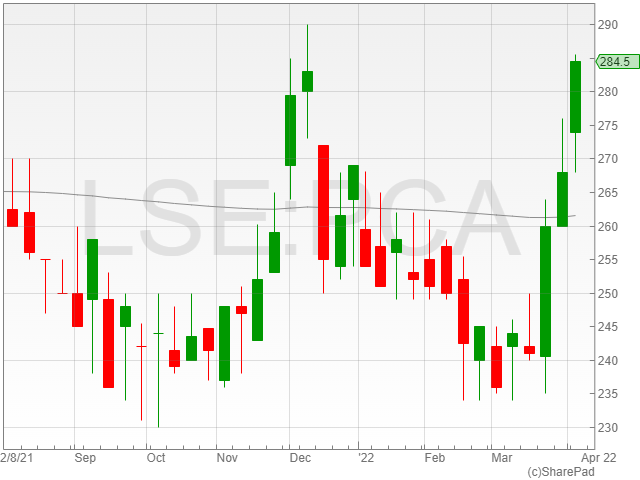

Palace Capital shares enjoyed a 2.3% rise to 280.5p per share in early morning trading on Wednesday morning after the investment company released an annual trading update projecting a strong performance exceeding market expectations for 2021.

The firm credited asset management success, lease activity and a slate of acquisitions for its promising results over the past year.

Palace Capital reported £28.1 million in cash on its balance sheet for 2021, alongside its disposal strategy ahead of target with gross proceeds of £31.5 million and an improvement to its portfolio income with steady rent collection and a reliable dividend increase.

The Group announced a 38% reduction in net debt to £73.6 million, and added that its EPRA earnings and adjusted PBT are projected to exceed market expectations.

Palace Capital announced a quarterly dividend of 3.2p per ordinary share, which is scheduled for payment on 14 April 2022.

The company confirmed a final dividend at a minimum of 3.7p to be paid in July 2022.

The property investment group said its goal is to take a higher level of risk in 2022, by using its core assets as a foundation from which to grab investment opportunities in the regional office and industrial sectors which would be riskier, yet provide stronger returns to shareholders.

Palace Capital currently aims to realign its portfolio with a distribution of 50% core assets, 40% value add/asset management and 10% invested in development.

“Following an extremely active period of portfolio management, the Company is well positioned with a higher quality portfolio delivering improved income and the opportunity for reinvestment underpinned by a significantly strengthened balance sheet,” Palace Capital CEO Neil Sinclair.

“It means that as we recover from the pandemic, we are well placed to address the future with confidence.”

The news of increased market share and performance in line with the company’s five-year strategy encouraged investors, and the group shares lifted nearly 3% to 1,660p in early morning trade on Wednesday.

Imperial’s top-five combustible markets, which contribute to over 70% of adjusted operating profit, have seen a growth in aggregate market share as a result of maintaining strict pricing discipline, and overall tobacco volume is on track.

The gains obtained from the United States, the United Kingdom, and Australia more than offset losses in Germany and Spain.

Customers in Greece and the Czech Republic have responded favourably to pilots of the Pulze heated tobacco system, as well as an improved consumer marketing offer for its blu vapour product in the United States.

Imperial made solid progress toward its strategic goal of creating a long-term, consumer-focused Next Generation Product (NGP) business, and it will offer an update on our next steps in the interim results which will be announced on 17 May 2022.

Due to the growth in Europe, first-half NGP sales are likely to be somewhat higher than in the previous period.

Imperial Brands is on target to ensure full-year results following the group’s updated guidance released on March 15, with adjusted operating profit growth of about 1% and full-year net sales increase of roughly 0-1% in constant currency.

On a constant currency basis, first-half group net sales are forecast to be almost flat compared to last year, which is in line with the group’s estimates due to a decline in cigarette sales in Europe, which has offset increases in other markets.

On a constant currency basis, H1 2022 group adjusted operating profit is forecast to increase by roughly 2%, owing to lower NGP losses.

Tobacco performance will be heavily weighted in H2, as projected. On a constant currency basis, H1 2022 tobacco operating profit will be roughly unchanged compared to last year, with additional investment in Imperial’s strategy offsetting the advantage of lower US litigation costs compared to last year.

Translation foreign exchange is estimated to be a 2% headwind on first-half earnings per share and a 1% drag on full-year earnings per share at current exchange rates.

The return to pre-COVID spending patterns as Northern Europeans resume overseas travel, as well as price phasing in some sectors, have boosted Europe’s performance. Price increases later in H1 will aid a greater revenue performance in H2 2022.

On a 12-month basis, Imperial Brand’s adjusted operating cash conversion continues robust, and it is on track to meet half-year and full-year forecasts.

The group’s adjusted net debt to EBITDA ratio will improve year on year, with a 12-month leverage forecast to be 2.4x at the H1 2022, down from 2.6x in 2021, reflecting seasonal cash flow changes. However, Imperial anticipates a year-over-year increase in leverage for the entire year.

Meanwhile, the group continues to assist our Ukrainian colleagues and their families with transportation and lodging to allow them to flee the most severely affected areas of the crisis, as well as resettlement assistance for those who have already left Ukraine.

Hilton Food Group shares fell 1.1% to 1,208p in early morning trading on Wednesday following the company’s announcement of an International Financial Reporting Standards (IFRS) pre-tax profit drop of 12.3% to £47.4 million against £54 million in 2020 in its preliminary results for 2021.

However, the Hilton Food Group’s IFRS basic earnings per share fell 7.4% to 45p against its 48.6p result in 2020.

The Hilton Food Group reported a sustained growth across all protein categories for the last two years, with meat and seafood hitting 14.3% volume growth, vegan and vegetarian recorded at 26.4% and added value easier meals coming in at 36% .

The protein company expanded into international markets, with over 75% of its business achieved outside the UK.

“This has been a year of delivery and diversification,” said Hilton Food Group CEO Philip Heffer.

“We have delivered another strong financial performance with volumes and revenue both growing, maintaining a trend of continuous volume growth every year since Hilton’s flotation in 2007.”

Hilton Food Group further acquired European vegetarian producer Dalco and entered the North American market with its acquisition of smoked salmon producer Foppen with a £75 million equity raise.

“We have also made strategic progress in diversifying the business. Last year, we set ourselves the goal of becoming the protein partner of choice,” said Heffer.

“Put simply, we want to offer all the proteins people want to put on their plates, in home and out of home, not just in Europe and Asia, but in North America too.”

“To reach that goal, we have been transforming our business to expand into new protein products and categories, to enter new international markets, to deepen our technology and engineering capabilities, and to expand our sustainability commitments across all protein categories.”

The firm announced a proposed final dividend of 21.5p, amounting to a total dividend of 29.7p, which was an increase over its 26p offering in 2020.

The euro-denominated bonds will be issued by Diageo Capital B.V., while the sterling-denominated bonds will be issued by Diageo Finance, with Diageo fully guaranteeing the payment of principal and interest in both cases.

The drawdowns will include the issuance of €750m bonds with a coupon of 1.500% per annum due June 2029, €900m bonds with a coupon of 1.875% per annum due June 2034, £300m bonds with a coupon of 2.375% per annum due June 2028, and £600m bonds with a coupon of 2.750% per annum due June 2038.

Each issuance’s proceeds will be utilised for general corporate objectives.

Barclays Bank PLC, BofA Securities Europe SA, Deutsche Bank Aktiengesellschaft, Goldman Sachs Bank Europe SE have been appointed as joint active book-runners for the euro-denominated bonds, while Credit Suisse Bank (Europe) S.A., RBC Europe Limited, and Standard Chartered Bank have been appointed as joint passive book-runners for the euro-denominated bonds.

Barclays Bank PLC, Deutsche Bank AG, London Branch, Goldman Sachs Bank Europe SE, Merrill Lynch International have been named joint active book-runners for the sterling-denominated bonds, while Credit Suisse International, RBC Europe Limited, and Standard Chartered Bank have been named joint passive book-runners.

Diageo shares gained 1.2% to 4,025p after the company announced the launch of its fixed-rate euro and sterling bonds in early morning trade on Wednesday.

Persimmon announced on Tuesday that it had signed the UK government’s developer pledge, following discussions with the Department for Levelling Up, Housing and Communities (DLUHC).

The pledge reportedly sets out the housing sector’s commitments to removing cladding and fixing fire safety issues in any building over 11 metres, and follows Persimmon’s earlier pledge in 2021 to protect its leaseholders from the costs of replacing cladding and making the necessary amendments to remove fire hazards linked to a selection of its properties.

According to Persimmon, the pledge commits its signees to address fire-safety concerns on all buildings 11 metres or over developed by the company 30 years before 5 April 2022, and to not claim any financial assistance from the government’s Building Safety Fund.

The building firm added that it believed the £75 million provision laid out for rectification works will remain sufficient to cover the necessary expenses covered under the Pledge.

“Over a year ago we said that leaseholders in multi-storey buildings Persimmon constructed should not have to pay for the remediation of cladding and fire related issues,” said Persimmon CEO Dean Finch.

“We are pleased to reaffirm this commitment today and sign the Government’s Developer Pledge.”

“We made this commitment last year as we believed it was not only fair for leaseholders but also the right thing to do as one of the country’s leading homebuilders.”

“We are pleased that we were able to work constructively with the Government to secure this agreement.”

Persimmon shares remained flat at 2,209.5p in late afternoon trading on Tuesday after the report.

A currency management solutions company, Alpha FX Group announced on Tuesday that it has recommenced its trading relationship with a key Norwegian client.

As a result of the impact on the client from the start of COVID-19, the company entered into a settlement agreement with the customer in March 2020, under which weekly repayments for unpaid margin would be required until June 2022.

The client’s financial situation has improved since that time, and they have routinely met all 104 of their weekly payback commitments. As a result, the outstanding gross balance as of 1 April 2022 has been decreased to £2.9 million.

Alpha FX can resume its trading relationship as a result of the client’s solid financial status and the regularity with which they have paid and decreased their outstanding liabilities.

Furthermore, as a goodwill gesture in re-establishing a trade relationship, the group has agreed to extend the client’s remaining weekly repayments, which were originally scheduled to conclude at the end of June 2022, until the end of December 2022.

Alpha has no reservations about the client’s capacity to fulfil their responsibilities under the terms of the original agreement as the client’s financial condition is the best it has been since the beginning of the relationship.

“Having learnt from the experience of having too much concentration to one client in March 2020, we have instituted limits on the value of our exposure to any client regardless of the strength of their credit standing. Additionally, since that experience, we have added further enhancements to our risk processes and controls with the aim of further protecting against such an occurrence in the future,” said Morgan Tillbrook, Chief Executive Officer, Alpha FX.

“We also continue to provide investors and stakeholders with improved visibility and assurance, by publishing our top 20 client and currency exposures on our website, the largest of which currently represents 4.86%.”

Petropavlovskshares (LON: POG) have been smashed by its exposure to Russia caused by the Russian invasion of Ukraine. However, the question is, are the damages permanent?

Petropavlovsk’s shares have fallen nearly 80% since the start of January 2022. The gold producer shares were once trading at 16.00p in February 2022, just before the invasion began. The stock closed at 3.85p on Monday as the stock rebounded from its lowest levels around 1.50p.

Petropavlovsk

Petropavlovsk is a major integrated Russian gold producer with JORC Resources of 19.50Moz of gold, including 7.16Moz of gold reserves.

Pioneer, Malomir, and Albyn, as well as the Pokrovskiy Pressure Oxidation (POX) Hub, are all located in the Amur Region of Russia’s Far East.

Since its inception in 1994, Petropavlovsk has produced a total of 8.7Moz of gold and has a proven track record of mine development, growth, and asset optimization.

Petropavlovsk is amongst the region’s leading employers and a major contributor to the region’s long-term economic growth.

The gold miner made headlines in January as KPMG found corporate governance problems including wrongdoing such as inflating the cost of mining licenses and conflict of interest to benefit senior management. Petropavlovsk’s chairman acknowledged the errors found in the report and reiterated that the company is installing new rules, policies and procedures in place to instil a “culture of zero tolerance for improper business practices.”

Later in January, the announced its sales and production report for Q4 2021 where the company noted a 26% year-on-year increase in total gold production from 1.135koz to 1.431koz as a result of improved output across its mines.

The group’s sales in Q4 2021 increased to 1.301koz from 1.131koz in Q4 2020.

The total gold production in 2021 for the group amounted to 4.498koz which was 18% lower than 2020. However, the group’s gold out was well within the guidance of 4.3koz to 4.7koz.

For 2022, Petropavlovsk had further reduced its gold production guidance between 3.8koz and 4.2koz which didn’t help investor sentiment.

Impact of Russia

Russia invaded Ukraine on the 24th of February after which Russian stocks began to crumble, with of course Petropavlovsk taking a barrage of punches due to its exposure in Russia.

The group released an announcement regarding the implications of Russian sanctions on the company in hopes to regain investor confidence in early March. Petropavlovsk said it does not consider its shares or debt instruments to be securities in which dealings are limited under the regulations.

Due to 50.10% ownership of Petropavlovsk being free from Russian entities and being domiciled in the UK, the company believed it would not be subject to sanctions.

Petropavlovsk has a $200m term loan and an $86.7m revolving credit facility with Gazprombank the company addressed in a statement.

The conditions of the facilities enabled Petropavlovsk to sell its gold to Gazprombank which was hindered due to the clauses of the sanction.

“Restrictions on purchasing and selling gold in Russia may make it challenging to find an alternative purchaser for the group’s gold output,” Petropavlovsk warned.

The sanction led asset freeze resulted in the company defaulting on payments such as an interest payment of $560,000 due on the term loan and the rouble equivalent of $9.5m under its revolving credit facility.

The assets being locked up with Gazprombank would lead to a barrier in operations and financial obligations for the gold miner. In order to prevent future issues from rising, the company began to discuss possible restructuring of the group’s debt with its advisers and the bank.

The alternative options however remain unclear for the company as factors such as the length of the sanctions impacting Gazprombank also play a role.

The company also announced the resignation of Natalia Yakovleva an independent non-executive director from the Board on Monday.

Petropavlovsk Valuation

Petropavlovsk shares once peaked at 27.66p during April 2021. The company has since lost 84.3%.

The group has a market cap of £152.4m and a ROCE of 19x.

Even though Petropavlovsk’s shares plummeted since the start of 2022, on Monday the shares gained 13%. Is that a sign of optimism for the gold miners? Maybe.

The reality is, apart from the exposure to Gazprombank, Petropavlovsk has a limited association with Russia. If the company establishes a successful plan to restructure its debt and avoid failure of future payments, there may be hope.

Based on current speculation, a goal of 16p for the Petropavlovsk share price seems difficult, but not unachievable.

FTSE 100 fell to 7,546 in early afternoon trade inn Tuesday, as the West placed more sanctions on Russia following the discovery of horrifying evidence of war crimes in Ukraine.

Oil prices gained 1.5% to $109 a barrel on Tuesday as a resolution to the war slips away and leading global exporter Saudi Arabia announced a rise in its oil prices for May.

The only positive impact of the rising oil prices fell on energy stocks such as BP, which gained 0.7% to 379p.

Shell shares lost 0.2% to 2,111p following the announcement of reported payments to the government. The group has paid $58.7b to governments. However, the group collected $46.1b in excise duties, sales taxes and levies on its fuel and other products on behalf of international governments.

Though rising oil prices may be “bad news” for the economy, heavyweights like BP can help “limit the losses for the FTSE 100” according to Russ Mould, Investment Director, AJ Bell.

FTSE 100 Risers

Croda shares rose nearly 4% to 8,055p after the UK government approved a £15.9m grant for the company to expand its manufacturing facility in Leek, Staffordshire.

“This investment will meaningfully enhance our lipid system capability and manufacturing capacity, ensuring that Croda plays a central role in both the development and future supply of this important delivery technology,” said Daniele Piergentili, President of Croda Life Sciences.

Halma shares gained 1.7% to 2,589p after HSBC increased the group’s price target from 2,120p to 2,365p.

Auto Trader shares increased 1.3% to 658p, despite Credit Suisse cutting Auto Trader’s price target from 532p to 514p.

ITV shares rose 0.04% to 82p on rumours of the group acquiring Channel 4 after the UK government said they would privatise the broadcaster that is funded by advertising, but publicly owned.

FTSE 100 Fallers

Kingfisher shares sank nearly 3% to 253p as the DIY consumer goods company’s shares faced the brunt of investor concern that consumers will be prioritising their expenses for essentials with the rise in the cost of living, leaving home improvement projects on the back burner.

Housebuilder stocks saw a fall today with Barratt Development losing 3% and Taylor Wimpey losing 2.8%.

“Housebuilders have been in the doldrums since the start of the year despite a supercharged housing market as investors priced in the cost of making repairs,” said Danni Hewson, a financial analyst at AJ Bell yesterday.

Vodafone shares fell 1.9% to 123p as Berenberg cut the group’s price target to 145p from 150p.

Airtel Africa shares dropped 2.8% to 140p on Tuesday after the company reported that it is unsure about the financial impact of regulatory SIM card measures at its Nigeria telecommunications unit that the group adopted.

Flutter Entertainment shares have been falling for quite some time, and on Tuesday, the shares dropped 1.4% to 8,965p as the UK announced the ban on using celebrities in advertising gambling products to curb its appeal to children under the age of 18.

The FTSE 250 was up 0.1% to 21,363 and the AIM was up 0.5% to 1,061 in early afternoon trading on Tuesday. Trustpilot helped the FTSE 250 higher with a 9% gain and raft of positive updates from AIM constituents.

Stronger commodities prices supported markets after Saudi Arabia said they were raising their May oil prices.

The price of Brent Crude oil rose to $109 per barrel following its plummet to $104 on Monday after state oil supplier Saudi Aramco increased its selling price for May to $9.35 per barrel for its Arab Light crude.

FTSE 250 Risers

Reviews company Trustpilot Group enjoyed a rise of 6.8% to 153.3p as the stock began to recover from a sharp selloff in 2022 which has seen their shares halve in value.

Lithuanian classifieds company Baltic Classifieds Group shares increased 4.9% to 153.8p as the stock continued to bounce back from significant losses sustained as the conflict in Ukraine began.

The IP Group surged 4.5% to 93.8p after the company’s First Light Fusion portfolio company reported a world first projectile-based fusion success which has the potential to open up the industry for faster and cheaper fusion energy.

FTSE 250 Fallers

Darktrace shares suffered a dip of 6.2% to 422.7p after investors turned pessimistic following claims by JP Morgan that the company looks set to struggle with customer retention amid rising competition and a projected increase in customer acquisition expenses.

“High competition and low customer stickiness will likely translate to higher customer acquisition costs and prompt Darktrace to increase investments in existing and new product development – both of which will limit margin leverage going forward,” said a spokesperson for JP Morgan.

Moneysupermarket.com fell 3.9% to 181.7p following speculation from Barclays that the insurance broker looks like it’s set for a weak period in Energy, and a current drop in its Money and Travel divisions, resulting in the bank dropping its rating from overweight to equal weight.

Housebuilding and urban regeneration group Countryside Properties dropped 2.6% to 271.4p as the rising cost of living impacts consumer spending.

AIM Risers

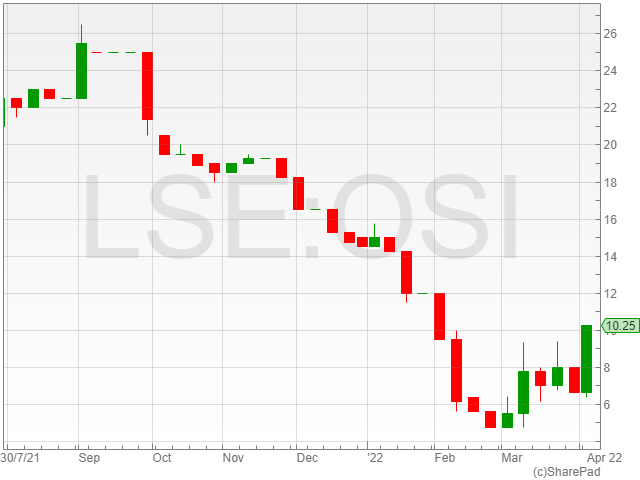

Osirium Technologies shares rose 45.1% to 9.2p following a strong Q1 report with growth in contract values along with a return to pre-pandemic levels.

Abingdon Health enjoyed an uptick of 17% to 12p after the firm reported the completion of the technical transfer of its Vatic KnowNow Covid-19 antigen test for diagnostics technology group Vatic Health.

Longboat Energy saw an increase of 17% to 72p in light of the company’s recent Kveikje exploration well oil and gas discovery based in the Norweigan North Sea.

“Excellent reservoir quality, close proximity to infrastructure and multiple development options make this an important and valuable resource and we look forward to working with the operator to mature the forward plan,” said Longboat CEO Helge Hammer.

“We believe that this is an asset that can be commercialised via either development or transaction given the high-value barrels that we have discovered.”

Sovereign Metals shares soared to touch all-time highs after the company announced their Kasiya Titanium Rutile project holds the world’s largest resource and is preparing for an updated scoping study.

Next Fifteen Communications rose as they released 2021 results that pointed to a 36% increase in revenue and encouraging organic revenue growth.

Echo Energy shares jumped 6% after production for Q1 2022 averaged 265 bopd, an increase of 10% compared to Q4 2021.

Borders and Southern Petroleum rose fractionally following the completion of a £1.35m funding round.

AIM Fallers

The Intercede Group plummeted 23.9% to 44.5p after the company reported an estimated 10% decline in revenue for 2021 on the back of delays in significant deals for the group.

Keras dipped 13.1% to 0.08p following a decline in interest after the shares surged to 0.09p from 0.04p after its acquisition of the Diamond Creek mine.

Gooch and Housego shares fell 4% after the group said revenue was expected to be weighted to the second half.

The international home repairs and improvements business, Homeserve delivered results for FY2022 earlier today which were in line with the group’s expectations.

HomeServe made significant strategic and financial progress in FY22, achieving an acceleration in performance over FY21, which was in line with expectations.

HomeServe’s three business divisions saw strategic progress with innovative new products gaining traction in North America, progress in building three complementary businesses in EMEA – Membership, HVAC and Claims Assitance; and progress in Home Experts on creating businesses to match homeowners with deals of quality.

North American Membership and HVAC

North American Membership and HVAC segment performed strongly.

Despite the ongoing effects of the Omicron on HomeServe and its partners, policy retention was 86% remaining the same as in 2021, and affinity partner households increased to £73M from £66m in 2021.

To promote future growth, the company is expanding its customer offerings to let households engage in the green home revolution and align with partners’ to achieve carbon reduction goals.

HVAC As A Service provides worry-free heating and air conditioning replacements with a yearly servicing and breakdown cover for a monthly subscription. After a successful trial with a large utility in New York State, the service is now available.

Through a new 4.6m household utility relationship and expansion with an existing partner, HomeServe’s installation and maintenance proposition for domestic electric vehicle charging is now available to 9m households.

In addition, HomeServe’s water loss cover product, which is supplied on a bill by municipal water utilities to protect their customers from unexpectedly large expenditures due to home water leaks, has seen strong growth.

EMEA Membership and HVAC

The division continued to execute on its transformation and growth targets across EMEA Membership and HVAC.

Customer numbers ended the year in line with the group’s forecasts, and policy retention was higher than in 2021 in the UK, indicating that the company’s transformation plan is on track.

France and Spain did well, with the Spanish claims handling company seeing a significant increase in job volumes.

In the second half, HomeServe’s Japanese joint venture inked two more marketing agreements.

Home Experts

As planned, the Home Experts segment turned a profit for the first time in a full year, owing mostly to Checkatrade’s sustained growth as the UK’s top online platform for connecting homeowners with quality trades.

Checkatrade had 47,000 paying trades at the end of the year compared to 44,000 in 2021, and the average revenue per trade is likely to surpass the Milestone 1 objective of £1,200 compared to £939.

As trade supply and consumer demand began to rebalance in the second half, the number of trades on the platform increased.

With robust cash generation in HomeServe’s busier second half largely offset by the CET acquisition in the UK and subsequent attractive HVAC M&A across all of HomeServe’s Membership & HVAC companies, net debt on 31 March 2022 was 2x EBITDA.