Whitbread announces rights issue to navigate COVID-19

Dow Jones keen to rebound after Moderna vaccine doubts

The buoyant start for the US gave a boost to European equities, which had initially suffered a sluggish opening. The DAX rose 0.7% to 11,170, while the CAC followed with a 0.2% increase, pushing it past 4,450 points.

Speaking on the UK, Spreadex Financial Analyst Connor Campbell stated,

The FTSE was up 0.6%, pushing the UK index back towards 6050. This as the pound fell 0.2% against the dollar and 0.6% against the euro. The fact Bank of England chair Andrew Baily refused to rule out negative interest rates – like Fed head Jerome Powell appeared to do last week – likely aided the FTSE and hurt the pound. Meanwhile against the euro specifically a better than forecast consumer confidence reading from the across the Eurozone gave the single currency a boost – it was also up half a percent against the greenback.

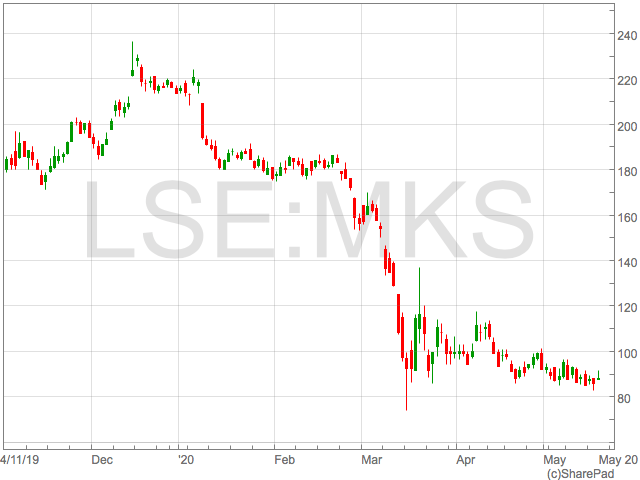

Marks and Spencer profit drops as strategy shifts towards food

The acquisition of a stake in Ocado Retail was probably the highlight of this strategy shift and is already providing M&S with a return. M&S acquired a 50% stake in Ocado Retail in 2019 for £750m to help boost their food offering as clothing sales continued to disappoint.

Marks and Spencer recognised a £2.6m profit from it’s investment in Ocado Retail in the 7 months to 1st March.

Shareholders will be pleased with the early news from the Ocado acquisition as sales at Ocado Retail jumped 40.4% in the 9 week period to 6th May, due to lockdown restrictions causing rocketing demand for home deliveries.

The market took the results well and shares rose over 2% on Wednesday morning. However, Marks and Spencer shares are down 63% over the last year, seeing them lose their position in the FTSE 100.

The acquisition of a stake in Ocado Retail was probably the highlight of this strategy shift and is already providing M&S with a return. M&S acquired a 50% stake in Ocado Retail in 2019 for £750m to help boost their food offering as clothing sales continued to disappoint.

Marks and Spencer recognised a £2.6m profit from it’s investment in Ocado Retail in the 7 months to 1st March.

Shareholders will be pleased with the early news from the Ocado acquisition as sales at Ocado Retail jumped 40.4% in the 9 week period to 6th May, due to lockdown restrictions causing rocketing demand for home deliveries.

The market took the results well and shares rose over 2% on Wednesday morning. However, Marks and Spencer shares are down 63% over the last year, seeing them lose their position in the FTSE 100.

£1bn Action plan

Marks and Spencer outlined £1bn worth of measures to help bolster the cash position which included £500m in cost reductions. The group, which closed 54 legacy stores in 2019/20, had previously announced it was scrapping its final dividend to improve the balance sheet. “Last year’s results reflect a year of substantial progress and change including the transformative investment in Ocado Retail, outperformance in Food and some green shoots in Clothing in the second half,” said Steve Rowe, Marks & Spencer CEO. “However, they now seem like ancient history as the trauma of the Covid crisis has galvanised our colleagues to secure the future of the business. The way our people have rallied to support our customers and communities has been awe-inspiring.” “From the outset we recognised that we were facing a crisis whose effects and aftershocks will endure for the coming year and beyond: Whilst some customer habits will return to normal others have changed forever, the trend towards digital has been accelerated, and changes to the shape of the high street brought forward. Most importantly working habits have been transformed and we have discovered we can work in a faster, leaner, more effective way. I am determined to act now to capture this and deliver a renewed, more agile business in a world that will never be the same again.”Severn Trent increases dividend

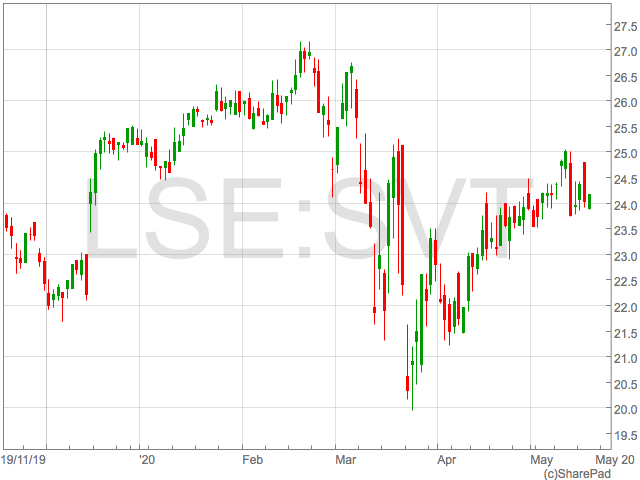

Liv Garfield continued to thank the Severn Trent team; “I want to say thank you to all of my awesome colleagues; it has been a challenging time, and across each and every part of the business, they have shown amazing commitment to ensuring our customers have continued access to one of life’s essentials. We know that this is a difficult time for our customers, and I am incredibly proud of the ways in which the business has responded. We also understand that for many people this will be a difficult time financially, and we have stepped up our support for those on our Priority Services Register and customers that need extra help with their bills.”

“Our business remains strong and we have made further progress against the things that really matter to our customers with leakage, supply interruptions and water quality complaints all improving. We have invested £3 billion in our long- term future over the past five years and are now very focused on emerging from this crisis in the best possible shape to deliver against the exciting plans we have set out for the next five years.”

Liv Garfield continued to thank the Severn Trent team; “I want to say thank you to all of my awesome colleagues; it has been a challenging time, and across each and every part of the business, they have shown amazing commitment to ensuring our customers have continued access to one of life’s essentials. We know that this is a difficult time for our customers, and I am incredibly proud of the ways in which the business has responded. We also understand that for many people this will be a difficult time financially, and we have stepped up our support for those on our Priority Services Register and customers that need extra help with their bills.”

“Our business remains strong and we have made further progress against the things that really matter to our customers with leakage, supply interruptions and water quality complaints all improving. We have invested £3 billion in our long- term future over the past five years and are now very focused on emerging from this crisis in the best possible shape to deliver against the exciting plans we have set out for the next five years.” Adamas at a discount

NAV

In 2019, NAV declined from 88p a share to 72p a share. There were some shares issued in the period to Infinity Capital Group as part of the purchase of a stake in another business and combined with the 2019 loss is the reason behind the fall in NAV per share. There was also a share buy back at a discount to NAV, though. Chinese dolomite quarry company Future Metal Holdings accounts for more than two-fifths of NAV. Production has recommenced at the mine and it should build up over the rest of this year. Cash should be generated and some of this could be distributed to Adamas.Cash

There was $4.1m in the bank at the end of 2019. There are investment opportunities but there is limited cash to invest. Many of the recent investments are in the form of a convertible, which provides an income for the company and helps to cover costs. There was a net loss of $2.8m last year, although that includes a $1.9m management incentive that was not paid at the year end. Also, 50% of that payment will be in shares. The incentive fee is based on NAV rather than NAV per share. Adamas has raised cash through a corporate bond issue. There was $1.9m raised last year and a further $1.7m raised in recent weeks, which adds to the cash pile. Up to $10m can be raised via this bond. The bond matures in October 2022 and there is an annual interest charge of 12.5%. Since the end of 2019, 1.26 million shares have been sold at 16.1p a share thereby raising £203,500. Longer-term, as income covers the cost base there is potential for a dividend.Portfolio

Future Metal is valued at $44.7m while the convertible bond investment in Hong Kong catering group Fook Lam Moon is valued at $27.5m. These make up the majority of the portfolio in terms of value. Newer investments include DocDoc, a Singapore-based AI technology focused clinical information provider. This investment is worth $2.2m but there is significant potential upside. Management says that there are plenty of investment opportunities. Many smaller companies in Asia find it difficult to obtain investment. Due diligence is important, and any additional investment will be carefully chosen. Many of the opportunities are technology companies, but there are also potential investments in other sectors.Discount

At 27.5p, the shares are trading at a 61% discount to NAV. That seems excessive, although there are reasons. At this stage a significant discount is warranted due to the lack of liquidity of the investments and the Adamas shares as well. There is a 55% majority shareholder and Infinity Capital Group owns 15.4%. Trading in the shares is at low levels. This is partly due to the fact that the shares are tightly held, but also due to a lack of investor interest. There will dilution from the issue of incentive fee shares, plus any loss, if there is one this year. There are positives, though. Future Metal already has a substantial valuation, but once the mine is fully up and running and generating cash it could provide an uplift in the valuation and thereby the Adamas NAV. It will also provide income to limit or prevent a group loss. DocDoc also provides upside, although it may not show through this year. There could always be disappointments to offset any positive moves in valuations, though. Adamas has an experienced management team and the potential for new investments is attractive. A three-fifths discount to NAV appears too high. A lower discount would probably be fairer at this stage in the group’s development. However, there is the worry that poor liquidity could mean that any buying interest might trigger a sharp rise in the share price before any purchase can be made.FTSE 100 turns red on poor economic data

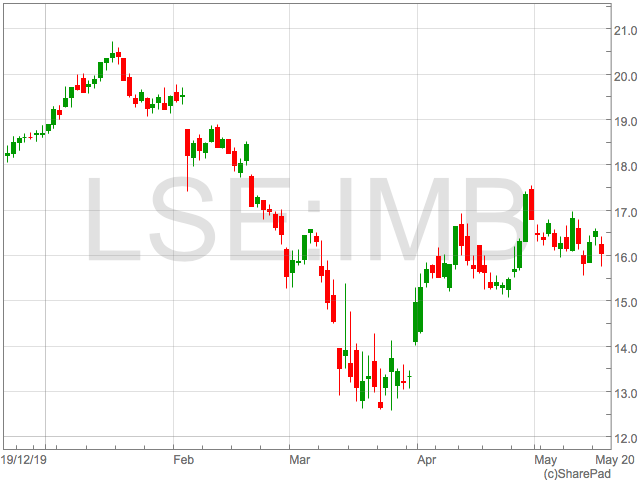

Imperial Brands slashes dividends to conserve cash

However, overall revenue was down just 0.9% as their traditional tobacco products gained market share.

“While we delivered against our revised expectations, we are disappointed with these results, and we remain fully focused on all opportunities to strengthen performance,” Dominic Brisby and Joerg Biebernick, Joint Interim Chief Executives of Imperial Brands in a statement.

They continued to to explained the current state of demand for their product mix:

“Our enhanced focus on tobacco has driven stronger in-market execution and an improved share performance, with gains in most of our priority markets. We have reduced our NGP spend following the poor returns on investment last year and this, together with recent weaknesses in the vapour category, has resulted in lower NGP revenue.”

“Overall, COVID-19 has so far had only a small impact on trading but we expect this to be more pronounced in the second half due to continued pressures on our duty free and travel retail business, changes in consumption patterns including downtrading and a reversal of some first half inventory build.”

“Agreeing the sale of our premium cigar business for €1.2 billion in the current climate was a major achievement and will further simplify the business and reduce debt. Deleveraging remains a key priority, such that the Board has decided to rebase the dividend by one-third to accelerate debt repayment, while retaining a progressive dividend policy, growing annually from the rebased level. This will strengthen the balance sheet and support a more flexible approach to capital allocation in the future.”

However, overall revenue was down just 0.9% as their traditional tobacco products gained market share.

“While we delivered against our revised expectations, we are disappointed with these results, and we remain fully focused on all opportunities to strengthen performance,” Dominic Brisby and Joerg Biebernick, Joint Interim Chief Executives of Imperial Brands in a statement.

They continued to to explained the current state of demand for their product mix:

“Our enhanced focus on tobacco has driven stronger in-market execution and an improved share performance, with gains in most of our priority markets. We have reduced our NGP spend following the poor returns on investment last year and this, together with recent weaknesses in the vapour category, has resulted in lower NGP revenue.”

“Overall, COVID-19 has so far had only a small impact on trading but we expect this to be more pronounced in the second half due to continued pressures on our duty free and travel retail business, changes in consumption patterns including downtrading and a reversal of some first half inventory build.”

“Agreeing the sale of our premium cigar business for €1.2 billion in the current climate was a major achievement and will further simplify the business and reduce debt. Deleveraging remains a key priority, such that the Board has decided to rebase the dividend by one-third to accelerate debt repayment, while retaining a progressive dividend policy, growing annually from the rebased level. This will strengthen the balance sheet and support a more flexible approach to capital allocation in the future.” FTSE 100 soars on vaccine hopes