Gateley, a legal and professional services firm, announced on Tuesday that it has reached an agreement with the Bank of Scotland and HSBC UK for a new revolving credit facility amounting to £30m.

Gateley’s new revolving credit facility provides £30 million in committed funding between the Bank of Scotland and HSBC UK until April 2025.

The dual bank club replaces the group’s previous £8m overdraft arrangements with Bank of Scotland and HSBC UK, giving it more flexibility to fund future growth and acquisitions.

The loan has an interest rate that is 1.95% higher than the SONIA reference rate.

“We are delighted to have agreed this new £30m facility with our long-term supportive banking partners of Bank of Scotland and HSBC UK. The facility will provide us with additional headroom to continue with our stated strategy to grow organically and through acquisitions,” said Rod Waldie, Gateley CEO.

“We continue to position ourselves to invest in and grow our Platforms to provide an increasing breadth of services to our clients.”

“The aggregation of complementary legal and consultancy services on our four market-facing Platforms of Corporate, Business Services, People and Property continues to differentiate Gateley, strengthen our appeal to clients and enhance our resilience.”

Leading global manufacturer of utility-grade energy storage, Invinity Energy Systems received 3 certifications from International Organization for Standardization (ISO) on Tuesday morning.

Following an exhaustive audit process conducted by top global assurance provider SAI-Global, Invinity Energy Systems has been certified as complying with ISO standards for Quality Management (ISO 9001), Environmental Management (ISO 14001), and Health & Safety Management (ISO 45001).

Invinity is now one of just three flow battery manufacturers in the world to hold all three certifications at the same time, confirming the company’s position as a leading producer of utility-grade solutions to the stationary energy storage industry.

International Organization for Standardization

The International Organization for Standardization (ISO) is a significant benchmark institution in the world.

The ISO creates standards to ensure the quality, safety, and efficiency of products, services, and systems. These standards are widely recognised as the gold standard for operational excellence among major industrial companies throughout the world.

Individual criteria to which Invinity has now been certified are critical to the company’s operations.

ISO 9001 specifies the requirements for a company’s quality management system (QMS) and is founded on fundamental quality management principles such as a strong customer focus, senior management involvement and accountability, process orientation, and continuous improvement.

ISO 9001 standards and processes will enable Invinity to provide consistently high-quality products and services to its clients.

An Environmental Management System (EMS) is defined by ISO 14001 as a systematic framework for measuring, managing, and minimising the immediate and long-term environmental impacts of an organization’s goods and operations.

Completing this certification will ensure Invinity’s customers and partners that the company honours its environmental commitments and operates with the least amount of environmental effect feasible.

ISO 45001 is a global standard for occupational health and safety that aims to manage and reduce any health and safety risks linked with Invinity’s activities for all stakeholders.

ISO 45001 standards, when used in conjunction with regional, national, and industry-specific workplace safety rules, will help Invinity formalise procedures to proactively improve health and safety performance, provide a safe and healthy workplace, and reduce the risk of causing irreversible harm to employees or the company as a whole.

These three certifications demonstrate Invinity’s commitment to not just producing a high-quality product, but also to being a leading supplier in the stationary energy storage sector.

Compliance with these three standards, according to the firm, will speed up Invinity’s commercial development by demonstrating to new customers that Invinity conforms to the highest operational excellence standards without the need for time-consuming and costly due diligence.

Finally, adhering to these ISO standards will aid Invinity’s expansion by laying the solid foundations required to expand and scale the company’s business in a ‘sustainable, responsible, and transparent way’.

Invinity

Invinity was formed in April 2020 by the combination of two industry leaders in the flow battery sector, redT energy plc and Avalon Battery Corporation.

Invinity is active in all major global energy storage markets and has operations all over the world, with over 25 MWh of systems implemented to date across more than 40 sites in 15 countries.

Flow batteries are made by Invinity Energy Systems for large-scale, high-throughput energy storage needs in business, industry, and electrical networks.

Factory-built flow batteries from Invinity run continuously for over 25 years with minimal degradation, making them ideal for the most demanding applications in renewable energy production.

Energy storage systems based on Invinity’s batteries are safe, dependable, and cost-effective, with capacities ranging from under 250 kilowatt-hours to tens of megawatt-hours.

Larry Zulch, Chief Executive Officer, Invinity said, “As Invinity commercialises our long-duration vanadium flow batteries, our focus must progress from simply developing leading technology to superb execution across the entire organisation.”

“We undertook the ISO process determined to meet the highest standards; by obtaining certification in these three major areas, we have demonstrated our ability to achieve them. This is a tremendous accomplishment by our team and I am very proud of the work they have done.”

Will Fulton and Kerri Hunter, Investment Managers, UK Commercial Property REIT

After a tough pandemic, commercial property recovered significantly in 2021

Industrials led the way, while segments of the retail and office markets remained weak

The outlook for individual sectors within commercial property is diverging with asset selection increasingly important

Commercial property was one of the success stories of 2021, as investors returned to the sector in search of inflation-adjusted income and diversification. However, performance was polarised between sectors and individual assets. The need for discernment characterises the market in 2022 and beyond as the outlook for different sub-segments of commercial property, and more particularly the characteristics of specific assets, diverges.

Over the past 12 months, industrial and logistics property has continued to thrive, driven by strong rental growth and high demand, again producing the best performance with total returns of 36%; in contrast the poorest area of the market, shopping centres, achieved a total return of -5%. In general, investors favoured higher quality assets, with the exception of the industrial sector where secondary assets performed well.

Retail warehousing was also a stand-out in 2021. This marks a break with its recent past and shows that the right retail assets still have a place in a commercial property portfolio. In general, those assets linked to discount retailers and with supermarkets performed best over the year. UK Commercial Property REIT focused its attention on additions in areas it has seen growth including student accommodation, retail warehousing, and selective industrial with value-add opportunities.

What lies ahead?

More recently, in the early months of 2022, the market has started to become less polarised. We have seen industrial property deliver strong returns, but the gap with the rest of the market is far smaller. The yield compression that has characterised the industrial market in recent years is slowing and from here, we believe returns will be driven by rental growth.

Elsewhere, the picture is more complex. Polarisation of prospective returns within each sub-sector of the asset class is apparent – within offices, within retail, and so forth.

The office sector is interesting. Overall, the outlook for the sector is weak as it adjusts to an environment of agile working. It is still not clear the type of office life that will emerge, but it will certainly be different and businesses will need to change their office footprint. However, there is a notable gap between prime office spaces, with demand, and secondary, where demand is limited.

Sustainability credentials are important across all commercial property, but particularly so in the office market, where tenants are increasingly demanding wellness facilities and a low carbon footprint, alongside the usual attributes of a strong location, access to local amenities and proximity to public transport. Offices with these characteristics are in short supply with good rental prospects.

There are also selected growth areas that have been weak, but should see an improvement; for example certain leisure assets and hotels with strong fundamentals.

Today’s portfolio

The UK Commercial Property REIT portfolio has benefited from a high weighting to industrial and logistics assets. From here we see a convergence of sector returns where stock picking will become increasingly important.

For example, we are looking at properties where we can reconfigure assets to source potential returns. A recent purchase of an office close to Park Royal in London, one of Europe’s most prized industrial/distribution locations, offers us the opportunity to redevelop the site to industrial after taking a good income yield from the existing asset. This was a more compelling opportunity than buying expensive industrial assets in the same area.

We are also interested in building a higher weighting in operational assets, such as hotels, following our two student accommodation development funding projects in Exeter and Edinburgh due to complete later this year.

Within retail, the Trust’s focus is on discount and food anchored retail warehousing. Our most recent purchase in retail was a 140,000 square foot retail park close to the Trafford Centre in Manchester with a range of convenience retailers as tenants.

Our portfolio remains focused on those areas showing structural growth, or where the strategic management of assets can aim to improve returns. We believe the Company’s well-let portfolio of scale, heavily weighted towards performing sectors, and with share liquidity, should have a broad reaching appeal with potential for future earnings growth.

Important information

Risk factors you should consider prior to investing:

The value of investments and the income from them can go down as well as up and investors may get back less than the amount invested.

Past performance is not a guide to future returns.

The value of property and property-related assets is inherently subjective due to the individual nature of each property. As a result, valuations are subject to substantial uncertainty. There is no assurance that the valuations of Properties will correspond exactly with the actual sale price even where such sales occur shortly after the relevant valuation date.

Prospective investors should be aware that, whilst the use of borrowings should enhance the net asset value of the Ordinary Shares where the value of the Company’s underlying assets is rising, it will have the opposite effect where the underlying asset value is falling. In addition, in the event that the rental income of the falls for whatever reason, including tenant defaults, the use of borrowings will increase the impact of such fall on the net revenue of the Company and, accordingly, will have an adverse effect on the Company’s ability to pay dividends to Shareholders.

The performance of the Company would be adversely affected by a downturn in the property market in terms of market value or a weakening of rental yields. In the event of default by a tenant, or during any other void period, the Company will suffer a rental shortfall and incur additional expenses until the property is re-let. These expenses could include legal and surveying costs in re-letting, maintenance costs, insurance costs, rates and marketing costs.

Returns from an investment in property depend largely upon the amount of rental income generated from the property and the expenses incurred in the development or redevelopment and management of the property, as well as upon changes in its market value.

Any change to the laws and regulations relating to the UK commercial property market may have an adverse effect on the market value of the Property Portfolio and/or the rental income of the Property Portfolio.

Where there are lease expiries within the Property Portfolio, there is a risk that a significant proportion of leases may be re-let at rental values lower than those prevailing under the current leases, or that void periods may be experienced on a significant proportion of the Property Portfolio.

The Company may undertake development (including redevelopment) of property or invest in property that requires refurbishment prior to renting the property. The risks of development or refurbishment include, but are not limited to, delays in timely completion of the project, cost overruns, poor quality workmanship, and inability to rent or inability to rent at a rental level sufficient to generate profits.

The Company may face significant competition from UK or other foreign property companies or funds. Competition in the property market may lead to prices for existing properties or land for development being driven up through competing bids by potential purchasers.

Accordingly, the existence of such competition may have a material adverse impact on the Company’s ability to acquire properties or development land at satisfactory prices.

As the owner of UK commercial property, the Company is subject to environmental regulations that can impose liability for cleaning up contaminated land, watercourses or groundwater on the person causing or knowingly permitting the contamination. If the Company owns or acquires contaminated land, it could also be liable to third parties for harm caused to them or their property as a result of the contamination. If the Company is found to be in violation of environmental regulations, it could face reputational damage, regulatory compliance penalties, reduced letting income and reduced asset valuation, which could have a material adverse effect on the Company’s business, financial condition, results of operations, future prospects and/or the price of the Shares.

Other important information:

Issued by Aberdeen Asset Managers Limited which is authorised and regulated by the Financial Conduct Authority in the United Kingdom. Registered Office: 10 Queen’s Terrace, Aberdeen AB10 1XL. Registered in Scotland No. 108419. An investment trust should be considered only as part of a balanced portfolio. Under no circumstances should this information be considered as an offer or solicitation to deal in investments.

The FTSE 250 was down 0.6% to 20,986.8 and the AIM was down 0.4% to 1,055.2 on Tuesday as the breakdown of Russia-Ukraine peace talks and the spiking cost of living dampened investor optimism heading after the easter break.

Spectris shares increased 5.5% to 26,540p after the company reported its divestment of Omega Engineering to Arcline Investment Management, along with its upcoming £300 million share buyback scheme.

“Today’s announcement is yet a further example of our approach to optimising our assets and successfully divesting businesses at multiples higher than the group as a whole,” said Spectris CEO Andrew Heath.

“This disposal, in conjunction with the share buyback programme, delivers clear value for shareholders, whilst also allowing us to take advantage of new growth opportunities for our core businesses, in line with our purpose.”

Harbour Energy shares rose 0.9% to 524.5p after the company reported its exit from the North Falkland Basin, with Navitas scheduled to buy all the shares in Harbour’s indirectly held subsidiary POEPL, via which Harbour holds its rights in the North Falkland Licenses.

JTC shares saw a decline of 6.4% to 758p following the group’s 57.2% drop in operating profits to £9 million compared to £21 million last year.

The SSP Group fell 5.9% to 230p after Deutsche Bank reduced the stock to a hold from a buy recommendation and cut the firm’s price target to 265p from 333p.

888 shares dipped 3.7% to 210p following Berenberg’s ‘buy’ recommendation, with a price target cut to 500p compared to 545p.

Arrow Exploration Group shares increased 15.3% to 15p after the company reported positive results from its RCE-2 Well, following its spudding on 2 April and its total drilled depth of 9,674 ft from 14 April.

The RCE-2 Well’s casing was finished on 18 April and cementing has been scheduled for 20 April, followed by a production testing programme.

“From the data we have, several of the pay zones are attractive and like the RCE-1 well, we believe more than one pay zone will be productive,” said Arrow Exploration CEO Marshall Abbott.

Empyrean Energy shares rose 10.5% to 11.2p after the firm announced elevated methane levels in its Jade drilling update, supporting the company’s prediction of light oil in the Chinese prospect.

“Drilling operations continue to run smoothly and safely, with progress to date right on schedule,” said Empyrean Energy CEO Tom Kelly.

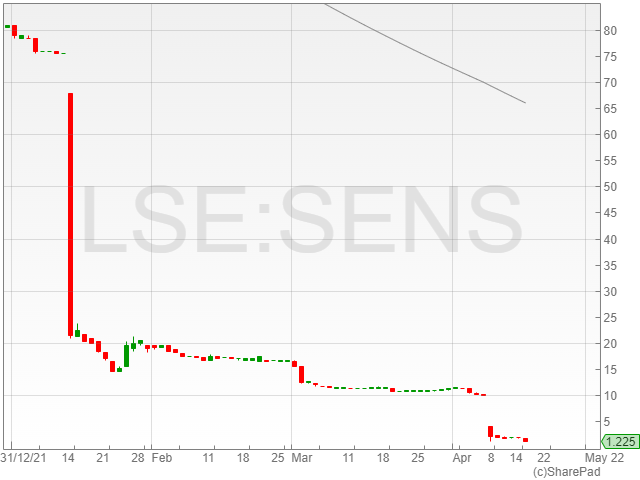

Sensyne Health shares plummeted following the firm’s proposed delisting from the AIM junior market, pending approval from shareholders at its general meeting on 20 May.

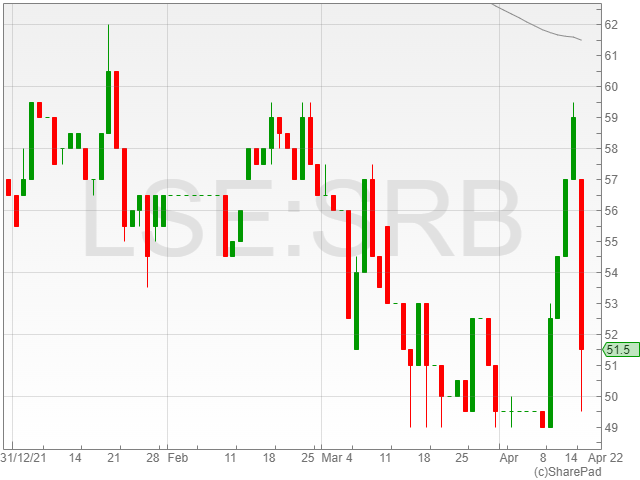

Serabi Gold dropped 13.5% to 51p after its 13% decline in gold production over the first quarter to 7,062 ounces from 8,087 ounces year-on-year had a reported knock-on effect on its full-year production guidance.

“At Palito, the first-quarter production results have been disappointing with 7,062 ounces produced, and while March was a significantly better month with improved grades and production, it was not possible to recover earlier shortfalls in planned production,” said Serabi Gold CEO Mike Hodgson.

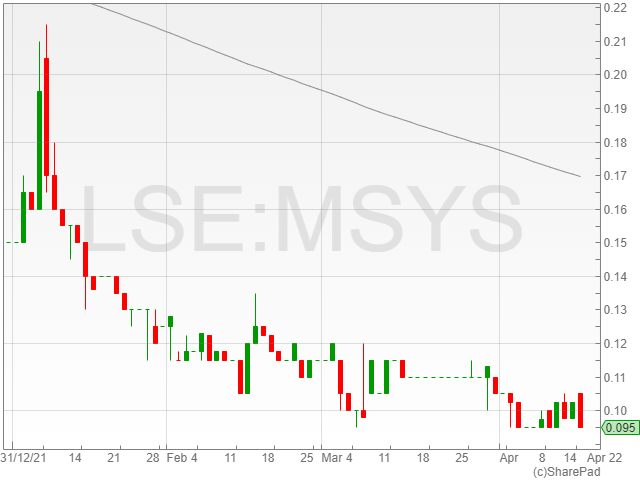

Microsaic Systems shares dropped 7.3% to 0.09p following the company’s announcement of a manufacturing services framework and initial contract with Innovenn UK Limited worth £400,000.

The agreement will reportedly see Microsaic refine and miniaturise existing monitoring technology for environmental and human health diagnostics.

“Microsaic’s business model has been transitioned to offer additional services which leverage the considerable depth and breadth of technical design, engineering and delivery expertise within its team,” said Microsaic acting executive chairman Gerard Brandon.

“By offering the skillsets that created the smallest compact mass spectrometer in the world, partner customers such as DeepVerge can outsource their engineering development of existing and new monitoring equipment and concentrate on growing their business.”

FTSE 100 fell 0.4% to 7,586 after a long Easter weekend with pharma and retail shares dragging the index down leaving “little to excite investors” according to Russ Mould, Investment Director, AJ Bell.

Commodity stocks provided some support for the index despite Brent crude falling 1% to $112 a barrel on Tuesday, shaking off concerns of disruption at production facilities in Libya.

Shell and BP shares gained 1.8% to 2,231p and 1.4% to 404p, respectively, as oil remains above the $110 mark.

JPMorgan has also raised Shell and BP’s price target to 2,850p and 500p respectively.

Shell share movement between December 2021 and April 2022

Mining Stocks

Mining and oil shares reaped the benefits of a rotation to shares that will thrive in an inflationary environment.

Mining companies such as Antofagasta, Glencore, Endeavour Mining, Anglo American and Fresnillo shares all gained on the FTSE 100 on Tuesday.

Antofagasta shares lifted 1.4% to 1,700p whilst Ferguson increased 1.5% to 10,170p followed by Glencore gaining 1% to 532p.

Antofagasta YTD Share Movement

Endeavour Mining, Anglo American and Fresnillo shares increased between 0.3%-0.7% to 2,047p, 4,198p, and 806p respectively.

Fresnillo YTD Share Movement

Rolls-Royce shares gained nearly 2% to 95p despite JPMorgan cutting the group’s price target by nearly a half from 140p to 75p.

Tesco shares were amongst the risers as the supermarket store gained 1.4% to 269p after Berenberg gave it a buy recommendation while reducing the price target to 320p from 327p.

Tesco YTD Share Movement

Amongst FTSE 100 losers are Reckitt Benckiser shares which have been tumbling 4% to 5,831p and Intertek Group with shares trading down 3.3% to 4,913p.

Scottish Mortgage Investment Trust lost 3% as US tech stock trading negatively in the pre-market.

ITV shares fell 3% to 74p after Berenberg cuts ITV to a sell recommendation from a hold recommendation with a revised price target cut by half to 64p.

Daprodustat is used on patients for the treatment of anaemia of chronic kidney disease.

GSK described the FDA review acceptance as a major milestone after winning regulatory submission acceptance by the European Medicines Agency and the approval of Duvroq, the same drug under a different name, in Japan.

Enhertu is developed jointly with Tokyo-based Daiichi Sankyo and AstraZeneca to focus on tumours with mutations of the growth-promoting protein HER2. The conjugate showed a 54.9% tumour response rate.

AstraZeneca shares were trading down 1% to 10,437p despite the news of the priority review of Enhertu.

AstraZeneca Shares between December 2021 and April 2022

Pearson said the contract expiration will have a minor earnings impact in 2022 and 2023, and that its financial projection for 2022 has not changed.

Pearson Shares between December 2021 and April 2022

Prudential shares dropped 1% to 1,057p despite SocGen raising Prudential’s recommendation to buy from hold as it increased its price target to 1,375p from 1,450p.

The pandemic is making a comeback in China with increasing covid cases and city wide lockdowns which has led to March retail sales performing below expectations. However, Q1 2022 GDP growth was 4.8% ahead of expectations for the country.

The IMF’s latest economic forecasts are due at 2pm today which is likely to cause turmoil in the markets.

JTC shares were down 2.9% to 787p in early morning trading on Tuesday, following the fund management services firm’s pre-tax profit climb of 147.2% to £27.8 million from £11.2 million.

The company reported a 28.2% increase in revenue to £147.5 million compared to £115.1 million last year as a result of strong net organic growth of 9.6% and inorganic growth of 18.6%.

JTC saw its EBITDA fall 23.8% to £26.6 million against £34.9 million, along with an EBITDA margin decline of 12.3% to 18% compared to 30.3% in 2021.

The group reported a 57.2% drop in operating profit to £9 million from £21 million, and its earnings per share saw a hike of 127.2% to 20.4p against 9p.

The company highlighted the continued integration of its seven acquisitions in 2021, and confirmed a net organic revenue growth of 8-10% per year in its medium-term guidance for 2022.

“2021 saw JTC execute on its inorganic growth strategy with seven high quality acquisitions completed in the year – the most we have ever achieved in a single calendar year,” said JTC CEO Nigel Le Quesne.

“The quality businesses in Segue, SALI and EFS, also supported our strategic push into the US.”

“Looking ahead, while much of the focus will be on improving and integrating what we have, we also remain of the view that the sector is primed for consolidation and that our proven approach to identifying, securing and integrating high quality acquisitions is a key part of creating long-term value for JTC and our stakeholders.”

The company announced a dividend per share of 7.6p compared to 6.7p, representing a 0.9p increase for 2021.

Spectris shares were up 4.8% to 2,637p in early morning trading on Tuesday, after the precision instruments company reported its divestment of Omega Engineering and its £300 million share buyback scheme.

Arcline confirmed that Omega will join its Dwyer Group portfolio of companies once the agreement has closed, citing interest in the group’s production of specialist sensors for Dwyer’s development of innovative sensors and instrumentation solutions for the environmental and building automation markets.

Omega reportedly generated sales of £129 million in 2021, with an adjusted EBITDA of £19.7 million and a gross assets book value of £197.7 million.

The deal is currently projected for completion early in the third quarter of 2022.

Spectris confirmed that sale of Omega Engineering will leave the firm with Malvern Panalytical, HBK and Industrial Solutions as its three core businesses.

The company said that the divestment would leave Spectris with an improved financial profile, with a specific focus on high precision measurement instruments.

“Spectris today is a more focused, more profitable, and more resilient business, underpinned by a very strong balance sheet,” said Spectris CEO Andrew Heath.

“We are more aligned than ever to end markets with attractive growth trajectories, supported by key sustainability themes.”

“The divestment of Omega will further improve our financial profile.”

Spectris also confirmed the launch of its £300 million share buyback scheme, which will see the group kick off an initial tranche of £150 million, followed by an additional tranche of £150 million to be launched pending shareholder approval at the firm’s Annual General Meeting on 27 May 2022.

“Today’s announcement is yet a further example of our approach to optimising our assets and successfully divesting businesses at multiples higher than the Group as a whole,” said Heath.

“This disposal, in conjunction with the share buyback programme, delivers clear value for shareholders, whilst also allowing us to take advantage of new growth opportunities for our core businesses, in line with our purpose.”

The E-commerce company, Ascential has signed an agreement to acquire Sellics which is a media execution service provider to challenger brands trading on Amazon, on Tuesday.

Sellics will be incorporated with Ascential’s Digital Commerce business unit’s challenger brand expert Perpetua, leveraging its scaled platform to greatly increase penetration of the European market for this fast-growing customer category.

Sellics’ objective is to make Amazon Advertising for eCommerce firms easier and more time-consuming while also enhancing their advertising performance and growing their business.

The group accomplishes this by combining a cutting-edge software platform for ad optimization and automation with market-leading actionable analytics and competitive information, as well as experienced advertising services.

Through a suite of software tools, the media execution service provider offers challenger companies who sell on Amazon in the US and Europe a mix of advertising spend optimization, campaign automation, and profit analytics.

Sellics’ headquarter is in Berlin and has 90 employees. The company is run by its co-founders Franz Jordan who is the CEO, Josef Vataman the CTO, and CMO Thomas Ropel.

“Sellics’ strong presence in the European challenger market and engineering expertise will accelerate Perpetua’s growth outside its existing US operations, while Perpetua itself will provide exciting growth opportunities for the Sellics’ customer base through its advanced product set,” said Duncan Painter, CEO, Ascential.

GlaxoSmithKline shares decreased 0.6% to 1,761.8p in early morning trading on Tuesday, after the company announced its accepted Food and Drug Administration (FDA) application for its chronic kidney disease anaemia treatment daprodustat.

The application was reportedly accepted following GlaxoSmithKline’s ASCEND phase three programme, which consisted of five trials which successfully met their primary efficacy and safety endpoints in both non-dialysis and dialysis patients.

The trials covered 8,000 patients over 4.2 years, with the results presented at the American Society of Nephrology’s Kidney Week last year.

The pharmaceutical giant commented that the drug was developed to provide patients with a convenient oral treatment for chronic kidney disease-linked anaemia complications.

The treatment was based on Nobel Prize-winning scientific breakthroughs, which demonstrated how cells sense and adapt to the availability of oxygen in the human body.

The move marks the third regulatory step in the treatment’s advancement after it achieved marketing authorisation approval from the European Medicines Agency (EMA) and secured regulatory submission acceptance and approval in Japan under the label Duvroq for renal anaemia.

AstraZeneca and Daiichi Sankyo announced that in the United States, Enhertu was granted Priority Review for patients with HER2-mutant metastatic non-small cell lung cancer who had previously been treated.

The supplemental Biologics License Application (sBLA) for Enhertu (trastuzumab deruxtecan) for the treatment of adult patients in the United States with unresectable or metastatic non-small cell lung cancer (NSCLC) whose tumours have a HER2 (ERBB2) mutation and who have received prior systemic therapy has been accepted, according to AstraZeneca and Daiichi Sankyo. Priority Review has also been given to the application.

Priority Review is granted by the Food and Drug Administration (FDA) to applications for medicines that, if approved, would provide significant benefits over existing options by demonstrating improved safety or efficacy, averting serious conditions, or improving patient compliance.

The FDA action date for their regulatory decision under the Prescription Drug User Fee Act (PDUFA) is in the third quarter of 2022.

The FDA approved Enhertu Breakthrough Therapy Designation in this cancer type in May 2020, prompting the Priority Review for AstraZeneca.

Lung cancer is the second most frequent disease worldwide, with over two million new cases expected to be diagnosed by 2020.

Patients with metastatic NSCLC have a particularly bad prognosis, with just about 8% living longer than five years following diagnosis.

There are presently no HER2-directed treatments licenced particularly for the treatment of HER2-mutant NSCLC4, which affects 2%-4% of non-squamous NSCLC patients.

Supplemental Biologics License Application

The sBLA is supported by the Phase I trial published in Cancer Discovery and is based on results from the registrational DESTINY-Lung01 Phase II trial published in The New England Journal of Medicine.

As assessed by independent central review, primary results from previously-treated patients with HER2-mutations of DESTINY-Lung01 revealed a confirmed objective response rate of 54.9% in patients treated with Enhertu (6.4mg/kg).

A total of one (1.1%) complete response and 49 (53.8%) partial replies were found.

A proven disease control rate of 92.3% was recorded, with most patients experiencing a reduction in tumour size.

AstraZeneca’s Enhertu’s median duration of response was 9.3 months after a median follow-up of 13.1 months.

The median progression-free survival was 8.2 months, with a 17.8-month median overall survival.

AstraZeneca’s Enhertu is currently being evaluated in a large clinical trial that will look at its efficacy and safety in a variety of HER2-targetable malignancies, including breast, gastric, lung, and colorectal cancers.

Susan Galbraith, Executive Vice President, Oncology R&D, AstraZeneca, commented, ” The DESTINY-Lung01 trial confirmed the HER2 mutation as an actionable biomarker in non-small cell lung cancer.”

“If approved, Enhertu has the potential to become a new standard treatment in this patient population, offering a much-needed option for patients with HER2-mutant metastatic non-small cell lung cancer who currently have no targeted treatment options.”

“The results of DESTINY-Lung01 showed that Enhertu is the first HER2-directed therapy to demonstrate a strong and robust tumour response in more than half of patients with previously treated HER2-mutant metastatic non-small cell lung cancer,” added Ken Takeshita, MD, Global Head, R&D, Daiichi Sankyo.

“Seeking approval in the US for a third tumour type in three years further demonstrates the significant potential of Enhertu in treating multiple HER2-targetable cancers.”

AstraZeneca shares dropped 0.1% to 10,526p on Tuesday despite announcing the Priority Review for Enhertu.