The Shell share price (LON:RDSB) should still be considered by investors, despite last week’s decision to cut their dividend.

Royal Dutch Shell made the historic decision to cut their dividend for the first time since world war two to conserve cash amid falling oil prices caused largely by the ongoing uncertainty surrounding coronavirus.

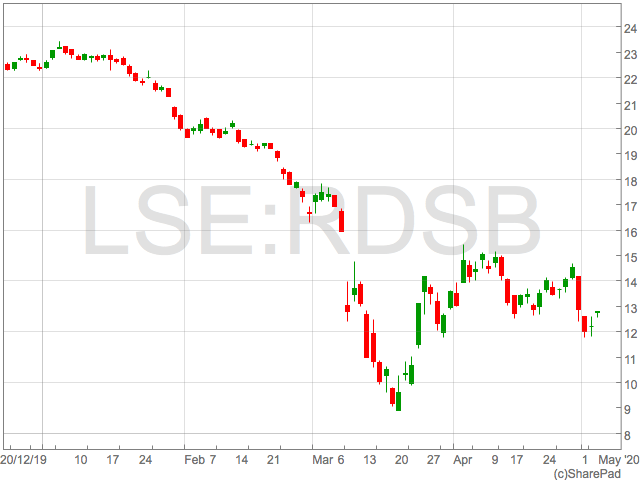

Royal Dutch Shell shares fell in the immediate reaction to the dividend amendment, meaning the company reversed most of the gains it made during April’s rally.

Shell share price

Shell shares are down 44% in 2020, having touched the lowest levels since 1995 during the worst of the selling in March which Shell shares briefly trading beneath 900p.

However, with shares finding support in the region of 1,200p, the market seems to found a price it is comfortable for Shell to trade at with a backdrop of lower oil prices, uncertainty around COVID-19, and a reduced dividend.

A change in any of these factors will likely impact the Shell share price and investors could see a sharp re-rating to the upside if the macro picture improves, or if Shell hints at a reversal of the dividend reduction.

However, with the timing of any economic recovery remaining uncertain, investors will be assessing Shell’s current business, and share price, to gauge whether now is an acceptable time to enter in anticipation of such a move.

Shell valuation

Shell valuation

Given the sharp drop, Shell trades at 30x predicted earnings which is well above average and makes Shell shares look very expensive. However, this valuation will take into consideration earnings over the next 12 months which will be factoring in the decimation in revenue caused by the lower oil price.

Yet investors should look past this to a time the economy returns to some form of normality as a truer picture of what Shell’s valuation will look like in the medium and long term.

What the ‘new normal’ will look like for the global economy is very difficult to accurately forecast, but there isa wide consensus demand for oil will increase as soon as economies reopen.

When this demand returns, oil prices are likely to rise and in turn, Shell’s profits. This is where the value lies for investors in Shell shares.

A scenario where Shell returns quickly to the same level of profitability as last year is unlikely, but Shell trades at just 8.5x trailing earnings which is very difficult to overlook, especially for the largest company by market cap listed in London.

In addition to looking forward to a rebound in oil prices, long term investors should take confidence for Shell’s investments in renewable energy sources and the diversification this provides the business.

Examples of Shell’s push into renewables are the acquisition of ERM Power, one of Australia’s leading commercial and industrial electricity retailers and French wind power company Elofi.

Whilst Shell’s renewables business is still in its infancy and may not provide the revenue to pull Shell out of the current crisis, it shows they are prepared for the next chapter in the global energy market.

Shell have a history of making bold decisions in times of uncertainty and the acquisition of BG Group during the last major down turn in oil demonstrates this. BG provided a significant exposure to the natural gas market, particularly in Asia where demand is expected to grow, and Shell had a minimal presence.

Having reduced the dividend, Shell may have some spare cash to allocate to acquisitions, if lower oil prices do not persist beyond 2020. Should Shell chose to make strategic investments and forgo a quick return to higher dividend payouts, the company is a very bright prospect for the long term investor, even if income investors look elsewhere in the short term.