The Property Franchise Group posted strong results on Tuesday following a year of organic growth boosted by acquisitions.

The online/hybrid estate agency revealed a 33% increase in profit before tax driven by a 23% jump in revenue to £10.2m.

The Property Franchise Group has recently changed its name from MartinCo to reflect the firms transformation from a single brand franchise to a multi-chanelled group harnessing the technological advancements in the estate agency business.

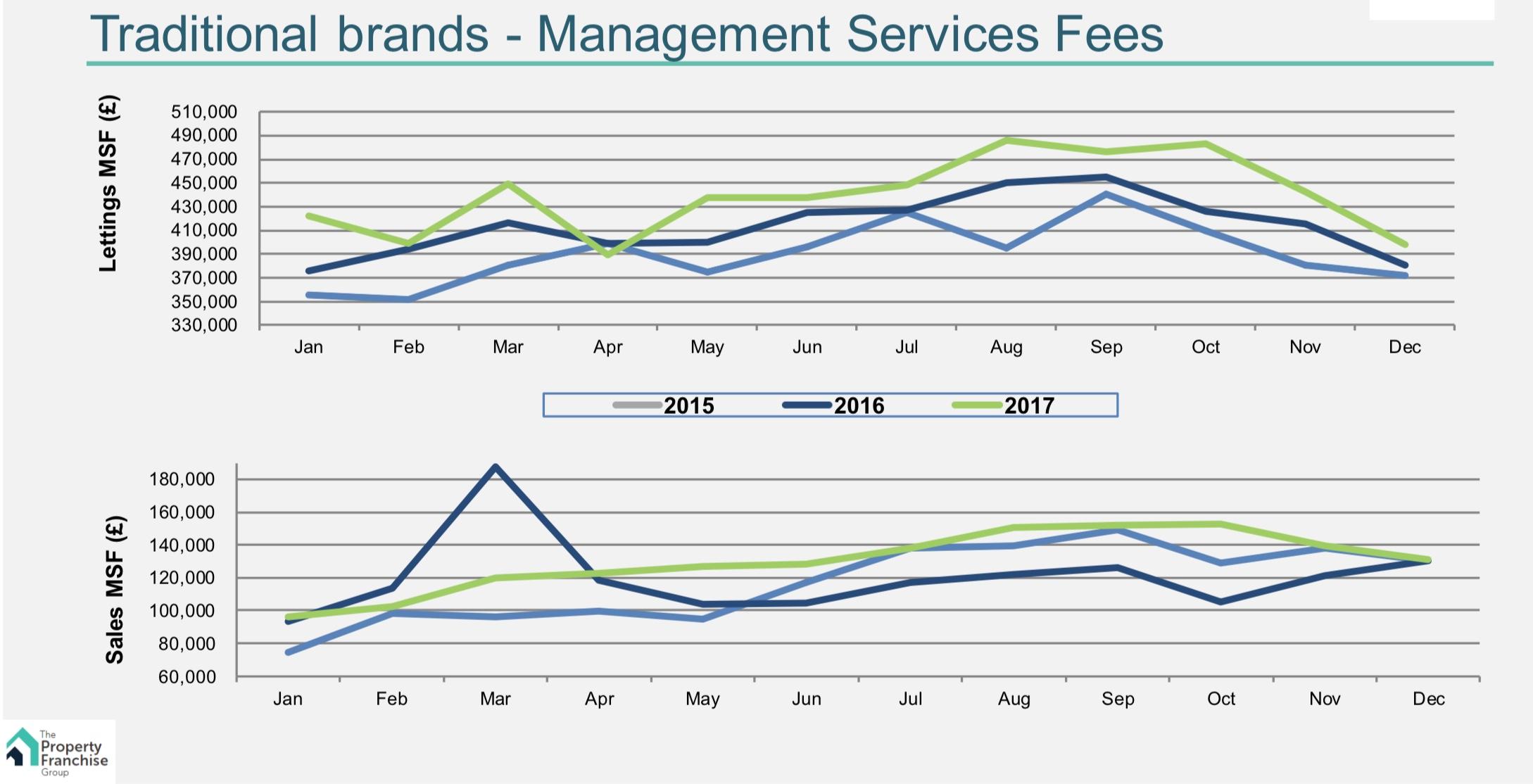

A key acquistion for the group has been EweMove that not only added 120 offices but also provided the digital technology to enhance the entire group with a robust digital outlet previously lacking in some its traditional brands.

EweMove came with the technology to help drive down the cost of winning new revenue across all brands. Whitegates, one of the groups brands focussed on the Midlands and North of England, saw a 649% increase in overall website conversions in what highlights Property Franchise Group’s push to compete with their digital led competitors.

UK Investor Magazine spoke with CEO Ian Wilson who was upbeat about the groups ability to grow in a transforming industry not only through technologcial advancements but through a business model that supports the groups franchisees.

The firm counts brands such as Martin&Co, Ellis&Co, Parkers and CJ Coles as their franchises and has enjoyed a 7% increase in the number of offices over the past year.

Mr Wilson also touched on plans for further growth through the acquisition of smaller agencies by their franchisees with support from the parent company in the form of cash back schemes to help support cash flow during the process.

On the topic of cash – of which the group has plentiful -cash in the bank increased to £2.6m supplemented by a near doubling of cash from operating activities.

The strong cash position has given the board the confidence to increase the dividend to a full year payout of 7.5p, giving the stock a current yield of around 5.5%.

The strong cash position has given the board the confidence to increase the dividend to a full year payout of 7.5p, giving the stock a current yield of around 5.5%.

Despite the strong profit growth and increase in the dividend, there is a reason to be vigilant.

The outlook for the UK housing market and changes lettings fees present potential risks but the fundamentals are resilient with a large proportion of revenue coming from ongoing management fees so while the group, like all lettings firms, will likely take a hit from the ban on upfront letting fees, it doesn’t represent a material threat to ongoing growth.