In this episode, we sit down with Alexander Selegenev, Executive Director of TMT Investments, the AIM-listed venture capital firm focused on high-growth technology companies across AI, software, and fintech.

Alexander opens with an introduction to TMT’s business and investment philosophy, then walks us through the firm’s strategy and thesis in detail.

We explore how TMT balances genuine excitement about artificial intelligence with the valuation discipline required to generate returns for shareholders.

We dig into the numbers, asking why deployed capital fell sharply in 2025 compared to the prior year, and what that tells us about how the team is reading the current opportunity set. Alexander then takes us through the portfolio’s core holdings, including the standout story of Scale AI, which delivered a 138% uplift in just eight months following Meta’s investment, and what originally attracted TMT to the business.

We also look at Bolt, now EBIT positive and active in more than 800 cities globally, and discuss how close the ride-hailing giant might be to an IPO or significant exit event. On the other side of the ledger, Alexander addresses the write-downs seen over the past year and the factors behind them.

Alexander provides insight into their thinking around balancing special dividends with share buybacks and what success looks like for TMT Investments.

RC Fornax has had a tough start to life as a publicly traded company, with poor sales and management issues driving shares down by 75% since its IPO in early 2025. But today’s update shows the firm may be heading in the right direction.

The defence engineering consultancy has reported a sharp pickup in order intake, with the company now guiding for more than £5.1 million in sales under purchase order or subject to contract for the current financial year.

This compares to around £4 million in revenue in 2025.

The AIM-quoted company said it secured around £1.9 million in orders during its second quarter, covering December through February, despite the usual seasonal lull over the Christmas period.

March has continued in the same vein, with roughly £1.4 million in new orders in the month alone, including three new purchase orders, two new public-sector opportunities, and six extensions to existing contracts.

That follows what the company described as its strongest ever quarter in the opening three months of FY26. Management points to a combination of improved market conditions and internal operational changes as the drivers, noting that it has already secured more recurring purchase orders this year through extensions and new wins than it did throughout FY25.

“The progress we are seeing represents a clear step change in the scale and consistency of our commercial performance. We are now delivering materially higher levels of orders on a recurring basis, with this improved run rate providing a stronger foundation for revenue visibility. Importantly, this momentum is not only supporting our expectations for the current year but is also establishing a more meaningful platform as we look ahead,” said Paul Reeves, Chief Executive Officer of RC Fornax.

“We are particularly encouraged by the strength of performance in the recent period, which delivered a robust level of order intake despite seasonal factors, and by the strong momentum we are seeing at the start of the current period.”

Building products supplier Brickability (LON: BRCK) has received an unsolicited bid approach from Atlas Holdings LLC and after initial contact and exchange of information a 65p/share indicative offer was made. The share price has not been that level since June 2025. That offer was rejected by the board. Atlas will be provided with additional information to see whether it can come up with a better offer. The share price jumped 26.3% to 51.8p.

Defence sector services provider RC Fornax (LON: RCFX) has won £1.4m in orders so far in the third quarter. Cavendish has maintained its full year forecast loss of £2m. The share price recovered 12.45 to 8.15p.

GreenRoc Strategic Materials (LON: GROC) says it has “achieved an independent ESG rating of BB following its latest annual submission to Digbee ESG”. The corporate ESG rating improved to BBB. The share price improved 13.1% to 4.75p.

CleanTech Lithium (LON: CTL) has published the pre-feasibility study for the Laguna Verde lithium brine project in Chile. This shows a NPV10 of $699m over a 25-year period. This assumes extracting 15,000t per year of battery-grade lithium carbonate. The operating cost is assumed to be $5,768/t and a sale price of $22,500/t. Upfront capex is $748m. First production would be 2031. The share price rose 10.1% to 9.25p.

FALLERS

Trading was restored in Ironveld (LON: IRON) shares following the publication of full year results to June 2025 and interims to December 2025. Cash was £75,000 at the end of 2025. The company is exploring funding operations. It hopes to generate cash when Daemaneng restarts operations and is producing DMS-grade magnetite. The share price slumped 44.8% to 0.024p.

Wellheads and connectors Plexus Holdings (LON: POS) reported a reduction in interim revenues from £2.9m to £1.2m because of delays in projects, particularly in the North Sea due to tax uncertainty and inability to offset decommissioning costs. Activity is likely to remain subdued in the second half with the assumption that work will recover in 2026-27. A full year loss is forecast before a return to profit in 2026-27. The share price lost 37% to 2.9p.

Digital finance hub Tap Global Group (LON: TAP) interim revenues fell from £1.8m to £1.7m. There was also £210,000 of income from settlement with crypto currency exchange Bitfinex. Cash was £433,000 at the end of 2025. The share price slipped 35.7% to 1.125p.

Beowulf Mining (LON: BEM) needs to secure additional cash in the near term. Heads of terms have been signed for the sale of Kosovo-based Vardar. This will help to finance the Kallak iron ore project PFS. Investors are being sought for Grafintec and this could raise €5m. The share price declined by one-quarter to 4.5p.

Bezant Resources (LON: BZT) has raised £2.07m at 0.065p/share. This will fund the acquisition of a further 20% of the Hope and Gorob copper gold project, taking the stake to 90%, and improve productivity at the processing plant. The share price dipped 20.6% to 0.0675p.

The FTSE 100 surged again on Tuesday after Donald Trump suggested he would end the war without reopening the Strait of Hormuz.

London-listed stocks jumped on the news, with the FTSE 100 trading above 10,200 in early trade. Oil prices slipped on the news, but Brent still remained above $110 per barrel.

Donald Trump’s comments suggest there could be an end to the war without the US securing some of its previously stated aims. There are signs that both sides could walk away claiming victory.

But Trump’s unpredictability makes any market positioning risky as he’s liable to post something to the contrary before long.

That could be why stocks rallied on Tuesday, but oil remained steady. Energy traders seemed unprepared to wind down their long positions with tensions still high in the region amid ongoing attacks.

Stocks, on the other hand, were quite happy to rally on the slightest hint of optimism on the suggestion that the conflict could be entering its final stages.

“The FTSE 100 consolidated Monday’s gains to stand firmly above the 10,000 mark as investors continue to weigh competing narratives over the Iran conflict,” said AJ Bell investment director Russ Mould.

US futures also rose on Tuesday, pointing to a stronger session in the cash market this afternoon.

London’s interest rate-sensitive stocks were among the best performers of the session.

Should the conflict end in the near term and the oil shock be prevented from causing a material impact on the global economy, there’s a whole raft of UK-listed stocks that will start to look attractive.

They include some of Tuesday’s top risers, including JD Sports, Barratt Developments, and the top riser at the time of writing, Antofagasta, which was 2.6% higher.

Housebuilders have been crushed during the Middle East war and could be among the sectors to recover if it looks like interest rates won’t have to be hiked to fight off inflation.

Persimmon added 0.8% as Barratts rose 2%.

Unilever shares were 0.7% higher after confirming late-stage talks on the potential sale of its foods business to McCormick for a reported mix of $15.7 billion in cash and McCormick shares, with Unilever owning 65% of the new entity.

“The market could be about to make its own version of Marie Rose sauce as a combination between Unilever’s food business, which encompasses Hellman’s mayonnaise, and McCormick, owner of French’s Ketchup, moves closer to fruition,” Russ Mould said.

“The presence of activist investor Nelson Peltz on the shareholder register since 2022 has led to consistent pressure on Unilever’s management to streamline the business.

“Having shed its ice cream division last year, this demerger of its food business is the first big strategic move under CEO Fernando Fernandez since he took the top job a year ago.”

The prospect of an end to the conflict is making the oil majors less attractive, with BP and Shell falling on Tuesday. BP was down 0.3%.

Written by Nick Brind, George Barrow & Tom Dorner, co-managers of the Polar Capital Global Financials Trust.

The global economy is entering a more complex phase. Interest rates are no longer anchored near zero. Governments are deploying fiscal policy more actively. Capital investment – in infrastructure, energy security, defence and digital capacity – is rising in strategic importance.

Financial companies sit at the centre of these shifts. They intermediate savings, allocate capital, underwrite risk and facilitate transactions. When the economic regime changes, the transmission mechanism runs directly through the financial system.

After a prolonged period defined by ultra-low interest rates and cautious balance sheet management, the financials sector today is operating in an environment in which capital generation and productivity gains may become more important drivers of returns.

The war in the Middle East is a reminder that this evolving economic backdrop is unlikely to be linear. It has contributed to higher energy prices and increased market volatility, reinforcing the importance of resilient balance sheets and disciplined capital allocation across the financial system.

We are liable to continue to see periods of uncertainty such as this and the impact it has on nearer-term growth and inflation. However, our focus is very much on the longer-term structural drivers, discussed below, that remain intact.

Normalised rates and capital discipline

For much of the previous decade, interest rates in developed markets were exceptionally low. That contributed to compressed margins in parts of the banking system and distorted the pricing of risk across asset classes.

A more normalised interest rate backdrop changes the equation. Banks are better able to earn appropriate spreads on deposits and loans. Insurers can reinvest premiums at more attractive yields. Savers once again receive compensation for capital. Risk is more explicitly priced.

This does not eliminate risk. Higher rates can expose weaker borrowers and create credit stress if growth slows. However, from a structural perspective, the financial system is operating in a more economically rational framework than during the zero-rate era.

At the same time, fiscal policy is becoming more active. Public investment initiatives require financing and private sector capital expenditure is responding to shifting geopolitical and supply chain realities. A well-capitalised and functioning financial system is essential to supporting that activity.

Regulatory recalibration

The financial system is entering this phase from a position of strength. Over the past decade, capital levels have risen materially and supervisory oversight has remained rigorous. Balance sheets are much more conservative and liquidity buffers higher than in previous cycles.

More recently, policymakers in parts of the US and Europe have begun to discuss whether elements of the regulatory framework can be simplified without compromising stability. In the US, proposals under discussion would allow large banks greater flexibility in returning capital to shareholders, supporting loan growth and improving capital efficiency. In Europe, there is growing focus on simplification and consolidation to enhance competitiveness.

This is not a wholesale loosening of safeguards. Rather, it reflects recognition that regulatory regimes can accumulate complexity over time. For investors, improved capital efficiency – if delivered prudently – can support stronger returns on equity while preserving resilience.

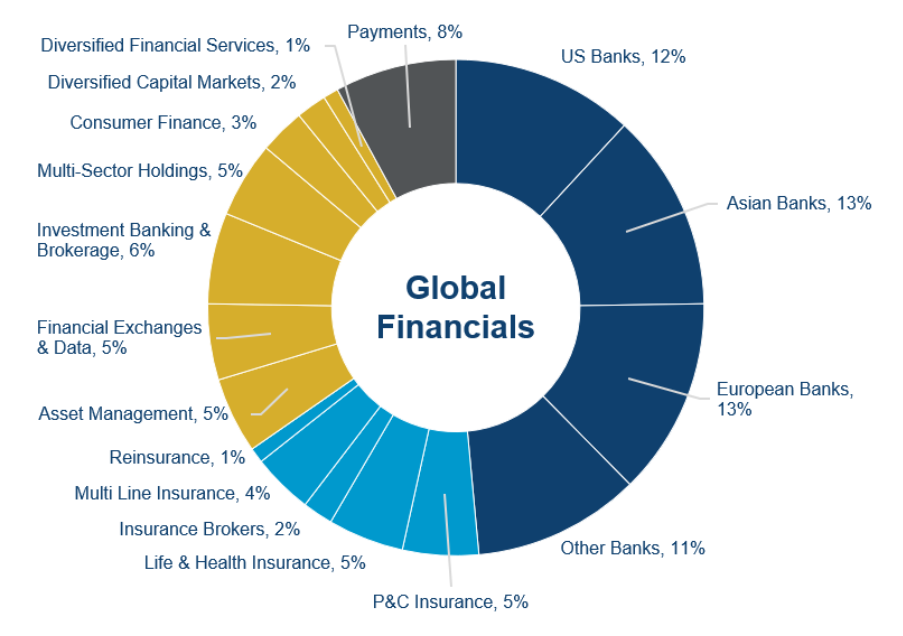

A broad and differentiated sector

Financials are the second largest sector within global equity markets and encompass a wide range of business models.

Source: MSCI, 30 January 2026.

Banks are one component, but insurers, exchanges, trading platforms, asset managers and specialist lenders each have distinct earnings drivers. Life insurers benefit from demographic and savings trends. Exchanges and platforms can benefit from elevated market activity. Asset managers are leveraged to flows and equity markets. Emerging market lenders operate in economies where financial penetration continues to deepen.

These subsectors respond differently to interest rates, growth, inflation and volatility. The diversity of drivers within financials allows for differentiated sources of return across the cycle.

In certain regions, particularly Europe, valuations remain at discounts relative to broader equity markets despite improved profitability. While valuation alone is not a catalyst, it can provide a degree of support if earnings remain disciplined and capital allocation rational.

Productivity and technology

Technological advancement is another important structural factor. Artificial intelligence and advanced data analytics are reshaping many industries. Earlier this year, concerns about disruption contributed to volatility across parts of the financial sector.

However, financial services are inherently data-rich and process-intensive. Credit assessment, fraud detection, compliance monitoring and customer servicing are areas where automation can enhance efficiency and accuracy. Several institutions have cited tangible productivity gains and medium-term return targets supported by technology adoption.

External research suggests that banking and insurance are among the sectors most exposed to productivity improvements from AI deployment. For well-capitalised incumbents, scale and data depth can be competitive advantages.

Rather than displacing established institutions, technology may reinforce the operating leverage of those able to implement it effectively.

Capital allocation and income

Financial companies are significant generators of cashflow. When capital buffers are comfortably above regulatory minimums, this can support dividends and, where appropriate, share buybacks.

The Polar Capital Global Financials Trust operates an enhanced dividend policy targeting a 4% annual distribution, paid quarterly. While dividends are not guaranteed and may be reduced in adverse market conditions, capital discipline remains central to our approach.

The Trust invests across the global financials universe, including banks, insurers, payment companies, exchanges and asset managers. Approximately 40% of the portfolio is currently invested in US and European banks, reflecting our view that many of these institutions combine strong balance sheets with improving capital efficiency and exposure to evolving macro conditions.

Active management is essential in a sector shaped by economic cycles, regulatory change and subsector rotation. Within the portfolio, we balance exposure to US banks benefiting from regulatory recalibration, European banks trading at valuation discounts, insurers positioned for long-term savings growth and platforms that can benefit from elevated market activity. This diversified positioning reflects our view that different parts of the sector will lead at different stages of the cycle.

Positioned for the next phase

The defining features of the previous era – ultra-low rates, subdued credit growth and continual regulatory tightening – are evolving. Today our investment world is characterised by stronger balance sheets, normalised interest rates, more active fiscal policy and regulatory recalibration.

Financials will not deliver returns in a straight line. Cyclical setbacks are inevitable, and periods of volatility should be expected. However, the sector’s central role in capital formation – combined with improved resilience, disciplined underwriting and more efficient capital allocation – suggests it is positioned differently for the phase ahead.

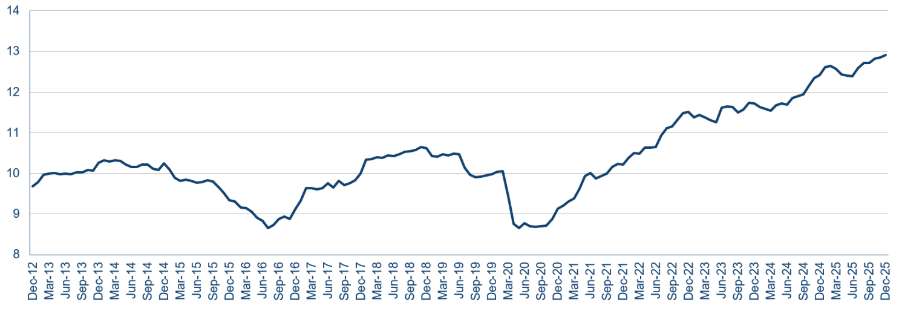

The graph below shows that financial companies are becoming more profitable, with their return on equity – a measure of how efficiently companies generate profits – has improved significantly.

Financials delivering stronger returns (%)

Source: Polar Capital, Bloomberg, 31 December 2025. Note: Return on Equity shown for the benchmark; MSCI All Country World Index Financials Index.

For the Trust, this aligns closely with how the portfolio is constructed. We focus on well-capitalised institutions with durable franchises, prudent risk cultures and the ability to generate attractive returns across the cycle. Our exposure to US and European banks reflects our view that capital efficiency and regulatory evolution can support sustainable profitability, while our holdings across insurers, exchanges and asset managers provide differentiated earnings drivers within the broader financial ecosystem.

In our view, the sector today combines three features that rarely coincide: structural resilience, improving capital dynamics and supportive macroeconomic conditions. That does not eliminate risk, but it does create a more constructive foundation than has existed for much of the past decade. The sector’s return on equity has improved materially over recent years, reflecting both stronger balance sheets and more disciplined capital allocation. For long-term investors willing to accept cyclical variability, we believe financials – and active exposure to them through a specialist strategy – offer a compelling opportunity as the economic regime continues to evolve.

The Company is an investment company with investment trust status and its shares are excluded from the Financial Conduct Authority’s (“FCA”) restrictions on the promotion of non-mainstream investment products. The Company conducts its affairs, and intends to continue to conduct its affairs, so that the exemption will apply.

The Company is an Alternative Investment Fund under the EU’s Alternative Investment Fund Managers Directive 2011/61/EU as it forms part of UK law by virtue of the European Union (Withdrawal) Act 2018.

The Investment Manager

Polar Capital LLP is the investment manager of the Company (the “Investment Manager”). The Investment Manager is authorised and regulated by the FCA and is a registered investment adviser with the United States’ Securities and Exchange Commission.

Key Risks

Investors’ capital is at risk and there is no guarantee the Company will achieve its objective.

Past performance is not a reliable guide to future performance.

The value of investments may go down as well as up.

Investors might get back less than they originally invested.

The value of an investment’s assets may be affected by a variety of uncertainties such as (but not limited to): (i) international political developments; (ii) market sentiment; and (iii) economic conditions.

The shares of the Company may trade at a discount or a premium to Net Asset Value.

The Company may use derivatives which carry the risk of reduced liquidity, substantial loss and increased volatility in adverse market conditions.

The Company invests in assets denominated in currencies other than the Company’s base currency and changes in exchange rates may have a negative impact on the value of the Company’s investments.

The Company invests in a concentrated number of companies based in one sector. This focused strategy can lead to significant losses. The Company may be less diversified than other investment companies.

The Company may invest in emerging markets where there is a greater risk of volatility than developed economies, for example due to political and economic uncertainties and restrictions on foreign investment. Emerging markets are typically less liquid than developed economies which may result in large price movements to the Company.

Important Information

Not an offer to buy or sell:

This document is not an offer to buy or sell or a solicitation of an offer to buy or sell any security, and under no circumstances is it to be construed as a prospectus or an advertisement. This document does not constitute, and may not be used for the purposes of, an offer of the securities of, or any interests in, the Company by any person in any jurisdiction in which such offer or invitation is not authorised.

Information subject to change:

Any opinions expressed in this document may change.

Not Investment Advice:

This document does not contain information material to the investment objectives or financial needs of the recipient. This document is not advice on legal, taxation or investment matters. Prospective investors must rely on their own examination of the consequences of an investment in the Company. Investors are advised to consult their own professional advisors concerning the investment.

No reliance:

No reliance should be placed upon the contents of this document by any person for any purposes whatsoever. None of the Company, the Investment Manager or any of their respective affiliates accepts any responsibility for providing any investor with access to additional information, for revising or for correcting any inaccuracy in this document.

Performance and Holdings:

All data is as at the document date unless indicated otherwise. Company holdings and performance are likely to have changed since the report date. Company information is provided by the Investment Manager.

Benchmark

The Company is actively managed and uses the MSCI ACWI Financials Net TR Index as a performance target.. The benchmark has been chosen as it is generally considered to be representative of the investment universe in which the Company invests. The performance of the Company is likely to differ from the performance of the benchmark as the holdings, weightings and asset allocation will be different. Investors should carefully consider these differences when making comparisons. Further information about the benchmark can be found here.

Third-party Data

Some information contained in this document has been obtained from third party sources and has not been independently verified. Neither the Company nor any other party involved in compiling, computing or creating the data makes any warranties or representations with respect to such data, and all such parties expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any data contained within this document.

Country Specific Disclaimers

United States

The information contained within this document does not constitute or form a part of any offer to sell or issue, or the solicitation of any offer to purchase, subscribe for or otherwise acquire, any securities in the United States or in any jurisdiction in which such an offer or solicitation would be unlawful. The Company has not been and will not be registered under the United States Investment Company Act of 1940, as amended (the “Investment Company Act”) and, as such, the holders of its shares will not be entitled to the benefits of the Investment Company Act. In addition, the offer and sale of the Securities have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”). No Securities may be offered or sold or otherwise transacted within the United States or to, or for the account or benefit of U.S. Persons (as defined in Regulation S of the Securities Act). In connection with the transaction referred to in this document the shares of the Company will be offered and sold only outside the United States to, and for the account or benefit of non-U.S. Persons in “offshore- transactions” within the meaning of, and in reliance on the exemption from registration provided by Regulation S under the Securities Act. No money, securities or other consideration is being solicited and, if sent in response to the information contained in this document, will not be accepted. Any failure to comply with the above restrictions may constitute a violation of such securities laws.

Further Information about the Company

Investment in the Company is an investment in the shares of the Company and not in the underlying investments of the Company. Further information about the Company and any risks can be found in the Company’s Key Information Document, the Annual Report and Financial Statements and the Investor Disclosure Document which are available on the Company’s website, found at: https://www.polarcapitalglobalfinancialstrust.com

BRCK Group has rebuffed a takeover approach from US private equity firm Atlas Holdings, saying the indicative 65 pence per share cash proposal put to the board in March fundamentally undervalues the business.

Atlas made its first unsolicited, non-binding approach in February, prompting BRCK’s board to engage under NDA to assess whether a recommendable offer might materialise. It didn’t.

When Atlas tabled its 65p proposal on 17 March, the board unanimously rejected it eight days later. BRCK is doing its best to fight off pressure from the US group, which clearly sees more value in building a products and services group than the UK market does.

BRCK has nonetheless left the door slightly ajar, agreeing to share limited further information with Atlas to see whether it is willing to improve its price.

The board has made clear, however, that it won’t be drawn into a full due diligence process unless Atlas comes back with something it would actually be prepared to recommend to shareholders.

GenIP has issued a bullish commercial update, pointing to continued order flow across the US, Asia and other key markets as it heads into 2026 on the back of around 330% revenue growth in FY25.

Asia has been a major strength for the group, growing by roughly 3,500% year on year and now accounting for the largest share of the company’s revenue.

Europe and Latin America also contributed meaningfully, up around 111% and 51% respectively, though from smaller bases.

There were no revenue figures in today’s update, but the announcement pointed towards growth in key offerings.

The technology commercialisation platform says client demand is shifting towards larger, multi-year engagements at the portfolio level rather than one-off technology evaluations. The company believes this trend should support both revenue visibility and deal sizes going forward.

Renewal conversations with FY25 clients are said to be progressing well, with several looking to expand their scope, consistent with the company’s reported 90% retention rate. This should see revenues grow again in the current financial year.

On the product side, GenIP said Invention Prioritizer is now in active use with several clients, including Brazil’s National Nuclear Energy Commission, while Invention Validator is completing its first deployment at a South African research university, carrying an expected 60% gross margin.

GenIP has also been building out its commercial team, bringing in a global enterprise sales lead to tap its previously largely unexplored corporate market, alongside a Latin America specialist with WIPO advisory credentials and a further Asia hire in the pipeline.

With its largest market still accelerating and a growing institutional pipeline at advanced stages across multiple regions, GenIP appears poised to build momentum as we move through 2026.

“GenIP is delivering strong progress across all of our strategic priorities. Asia’s exceptional growth, Europe’s accelerating momentum and the long-term potential we see in Latin America demonstrate the global demand for our platform and products,” said Melissa Cruz, Chief Executive Officer of GenIP.

“Clients are deepening their engagement with us, adopting our broader product suite and increasingly seeking portfolio-level insight. With a growing pipeline, strong renewal activity and a clear strategic focus, GenIP is well positioned for its next phase of growth.”

GenIP shares were hit last after the company conducted a heavily discounted placing. Since then, shares have built a base around 9p – 10p and now have a market cap of less than £2m.

The FTSE 100’s commodity sectors helped drive outperformance on Monday as Donald Trump threatened to seize Iran’s key oil hub on Kharg Island.

London’s leading index was 0.9% higher, at 10,062, at the time of writing, as oil traded above $115 and metal prices rose. The German DAX was just 0.3% higher.

“Market nervousness around the situation in the Middle East continues to ratchet up as the Iran conflict enters a fifth week,” says AJ Bell head of financial analysis Danni Hewson.

“Comments from President Trump about seizing Iranian oil and the country’s Kharg Island export hub, a build-up of US troops and the involvement of Tehran-backed Houthis in the war all create the impression of a conflict that is escalating rather than drawing to a close.”

The FTSE 100 managed to shake off souring sentiment on Monday due to its heavy weighting in commodity companies. But it was not oil majors driving the index higher, rather metals companies such as Rio Tinto, Melten Energy & Metals, and Glencore.

Mining shares rose on Monday after strikes at aluminium facilities in the UAE and Bahrain threatened already-constrained supply and drove prices higher.

Rio Tinto was the top riser, adding 3.6%.

Oil prices at $115 per barrel served as another buying signal for the FTSE 100 oil majors, which have been trading steadily higher amid the war in the Middle East. Shell added 1.4%, and BP rose 1.6%. The pairs gains were measured, but their weighting within the FTSE 100 went a long way to lifting the index.

A 1.6% rally in AstraZeneca, the FTSE 100’s largest constituent by market cap, played a part in index-level gains on Monday.

Financials St James’s Place, Prudential, and M&G were among the worst performers on the session.

Since falling sharply after the US and Israel launched attacks on Iran at the beginning of March, the FTSE 100 has formed a range between 9,850 and 10,100 as the index trades headline to headline.

Traders will be aware that it will likely take a major escalation or de-escalation in the conflict for the FTSE 100 to break out. A break could be fast and dramatic.

Halo Minerals shares sank on its AIM debut today, after raising £4 million at 18p per share to advance a copper extraction project targeting legacy mining waste in northern Chile.

The company began trading under the ticker HALO with a market cap of around £20 million before shares sank around 26% to trade at 13.25p,

The company’s core asset is the Playa Verde Project in the Atacama Region, comprising six mining concessions covering 13.57 square kilometres of copper-bearing tailings near the coastal town of Chañaral.

The project carries a JORC-compliant mineral resource of 53 million tonnes at 0.24% copper, with ore reserves of 32.2 million tonnes at 0.25% copper, containing around 79,000 tonnes of fine copper.

Based on those reserves, and using a copper price of $5.30 per pound, the project carries a post-tax NPV of $154 million and an IRR of 50.9%. These are attractive numbers, but not ones that have inspired confidence in the company as trading began on Monday.

The IPO is intended to take Playa Verde to a final investment decision or to a point at which alternative project funding can be secured.

Beyond Chile, Halo says it will also pursue additional growth opportunities in other jurisdictions. Investors in the IPO will hope the £4 million war chest can be put to work to progress these before long after the poor start to life on AIM.

Cairn Financial Advisers is acting as nominated adviser with Global Investment Strategy UK as broker.

Pulsar Helium (LON: PLSR) executive chair Neil Herbert exercised nearly 1.6 million options at C$0.45 each, raising C$719,000 for the company. The share price increased 17.5% to 121p.

Abingdon Health (LON: ABDX) has won a series of contracts worth £4.8m with a US client. This covers the development of multiplex quantitative lateral flow assay systems for human testing which will be delivered over 27 months. This supports the decision to expand capacity in the US. There could be a subsequent manufacturing contract. The company is set to move to around breakeven in 2026-27. The share price gained 10.3% to 8p.

Monoclonal antibodies developer Bioventix (LON: BVXP) reported interim revenues 9% lower at £6.2m. China was a tough market and some products are maturing. Pre-tax profit was slightly lower at £4.9m. Cash was £5.1m at the end of 2025. The customer base is being broadened and there is longer-term potential for royalties from the company’s antibodies that are included in products. Full year pre-tax profit is set to fall from £10.2m to £9.6m. The full year dividend is set to be unchanged at 150p/share even though it is not going to be covered by earnings. The share price recovered 9.09% to £15.

Security printing and authentication services provider Spectra Systems (LON: SPSY) more than doubled pre-tax profit to $25.2m on revenues 31% ahead at $64.3m in 2025. This was boosted by a major contract. The dividend is 17% higher at 13.6p/share. Net cash is $11.1m. The closure of the business in France has been delayed. Zeus has upgraded its 2026 pre-tax profit forecast by 12.5% to $11.1m. The share price rose 8.73% to 137p.

FALLERS

In-game advertising technology developer Mirriad Advertising (LON: MIRI) says that the expected upturn in February and March did not happen because of the Middle East conflict. It did sign a services agreement with a UK media conglomerate. There is £675,000 in the bank, but more cash will be required before the 2025 accounts are published. The share price dived 63.6% to 0.002p.

Pri0r1ty Intelligence (LON: PR1) says auditors still have not completed the audit for the year to September 2025 and trading in the shares will be suspended on 1 April. The AI business undertook two acquisitions, including a reversal, last year which complicates the accounts. There is also an impairment review on intangible assets. The share price slipped by one-fifth to 1.6p.

Wound healing technology developer AOTI Inc (LON: AOTI) says 2025 revenues were $66.5m, up 15% on 2024. Underlying pre-tax profit was $3.1m, compared with a loss last year. Net debt reached $6.5m. There is a $1.7m provision on money owed by Arizona. Revenues could still rise this year even though AOTI is pulling out of Arizona due to difficulty in getting paid, but profit could decline to $1.2m before starting to grow again. Outstanding debt from Arizona may eventually be reclaimed. A CMS local coverage determination is still expected in the near-term and that will provide some positivity. The share price declined 13.65 to 28.5p.

Graphene technology developer Directa Plus (LON: DCTA) is in discussions with an institution that could provide funding of up to £2.5m. This would require shareholder approval. Talks with Nant Capital ended without agreement on a non-dilutive loan. Directa Plus has enough cash until May but needs more funds to continue trading after that. The sale of a property could raise €500,000 and the Sectar subsidiary could also be sold. The share price fell 11.8% to 7.5p.