With both of the FTSE 100’s major oil companies recently reporting, the BP share price (LON:BP) and Shell (LON:RDSB) have become very different propositions to the companies investors are traditionally accustomed to.

In the wake of the coronavirus crisis, the global oil market is yet to recover and has forced major changes at London’s largest oil companies.

In this article we explore whether the BP share price now offers better value than the Shell share price given the historic conditions in the global energy market.

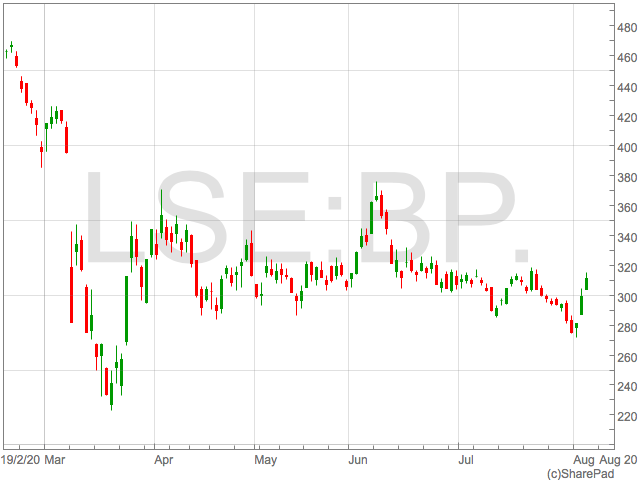

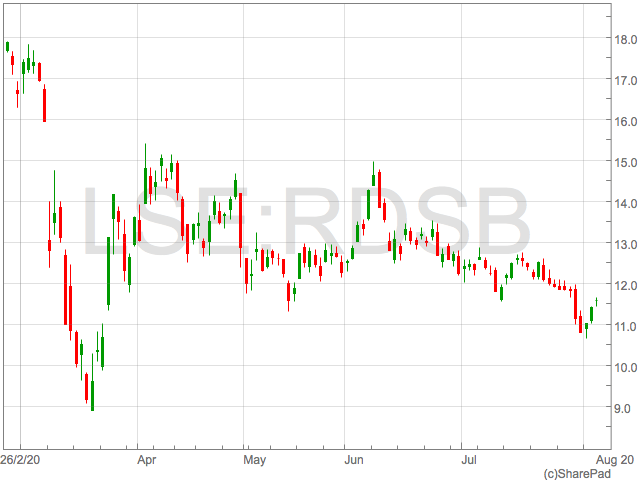

BP share price

By first looking at the the BP share price in absolute terms, it is evident that BP has outperformed Shell in 2020 with BP shares down 34% year-to-date and Shell losing 46% of it’s value.

Having trading mostly inline with each other, a deviation in the two companies became pronounced as the two companies announced their second quarter earnings.

This deviation was largely noticeable in the performance of the shares on the respective days of their announcements, providing a gauge of investor sentiment to the underlying performance of the businesses.

BP shares rallied some 4%, whilst Shell sank around 6% on the day of their announcements.

The rally in BP shares took place despite a cut in their dividend, suggesting the market had largely priced in a reduction in payouts and were more concerned with the underlying profitability and management of the companies.

Second Quarter Losses

Both companies reported historic drops in profitability. BP reported a $6.7 billion adjusted loss in the second quarter compared with a $2.8 billion profit in the same period a year prior.

Shell, on the other hand, produced an adjusted profit of $600 million, down from $3.5 billion a year ago

With BP swinging to huge loss but still able to stage a rally, the reaction in the share prices following the releases should be attributed to analyst estimates going into results.

The reaction in BP’s share price reflects the significant beat of a loss of $8.45 billion, predicted by analysts polled by Bloomberg whilst Shell beat by a much smaller margin.

Dividends

As BP released the dramatic loss, they took the historic decision to slash their dividend in half by cutting it from 10.5 cents to 5.25 cents.

With GBP/USD exchange rates currently at 1.309, this equates to 4.01p meaning if this level of dividend is maintained, investors can expect an annual yield of 5% from a BP share price of 314p.

Shell took the decision to cut their dividend in the prior quarter, slashing the dividend by two thirds to 16 cent. This was maintained in the second quarter and with Shell trading at 1,158p, investors in Shell will be receiving a yield of 4.2%.

Based purely the income from the two shares, BP would seem more attractive to income seekers with their higher yield, but this approach is too simplistic to fully evaluate the relative value of each company’s equity.

It must be noted the earnings coverage of these dividend is non existent in the case of BP and negligible in the case of Shell so attention must be paid to the cash position of each company.

Cash

BP’s cash position has actually improved based from the end of 2019 as the company tapped the bond market for cash to the tune of $11 billion.

The bond issue, coupled with $25 billion of impairments and writes offs, helped offset BP’s whopping $20 billion pretax loss meaning BP’s cash rose to $34.6 billion from $18 billion in the first quarter.

With dividend payments reducing, this amount of cash would seem sufficient to support dividends and provide resources for their shift strategy towards a low carbon energy producer.

However, the $20 billion pretax loss should be a concern for investors as a similar drain in the coming quarters would put the cash position under pressure.

This is highlighted by BP’s lack of Free Cash Flow. Measured by deducting investing cash from operational cash flow, BP’s Free Cash Flow amounts to a $272 million deficit.

Shell, conversely, produced Free Cash Flow of $12 billion, suggesting Shell has greater scope to invest in the next chapter of their shift towards greener fuels and the next big growth area for energy companies.

Shift To Renewables

Shift To Renewables

With the destruction of oil demand and associated fall in oil prices, the focus on renewables has increased for both BP and Shell.

Both companies have strategies to increase the proportion of clean power they produce, and when assessing the relative value of each over the long term, this must be central to any valuation thesis.

However, with revenue from renewables limited in both companies, the judgement of their low carbon activities falls to natural gas.

In this respect, Shell has a far larger exposure to natural gas and would be judged to be ahead of BP in becoming a greener energy producer.

Summary

With the absence of any meaningful multiples based on earnings in the first half of 2020, the assessment of value falls to cash and ability to shift towards the demands of government targets on emissions.

In both of these respects we would feel Shell has the edge over BP, despite BP providing investors with a higher yield.