-for-like revenue less pass-through expenses increased by 8.6%, with GroupM accounting for about 36% of WPP revenue less pass-through costs, which increased by 12.8% in the first quarter.

Global Integrated Agencies was up 5.6% excluding GroupM, with Hogarth being the best performer.

Despite a solid prior period, AKQA Group, Ogilvy, and Wunderman Thompson all saw significant growth, and VMLY&R did as well.

Like-for-like revenue less pass-through costs increased 14.1%, continuing the robust trend of the previous 18 months.

H+K, BCW, and Finsbury Glover Hering, which has now merged with SVC, all grew by double digits on a like-for-like basis.

Specialist Agencies’ revenue increased by 13.0%, continuing a trend that began in 2021 and despite a very strong preceding period. The majority of the larger agencies grew by double digits on a like-for-like basis.

Contracts

WPP experienced great growth across all business sectors and geographies, with strong client demand for its integrated offering which amounted to £1.8bn in new contracts.

WPP has extended its relationship with Mars as their global media partner, added digital to our Sky media remit, won the global creative account for JDE Peet’s, and been named strategic communications partner by Migros, with a focus on commerce strategy, data, and content, in new business reviews so far this year.

It also landed new contracts with Samsung and Square.

WPP Developments

WPP led the holding company rankings for media and effectiveness in 2022, while MediaCom, Mindshare, and Ogilvy were all ranked first in their respective areas.

WPP launched Everymile, a new digital commerce managed service that will provide brands with a fully outsourced direct-to-consumer (DTC) e-commerce solution, this week.

The Metaverse Foundry, a global workforce of over 700 individuals devoted to providing brand experiences for clients in the metaverse from concept to execution, was unveiled by Hogarth, WPP’s speciality global creative content production company, in February.

Essence and MediaCom will unite to become EssenceMediacom, a new agency offering that combines Essence’s digital and data-driven methodology with MediaCom’s scalable multichannel audience planning and strategic media capabilities, the company announced yesterday.

WPP is also forming GroupM Nexus, the world’s top media performance organisation, by combining Finecast, Xaxis, and GroupM Services, GroupM’s global community of activation professionals.

Mindshare will also finalise its merger with Neo, a worldwide performance agency.

Mark Read, Chief Executive Officer, WPP, said, “The year has started very well with continued momentum from 2021 resulting in strong growth across all businesses and regions. Demand is strong for our services, particularly in digital media, ecommerce, data and marketing technology.

“We continue to see strong demand for our services from our clients and to invest in the many opportunities for growth driven by the digital transition, including Choreograph and the recent launch of Everymile.”

“As a result of a strong first quarter, we now expect our growth to be in the range of 5.5% to 6.5%, up from around 5% at the start of the year. We remain very mindful of the impact of the broader macroeconomic environment on our business and will respond quickly to any changes as the year progresses.”

Fresnillo shares were up 2.4% to 791.3p in early morning trading on Wednesday, following a 5.1% increase in silver production compared to Q1 2021 and flat rate of gold production against Q4 2021 of 149.8 koz.

The mining group mentioned a 34.4% drop in attributable gold production compared to Q1 2021, due to an expected lower volume of ore processed and ore grade at its Herradura mine.

Fresnillo commented that its boost in silver production came as a result of a higher contribution of ore from its Juanicipio plant, however the uptick was offset by the projected lower volume of ore processed at its Saucito mine.

The company confirmed that gold production remained flat due to a lower volume of ore processed at its Noche Buena operation, alongside the smaller impact of a lower volume of ore processed at Sautico and San Julian Veins.

However, Fresnillo saw its decline in gold offset by a higher ore grade and recovery rate at Herradura.

The firm also mentioned an attributable silver equivalent ounces of 25.3 moz across Q1 2022.

The company noted a 3.4% rise in attributable by-products against Q1 2021 due to a higher contribution of development ore from Juanicipio, which was slightly offset by a lower ore grade at San Julian DOB.

Fresnillo added that its by-product zinc production increased 3.6% as a result of a higher contribution of development ore from Juanicipio, along with a higher ore grade and recovery at Saucito.

The production was partially offset by a lower ore grade at Fresnillo, with a 20.2% attributable by-product lead and zinc production decrease, which was driven by lower ore grades and decreased volumes of ore processed at Saucito.

Fresnillo said its full-year guidance remained unchanged, with an estimated silver production between 50.5 to 56.5 moz and attributable gold production between 600 to 650 koz.

The company continued to roll out its selection of initiatives during Q1 to tackle the labour shortage, including recruitment campaigns, training and investment in new equipment.

Fresnillo said it expected to complete the staffing process at its San Julián and Ci é nega operations in Q3 2022, with its open pit mines already fully-staffed.

The mining group also warned that it was experiencing delays with new equipment deliveries due to global supply bottlenecks.

“We are reporting a solid first quarter’s production, in line with expectations,” said Fresnillo CEO Octavio Alvidrez.

“We have taken proactive steps to manage the impact of the Mexico labour reforms, and though we continue to see some covid-related absenteeism at our mine sites, this declined during the quarter and we are currently seeing a limited covid impact.”

“Like other industry sectors, the labour market remains very tight, and we have also seen some delays to equipment deliveries given the global supply constraints. Our full year guidance is unchanged.”

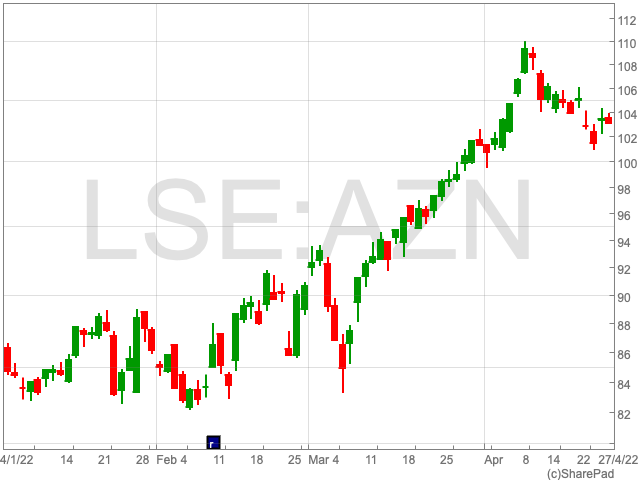

AstraZeneca announced on Wednesday that Enhertu was granted Breakthrough Therapy Designation in the US for patients with HER2-low metastatic breast cancer.

AstraZeneca and Daiichi Sankyo collaborated to create Enhertu, which has received Breakthrough Therapy Designation in the United States for the treatment of adult patients with unresectable or metastatic HER2-low breast cancer who have received prior systemic therapy in the metastatic setting or who have developed disease recurrence during or within six months of completing adjuvant chemotherapy.

Patients with hormone receptor-positive breast cancer should have received endocrine therapy or be ineligible for it.

The FDA Breakthrough Therapy Designation expedites the development and regulatory review of possible new medications that are intended to treat a serious ailment and fill a major unmet medical need.

The new treatment, Enhertu must have shown promising preliminary clinical outcomes that show a significant improvement over existing medicines on a clinically important endpoint.

Up to half of all breast cancer patients have tumours with a HER2 immunohistochemistry score of 1+ or 2+ in combination with a negative in-situ hybridisation test, a level of HER2 expression that makes them ineligible for HER2-targeted therapy at this time. For individuals with metastatic breast cancer, HER2 testing is commonly used to determine the best treatment options.

Targeting the lower end of the HER2 expression spectrum could be another way to slow disease progression and extend survival in metastatic breast cancer patients. Chemotherapy is now the only treatment option for HR-positive tumours that have progressed on endocrine (hormone) therapy. Those who are HR-negative have a limited number of possibilities.

Susan Galbraith, Executive Vice President, Oncology R&D, AstraZeneca said, “Today’s news is a significant validation of the potential we see for the historic DESTINY-Breast04 trial to enable a paradigm shift in how breast cancer is classified by targeting the full spectrum of HER2 expression.”

“Enhertu continues to show transformative potential, and this milestone represents an important advance for patients with HER2-low metastatic breast cancer who are in urgent need of new treatment options and better outcomes.”

Based on findings from the key DESTINY-Breast04 Phase III study, which showed good high-level results in February 2022, the FDA awarded the Breakthrough Therapy Designation.

Enhertu showed a statistically significant and clinically meaningful improvement in progression-free survival and overall survival in patients with HER2-low unresectable and/or metastatic breast cancer in all randomly selected patients with HR-positive and HR-negative disease compared to the physician’s choice of chemotherapy, which is the current standard of care, in the trial.

Enhertu’s safety profile was similar to that of prior clinical trials, with no new safety issues discovered. The findings will be presented at a medical conference in the near future.

Enhertu has now been designated as a Breakthrough Therapy in breast cancer for the third time.

In 2020, Enhertu received two more Breakthrough Therapy Designations for HER2-mutant metastatic non-small cell lung cancer and HER2-positive metastatic gastric cancer.

“Historically, only patients with HER2-positive metastatic breast cancer were shown to benefit from HER2-directed therapy,” added Ken Takeshita, Global Head, R&D, Daiichi Sankyo.

“DESTINY-Breast04, in which Enhertu showed a clinically meaningful survival benefit in patients with HER2-low metastatic breast cancer, is the first trial to demonstrate that selecting patients for treatment based on low expression of HER2 has the potential to change the diagnostic and treatment paradigms for these patients.”

“This Breakthrough Therapy Designation acknowledges the potential of Enhertu to fulfil an unmet medical need and we look forward to working closely with the FDA to bring the first HER2-directed therapy to patients with metastatic breast cancer whose tumours have lower levels of HER2 expression.”

Audio equipment supplier Focusrite (LON: TUNE) reported a dip in interim revenues but the second half comparatives are not as tough and there are new product launches planned.

Component shortages have held back progress, particularly for ADAM Audio, whose revenues fell by one-third. This will still hamper the business during the second half, but the problem is easing. Demand increased for Martin Audio products as live music started up again. Martin revenues recovered from £8.7m to £12.4m.

In the six months to February 2022, revenues fell 3% to £92.9m. Sales fell in North America and Europe, bu...

Northcoders Group (LON: CODE) is one of the better performing new AIM admissions from last summer. The software coding training company raised £3m at 180p a share last July and the share price has risen to 262p, a 7p rise on the day of the 2021 results. Even after that share price rise, the long-term potential is still enormous.

There remains a shortage of trained IT staff in the UK. There is plenty of demand for the training it is just a case of being able to provide. Teaching staff numbers more than doubled last year and more have been taken on this year.

Part of the strategy at the time of ...