The FTSE 100 was trading deep in the red on Thursday after the Bank of England voted to keep rates on hold at 3.75%.

London’s leading index was down 1% at the time of writing, but it was more a consequence of a hawkish Federal Reserve than of any commentary from the BoE, which voted 7-2 to keep rates at 3.75%.

“The two votes for a hike show there are some policymakers still concerned about underlying inflation pressures,” said Luke Bartholomew, Deputy Chief Economist, at Aberdeen.

“But with the recent fall in energy prices and the softer inflation data yesterday, events are evolving in line with, or potentially even better, than the Bank’s scenario A from the last meeting, which was consistent with keeping rates on hold this year.”

The BoE followed a surprisingly hawkish Federal Reserve instalment last night, which knocked US stocks lower going into the close. Those who hoped that the appointment of the new Fed Chair, Kevin Warsh, would usher in a new chapter of dovishness and lower interest rates were left bitterly disappointed by predictions of an interest rate hike later this year, despite the supposed resolution of the conflict in the Middle East.

“Even though the Federal Reserve wasn’t expected to raise US interest rates at its meeting last night, nine of the 18 committee members predicted an interest rate hike this year, while just one said they expected a cut. That took the market by surprise and caused a wobble on Wall Street,” said Russ Mould, investment director at AJ Bell.

The Bank of England was widely expected to keep rates on hold ahead of today’s announcement, so the decision to leave rates at 3.75% didn’t come as a surprise and barely moved the dial for FTSE 100 stocks.

Most of which were down at the time of writing as investors focused on the outlook for US interest rates.

Tesco was the headline corporate story on Thursday, releasing Q1 numbers showing market share gains but slowing sales growth, raising concerns about what margins would look like in the current financial year.

“With margins under the spotlight, management’s confidence in maintaining full-year profit guidance should reassure investors that Tesco is managing the balance between competitiveness and profitability effectively despite a subdued trading backdrop,” said Garry White, Chief Investment Commentator at Charles Stanley.

Whitbread shares were flat after reporting group sales up 2% and UK accommodation sales up 3%, while Germany stormed ahead with 13% growth.

Derren Nathan, head of equity research, Hargreaves Lansdown, said: “As England got off to a steady start at the World Cup, Whitbread checked in with a resilient opening quarter of its own. In the core UK division, accommodation sales were up 3% in the first quarter, a meaningful acceleration from the 1.9% reported for the first 8 weeks.

“Around two-thirds of the growth was organic, with the rest from new rooms. London led the way with a 7% sales increase, shrugging off concerns of a fall in visitor numbers due to the conflict in the Middle East.”

Fresnillo was sharply lower after Berenberg cut its price target for the precious metals miner to 3,300p.

Persimmon was the FTSE 100’s top faller, losing 6% as it traded ex-dividend.

Ascent Resources (LON: AST) says that the Tribunal in the Company’s Energy Charter Treaty arbitration against the Republic of Slovenia (ICSID Case No. ARB/22/21) proceedings have closed. A final award is expected before the end of June. The share price is 12.5% higher at 0.45p.

Driver monitoring technology company Seeing Machines (LON: SEE) has agreed an expansion of an existing automotive programme. This extends the range of vehicles using the technology. There is an additional $31m that will be earned and production starts later in 2026. This follows the new contracts announced on Monday with two Japanese car manufacturers that are existing clients. Production starts in 2028 and the contracts will generate revenues of $11m. The share price gained 9.18% to 4.64p.

Genedrive (LON: GDR) says Manchester University NHS Foundation Trust has transitioned the Genedrive MT-RNR1 ID testing kit for the prevention of Antibiotic Induced Hearing Loss in neonates to a routine service. The share price increased 6.12% to 1.3p.

Chief executive Lynden Jones has acquired a further 13,125 shares in logistics services and equipment supplier Touchstar (LON: TST) at 79.5p each. Earlier in the month he bought 50,000 shares at 77p each. He did not own any shares at the end of 2025, and he currently holds 450,000 shares. The share price improved 3.95 to 80p.

MedPal AI (LON: MPAL) has launched Juno, an agentic AI health companion. The share price rose 3.95 to 4p.

FALLERS

Richard and Charlotte Edwards have reduced their stake in Pacsco Ltd (LON: PACS) from 26.6% to 12.5%. The share price slipped 22.2% to 0.35p.

Offshore energy services provider Tekmar Group (LON: TGP) improved interim revenues by 31% to £16.2m and the loss was more than halved from £2.7m to £1.1m. Net debt was £3.6m at the end of March 2026. Activity is at record levels and capacity utilisation is increasing. Tekmar could get near to breakeven in the year to September 2026. The share price declined 7.74% to 15.5p.

Video games publisher tinyBuild (LON: TBLD) is trading ahead of expectations in the first five months of the year. The back catalogue is performing well and there are big budget new releases coming up. Zeus is leaving its forecasts unchanged for the time being. Revenues are expected to improve from $35.5m to $40.7m, pre-tax profit is set to decline from $5.5m to $4.3m. The share price fell 2.7% to 9p.

Ex-dividends

Aeorema Communications (LON:AEO) is paying a dividend of 1p/share and the share price fell 0.5p to 65p.

Concurrent Technologies (LON:CNC) is paying a final dividend of 1.16p/share and the share price rose 0.5p to 263.5p.

Eleco (LON:ELCO) is paying a final dividend of 0.85p/share and the share price decreased 0.5p to 121p.

Gooch & Housego (LON:GHH) is paying an interim dividend of 4.9p/share and the share price declined 27p to 961p.

MHA (LON:MHA) is paying a dividend of 1p/share and the share price dipped 1.5p to 140p.

RWS Holdings (LON:RWS) is paying an interim dividend of 1.75p/share and the share price slipped 2.05p to 81.65p.

Vianet (LON:VNET) is paying a final dividend of 2p/share and the share price fell 1p to 66p.

Dumping Frame, Infrastructure Reality: While the market sees Chinese EV makers as dumping excess capacity overseas, they are actually making strategic investments in Europe. BYD is building a 3,000-station flash charging network to accelerate EV adoption, while Chery, SAIC, and others are investing in European factories.

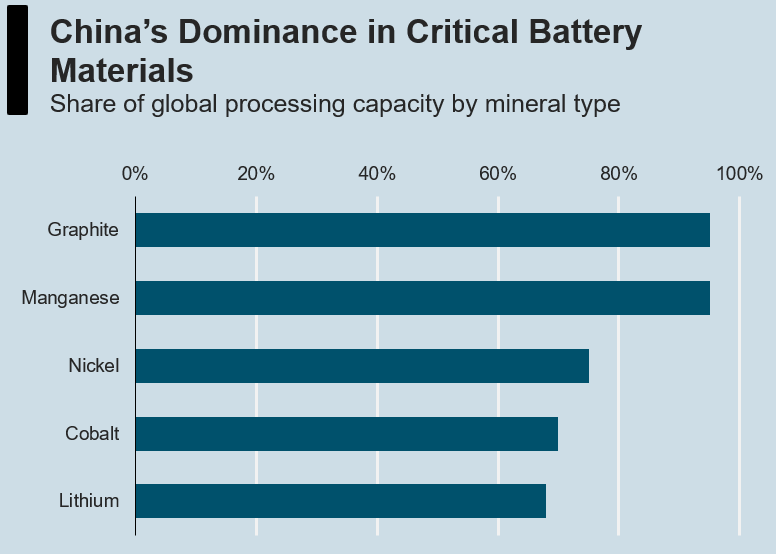

BYD’s Battery Advantage: BYD not only produces vehicles — it is also the second largest EV battery maker globally, backed by China’s dominance over battery mineral processing: over 90% of graphite and manganese, 70% of cobalt and lithium, and 75% of nickel.

Infrastructure Beats Tariffs: The EU’s tariff and MIP regime targets finished vehicle imports. China’s EV infrastructure strategy turns trade policy into a sideshow.

The market frames Chinese EV expansion in Europe as dumping tactics — excess capacity seeking outlets, containable with tariffs.

The reality is that Chinese EV makers are making strategic investments in Europe. BYD is planning to build an extensive fast charging network across Europe, while various brands including Chery and SAIC are investing in factories.

This indicates these brands are implementing a long-term EV strategy instead of short-term dumping of domestic capacity.

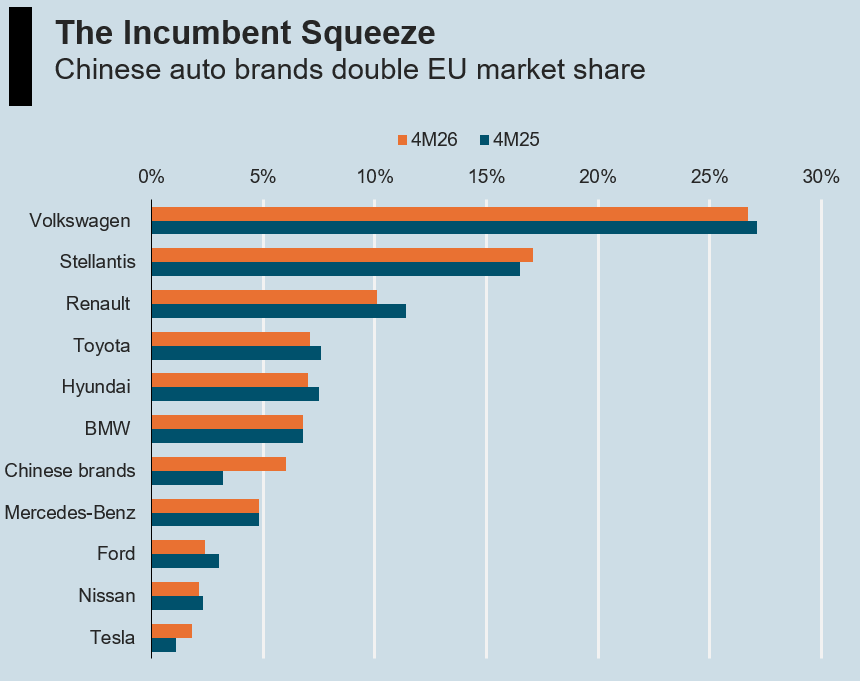

Chinese Auto Brands Gaining Strength in Europe

Chinese auto brands doubled their combined EU market share to 6% in the first four months of 2026, according to ACEA, ahead of Ford, Tesla, Nissan, Mercedes, and approaching BMW.

Among Chinese brands, SAIC/MG led with 2.0% market share, followed by BYD (1.9%), Chery (1.3%), and Leapmotor (0.8%).

Source: ACEA, AP

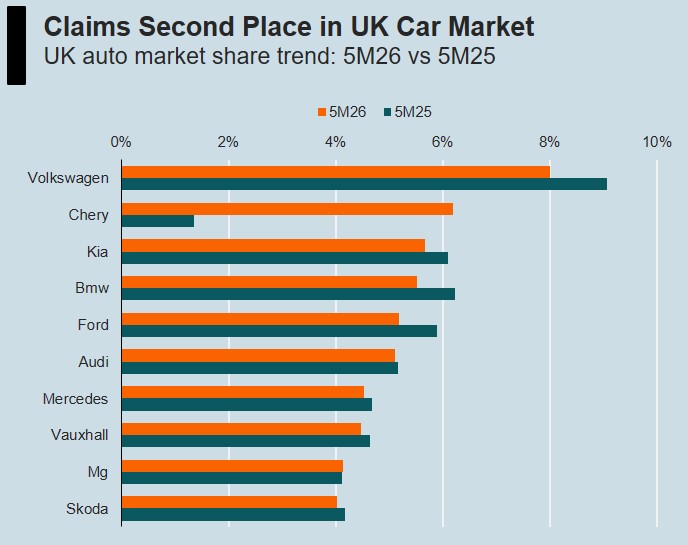

In the UK, the situation is more dramatic. In the first five months of 2026, Chery has become the No. 2 automaker in the UK with 6.2% market share, just behind Volkswagen. Its premium SUV, Jaecoo 7, which offers the look and feel of a Range Rover for less than half the price, has become a major success.

Source: SMMT, AP

Unlocking the Full EV Potential

Despite strong sales growth, the majority of Chinese EVs sold in Europe today are plug-in hybrids (PHEV), not pure battery electrics (BEV). Mileage anxiety remains the primary reason, hindering the EV adoption curve.

The biggest barrier to EV adoption in Europe is not vehicle price. It is charging infrastructure.

Chinese EV makers are now addressing this directly, not through lobbying or policy, but through infrastructure investment.

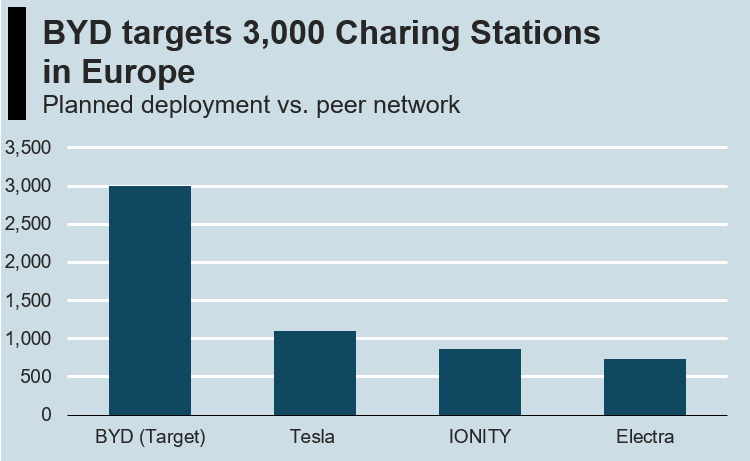

The most ambitious plan belongs to BYD.

BYD plans to build 3,000 flash charger stations across Europe. Each station delivers 3x the power of Tesla’s V4 Superchargers (1,500kW versus 500kW).

In June 2026, its first flash chargers went live in Germany and the UK, which take a compatible vehicle from 10% to 70% in five minutes. BYD reportedly targets pricing 34-38% below IONITY and roughly 17-28% below Tesla’s Supercharger network.

A structural detail: BYD equips each flash charging station with on-site battery storage — not to bypass the grid, but to bypass the grid upgrade. A 1,500kW charger needs peak power most sites cannot supply. The battery trickle-charges at 100-200kW from the existing connection and delivers the burst during a five-minute flash session. No utility upgrade is required.

BYD’s plan represents Europe’s largest EV charging network, beyond the scale of Tesla or IONITY. Existing networks operate at lower power levels, resulting in longer charging times than BYD’s 1,500kW flash chargers.

Source: Companies, AP

The Hidden Edge in Battery

The key question is why BYD can build a massive EV charging network at low cost.

The answer lies in China’s hidden dominance in the EV battery supply chain.

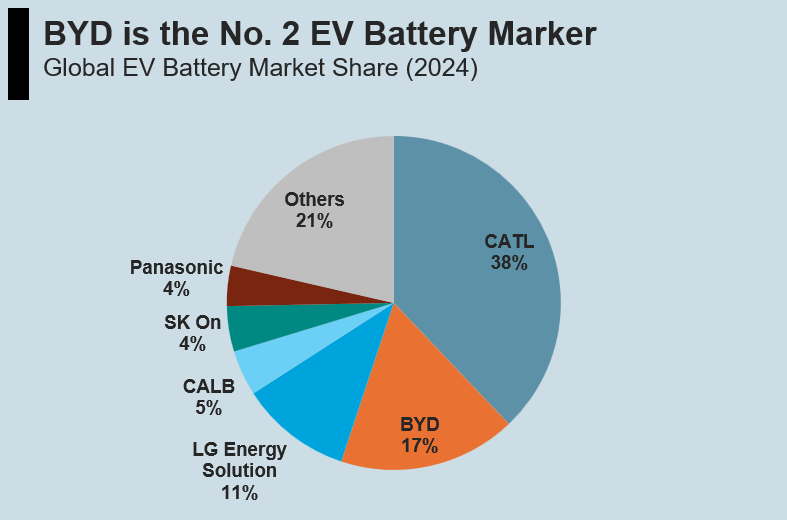

BYD not only produces vehicles. It is also the second largest EV battery maker globally.

Source: CATL, AP

This is supported by China’s dominance over battery mineral processing — over 90% of graphite and manganese, 70% of cobalt and lithium, and 75% of nickel.

Source: IEA, AP

This gives BYD access to essential raw materials for EV batteries at low cost, helping it build a leading position in the global EV battery market.

On the flip side, European battery production costs nearly 50% more than in China, according to the Central European Institute of Asian Studies.

This is illustrated by the bankruptcy of Northvolt, the continent’s flagship battery maker, in 2024.

Local Production Strategy

Chinese EV makers are strategically building new manufacturing capacities overseas instead of dumping domestic capacity.

BYD’s Hungary plant begins serial production with the Dolphin Surf compact EV. The company is also securing an existing factory for a second European plant, with a third factory under discussion.

SAIC/MG is investing €200m in a Ferrol, Galicia factory with 120,000-unit capacity, scheduled to commence operation in 2028.

Chery is producing vehicles through its Barcelona joint venture with Ebro at the former Nissan plant, and is separately in collaboration talks with Nissan for broader cooperation.

Xpeng and GAC Aion use contract manufacturing through Magna Steyr in Austria.

Leapmotor has deepened its partnership with Stellantis for dual-plant European production. One plant will produce Leapmotor’s own B10 SUV for the European market; the other will build a new Opel EV on Leapmotor’s platform.

In addition to regulatory hedge, local design and production can be better tailored to European consumer preferences, safety standards, and regulatory requirements.

On the supply side, some European car makers are under financial pressure, creating acquisition and partnership opportunities. The Chery-Nissan collaboration talks signal that Chinese makers can access existing European manufacturing capacity, which offers a faster route to local production than greenfield construction.

The Incumbent Challenges

European automakers struggle to replicate BYD’s charging infrastructure due to lack of a battery supply chain.

No European OEM has in-house battery production that matches Chinese cost structures.

They need to coordinate across separate suppliers for cells (CATL, LG, Samsung), charger hardware (ABB, Alpitronic, Siemens), and network operation (IONITY, or their own fragmented efforts), adding business friction.

The IONITY consortium (BMW, Ford, Hyundai, Mercedes-Benz, and Volkswagen) illustrates the problem. Five OEMs with different strategies funding a shared charging network cannot match the decision velocity of a single vertically integrated operator. BYD can decide to build 3,000 stations and execute. IONITY must negotiate pricing, vendor selection, and market prioritisation across five headquarters.

The Tesla Benchmark

Tesla wrote the playbook for entering the European EV market. First, build the charging network. Then, build the local factory. Then, sell the vehicles at scale.

Tesla’s first European Superchargers went live in Norway in 2013. Gigafactory Berlin began production in 2022 — nine years later. The strategy was infrastructure first, then production once scale was reached.

BYD is following the same sequence but compressing the timeline. First flash chargers went live in June 2026, and Hungary factory production starts the same year.

BYD has two structural advantages Tesla never had. First, Tesla buys battery cells from CATL and Panasonic. BYD manufactures its own cells — the second largest EV battery maker globally. Second, Tesla’s V4 Superchargers deliver 500kW. BYD’s flash chargers deliver 1,500kW — matched to its own Blade Battery 2.0 architecture.

Not All Chinese Makers Are the Same

The market may treat Chinese EV makers as a group but their European strategies differ significantly.

BYD is the full-stack player. Batteries, vehicles, charger hardware, network operation, factory construction — it controls the entire chain. This makes it the most formidable competitor for European incumbents.

SAIC/MG and Chery are pure-play EV makers with no vertical integration. They are investing in European manufacturing facilities via greenfield projects as well as partnerships with existing plants.

Xpeng and GAC Aion are the asset-light players, via manufacturing contracts through Magna Steyr.

Leapmotor leverages its Stellantis partnership to access two European plants (Zaragoza and Madrid) and an established dealer network. In return, Stellantis gets access to Leapmotor’s EV platform for its own models, including a new Opel EV.

Each strategy has a different risk/reward profile. BYD’s full-stack model is the one European incumbents cannot match structurally. The others are manageable through conventional competition — price, brand, and dealer networks.

This article is a “periodical publication” for information only and is not investment advice or a solicitation to buy or sell securities. This article does not constitute a “personal recommendation” or “investment advice” under UK FCA regulations. Investing in equities involves significant risk. The author holds NO position in the securities mentioned. There is no warranty as to completeness or correctness. Please do your own due diligence or consult a licensed financial adviser. Please read the Full Disclaimer before acting on any information. Images created with the assistance of AI.

From tomorrow morning, Friday 19th June, the world's first listed SpaceTech investment company will be included in the FTSE 250 Index.

That means that Index tracking funds not already in the stock will be paying attention to expanding their portfolios by adding the shares of the £483m-capitalised Seraphim Space Investment Trust (LON:SSIT) onto their holdings.

The inclusion of the group’s equity is said to reflect the growing Trust’s value and reinforces its long-term growth potential, together with the substantial recent intere...

Nanoco Group shares jumped on Thursday after announcing it plans to adjourn Friday’s general meeting, having concluded it is unlikely to secure the backing needed to take the company private.

The board had called the meeting, set for 10.30 a.m. on 19 June, to seek approval for cancelling the ordinary shares’ listing on the Official List and their admission to trading on the London Stock Exchange’s main market.

Pushing that through requires 75% of votes cast, and the directors now accept that the resolutions are unlikely to clear that bar.

Shares were 28% higher at the time of writing, but the future still remains uncertain.

The proposal, first set out on 27 May, was framed as a way to cut operating costs and channel the remaining company resources into its more promising business areas, with the aim of generating greater value for shareholders.

But after talks with shareholders, the directors realised they wouldn’t get the backing required to take the company private and are seeking alternatives.

The board still believes that a delisting would serve investors’ best interests.

Rather than press a vote it expects to lose, the board intends to adjourn the meeting to weigh up other options and keep talking to shareholders.

The company enjoyed a sharp increase in revenue in its half-year ended 31 January and said it had £10m cash as of 30 April. Investors may wonder why the firm would want to take itself private.

Seeing Machines shares were higher on Thursday after announcing it had won a $31 million expansion of an existing automotive production programme with a major European carmaker, deepening one of its established commercial relationships at a time when in-cabin sensing is moving firmly into the mainstream.

The deal widens deployment of the company’s Driver and Occupant Monitoring System across additional vehicle models, with production slated to begin in the second half of 2026.

Delivered through a key Tier 1 partner, it extends programmes already running in China, the United States and Europe.

Paul McGlone, CEO of Seeing Machines, said: “This expansion is a significant milestone for Seeing Machines and reflects both the strength of our technology and the depth of our existing OEM and Tier 1 relationships. The addition of further vehicle platforms demonstrates the opportunity to grow program value over time as customers broaden deployment across their model portfolios.

This is a further phase of adoption by an OEM that already trusts the technology in production, pointing to a customer scaling up rather than testing the waters.

Looking at the bigger picture, carmakers are rolling out driver monitoring across a broader range, driven by tightening safety regulations and buyers who increasingly expect it as standard.

Today’s deal follows a recent $11m win with a Japanese OEM. Seeing Machine shares were 7% higher at the time of writing.

Tesco shares slipped on Thursday after the supermarket revealed sales growth had slowed despite market share growing in the first quarter.

Group sales rose 1% during the period, driven by a 1.8% increase in the UK and 3.3% in Ireland. But this was well below the 3.5% UK growth the group enjoyed in the last full year period.

Mark Crouch, eToro’s Market Analyst said: “Even as growth moderates against tough comparisons from last year, Tesco’s first-quarter update shows the supermarket giant continues to outperform the broader grocery market. Like-for-like sales growth of 1.8% may have fallen short of market expectations, but the more important takeaway is that Tesco is still gaining market share in an intensely competitive environment.”

“The decision to maintain full-year profit guidance suggests management remains confident that its value-led strategy is working. Extending Aldi Price Match to more than 2,000 Express stores underlines Tesco’s determination to protect its customer base as households remain highly price-conscious.”

The efforts to win customers away from the discounters are working – market share is still rising, and sales are up. Investors, however, may start looking to margins and how they will perform against a backdrop of stiff price action to maintain their dominant presence in the UK.

But Tesco seems to have cleared the first hurdle by maintaining its adjusted operating profit guidance for the year between £3.0bn and £3.3bn.

Garry White, Chief Investment Commentator at Charles Stanley, said: With margins under the spotlight, management’s confidence in maintaining full-year profit guidance should reassure investors that Tesco is managing the balance between competitiveness and profitability effectively despite a subdued trading backdrop.”

Tesco shares were down 2% at the time of writing on Thursday.

Nick Trian, Portfolio Manager of Finsbury Growth & Income Trust, provides and introduction to the team’s investment philosophy; focussed on building a concentrated portfolio of “quality”, world-class, UK-listed companies that have strong brands and/or powerful market franchises resulting in a very different portfolio when compared to the benchmark FTSE All-Share Index.

Oriole Resources (LON: ORR) is about to commence drilling at the 85%-owned Wapouze limestone project in Cameroon. It will target outcropping limestone/marble units that have previously been classified as high-grade carbonate material. BCM International will cover $120,000 of drilling costs in return for 24.4 million shares issued at 0.36p each. Discussions with other partners continue. The share price gained 8.31% to 0.365p.

Equity Development has initiated research on Halo Minerals (LON: HALO), which extracts minerals from legacy mining waste. The share price improved 8.22% to 9.875p.

Geo Exploration (LON: GEO) says initial results from airborne surveys have identified a new high priority target at the Gorge project in Western Australia. It has improved the definition of the previously recognised 5km trend of historical gold mineralisation. New uranium anomalies have been identified. The share price rose 6.25% to 0.1275p.

Neil Partington has taken a 3.54% stake in Caledonian Holdings (LON: CHP). The share price is 6% higher at 2.65p.

Arrow Exploration (LON: AXL) reports positive results from the Icaco-2 vertical well in Colombia. The total net pay is 100 feet, and it is producing 830 barrels/day from the Ubaque formation. The drilling programme has been expanded from five to ten wells with a focus on the northern area of the field. Cash is currently $26.7m. The share price is 3.77% ahead at 27.5p.

FALLERS

Gfinity (LON: GFIN) has raised £250,000 at 0.035p/share and this will help to accelerate the commercialisation of Connected IQ and provide working capital. The share price dived 28% to 0.036p.

University technology investor Frontier IP (LON: FIPP) has raised £4m at 12p/share and a retail offer could raise up to £400,000. There was £1.6m in the bank at the end of 2025. There are six core holdings in the portfolio and some of these may be nearing realisations. The cash will help to finance near-term opportunities. It will also help to fund development of the company’s new facility which will help to develop new investee companies. Annual overheads have been reduced to £2.5m. The NAV was 52.7p/share at the end of 2025. The share price slumped 25.6% to 12.65p.

A placing by Acuity RM (LON: ACRM) has raised £400,000 at 0.75p/share and a retail offer could generate up to £50,000. The cybersecurity risk management company wants to invest in sales and marketing and development of new AI product Risk OS. The 2025 revenues were flat at £2.1m, but the operating loss fell to £190,000. Cash was £322,000 at the end of 2025. The share price slipped 18.9% to 0.75p.

Switch Metals (LON: SWT) has commenced drilling at the Issia project targeting hard rock tantalum and lithium. Maiden tantalum mineral resource estimate work is at and advanced stage. The share price fell 4.65% to 10.25p.

The FTSE 100 fell on Wednesday, with commodity shares weighing on the index as oil prices continued to fall back.

Brent Crude is now trading at $79 after hitting highs above $110 in the depths of the Middle East conflict.

UK inflation provided a reason to be optimistic on Wednesday as May’s CPI reading came in cooler than expected at 2.8% versus expectations of 3%.

The pound fell against the dollar in the immediate reaction to the news, but this failed to translate into any meaningful support for the FTSE 100.

Lale Akoner, Global Market Strategist at eToro, says: “The inflation scare markets were worried about didn’t really pan out. Today’s numbers give the Bank of England a bit more flexibility, but don’t expect any rush to cut rates.”

“Services inflation is still too high, and with energy bills heading higher over the summer, policymakers will want to see wages cool more decisively before they sound confident the job is done.”

Although prices still rose at a worrying rate in May, particularly energy prices, falling oil prices since the announcement of a deal between the US and Iran could help lower inflation in the coming months.

We’ll learn more about the trajectory of interest rates from the Bank of England later this week, when it issues its interest rate decision.

Oil prices and inflation expectations were driving the FTSE 100 trade on Wednesday, with oil majors weighing on the index and offsetting gains in interest rate-sensitive sectors.

Susannah Streeter, Chief Investment Strategist, Wealth Club, said that the “easing of oil prices weighs on energy giants, but consumer-focused stocks are rising as there’s light at the end of the tunnel for households dealing with a deluge of higher bills. Clothing retailers, housebuilders and airlines have nudged higher as the chances of rate hikes ease off and hopes are high that consumers may have a bit more to spend than expected.”

BP and Shell lost 1% each. Shell is now around 20% lower than its most recent high and has erased almost all of the gains since the Middle East conflict began.

Miners were also lower, acting as a drag on the index. Rio Tinto was 1.6% lower at the time of writing.

Rolls-Royce was the FTSE 100’s top riser as the stock rose 1.9% and flirted with all-time highs.