The two-year US Treasury yields reached 2.495% on Monday morning, marking the highest level since 2019.

On Monday, two-year Treasury yields hit their highest level since early 2019, as investors bet that the Federal Reserve would deliver more rate hikes in the months ahead to keep inflation in check.

In a frequently studied section of the yield curve, the difference between 2-year and 10-year bond yields remained inverted and was recently at minus 6.75 basis points.

The robust March jobs report reinforced the argument that the Fed will need to raise rates quickly to combat rising inflation and a tight job market.

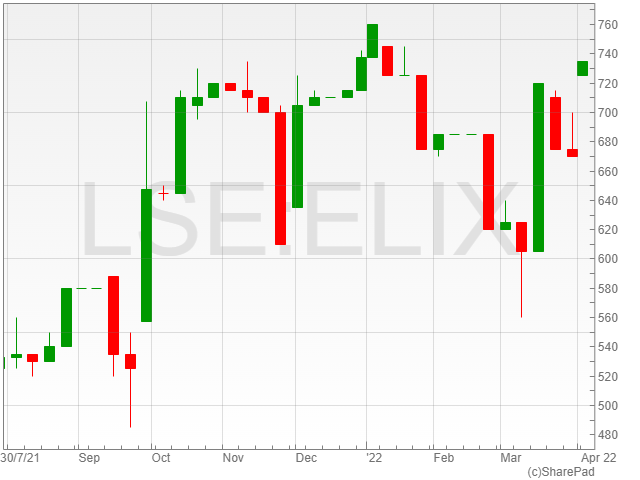

Elixirr shares were up 4.4% to 700p in early morning trading on Monday following the announcement of its 2021 results, which included a 67% increase in revenue to £50.6 million against £30.3 million in 2020.

Elixirr reported an adjusted EBITDA growth of 62% to £15.7 million compared to £9.7 million in 2020 and a pre-tax profit increase of 109% to £12.2 million against £5.8 million in 2020.

The business management consultant firm announced an adjusted diluted earnings per share increase of 58% to 24.2p compared to 15.3p in 2020.

The company also noted a net cash position of £31.8 million following its £17.5 million result in 2020.

Elixirr said that it expects a revenue of £70-75 and an adjusted EBITDA margin of 27-28% in 2022.

The group highlighted its operational accomplishments for 2021, including the acquisition of the Retearn Group in April, and its post period-end acquisition of iOLAP, which is set to add specialist data and analytics capabilities to the company and accelerate its US business growth.

The firm also noted an organic revenue growth of 35%, including 100% growth in its US business, alongside the addition of over 80 new clients and a 50% clientele repeat business rate.

“2021 has been another phenomenal year for Elixirr,” said Elixirr CEO Stephen Newton.

“We have stayed resolute in our commitment to provide a bespoke and high-quality service to our clients, all made possible by the dedication and talent of our teams.”

“This has contributed to our fantastic performance in the market this year and consistent growth since listing.”

Healthcare technology providerInduction Healthcare has collaborated with NHS Trusts in South West London to assist with long-term outpatient care change.

The collaboration comes at a time when the NHS secondary caregivers in England are focusing and spending heavily on digital transformation, with Induction Zesty reportedly set to benefit Trusts in South West London.

Induction Zesty has been advertised as a hospital’s ‘digital front door’, with an easy setup that allows users to manage their appointments, communications, and virtual consultations from the comfort of their smartphone.

Patients can now have a cohesive perspective of their care journey, spanning various caregivers, on a single digital platform.

The combined contracts, which cover 4 of SW London’s NHS Trusts, have periods between 2 to 9 years and will generate a total revenue of roughly £3.6m with an ARR of around £650,000 from FY23 onwards. As installation work is finished and the sites go operational, the firm expects to generate roughly £450K in revenue in FY23 from these deals.

The contracts were partly influenced by a strategic partnership between Cerner and Induction. The partnership developed a combined solution that was made available as part of a value-added reseller agreement to NHS Trusts, which were already Cerner clients as an extension of their current Cerner EPR contracts.

“This is an exciting first step and strong proof point in our strategy to support regional digital transformation via newly forming Integrated Care Systems,” stated, Induction CEO, James Balmain.

“We have a strong pipeline of further Cerner customers who are keen to purchase the joint Induction/Cerner patient portal. Equally encouraging is the positive reaction we’ve seen from customers around the integration of Attend Anywhere into our Induction Zesty product.”

Induction Healthcare shares increased nearly 4% to 42p following the announcement of collaborating with 4 NHS Trusts.

“I have had 11 tremendous years at Aviva, but the time is now right for the challenge of a new sector, and I am hugely excited at the opportunity of being part of Persimmon,” said Windsor back in January.

“I wish Amanda and the rest of Aviva all the best for the future. I am very proud of what we have achieved over the last 18 months.”

Jones’ appointment is scheduled to take effect from 5 September 2022, and follows her position as CFO of RSA Insurance and Interim CEO and of the RSA UK and International business.

Aviva highlighted Charlotte Jones’ previous work experience in finance, including as CFO of Jupiter Fund Management, in which her responsibilities extended to membership on the Board and the Executive Committee with responsibility over finance and corporate strategy.

Jones was also the Head of Group Finance at the Credit Suisse Group and Deputy Group CFO at Deutsche Bank Group.

Her appointment will be confirmed pending approval by the Prudential Regulation Authority and the Financial Conduct Authority.

“This is a really excellent appointment for Aviva,” said Aviva CEO Amanda Blanc.

“Charlotte is a highly experienced CFO with an impressive track record across the insurance and asset management industries.”

“She is an exceptional addition to Aviva and will play a central role as we accelerate our performance and grow.”

Jones added: “”Aviva is both an amazing brand and a business really focused on delivery, and so the opportunity to join as CFO is fantastic.”

“I look forward to working with Amanda and the team, and making Aviva the undisputed market leader in insurance, wealth and retirement.”

Aviva Canada CFO Colin Simpson is set to act as interim CFO until the company welcome Jones to the position in September.

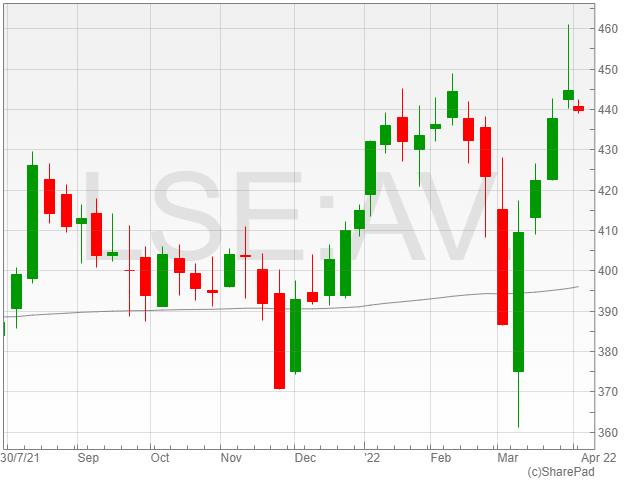

Aviva shares were down 0.5% to 442p in early morning trading on Monday.

The terms of the acquisition were circulated to shareholders in March 2022.

Hochschild Mining is a major precious metals firm that specialises in silver and gold exploration, mining, refining, and sales.

The company has been mining precious metal epithermal vein deposits, and currently owns and manages three underground epithermal vein mines with two in southern Peru and one in southern Argentina.

The mining group is also working on several long-term ventures throughout the Americas.

Amarillo is developing two gold properties in Brazil, both of which are near strong infrastructure and in mining-friendly locations. The Posse gold project is located in Goiás State on Amarillo’s Mara Rosa property.

It reported a favourable definitive feasibility study that demonstrated that it can be turned into a lucrative operation with low costs and a high financial return.

Mara Rosa further suggests that more near-surface deposits could be discovered, extending Posse’s mine life beyond the original ten years.

Ignacio Bustamante, Chief Executive Officer, Hochschild said, “We are delighted to have closed the acquisition of Amarillo which adds the exciting Posse project in Brazil to our portfolio. We can look forward to the commencement of construction and the opportunity to generate strong sustainable value for the Company and the project’s local stakeholders.”

The FTSE 100 gained 0.3% to 7,536 on Friday despite a softer than expected US job data release on Friday. The commodity focused FTSE also shook off a falling oil price to finish the week in positive territory.

Warning signs of a recession have been flashing with the US 5-year and 30-year Treasury yields inverting for the first time since 2006. With worries of an approaching downturn, investors would have watched Friday’s US job data closely for insight on the health of the world’s biggest economy.

The Non-Farm Payroll revealed an increase of 431,000 jobs in March, missing estimates but positively impacting the unemployment rate as it almost reached pre-pandemic levels.

“Wage growth exceeding forecasts could cause markets to wobble but equally that might encourage the Fed not to be overly aggressive at its next policy meeting,” commented Mould.

Oil prices bounced back and increased 0.3% to $105 a barrel on Friday, following sharp declines this week on news of Biden’s plan to supply oil from the US Strategic Petroleum Reserve.

FTSE 100 Risers

Reckitt Benckiser shares increased 3.1% to 6,015. Miners Anglo American and Rio Tinto gained 2.9% to 4,087p and 2.1% to 6,211p respectively.

The retail sector seems to be picking up today despite the rise in the cost of living with Next shares were up 1.9% to 6,141p, JD Sports increased 2% to 151p and Kingfisher shares gained 1.6% to 260p.

Unilever shares rose 1.9% to 3,519p as Morgan Stanley cut the company’s recommendation to ‘over-weight’.

Housebuilding shares had some reprieve on Friday as the sector rebounded from a recent sharp sell off, with Taylor Wimpey leading the sector with gains of 2% to 133p, aside from the exception of Barratt Developments with shares falling 0.1% to 521p.

FTSE 100 Fallers

Aviva shares are down 1.6% to 444p as the company announced the successful completion of its £1bn buyback programme for an average of 408p per share.

3i Group shares decreased 0.67% to 1,379p after the company provided an update on its portfolio regarding no investments in listed close-ended investment funds.

Electrocomponent shares were down 4% to 1,040p. Catering providers, Compass Group shares fell 3.1% to 1,598p. Prudential shares lost 1.1% to 1,121p.

Pearson shares fell 0.8% to 743p as it continued to drop after Apollo withdrew its interest in the company.

The FTSE 250 was up 0.2% to 21,218 and the AIM was up 0.2% to 1,044.5 on Friday as a number of positive company updates helping lift London’s small and mid cap indices.

Rebounding retailers such as Currys also helped lift the indices after recent downside in the sector.

The price of oil hit $104 per barrel for Brent Crude after US President Joe Biden announced the released of one million barrels per day from the country’s Strategic Petroleum Reserve, in a bid to knock down the spiking oil price due to Russia’s war in Ukraine.

Energy prices are set to impact households with a 54% rise in the energy price cap announced by Ofgem today. The cap increase is estimated to add £700 per year to the average household energy bill.

FTSE 250 Risers

888 Holdings shares rose 5.2% to 194.1p as the company enjoyed the boost from its announced strategic investment to launch the group’s new 888Africa venture across select regions in the continent.

Moonpig shares were up 4% to 233.1p in anticipation of the company’s trading announcement next week, which is projected to report an optimistic £283 million in revenue by analysts.

“The group reported a strong set of half year results, and upgraded revenue targets.”

“However, things are still slowing quite dramatically,” said Hargreaves Lansdown equity analyst Sophie Lund-Yates.

“Next week it will be important to see that Moonpig is on track to reach the £283m in full year revenue that analysts are expecting, although this might be a tall order.”

Ferrexpo shares increased 4.1% to 194.3p in anticipation of its trading update next week, however disruption to the firm’s operations in Ukraine have thrown a spanner in the work for its results.

“We will look to publish our accounts as soon as the situation in Ukraine permits us to do so,” said Ferrexpo CEO Jim North.

FTSE 250 Fallers:

Provident Financial fell 5.1% to 290.9p following the dissipating excitement of its 2021 results, which reported a £173.9 million pre-tax profit increase from £39.5 million in 2020.

Oxford BioMedica shares decreased 4.7% to 642p.

Ascential shares dipped 2.6% to 337.4.

AIM Risers:

Quiz shares were up 44.8% to 15.5p after its trading update reported predictions of a £500,000 profit after devastating losses last year, alongside a projected £78 million company revenue.

Simec Atlantis Energy rose 23.2% to 1.9p following a £2.5 million loan for its MeyGen tidal stream project from Scottish Enterprise.

Borders and Southern Petroleum shares increased 17.1% to 1.7p, despite the falling oil prices.

AIM Fallers:

Sustainable work-from-anywhere digital ecosystem company Actual Experience shares fell 14% to 11.4p as the company continued suffer as economies reopened.

UK house prices saw its fastest rise in 17 years in March, with the average house price increasing £33,000 compared to 2021, however, a number of pressures including the cost of living crisis alongside rising interest rates could deal a blow to prices in 2022.

On Thursday, the National Statistics Office announced a growth of 1.3% in the UK’s GDP, with a 6.8% fall in the household saving ratio.

It’s not breaking news that consumer spending and the cost of living are currently being impacted by rising fuel costs and inflation.

With the exception of well-off consumers, buying a home, and keeping up with mortgage payments is becoming more and more difficult. Companies such as Lloyds and Santander are trying to ease the process by introducing competitive mortgage rates, however, if interest rates continue to rise, banks will be forced to increase mortgage rates.

With the cost of living on the rise, paying off mortgages is becoming a struggle for consumers who are tackling problems associated with keeping the heat on and finding cheaper modes of transport for their daily commute. This struggle may hurt buyers’ sentiment and impact activity in the housing market.

If soaring inflation alongside increasing interest rates persists, the housing market may see a slow down in the coming year.

Mike Scott, the chief analyst at estate agency Yopa, said “[the] housing market cannot ignore the wider economy forever” resulting in a slow down but not a “significant fall” in housing prices.

Housebuilding shares

Now question is, what’s going to happen to housebuilding stocks with prices rising all over the place?

To begin with, we have to look at the consideration that margin pressures will prevail when the cost of construction increases for the property builders. With higher costs and flat or decreased revenues, the company will see a decline in profits.

When analysing property builders and their financial health, investors should look out for the strength in the company’s order book, its revenue levels, dividend yield, and factors impacting its operation and outlook for the coming year.

Taylor Wimpey

Taylor Wimpey (TW) saw an increase in revenue to £4.28bn from £2.79bn in 2020, almost reaching pre-pandemic levels of £4.34bn. The company’s pre-tax profit more than doubled from 2020 to £679m in 2021.

Despite a drop in orders from 10,685 to 10,009 in 2021, the group achieved a total of 14,302 projects, including collaborations with joint ventures, which exceeded a total of 9,799 houses in 2020.

Taylor Wimpey also saw a year-on-year increase in net cash from £545m in 2019 to £719m in 2020 and £837m in 2021. The group returned to paying a dividend from nil to 8.2p in 2021, and has a dividend cover of 2.1x. Taylor Wimpey has a forward PE of 6.9x and a ROCE of 16.7. Taylor Wimpey shares lost 24% YTD.

Countryside Properties

Countryside revenues soared 54% to £1.37bn from £892m. The property builder made an operating loss of £5.4m in 2020, however, in 2021, the company returned to profits of £71m.

Countryside held net cash of £41m, which is down from £98m during 2020. The group’s EPS has also increased from a loss of 8p to a profit of 13.8p in 2021. In 2021, Countryside Properties increased output by 33% to 5,385 homes compared to 2020.

The shares of Countryside Properties lost nearly 40% since January 2022. The group has a P/E ratio of 9.2x and a ROCE of 7.7x.

Persimmon

Persimmon reported total revenue of £3.61bn in 2021, an increase from £3.33bn in 2020, just missing pre-pandemic levels of £3.66bn in 2019.

The company said “disciplined cost control, combined with a positive pricing environment” had a positive impact on profit before tax, as it increased from £783m to £966m in 2021.

Persimmon completed 14,551 houses in 2021 compared to 13,575 with the average new house selling price at £237,078 instead of £230,534 in 2020. The group also reported current forward sales of £2.21bn since January 2022 and said that demand has stayed strong despite the cost of living rising across the globe.

The group proposed a total dividend of 235p for 2021, unchanged from 2020, with intereim dividend of 125p and a final dividend of 110p. The group’s dividend cover is 2x and has a forward P/E of 8.4x with a 25.4x ROCE. The company’s shares dropped 25% YTD.

Bellway

Recently, Bellway posted its interim results in which the company reported a 3.5% rise in revenue to £1.78bn in 2022 as a response to strong market conditions.

Bellway had an output of 5,694 houses in 2022 compared to 5,656 in 2021 due to “strong operational delivery” despite production problems. The company also saw a 5.8% rise in the overall reservation rate to 202 per week compared to 191 in 2021.

The company’s profits increased by 8.9% to £327m as opposed to £300m in 2020 as Bellway maintained cost controls and price optimisations. The group noted net cash of £195.8m which will help them invest in opportunities for growth.

Bellway increased its interim dividend to 45p compared to 35p in 2021, and the board anticipated a 3x dividend cover with respect to underlying earnings. However, the company plans to reduce that coverage to 2.5x to assist in obtaining more growth opportunities through investments.

Bellway’s forward P/E ratio is 6.1x and ROCE is 14.5x with a dividend yield of 4.8%. Bellway’s shares dropped 26% since the start of 2022.

In general, it seems that property builders are optimistic about the future with them confident about sales for 2022 and are showing a propensity to invest in additional land. Going forward, I think despite consumer spending taking a hit, and potential market volatility, home building stocks will provide long-term investor value.

The business will reportedly create a new Adhesive Technologies division for Synthomer, giving the group a leading position in the international adhesive market.

“The business is well-invested, with six manufacturing facilities, a highly skilled and experienced workforce and has a … strong innovation pipeline which will deliver meaningful revenue growth over the next few years,” said Synthomer Chief Executive Calum MacLean in a statement last October.

Synthomer said it expects the new division to bring in an earnings per share in the double-digits within its initial year, alongside annual pre-tax synergies predicted at $23 million at the close of its third year in operation.

The company highlighted its increased exposure to attractive high-end markets with strong gross domestic product (GDP) fundamentals.

The news followed the company’s strategy reported in its 2021 annual results, in which 99% of shareholders voted in favour of raising its borrowing restriction from £1.5 billion to £2 billion in order to accommodate the acquisition, with an extra £200 million equity placing at an Extraordinary General Meeting in December last year.

“Our Adhesive Technologies division adds a very exciting new growth dimension to Synthomer,” said Synthomer CEO Michael Willome.

“Its portfolio takes us into more specialised, more global and higher growth segments and as part of Synthomer, we are confident that we will be able to expand this part of our business significantly.”

“I would like to extend a warm welcome to our new Adhesive Technologies employees around the world.”

“I look forward to working together and realising the value potential that lies ahead.”

Synthomer shares were up 0.2% to 306.4p in early afternoon trading on Friday after the company made its announcement.

The US added 431,000 Nonfarm Payrolls (NFPs) in March this year, coming below the forecast 490,000 increase projected by the US Bureau of Labour and Statistics.

However, the figure was compensated by a 750,000 result in February, representing a 72,000 surge compared to initial predictions of 678,000.

Unemployment in the US fell to 3.6% in the latest figures from the US Nonfarm Payrolls (NFP) report, amounting to a 0.1% boost against the projected level of 3.7%.

Government payrolls reportedly increased by 5,000, a decline from the 11,000 rise in February, and manufacturing payrolls increased by 38,000 in March, which exceeded the expected figure of 30,000 and matched the 38,000 gain from February, which had initially been predicted at 36,000.