Hikma Pharmaceuticals, a multinational pharmaceutical company, announced on Wednesday that it has received preliminary approval from the US Federal Trade Commission (FTC).

The company will now work to complete its previously announced acquisition of Custopharm from Water Street Healthcare Partners on September 27, 2021.

The parties have now received all necessary regulatory approvals to complete the deal. Hikma will make another announcement after the transaction is completed.

Tesco has long been one of the UK’s stalwart institutions, and has remained at the top of the food chain as one of the country’s “Big 4” grocers, alongside Asda, Sainsbury’s and Morrisons.

However, despite Tesco’s sparkling financial results for the last year, the supermarket warned shareholders of its widened profit guidance for the coming year as Russia’s invasion of Ukraine, the rising energy price cap and the spiking rate of inflation lead to a cost of living crunch which risks driving customers out of Tesco, and into the aisles of its discount competitors.

Tesco Financial Results

Tesco enjoyed shining financial results in its report for 2021-2022, with a profit of £176 million after a loss of £175 million in the previous year, along with a revenue of £922 million against a top line of £735 million the year before.

The supermarket also noted a 2.5% increase in Group sales to £54.7 billion against £53.4 billion in 2020-2021.

Russia’s war in Ukraine has sent the UK economy into a tailspin, with goods and services including oil, food and housing all caught in the chaotic fallout. This has been reflected in the Tesco share price which is down 9% so far in 2022.

The UK energy price cap also rose 54%, tacking on an average of £700 to the energy bills of British households and adding to the burden of climbing food prices which left consumers between the stomach-churning options of heating or eating in the middle of a cold spring snap.

Inflation hit a rate of 7% in March 2022, the highest level since records began in the 1990s, and the pain is only set to get worse with a peak of over 8% inflation in the dead of winter this year.

The Group has warned that a variety of factors including post-lockdown customer activity and cost inflation would contribute to its widened profit guidance, along with the supermarket’s significant investment to retain its market price position.

The surging cost of living might just create the ideal opportunity for its lower-priced competitors to step in and dull the burnished glow from Tesco’s shares.

Discounter Diversion

Grocery inflation reached a peak of 5.2% in March, according to data from Kantar, which saw customer levels at discount stores surge.

Longstanding discount giants including Lidl and Aldi reaped the benefits of tighter belts on customers, with Lidl earning a 6.4% market share and Aldi soaring to an 8.6% slice of the supermarket pie, less than a mere 1% from Big 4 player Morrisons.

“More and more we’re going to see consumers and retailers take action to manage the growing cost of grocery baskets,” said Kantar head of retail and consumer insight Fraser McKevitt.

The fact that this trend can already be spotted before the full impact of rising inflation has hit consumer wallets bodes poorly for the grocery giants across the UK.

The recent downturn in household budgets has trimmed customer spending down to its bare bones, and is eating into the basic necessities of living.

Tesco Shares Valuation

The grocer’s current price-to-earnings ratio is 12.3, with a forward price-to-earnings ratio of 12.6, which indicates that the group is projected to produce tepid profit growth moving into 2022-2023.

The predicted growth hardly leaves room for bounding optimism over the company’s prospects, and with fairly good reason in light of the surging cost of living in recent times.

One would think the Tesco share price is set to struggle this year as the company fights to maintain, let alone grow, its customer base.

Shell shares have enjoyed solid gains over the past 12 months with macro-economic pressures providing an ideal environment for earnings growth.

Since February 2022, sanctions and bans on Russian oil supply along have provided energy stocks with higher oil prices and expectations of higher earnings. This was a welcome relief to oil firms after the pandemics latest strain, Omicron, resulted in lockdowns across the globe and halts in production hurting oil prices, and in turn hurting Shell.

However, the oil and gas company’s shares have gained 31% year-to-date as curbs on oil imports from the world’s second-largest exporter, Russia, caused inflationary pressures which boosted the price of oil across the globe.

Shell has the largest market capitalisation on the FTSE 100 with a market cap of £168bn as of Tuesday. The Shell share price six month low was 1,556p in late November 2021. However, since then the Shell shares have consistently produced respectable gains.

Shell Recent History

September

Before September 2021, Shell shares were moving with relative steadiness. However, a series of events have helped boost the Shell share price higher over the last 6 months.

The facility in Rotterdam was amongst the largest of its type in Europe and was located at Shell Energy & Chemicals Park Rotterdam, formerly known as the Pernis refinery.

The facility is capable of producing 820,000 tonnes per year of sustainable aviation fuel and diesel from waste, where aviation fuel is expected to produce more than half the output capacity of the facility.

West Delta-143 is a transfer station for production from Shell’s assets in the Mars corridor in the Mississippi Canyon area of the Gulf of Mexico to onshore crude terminals.

During the same period, Shell announced the sale of its assets in the Permian Basin of the US to rival ConocoPhillips for $9.5bn. The proceeds from the sale would be used towards a $7bn payout to shareholders and strengthen its finances which gave the shares of the company a boost.

Amongst disposals, the company’s subsidiaries also completed the sale of upstream assets from Shell Egypt NV and Shell Austria GmbH in Egypt’s the Western Desert to Capricorn Egypt and subsidiaries of Cheiron Petroleum for 50% each.

Overall, in September, despite losses created through hurricane damage in the US, the company’s disposal of assets helped the group’s overall share price performance, and stock kicked off what would be a sustained uptrend.

October

October disclosed Q3 results for the company which included the damages caused by Hurricane Ida on the group’s assets in the Gulf of Mexico. The damages amounted to £400m and were expected to hurt Shell’s earnings in Q3 2021.

Shell expected the Upstream segment to take the biggest hit, with adjusted earnings to fall by $200m-$300m. Production in the Upstream segment is expected to see a 4.7% decline to 2m- 2.1m barrels of oil equivalent per day (BPD) in the third quarter.

The group expects Oil Products to be lowered by $50m-$100m and Chemicals to take a $100m hit.

In mid-October, Brent Crude reached $84 a barrel for the first time in 3 years lifting oil stocks including Shell.

Shell released its Q3 results in late October where the company reported a loss attributable to shareholders of $447m compared to a profit of $489m in 2020 due to pressure from activist investors.

The oil and gas company saw a decline of 200,000 BPD from Q2 2021 to 3.1m BPD in the third quarter. However, Shell pledged additional returns to shareholders following the sale of its Permian Basin assets amounting to $7bn which restored investor faith in the shares.

November

Shell shares were steady through the first couple of weeks in November despite the company announcing the re-commencement of operations at its Maras and Ursa platforms in the US Gulf of Mexico and had started exporting oil and gas through the West Delta-143 A facility.

The company also announced that 100% of the Shell-operated output in the Gulf of Mexico will resume online before expectations once Mars and Ursa are producing optimally.

Around mid-November, Shell announced that it plans to simplify its share structure and change its name to Shell PLC from Royal Dutch Shell. Instead of the ‘A’ and ‘B’ share structure, the company planned for a conventional single share structure to allow for an ‘acceleration in distributions by way of share buybacks, reduce the risk for shareholders, and let the company manage its portfolio with greater flexibility’.

Shell shares began to rise again from the start of December 2021 with its first announcement for the month being the completion of the sale of its assets in Permian to ConocoPhillips for $9.5bn in cash.

The company commenced the first tranche of share buybacks following the sale of its Permian business, coming up to $1.5bn right after the sale was completed which were later cancelled. This buyback is part of the $7bn shareholder distributions pledged by the company in September.

Plans to move to London for the corporation were set around mid-December followed by the company announcing the acquisition of Savion.

Amongst other expansion strategies, the company faced contract renewals and extensions around late December with companies such as Smart Metering Systems. The company also signed an agreement with the government of Oman for gas production at the Saih Rawl field.

In December, the company also pulled out of its plan to develop the Cambo oilfield in the North Sea near the Shetland Isles due to criticism from activists leading to investors becoming worried. However, the company does rethink this move later on in 2022.

Adding to news that may upset investors, a South African court banned Shell from conducting energy exploration using seismic waves of a touristic stretch of coastline.

Year to Date

The start of 2022 was still dealing with the pandemic which hurt manufacturers worldwide as lockdowns were implemented to curb the widespread Omircon variant along with supply issues impacting oil prices.

Adding to the debacle of 2022 was the Russian invasion of Ukraine which played the largest role in the volatility that Shell shares have seen this year.

Shell began the year with a confirmation on continuing the share buyback programme “at pace”, despite seeing a slight hit on oil products demand due to the Omicron variant.

During the end of January, Shell started operations of its first hydrogen electrolyser in China through its joint venture with Zhangjiakou City Transport Construction Investment Holding Group. The group ended the month by finally unifying its shares.

The second month of 2022 saw the start of the war and Shell reported its Q4 2021 results along with its final report.

Shell had a $29.8bn pretax profit in 2020, compared to a $267bn loss in a Covid-affected 2020. Pretax earnings increased from $1.2bn to $16.3bn in the fourth quarter.

The company’s adjusted earnings in Q4 increased to $6.4bn, up from $393m in 2020. Shell’s Integrated Gas division drove the increase, which was up 55% from $4.1 in the previous quarter. Adjusted earnings for the year surpassed the market consensus of $18bn, up dramatically from $4.9bn in 2020.

Average liquid prices rose to $77.75 a barrel in Q4, up from $68.04 a barrel in Q3, boosting the Integrated Gas, Renewables & Energy Solutions unit.

Shell also increased its annual dividend by 37%, from $0.6530 per share in 2020 to $0.8935 per share in 2021. The company’s Q1 2022 dividend will be increased to $0.25 per share, up from $0.24 in Q4 2021.

Meanwhile, Q4 output was a bit of a mixed bag. Production of integrated gas declined to 927,000 BPD in the fourth quarter, down from 938,000 in Q3. The first quarter of 2022 is expected to produce between 760,000 and 820,000 BPD.

Upstream output increased by a quarter to 2.16m BPD, up from 2.08m Q3 figures. The range for the first quarter is between 2m and 2.2m.

Following Russia’s invasion of Ukraine, Shell said that it will withdraw its joint ventures with Russian energy major PJSC Gazprom, as well as its involvement with the Nord Stream 2 pipeline project.

Shell will sell its 28% ownership in the Sakhalin-II liquefied natural gas facility, its 50% stake in Salym Petroleum Development NV, and its 50% stake in the Gydan energy venture, among other things.

The Salym JV is focused on the development of the Salym fields in western Siberia’s Khanty Mansiysk Autonomous District, while Gydan is a joint venture between Gazprom and Shell for the exploration and development of a block in northwestern Siberia’s Gydan peninsula.

Shell was also one of five energy companies that agreed to offer funding and guarantees for up to 10% of the estimated cost of Nord Stream 2.

Shell had announced that it will stop buying Russian crude on the spot market and close its service stations, aviation fuels, and lubricants activities in Russia.x

Following the invasion of Ukraine, the UK business also apologised for purchasing a cargo of Russian oil which gave hope to ethical investors.

In early January, Shell and Iberdrola SA’s ScottishPower joint venture won multiple bids to develop 5 gigawatts of floating wind power in Scotland as part of Crown Estate Scotland’s ScotWind Leasing bidding process.

In late January, Shell sold its 50% interest in Deer Park Refining Partnership for $596m, in a combination of debt and cash.

At the end of March, the company began production at subsea development PowerNap which is located in the US Gulf of Mexico. The development is expected to produce 20,000 BPD at its peak. The company also obtained an extension to its license on the Cambo oilfields from the UK government.

Shell Share Price Valuation

Shell has a market capitalization of £168bn and its shares have gained 31% YTD.

In the last 6 months, Shell shares have increased 25% with the stock seeing a 2% rise to 2,232p on Tuesday.

Shell has a forward P/E of 6x with a trailing P/E of 14.2x and a ROCE of 8.6x.

The company has a dividend yield of 3.1x and a cover of 2.3x which may mean better dividends for investors in the future can be expected.

Shell’s Outlook

Shell is well spread across the globe to withstand Russia’s sanctions and the problems it caused for the company.

With the Shell share price on the rise since the start of 2022, it’s easy to think that investors who are yet to buy Shell have missed the boat. However, with the booming commodities market and possibility of higher dividends in the future, investors may have scope for decent returns in the near future with an allocation to Shell shares.

The FTSE 100 was up 0.4% to 7,634 in late morning trading on Wednesday, despite the gathering storm of rising inflation and the spiking cost of living.

The markets also seem to have grown accustomed to Russia’s invasion of Ukraine after the chaotic upheavals of late February and March, with investors adjusting to the new reality of Putin’s knock-on effect on supply chains and international oil and food cost surges.

“The markets seem to be stuck in a bit of a holding pattern. They’ve absorbed the shock of Ukrainian conflict and seemingly shrugged it off, while also reacting calmly to an escalating cost of living crisis and new Covid disruption in China,” said AJ Bell investment director Russ Mould.

“It feels like something will have to give at some stage but when that might be and what the catalyst could be remains to be seen.”

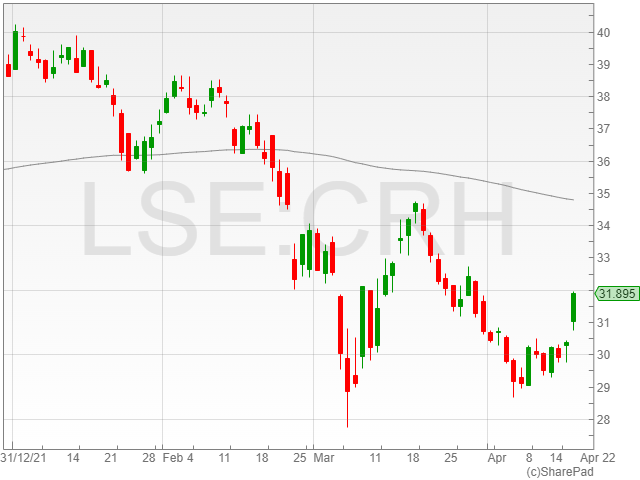

CRH hit the top risers with a 4.4% increase to 31,727p in light of sparkling Q1 results with growth in earnings and sales expected for the first half of the year.

“The continued delivery of our solutions strategy resulted in a good start to the year,” said CRH CEO Albert Manifold.

“Although a number of challenges and uncertainties continue, our demand backdrop remains favourable.”

The acquisition marks the company’s breakthrough into Southern Europe, with assets across France and Spain.

“The project portfolio brings some excellent assets and will provide a real springboard for our expansion plans in Europe across wind, solar, batteries and hydrogen,” said SSE Renewables managing director Stephen Wheeler.

Covid-19 cases and strikes at its Kitimat smelter also served to exacerbate the company’s difficulties in a tricky quarterly update.

Hikma Pharmaceutical shares were down 1.1% to 20,570p after the group’s recent success in gaining approval from the US Federal Trade Commission for its scheduled acquisition of US generic injectables company Custopharm Inc for $425 million.

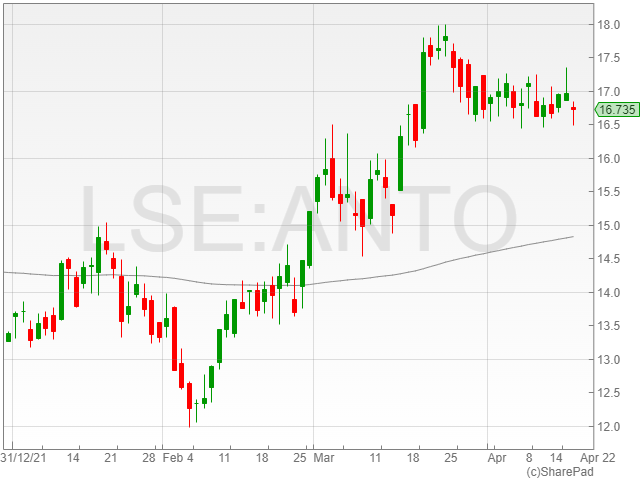

Antofagasta shares dropped 1% to 16,702p after RBC hit the company with an ‘underperform’ recommendation and cut its price target to 1,300p from 1,350p.

FTSE 250 was trading down 0.13% to 20,935 as the AIM all share index traded flat at 0.05% to 1,005 as the UK’s small and mid cap markets traded sideways.

QinetiQ expects a 5% rise in revenues from £1.3bn in 2021 and predicts underlying operating profit will reach at least £135m.

The company experienced a strong order intake which amounted to £1.2bn in 2022.

QintetiQ enjoyed significant growth due to help from its EMEA Services segment where the company provides services such as training and research for maritime and air & space clients.

Petershill Partners announced its full-year results today which helped shares gain 2% to 217p. The company reported an IFRS profit after tax of $248m and raised $720m in IPO which was net of share issue costs.

Petershill’s board proposed a final dividend of $0.02 which was in line with the guidance. The company also intended to launch a share buyback programme of up to $50m.

Since the IPO, Petershill has completed 5 acquisitions worth $458m in total and expects that investments will be 9% accretive to the consensus earnings forecast by 2023.

Centamin shares sunk 7% to 90p despite the company reporting quarterly results in line with guidance and stating the outlook for 2022 remains unchanged.

The company predicted lower production in Q1 2022 than in any other quarters due to underground transitions, which amounted to 93,109 oz of gold.

Centamin generated a revenue of $174.6m from the sale of 92,559 oz of Au at an average of $1,883/oz. The company recorded cash costs of $1,006/oz produced.

Centamin recorded CAPEX of $71.4m due to the quarterly investment which peaked in 2022, with major investments in the paste fill facility, solar power plant, and underground transition.

In Oxford’s preliminary results, the group noted a 63% revenue increase to £142.8m in 2021, up from £87.7m. The company recorded a pretax profit of £19.9m.

Oxford BioMedica forecasted an operating loss before interest, tax, depreciation, and amortisation of £35.9m in 2022, down from £35.9m in 2021.

Quilter shares fell 3% to 140p as the company reported said as a result of market uncertainty related to Russia’s invasion of Ukraine, the market value of its investments fell in the first quarter.

Quilter’s assets under management and administration decreased by 4% to £107.2bn at the end of March 31 from £111.8bn in December 2021.

Wood Group shares dropped nearly 1% to 190p following the company reporting a 14% fall in revenues on an LFL basis summing to $6.4bn, as the growth gained from Consulting and Operations was offset by declines in projects.

Wood Group’s pretax loss decreased from $148.6m to $80.6m in 2021. The company noted $160m in exceptional items which included a $99m write-down of its Aegis Polan contract and $78m of restructuring costs.

Bion lost more than three-quarters of its share value on recommencement of trade on the AIM following a period of suspension. Bion’s shares fell 75.8% to 0.4p.

Kefi Gold and Copper shares plummeted 30% to 0.84p after the company announced oversubscribed fundraising to raise £8m. The amount will be raised through a firm placing of 550,000,000 new ordinary shares of 0.1p each in the capital of the company for 0.8p per Ordinary Share to raise £4.4m and a conditional placing of 450,000,000 new Ordinary Shares at the placing price to raise £3.6m arranged by Tavira Securities.

Cornerstone gained 20% to 21p after the company reported its highest-ever unaudited quarterly revenue on Wednesday with total unaudited revenue for Q1 2022 reaching £946k. Cornerstone’s board remains confident in the group’s outlook for 2022.

Naked Wines shares increased 16.5% to 384p following the company’s announcement of its latest trading update where the company said its performance was in line with expectations driven by repeat customer sales, strong retention and demand from existing members.

Naked Wines’ group sales increased 5% YoY on a constant currency basis and 3% reported. The group saw sales retention of 80% whilst the guidance predicted the mid-70s. Naked Wines’ repeat customer sales increased by 13% YoY on a constant currency basis.

Companies such as Volex and Coral also released trading updates on Wednesday where the companies said that results are ahead of expectations sending its shares to gain 13.7% to 281p and 12.5% to 15.7p respectively.

Broker Price Target Changes

Quite a few companies faced alterations in its broker price target on Wednesday including companies such as Lancashire Holdings and Wizz Air.

Barclays cut Lancashire Holdings’ price target to 731p from 781p, however, the company’s shares still gained 0.86% to 409.9p.

Hiscox and Beazley shares lifted 0.16% to 924p and 0.84% to 396p after Barclays raised both companies’ price targets to 1,067p and 541p respectively.

Wizz Air shares fell 0.2% to 2,943p after UBS and Berenberg both cut its price target to 3,660p and 3,500p from 4,050p and 4,400p respectively.

Marshalls’ shares dropped 0.35% to 647p after Berenberg cut its price target to 770p from 790p.

Bodycote’s shares lifted 0.48% lifting 633p despite Jefferies cutting Bodycote’s price target from 1,115p to 920p.

Netflix is losing its sparkle as competitors and the increasing cost of living finally seem to have struck a blow to the streaming giant, with shares falling 25.5% on the back of its announced results.

The company reported a considerable slowdown in revenue growth, with a 9.8% rise to $7.9 million compared to 24.2% in the same period last year, following a 16% growth last quarter.

The group expects the trend to continue, with its Q2 growth forecast at 9.7% after Netflix’s first subscriber loss in 10 years of 200,000 paying members in the first quarter. The streaming said they would lose 2 million over the next quarter.

However, a lower than expected content spend brought Netflix below management expectation with an operating income of $2 billion, with an anticipated expense of $1.7 billion in the upcoming quarter.

The company said that it was currently aiming to maintain an operating margin of approximately 20% as it searches for means to spark off revenue growth and tackle the issue of shared passwords.

“Households around the world may have racked up a record breaking 627m hours watching Netflix’s smash hit Bridgerton, but a lot of those people weren’t paying,” said Hargreaves Lansdown equity analyst Laura Hoy.

“The streaming service has made its way into just about every home with an internet connection and that’s made it much harder to continue growing revenue.”

The issue has been slightly exacerbated by the service’s withdrawal from Russia, bringing a 700,000 member decline along with the 200,000 drop in new paying subscribers for the first quarter.

In other territories, rising prices saw a 600,000 member decline across the US and Canada, with a 400,000 subscriber fall in Latin America.

However, the streaming firm enjoyed a 400,000 member increase across Europe, the Middle East and Africa.

Netflix noted a current level of 221.6 million paying subscribers over the period, however competitors including Disney+ and Amazon are quickly eating into its subscriber base.

“Price increases helped offset pain from a decline in new subscriber numbers—but the group’s looking for a more permanent way to cope with rising demand on the public’s attention,” said Hoy.

The company paid $3.6 billion on content additions during the term, alongside a net debt of $8.6 billion and a free cash flow rise from $692 million to $802 million, due to rising profits.

The group confirmed its planned acquisition of Next Games in addition to its streaming provision, with the deal scheduled for completion in the second half of the year.

“The group spent over $17bn on content last year, and that’s likely to be a minimum for this year’s spend,” said Hoy.

“Protecting profits is high on management’s priorities with an aim to keep margins over 19%, but as revenue growth stagnates, it’s difficult to see how the group will continue to grow its user base without succumbing to eyewatering content costs.”

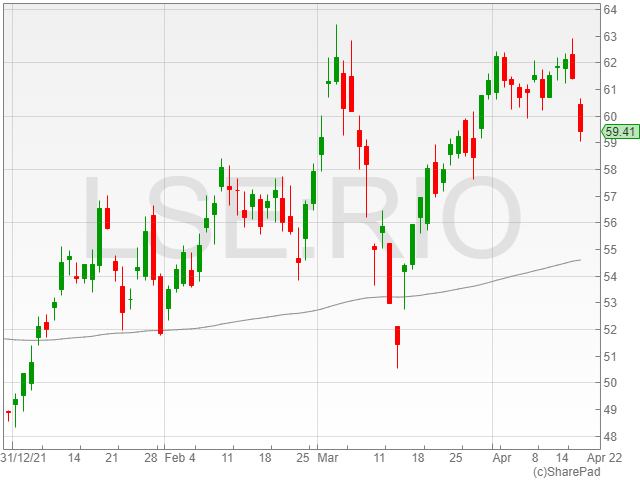

Rio Tinto shares were down 2.7% to 118.3p in early morning trading on Wednesday after the mining giant reported a “challenging” first quarter in 2022.

The company said that it produced 71.7 million tonnes of iron ore from its Pilbara operations, noting a 6% drop compared to the first quarter of 2021, along with an 8% slide in Pilbara shipments to 71.5 tonnes.

Rio Tino assured investors that it expected increased production volumes and improved product mix in the second half, as a result of the Robe Valley wet plant commissioning and its ramp up of Gudaj-Darri.

“Production in the first quarter was challenging as expected, re-emphasising a need to lift our operational performance,” said Rio Tinto CEO Jakob Stausholm.

“We launched seven more deployments of the Rio Tinto Safe Production System, building on the achievements from the previous rollouts.”

“As we ramp up Gudai-Darri, our iron ore business will have greater production capacity and be better placed to produce additional tonnes of Pilbara Blend in the second half.”

The group’s current full year ship guidance reportedly remains unchanged.

The mining firm’s 13.6 tonnes on Bauxite production were in line with the first quarter of last year’s production, and its 0.7 million tonnes of aluminium production was 8% lower than the same period in 2021, due to reduced capacity at its Kitimat smelter in British Columbia following a strike which kicked off in July 2021.

Production is expected to gradually restart at Kitimat from June until the end of this year, with Rio Tinto’s other smelters maintaining a stable performance despite rising cases of Covid-19 among its staff.

The group enjoyed a 4% increase in mined copper production to 125 thousand tonnes and a 3% rise in pellets and concrete production at Iron Ore Company of Canada.

However, the firm also saw a 2% drop in titanium dioxide slag production at 273 thousand tonnes as a result of equipment reliability complications at Rio Tinto Fer et Titane in Canada.

Rio Tinto reported that its Oyu Tolgoi project had seen some welcome progress, highlighting the agreement struck with Turquoise Hill Resources and the Mongolian Government to move the project forward after an uphill battle to kickstart production in the region.

“We made notable progress during the quarter with the commencement of underground mining at Oyu Tolgoi following a comprehensive agreement reached with the Government of Mongolia,” said Stausholm.

The firm also noted its non-binding proposal with the Turquoise Hill Board to acquire the 49% of issued and outstanding shares which Rio Tinto does not currently own for a proposed price of $34 per share.

The proposal values Turquoise Hill minority shareholdings at a reported $2.7 billion.

Eckoh is pleased to report that its contract with Capita for a big public sector organisation has been renewed.

The primary goal of Capita’s service to its clients is to maximise the amount of money collected from the general population.

The new contract with Capita is for 5 years and is worth a minimum of £2.1m over that time, making it both longer and more valuable than the prior agreement.

Eckoh has been assisting Capita and its client since 2018, handling all inbound calls to the contact centre, securing telephone and automated payments, and enabling enhanced self-service automation to improve the customer experience and boost the percentage of successfully collected money.

The contract’s renewal and extension demonstrate Capita’s continued faith in Eckoh’s expertise and product solutions, as well as its commitment to providing a superior customer experience.

Capita’s first hurdles included lowering customer service expenses, expanding the number of successful payments, and completely complying with the Payment Card Industry Data Security Standard without sacrificing customer service quality.

Eckoh responded by delivering CallGuard, a proprietary payment technology that secures telephone payments made by contact centre agents, as well as the EckohPAY solution, which offers the same security for payments made within the automated voice system.

Eckoh’s powerful natural language self-service and intelligent call routing technology provide accurate speech recognition so that calls are directed to the correct location the first time, whether it’s an agent or a self-service facility.

These new features allow the client to provide self-service for operations such as changing addresses, making secure payments, updating accounts, and more without requiring an agent. This lowers customer support expenses while giving clients more control over their accounts for Eckoh.

Capita’s whole contact centre has now been de-scoped from the rigours and cost of full Payment Card Industry Data Security Standard compliance, resulting in a considerable increase in revenue collection and enhanced customer satisfaction.

Nik Philpot, Eckoh’s CEO commented, “Capita is a longstanding and highly valued partner, so we’re delighted to be renewing this significant contract for another 5 years, which follows the 6 year contract renewal worth £4m we signed with them for the congestion charge in 2020.”

“Eckoh’s comprehensive technology portfolio means we are uniquely placed to provide a full suite of customer engagement solutions that are underpinned by market leading security. We can help organisations to meet today’s contact centre security challenges and support them in delivering on their digital transformation initiatives.”

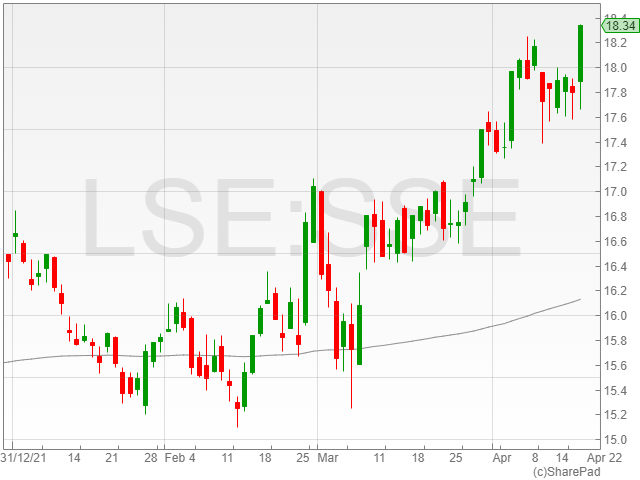

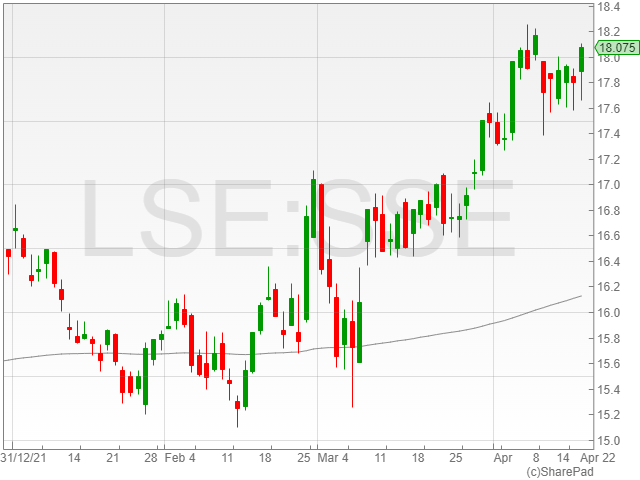

SSE shares were up 1.6% to 1,815p in early morning trading on Wednesday after the energy company acquired from Siemens Gamesa Renewable Energy’s (SGRE) existing European renewable energy development platform for €580 million.

The portfolio includes a reported 3.9GW of onshore wind developments, with half of the assets located in Spain and the rest situated across France, Italy and Greece.

The agreement is on track for completion by September 2022, and marks the energy giant’s entry into the Southern European market on the back of its existing 4GW of renewable energy assets based in the UK and Ireland.

The company also said that there is scope for up to 1GW of additional co-located opportunities for solar development.

SSE Renewables confirmed that it is currently aiming to have 500MW of renewable energy projects from the SGRE assets operational by March 2026, alongside an additional 500MW in the company’s production pipeline.

The acquisition stands to boost the group’s Net Zero Acceleration Programme (NZAP), and ticks several vital boxes on the company’s target list.

The acquisition is set to bring 4GW of net additions over five years, doubling SSE’s installed renewables capacity to 8GW by 2026, alongside a pipeline consistency of at least 15GW of renewable development.

The portfolio will also bring the firm towards a delivery of at least 1GW in net capacity additions per year over the second half of the decade and triple the company’s installed renewables capacity to over 13GW, with an additional fivefold increase target to 50TWh in renewables output per year by 2031.

“We are delighted to boost the delivery of SSE’s Net Zero Acceleration Programme by expanding our existing renewables business into Southern Europe through this acquisition,” said SSE Renewables managing director Stephen Wheeler.

“Mainland Europe is an exciting growth market for onshore wind, with clear carbon reduction targets and supportive policies, and the expert management team will complement our sector-leading capabilities perfectly.”

“The project portfolio brings some excellent assets and will provide a real springboard for our expansion plans in Europe across wind, solar, batteries and hydrogen.”

Petropavlovsk released an announcement on Wednesday regarding the repayment of $300m to Gazprombank (GBP) which sent its shares tumbling 25% to 1.57p in early morning trade.

Russian gold miner Petropavlovsk has seen turbulent times especially due to its exposure and association with GPB due to the Russian invasion of Ukraine. GPB is on the UK Sanctions List and has been designated for an asset freeze under the Russia Regulations 2019 which was previously reported.

Following up on Petropavlovsk’s prior announcements, the group has now received warnings from GPB claiming that they must make prompt repayment of approximately $201m including accrued interest under the company’s Committed Term Facility Agreement with GPB.

GBP also said Petropavlovsk has to make a repayment of approximately $87.1m including accrued interest due under the group’s Russian companies’ revolving credit facilities by April 26, 2022.

GPB has also received notice from Joint Stock Company UMMC-INVEST, as successor agent under the Term Loan, that all of its rights under the Term Loan and accompanying finance instruments have been assigned to UMMC-INVEST.

The ramifications of these notices are being discussed with the company’s advisers.