Funds would also be used for working capital and corporate costs.

The fundraise comes shortly after the release of their full year results which showed the company had £6.2m in cash and cash equivalents as of 30th June 2021.

The Chairman’s Statement in the full year results highlighted Greatland Gold’s plans to accelerate development in the pursuit of early cash flow.

“The Havieron gold-copper discovery is a world class deposit and continues to deliver excellent results with significant intercepts of high-grade gold and copper outside of the existing resource shell. With over 200,000 metres of drilling now completed, the equivalent distance of London to Sheffield we have significantly enhanced our understanding of the deposit and of the likelihood of continuing to upgrade to the Mineral Resource Estimate in the near-term.”

“Subsequent to the year end, a Pre-Feasibility study was released on an initial segment of the Havieron deposit which has detailed a development pathway to first gold produced and operating cashflow. The study revealed the tip of the Havieron iceberg with a fraction of the initial resource supporting the total capex of the project, justifying a fast start approach to early cashflow generation and reinvesting back into Havieron development and infrastructure. This supports our belief that the profile of Havieron makes it a globally unique opportunity for bringing a low risk, low capex tier-one gold-copper mine into production.’

The latest figures found retail sales in the UK to rise 0.% in October.

The Office for National Statistics (ONS) said retail sales rose last month after two months of no movement.

Non-food stores saw sales rise by 4.2%. Toy stores and sports equipment stores saw particularly strong sales whilst clothing sales are now just 0.5% below pre-pandemic levels.

Danni Hewson, AJ Bell financial analyst, comments on retail sales figures: “Consumers seem to have heeded warnings from some retailers that the best way to make sure they have exactly what they want under the tree this Christmas is to buy early.”

“Santa’s sack this year will be filled with clothes, toys and games. It will also contain a substantial number of second-hand items, whether that’s a reaction to rising prices, to a glut of goods thanks to lockdown clear outs, or because people are thinking more sustainably, the result is the same.”

“What is worth noting is our changing habits. Christmas shopping is an experience, not always an enjoyable one, but one that does seem to demand at least one in-person shopping trip. Finding that perfect gift is often about browsing and that’s had a knock on to online sales.”

“Though still way above pre-pandemic levels the last month saw online retail fall to its lowest level since March 2020, a factor which will boost confidence amongst bricks and mortar retailers, particularly those independents that offer the unique and great service to boot.”

Nationwide profits have more than doubled for the first half of the year.

In the same period last year, profits were £361m. They have now doubled ti £853m for the six months to 30 September.

Chief financial officer Chris Rhodes said: “During the pandemic, strong demand for mortgages, coupled with macro-economic uncertainty, led to higher margins on mortgage lending. This resulted in significantly higher income, and a very strong overall financial performance.”

“These have been very popular, resulting in a successful ISA season, increased deposits, higher mortgage lending, and a larger share of the current account market.”

Despite an eventful decade that has proved unsettling for markets, The Henderson Smaller Companies Investment Trust has consistently outperformed its benchmark by looking through the noise and sticking to its tried and tested investment process. In this article, Neil Hermon, Portfolio Manager of the Henderson Smaller Companies Investment Trust, explores moments that have defined the decade in Europe and reveals the ‘secret sauce’ to the Trust’s long-term outperformance.

Look past the noise, it’s the stocks that count

Investors could spend months mulling over geopolitical events or gloomy economic forecasts and what they might mean for their portfolios and their stock picking process. The ‘macro’ is undoubtedly important – unexpected events such as the pandemic, can shake markets vigorously – so it’s understandable that they’re given close attention. Yet, very few long-term investors attribute their investing success to how they navigate the range of complex scenarios that may play out in markets, but rather a disciplined approach to stock picking that remains consistent.

The past decade is a case in point. Though, by some measures, it was a blinding success for some equity investors, many describe the period as the ‘most hated rally in history’. Fresh from a searing financial crisis and a prior decade that proved a flop for equities, gains were built on a hesitant economic recovery, sceptical investor optimism, and underpinned by doses of emergency stimulus. With newspaper tabloids pedalling potential catalysts for the next financial downturn, there seemed plenty to worry about for European and UK investors.

At Henderson Smaller Companies Investment Trust, we looked past this macro noise, and instead focused on finding high quality, high growth businesses within the small and mid-cap (smid-cap) market. As long-term investors, we believe that these sorts of companies will weather the storms and thrive in years beyond them. The Trust aims to maximise shareholders’ total returnsby investing in smaller companies that are quoted in the UK. And through a disciplined and consistent investment approach and philosophy, the Trust has beaten its benchmark in 16 of the 18 years, in which I have been the manager.

A decade of curveballs

There is a reason why some call it the most hated bull market in history, and this resonates particularly strongly with European and UK investors. Still recovering from the financial crisis, the 2011 sovereign debt crisis dealt a fresh blow to Europe’s recovery. Political churn uncovered financial mismanagement by a range of governments, starting with Greece. Ratings downgrades and rising yields ensued, and snappy headlines containing the now infamous ‘[country]-exit’ portmanteau – in this case ‘Grexit’ – led to fears of contagion across the bloc and abroad.

To thwart the dissolution of the union, politicians argued and debated, and rounds of bailouts eventually followed. Meanwhile, central banks dosed markets with quantitative easing (QE) to sooth concerns and keep borrowing costs low amid the uncertainty. Yet still, the crisis dragged on for years, and European equities remained broadly out of favour.

Some would say the difficulties in finding a political solution in Europe laid the groundwork for Brexit, with groups taking aim at the perceived sluggishness of multilateral organisations such as the European Union and the International Monetary Fund amid a backdrop of rising nationalism. After the shock UK referendum result in 2016, four years of political spats between Britain and its incensed neighbour followed, and it was UK equities’ turn to feel the cold from investors.

Protracted Brexit uncertainty segued neatly into pandemic chaos, which sparked a global bear market. The impact was sharp and dramatic, although relatively short-lived thanks to the rapid injection of fiscal and monetary stimulus. Though Brexit uncertainty has abated, and we slowly put the pandemic to bed – the threat of inflation, rising transportation costs and concerns that central banks will begin removing stimulus and raise interest rates have emerged to hang over markets. It seems the anxiety never ends.

Remaining clear-eyed

Though the decade reads rather nightmarishly, the returns have been quite the opposite and particularly strong for smid-cap stocks as illustrated below1:

Returnsover the last decade

FTSE 100

+93%

Euro Stoxx-600

+178%

FTSE 250

+198%

Numis Smaller Companies Index

+211%

Henderson Smaller Companies Investment Trust

+521%

Source: Bloomberg, 31/08/2011 to 31/08/2021

Warren Buffett once remarked that he doesn’t concern himself with the “macro stuff” because, although important, it is ultimately “not knowable”. Instead, he mused, it is much better to focus on “what is important and knowable”. For us, the Henderson Smaller Companies Investment Trust team – bottom-up stock pickers – what is important and knowable are the companies we invest in.

First, smaller companies tend to outperform broader markets over time. This is because by their very nature, they are more innovative, faster-growing, and have more entrepreneurial management at the helm. In addition, the ability to leverage their operations makes easier for them to turn a pound of earnings into two when compared to larger firms.

Second, we believe that strong, high-quality growth companies are not only positioned to survive the crisis of the day but should continue on a trajectory of solid growth as idiosyncratic macro events fade into the history books. However, small, and mid-cap stocks can be more volatile compared to their large counterparts.

We constantly follow the tried and tested process I have been using ever since taking over management of the Trust in 2003. The primary ingredient we look for in a company is solid fundamentals – all the essential bits of a business that contribute to its success. By understanding these fully and ensuring they’re robust, we gain detailed insight into the potential of the company.

Alongside the insights and expertise of the small and mid-cap team at Janus Henderson Investors, we evaluate companies through our ‘4Ms’ process. We analyse the quality of the business ‘model’ and its ‘management’, the ways in which it makes and uses its ‘money’, and the ‘momentum’ of its earnings reported to investors. This enables us to gain a clear understanding of the business and its markets. This also includes a strong valuation discipline encompassing a wide range of valuation techniques to ensure that the growth stocks we are purchasing are bought at an attractive price. It’s neatly summed-up as GARP – growth-at-a-reasonable-price.

The buy and sell criteria surrounding the 4M’s model is outlined in the chart below2:

What is more, we aim to hold on to stocks and ‘run our winners’ as we believe long-term investing is consistent with wealth creation. This is evidenced in our portfolio holdings: 19 stocks have been held for longer than 10 years and have weathered the storms of the last decade, while helping deliver exceptional performance. Prime examples of stocks that fit this bill can be seen in the table below3:

Stock

Tenure

Return (share price total return)

Bellway

+15 years

+707%

RWS

+15 years

+883%

Howden

+10 years

+1008%

Source: Bloomberg, share price total return, 31/08/2011 to 31/08/2021

This consistency of approach has also delivered at the portfolio level. The Trust has returned +521% over the last decade (ending August 2021) compared to the benchmark (Numis Smaller Companies Index) return of +211%. This is significantly higher than its large-cap counterparts which have returned +93% (as measured by the FTSE 100) over the same period. More recently, the Trust outperformed its benchmark over its last financial year ending May 2021 – meaning it has outperformed its benchmark in 16 of the last 18 years. It also marks the 18th consecutive year the Trust has increased its total dividends. This consistency in outperformance not only reflects the quality of the team, but also highlights the importance of staying disciplined and sticking with a tried and tested investment process, in spite of the macro noise that has characterised the decade.

The next leg

On the whole, the outlook for markets looks much brighter than it has been for years. Companies are performing strongly, profits are growing buoyed by the release of pent-up consumer demand, and UK valuations remain cheap compared to developed markets. However, inflation poses a risk, QE will soon be withdrawn, and who knows what might cause the next financial downturn. What is clear, however, is this is a stock pickers market and the ability to tune out the noise and focus on the fundamentals will be key to generating solid returns. As such, we at Henderson Smaller Companies Investment Trust, will continue to focus on what is “important and knowable”.

2 Source: Henderson Smaller Companies Investment Trust: A decade of outperformance, as at August 2021

3 Source: Bloomberg, share price total return, 31/08/2011 to 31/08/2021

Discrete year performance % change (updated quarterly)

Share Price

Nav

30/09/2020 to 30/09/2021

66.1

56.6

30/09/2019 to 30/09/2020

-10.6

-4.0

28/09/2018 to 30/09/2019

-2.9

-5.2

29/09/2017 to 28/09/2018

18.4

10.6

30/09/2016 to 29/09/2017

23.6

26.2

All performance, cumulative growth and annual growth data is sourced from Morningstar

References made to individual securities should not constitute or form part of any offer or solicitation to issue, sell, subscribe, or purchase the security. Janus Henderson Investors, one of its affiliated advisors, or its employees, may have a position mentioned in the securities mentioned in the report.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

IMPORTANT INFORMATION

Please read the following important information regarding funds related to this article.

Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser.

Specific risks

If a trust’s portfolio is concentrated towards a particular country or geographical region, the investment carries greater risk than a portfolio diversified across more countries.

Most of the investments in this portfolio are in smaller companies shares. They may be more difficult to buy and sell and their share price may fluctuate more than that of larger companies.

This trust is suitable to be used as one component in several in a diversified investment portfolio. Investors should consider carefully the proportion of their portfolio invested into this trust.

Active management techniques that have worked well in normal market conditions could prove ineffective or detrimental at other times.

The trust could lose money if a counterparty with which it trades becomes unwilling or unable to meet its obligations to the trust.

Shares can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

The return on your investment is directly related to the prevailing market price of the trust’s shares, which will trade at a varying discount (or premium) relative to the value of the underlying assets of the trust. As a result losses (or gains) may be higher or lower than those of the trust’s assets.

The trust may use gearing as part of its investment strategy. If the trust utilises its ability to gear, the profits and losses incured by the trust can be greater than those of a trust that does not use gearing.

Derivatives use exposes the trust to risks different from, and potentially greater than, the risks associated with investing directly in securities and may therefore result in additional loss, which could be significantly greater than the cost of the derivative.

References made to individual securities should not constitute or form part of any offer or solicitation to issue, sell, subscribe, or purchase the security. Janus Henderson Investors, one of its affiliated advisors, or its employees, may have a position mentioned in the securities mentioned in the report.

For promotional purposes. Not for onward distribution. Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser. Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the law change. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Capital International Limited (reg no. 3594615), Henderson Global Investors Limited (reg. no. 906355), Henderson Investment Funds Limited (reg. no. 2678531), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Henderson Management S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

Founders Omid and Nima Pakseresht along with their executive team of impact and finance professionals have just secured 140% of their pre-seed target in the first 24 hours of their public crowdfunding launch from 75 investors.

Currently raising investment on Seedrs, GOODFOLIO is building a simple, transparent, and personalised ethical investment platform. GOODFOLIO enables everyday and sophisticated investors to invest in companies and industries that share their ethical values.

GOODFOLIO’s mission is to increase the flow of capital into sustainable industries and responsible companies.

Although 77% of people with over £25k in investable assets would choose sustainable investments, only 13% have already done so.

Starting with Stocks and Shares ISAs and General Investment Accounts, GOODFOLIO’s soon to be launched investment platform aims to address this gap by providing the tools and resources needed for investors to build and manage customised portfolios that align with their ethical values.

Having made substantial accomplishments to date and in a short space of time, GOODFOLIO aims to make ethical investing the norm.

Assembled a diverse and engaged leadership team and advisory board with extended leadership experience in finance, impact and technology

Build a valuable waiting list community of 150+ future customers with average £90k in investments

Signed letter of intent with a UK charitable trust to use GOODFOLIO for management of $1m+ in investable assets once regulated and launched

“This is a beautiful and very inspirational project and I hope it picks up and changes the way people look at investment” waiting-list member and market research participant.

The Funds Under Management in responsible and sustainable investment funds grew by 89% between January 2019 and June 2020 to £33 billion. The top 3 incumbent UK investment platforms (Hargreaves Lansdown, interactive investor, and AJ Bell) generate an estimated ~£1bn in annual revenue.

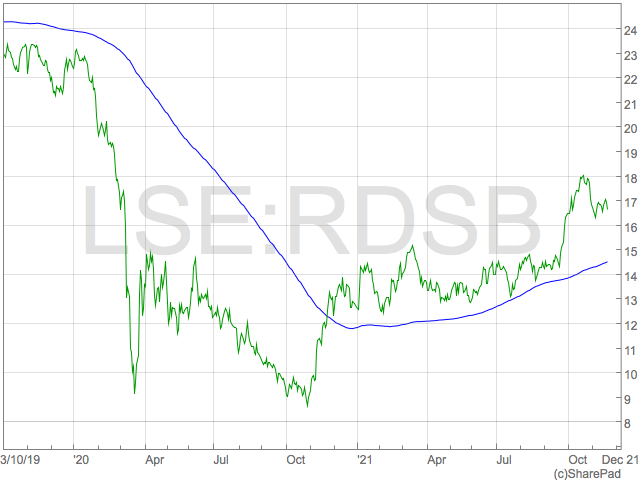

The Shell share price rally has been derailed by a poor Q3 update and the recent dip could be looked upon as an opportunity for investors seeking a buying opportunity in Shell shares.

Recent news around Shell has focused on their decision to change their share structure and fighting off activist investor plans to break the company up, but the value we see in Shell shares stems from their transition to clean energy and the strength of their current energy business.

While Shell is under pressure to become cleaner and greener faster than they currently are, investors will do well to remember Shell is a huge business and although this process is underway, it will take many years for Shell to earn significant revenues from green energy.

However, Shell are growing their operations in clean energy in a big way. We previously wrote Shell’s future prosperity, and shareholder returns, was inextricably linked to how fast they pivot to clean energy and low carbon solutions.

With COP26 driving home the need to drastically change our energy consumption mix, the spotlight is on Shell is now more than ever.

investors will be pleased that Shell has significantly ramped up their activities in clean energy in an effort to meet Net Zero targets.

Another example of Shells shift to be cleaner is a recent partnership to build a 58-megawatt solar farm in Alberta.

“We are transforming Scotford into a world-class site that will provide our customers with lower-carbon fuels and the products they desire,” said Mark Pattenden, Shell Canada Senior Vice President, Chemicals and Products.

“Partnerships like this will enable Scotford to contribute to Shell’s overall plan to become a net-zero emissions energy business by 2050, in step with society.”

While these projects highlight Shell’s intention to become greener, the fact still remains the company earns almost all of its money from the production and distribution of fossil fuels, and for now, will be the focus of investors determining the value of Shell’s business.

Shell share price

Investors who held throughout the pandemic will now be feeling slightly better about their holdings, however Shell shares are yet to get anywhere near the 2,300p pre-pandemic highs.

Despite Shell enjoying higher energy prices, their Q3 results were a major disappointment for investors and derailed a steady rally in shares.

“Normally one shouldn’t get too hung up over a mere three months’ trading, but this was meant to be Shell’s big quarter, given the surge in oil and gas prices in the past few months. Sadly, it has missed earnings forecasts and left investors feeling frustrated,” said Russ Mould, investment director at AJ Bell after Shell’s Q3 results.

This frustration caused a near 10% decline in the Shell share price over the following days.

we would argue this dip presents an opportunity for buyers looking for a long term holding in Shell.

The attractiveness stems from the dividend and the low forward PE ratio.

Shell has as a forward PE ratio just 9 based on analyst expectations of earning for next year. Of course, this is highly dependant on the price of oil and gas over the next 12 months and it is highly unlikely Shell disappoint on the earnings front in Q4 as much as in Q3.

In addition, the Shell dividend is creeping back up to what it was and strong cash flow generation in Q3 will support further increases in the regular dividend in the future.

Investors also have a $7 billion distribution from the sale of their Permian assets to look forward to.

The FTSE 100 underperformed European peers on Thursday as the inverse relationship with the pound stopped the index in its tracks.

Despite strong gains in the house builders and Royal Mail, the FTSE 100 failed to produce the gains evident in European indices as the miners, energy companies and consumer stocks earning a large proportion of their revenue overseas fell.

“The FTSE 100 continues to drift having fallen just short in its effort to reclaim pre-pandemic levels,” says AJ Bell investment director Russ Mould.

“Once again, the index is left in the miserable position of being shown up by its global peers, many of which had put their Covid losses behind them months ago or even longer. In a global index sports team the FTSE is getting picked dead last.

“Mounting inflation has helped drag the index back as it raises the likelihood of a pre-Christmas rate rise, thereby boosting the pound. When some 70% of its constituents’ earnings are derived from overseas, strength in sterling isn’t that helpful.”

“We have delivered good financial and operational performance. Strong leasing activity, significantly improved rent collection and increasing values across our Campuses and Retail Parks have driven 6.1% total returns in the half,” said Simon Carter, British Land CEO.

Royal Mail was also higher after releasing a robust report showing progress in their strategic review and a jump in parcel deliveries. The group said they would return £400m to shareholders.

After strong results, the Royal Mail has promised a £400m to shareholders.

The group saw a pandemic boom and adjusted operating profits surged to £404m for the six months ended in September. Royal Mail has forecast full-year profits of £500m.

“The pandemic has resulted in a structural shift and accelerated the trends we have been seeing,” said chief executive, Simon Thompson.

“Domestic parcel volumes, excluding international, are up around a third since the pandemic, whilst addressed letter volumes, excluding elections, are down around a fifth.”

“This reaffirms that our strategy to rebalance our offering more towards parcels is the right one, and demonstrates the need to start defining what a sustainable Universal Service is for the future.

“I want to thank our teams for what we have delivered so far: it is an impressive start but there is still much more to do together,” he added.

Investec profits have more than doubled in the first half of its new financial year.

Increased client activity and lower funding costs boosted profits at the FTSE 250 group, which is offering 15% of its 25% stake in asset manager Ninety One in shares to its shareholders.

Investec has announced an interim dividend of 11p.

CEO Fani Titi said: “We’re in the process of reducing our group portfolio to add further value to shareholders, now that we’ve seen a recovery in the level of uncertainty in the market, paired with our significant earnings recovery.”

“Due to that recovery, this 15 per cent was the surplus capital we could deploy, and we remain flexible about what we will do with the remaining 10 per cent in the future.”

“We maintain a level of conservatism for factors that remain difficult to model,” Titi told reporters, highlighting the firm’s caution around the remaining uncertainties in the economy’s recovery from Covid and expected market volatility.

“The changes made to simplify and focus the group are bearing fruit, positioning us well for the future.”

Flutter Entertainment has said it will buy bingo group Tombola in a £402m deal.

The owner of Paddy Power and Betfair has purchased the group and the deal will be completed early next year.

Tombola has around 400,000 monthly users and is based in Sunderland and Gibraltar. It had revenues of £164m in the year to the end of April.

“Tombola is a business we have long admired for its product expertise, highly recreational customer base and focus on sustainable play,” said Peter Jackson, chief executive of Flutter.

“The brand aligns closely with Flutter’s safer gambling strategy, a key area of focus for us.”

“As the time comes for Phil to hand over the reins, I would like to thank him for building the success story that the business is today and I look forward to welcoming the Tombola team to Flutter and growing a sustainable business for the future together,” he added.