First Tin has two tin projects in relatively safe jurisdictions in New South Wales, Australia and Germany. An independent ESG Digbee audit is underway, and this will make them even more attractive to customers. Supplying traceable and verifiable tin is important to the strategy.

Demand for tin is likely to outstrip supply and this could keep the tin price up. The Australian project should be profitable even if the tin price fell. Industries that require tin include electric vehicles, energy storage, semiconductors and mobile telecoms.

The shares opened at 32.5p and ended the first day of tradi...

Aura Renewable Acquisitions is a new shell seeking acquisitions in the renewable energy sector and it plans to build up a significant group covering the UK and international markets. The initial intention is to focus on the supply chains of the renewables sector.

The share price opened at 15p and ended at 17p (16p/18p), which is a 70% premium to the issue price. There were 16 trades and the largest was worth £6,561.

The shares are trading at double the level of cash held by Aura Renewables, although the quotation does also have a value. High enough for now.

==========

Aura Renewable Acquisitio...

Managed IT and networking services provider AdEPT Technology (LON: ADT) reassured the market that the 2021-22 figures will be in line with expectations. There will be additional costs this year, but the poor performance of the share price is puzzling considering that the prospective earnings multiple is so low.

There was a good finish to the financial year and that meant that the revenues and profit will be broadly in line with forecasts. Managed services revenues continue to increase. New clients include the TUC and Rolls-Royce.

There was some disruption from electronic component shortages an...

Anglesey Mining (LON: AYM) has made the switch from the Main Market to AIM. Anglesey Mining has been listed since May 1988, but management believes AIM is a more suitable market because it will provide greater flexibility for transactions and potential tax benefits.

The company’s main asset is the 100%-owned Parys Mountain copper lead zinc deposit in Anglesey, north Wales. Drilling is ongoing and further environmental work is required to obtain permits for restarting operations.

Four of the nine planned holes have been completed. Assay results from recent samples should be available in the nex...

Attraqt Group (AIM: ATQT) are unchanged at 30.5p with a Mkt Cap of £61m after reporting its finals to December. ATQT provide AI (Artificial Intelligence) search and SaaS solutions to online retailers and brand owners that are seeking increase sales by improving online shopping. The platform enables internet retailers to personalise services to individual customers, in real-time, across both online and offline channels (omnichannel). ATQT system recorded a 100% availability through peak trading periods of Black Friday and Christmas. Its Revenue increased 9% to £22.9m with Gross Margins slippi...

Strong corporate updates helped the FTSE 250 and the AIM index finish the week on a positive note, adding to a reasonable week of gains in the UK’s small and mid caps markets.

Travel shares enjoyed a positive session after airline regulators urged airline companies to set deliverable schedules in light of recent flight cancellations due to staffing issues as a result of the latest wave of Covid.

This lead to airline company’s such as EasyJet and Wizz Air shares to rebound after a turbulent week with over 200 flight cancellations between them.

FTSE 250 Risers

The iron ore miner, Ferrexpo shares flew 11% to 186p despite the company’s production update stating an 11% fall in iron ore pellet production due to operational and logistical constraints following the Russia-Ukraine war.

Ferrexpo reported a total iron ore pellet production of 2.7m tonnes in Q1 2022, in line with the same period in 2021.

The group generated sales of 2.6m tonnes in Q1 2022, scaling production activities to meet the accessible pellet demand in the market.

“Ferrexpo’s production was remarkably down just 2% year-on-year in the first quarter – its operations are after all outside the main conflict zones,” said Russ Mould, Investment Director, AJ Bell.

“However with the limitations associated with exporting to Europe via rail and barge, management are understandably looking for alternative seaborne options while activities at its usual hub – the Black Sea port of Pivdennyi – remain suspended.”

CMC shares gained 9% to 262p after the online trading company said it expects its annual profit to come at the upper end of forecasts after enjoying its “strongest quarter” of its financial year. The company saw annual net operating income amount to £280m, on the top end of expectations, in Q4 2021.

CMC saw a hike in usage during the pandemic despite market volatility leading to a net operating income of £409.8m, 32% higher than Q4 2021 figures. However, compared to pre-pandemic times, CMC’s net operating income increased 11% from £252m.

Volution Group shares rose 3.3% to 425p after Jefferies raised the company’s price target from 480p to 560p.

JP Morgan cut Countryside Properties’ price target from 280p to 250p helping the shares increase by 3.7% to 276p.

EasyJet and Wizz Air shares gained 3.3% and 2.3% on Friday after the UK aviation regulator urged airlines to set “deliverable” schedules after staffing issues disrupted operations leading to flight cancellations.

EasyJet shares movement from 29-11-21 to 8-4-22

FTSE 250 Fallers

International Public Partnerships shares dropped 4% to 164p after the company announced its plans to raise £250m through an equity issue. The funds raised will be used towards part-payment of a corporate debt facility and investing in its pipeline.

888 Holdings’ shares fell after the company announced an accelerated bookbuild to acquire William Hill yesterday. At the time, 888 also announced the enterprise value of William Hill assets has been lowered to £1.95bn on Thursday.

UBS cut Victrex’s price target to 1,750p from 2,150p leading the company’s shares to drop 0.7% to 1,800p today.

On Friday, abrdn Private Equity Opportunities Trust, NCC Group, Spirent Communications and Homeserve saw their shares lose 2.3% to 500p, 2.2% to 192p, 1.5% to 237p and 0.8% to 873p.

AIM Fallers

Sensyne Health cratered 80% to 2p after the company had to raise £15m to save the sinking ship leading to worried investors as the company already was not generating returns.

Uru Metals’ shares rebounded 18% to 325p after seeing highs of 400p on Thursday.

Engage XR shares rebounded 8.8% after the share gained 50% yesterday following the company’s statement regarding funding being provided to Engage’s US partner VictoryXR by Meta Immersive Learning to help roll out 10 ‘digital twin’ university campuses in the metaverse using Engage’s platform.

Osirium Technologies stumbled on Friday after a transformational week for the company following the company’s announcement of a record quarter for bookings in Q1 2022 on Tuesday.

Sound Energy shares sank 8% to 2.1p after the company decided against making a bid for Angus Energy.

Sound Energy’s decision to not make an offer to Angus Energy lead Angus’ shares to fall 5.5% to 1.3p on Friday.

AIM Risers

The transport system services provider’s shares soared 38% to 146p after Journeo signed a 3 year deal with FirstGroup’s First Bus UK for £9m, marking it the largest deal till date for Journeo.

Webis Holdings gained 13% to 3.5p after the company said its US subsidiary, WatchandWager.com inked a deal for the next 5 years to operate at a racetrack in Arizona.

Avacta Group’s shares rallied 9.5% to 97.5p after drug developer and diagnostics company said AffyXell Therapeutics, its joint venture with Daewoong Pharmaceutical, signed an agreement with Biocytogen to collaborate on a new immune disease in vivo models, testing the toxicity of and conducting proof-of-concept for AffyXell’s drug candidates, using the developed disease model.

Jet2 shares increased 4% to 1,204p after the company reassured investors that signs of recovery are being seen its order books as travel restrictions ease. The company noted a 14% increase in summer sale seat capacity compared to the summer of 2019.

Invinity Energy Systems rose 12% to 90.5p after the manufacturer of utility-grade energy storage announced the completion of a successful test and validation program by Hyosung Heavy Industries and subsequently signing a non-binding MoU for a global partnership with an exclusive relationship in Korea.

Physiomics, oncology consultancy company, signed a new contract with Servier Group to provide specialist mathematical modelling services using the Virtual Tumour software platform. The deal helped the company’s shares gain 0.5% to 4.5p on Friday.

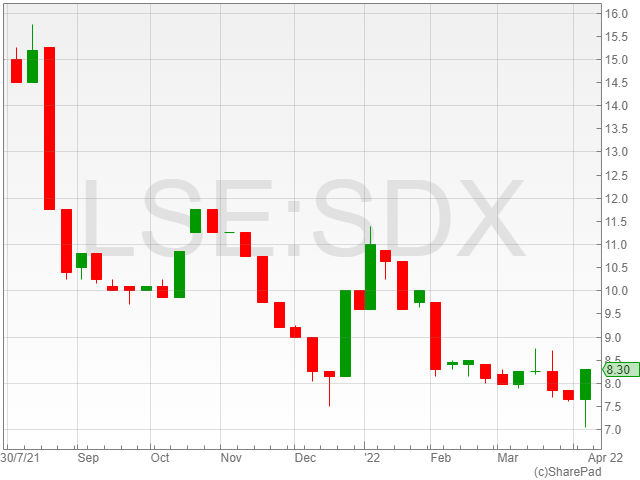

SDX Energy shares were up 2.1% to 8.2p in late afternoon trading on Friday after the energy firm reported the successful spudding of its MSD-20 infill development well on its Meseda field.

The well is estimated to take around six weeks to drill, finish and tie-in to the group’s existing infrastructure.

The MSD-20 is expected to cost around $900,000 to $1 million to drill and tie-in, with an initial production of 300 barrels of crude oil per day.

The resulting contribution to the company’s cashflow is projected to recoup the project’s costs in an estimated five to six months, based on the current price of oil.

The well is the third of 13 total wells in the company’s drilling project on the Meseda and Rabul oil fields based in the West Gharib concession in the Egyptian Eastern Desert.

The energy firm’s first two wells have already been tied-in and are actively contributing to the company’s oil production.

SDX Energy is currently aiming for a production growth to 3,500 to 4,000 barrels of crude oil per day from its 13 wells by early 2023.

“I am pleased that we have spud MSD-20, the third well in the campaign, so quickly after bringing MSD-21 and MSD-25 onto production, which is testament to the efficiency of the operations team in country and bodes well for the rest of the campaign,” said SDX Energy CEO Mark Reid.

“West Gharib is a very high margin asset in our portfolio with a Netback of US$37/bbl at US$71/bbl Brent in FY2021.”

“I look forward to updating the market further as the campaign progresses.”

The FTSE 100 gained more than 1% on Friday after the market enjoyed a wave of optimism, as reports from REC and KPMG revealed that UK starting salaries rose at their fastest rate in March since records began in the late 1990s.

It was a great day for miners, banking and investment groups, and oil companies, with the stocks swept up in a commodities rally and hopes of a stronger global economy.

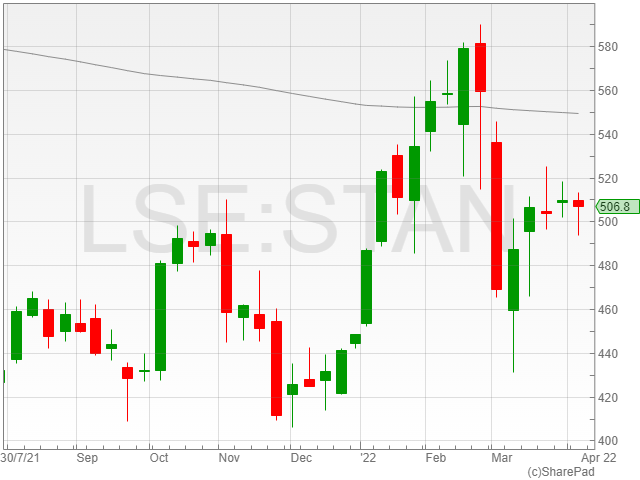

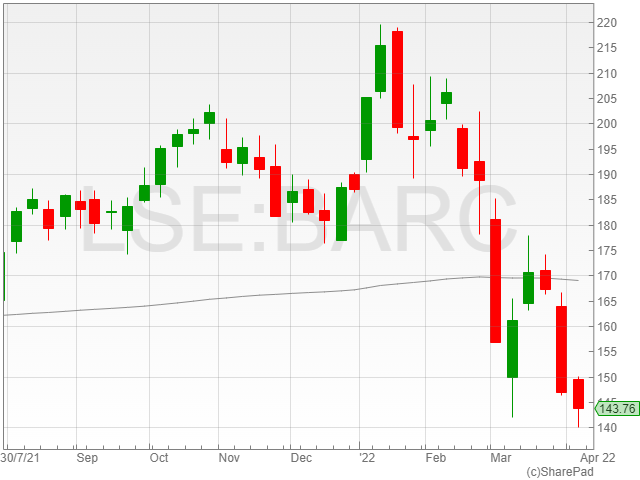

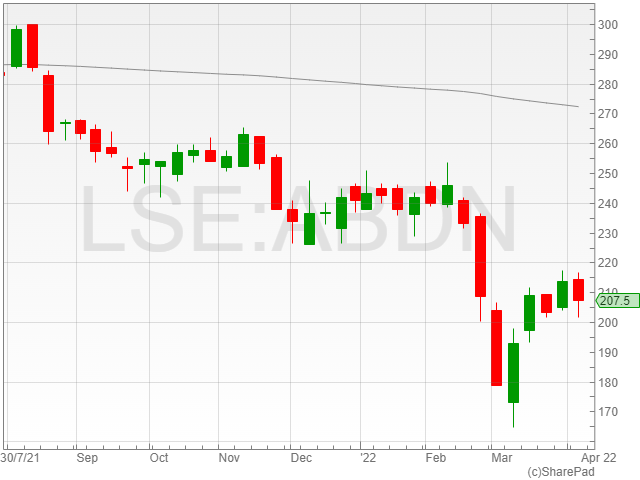

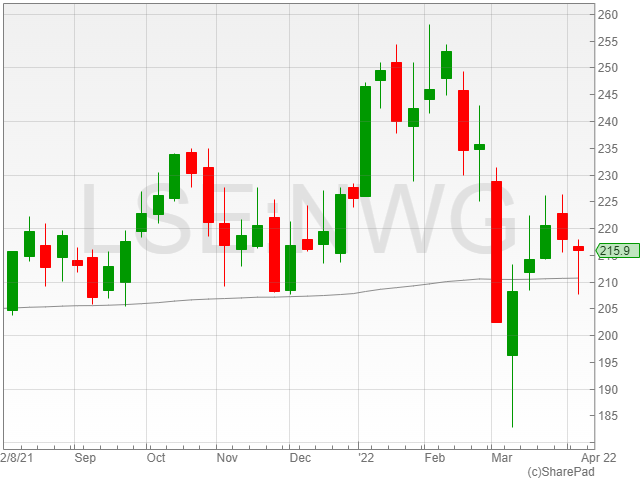

The FTSE 100 was anchored by the financial companies, with Standard Chartered rising 2.8% to 508.6p, Barclays shares increasing 2.7% to 144.5p, abrdn gaining 2.3% to 207.7p and NatWest receiving a 2% boost to 216.6p.

Standard Chartered shares August 2021-April 2022Barclays shares August 2021-April 2022abrdn shares August 2021-April 2022NatWest shares August 2021-April 2022

“Commodities firms and financial stocks, the latter boosted by expectations of faster rate hikes, helped lead the charge higher,” said AJ Bell investment director Russ Mould.

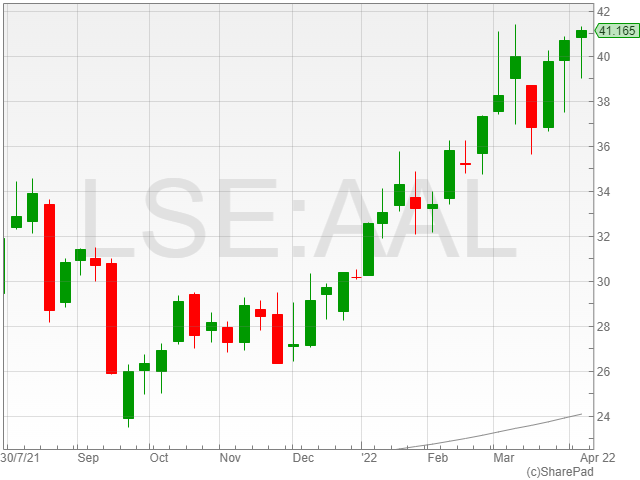

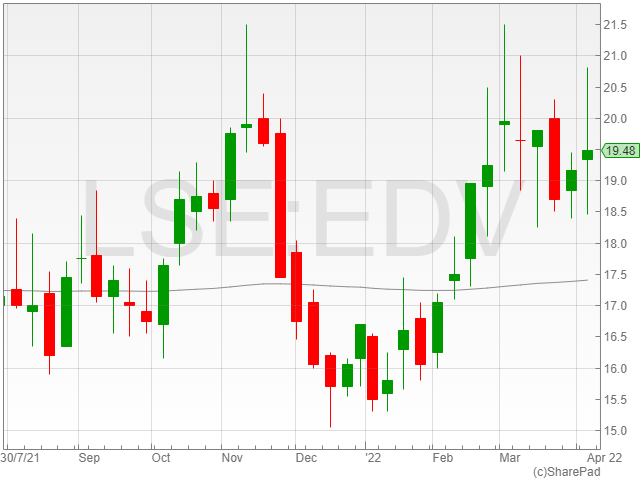

Anglo American shares enjoyed a boost of 3.2% to 41,065p and Endeavor Mining rose 2% to 19,485p.

Anglo American shares August 2021-April 2022Endeavour Mining shares August 2021-April 2022

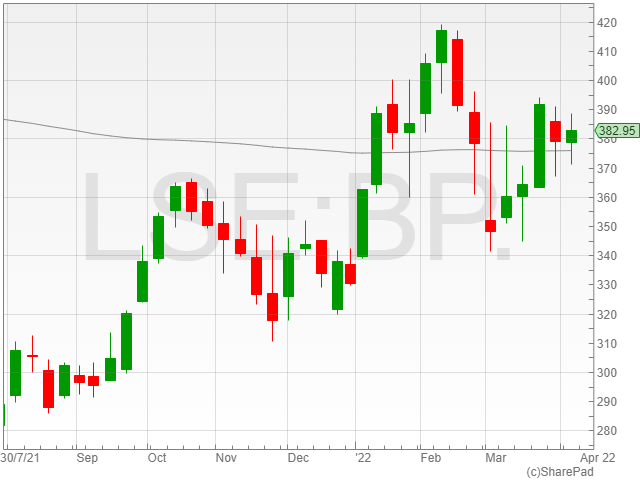

BP shares rose 2% to 385p, following the minor 0.5% upswing in the Brent Crude price to $101 per barrel.

BP shares August 2021-April 2022

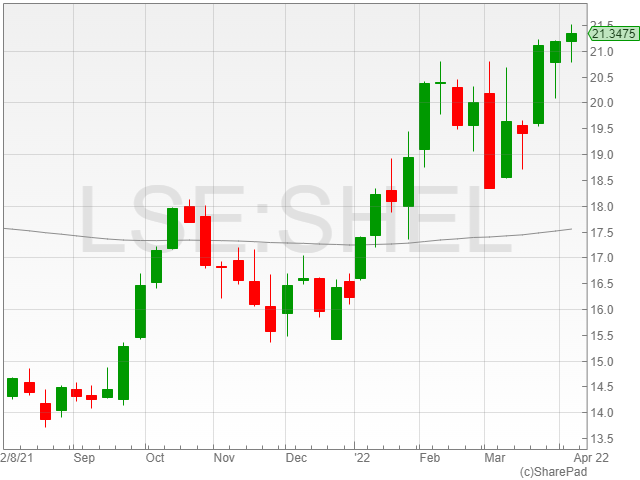

Shell shares increased 2.9% to 21,477p as the company gained back ground after its nasty shock yesterday, following the announcement that its exit from Russia would cost it an estimated $5 billion.

Shell shares August 2021-April 2022

Although investors might be celebrating today, there does remain the risk that the increase in salaries will not work as a counterbalance to the spiking rates of inflation.

“Investors continue to wrestle with the challenges posed by rising interest rates and surging inflation with the latest data on wages in the UK offering an indication of how entrenched inflationary pressures are,” said Russ Mould.

“The risk is even the most generous salaries will see their buying power severely pinched by the rapidly escalating cost of living.”

AffyXell Therapeutics, a joint venture between Avacta and Daewoong Pharmaceutical, has entered into a collaboration agreement with Biocytogen, a Chinese company specialising in developing new biological drugs, and the Korea Non-Clinical Technology Solution Center (KNTSC), according to Avacta Group, a clinical-stage oncology drug company.

The partnership will focus on the development of new immunological illness in vivo models as well as proof-of-concept and toxicity assessment of AffyXell’s therapeutic candidates utilising the disease models created.

Biocytogen’s gene-editing platform, which develops mouse models capable of manufacturing human antibodies, will benefit these models.

The alliance aims to improve AffyXell’s programme translation into human trials and speed up medication development.

KNTSC’s involvement in the partnership is to provide pre-clinical trial infrastructure and management.

AffyXell was formed in January 2020 as a joint venture between Avacta and Daewoong to explore innovative mesenchymal stem cell therapeutics.

AffyXell is merging Avacta’s Affimer platform with Daewoong’s mesenchymal stem cell platform to genetically modify stem cells so that they can manufacture and secrete therapeutic Affimer proteins in the patient.

The Affimer proteins are meant to boost the therapeutic effects of mesenchymal stem cells, resulting in a cutting-edge cell therapy platform.

Dr Alastair Smith, CEO of Avacta stated, “The quality of pre-clinical disease models and their ability to translate into humans is critical for reducing risk and timelines associated with drug development. This collaboration has the potential to significantly accelerate AffyXell’s programmes.”

“We expect this contract to allow Affyxell to exert a synergistic effect on developing next-generation cell gene therapy for overcoming immune diseases based on our non-clinical animal model development and non-clinical experimental know-how related to immune diseases,” added Biocytogen CEO, Yuelei Shen.

Avacta shares rose 17% to 103p after the company announced its joint venture Affyxell enter into an agreement with Biocytogen and KNTSC.

Randazzo has reportedly agreed to stay on as interim CEO of the company while the MC Mining board looks for his replacement.

The former executive director joined the mining group in November 2019 as a non-executive director, before rising to interim CEO and executive director from February 2021.

Randazzo’s time in the position included the successful stabilisation of MC Mining’s portfolio during a turbulent and challenging time for the firm due to social unrest in South Africa, causing trouble for its operations in the region.

The additional highlights over his tenure included diligent cash management, successful negotiations to extend company debt facilities and vendor payments, alongside the conclusion of a $5.7 million funding package announced by the company on 1 February 2022.

Randazzo also initiated and directed a bankable feasibility study carried out for the group’s Makhado hard coking coal project, and conducted talks with a selection of potential key cornerstone financers for the venture.

“On behalf of the Board I would like to thank Mr Randazzo for his significant contributions as Executive Director,” said MC Mining chairman Khomotso Mosehla.

“Mr Randazzo agreed to serve in this role during a challenging time and has successfully guided MC Mining during difficult business conditions.”

“He has been instrumental in setting the foundation for the Company to complete a funding package for the development of the Makhado Project. The Board is very grateful for his commitment.”