Rolls-Royce shares have recorded astronomical gains since their post-pandemic lows, providing investors who dared to buy the stock in the midst of the coronavirus market crash with once-in-a-lifetime returns.

The airline industry’s recovery from the pandemic and Rolls-Royce’s delivery on an ambitious growth strategy have powered shares higher, taking Rolls-Royce shares to lofty valuations that some may argue demand additional growth from the company to justify the current multiples.

Notwithstanding the growth prospects of their core aerospace, defence and power segments, investors will be looking towards Rolls-Royce’s ‘New Markets’ division, which includes the firm’s nuclear Small Modular Reactors (SMR), for a potential source of future growth.

Rolls-Royce is positioning itself at the forefront of a nuclear renaissance, with its Small Modular Reactor (SMR) technology representing what could become the company’s most significant long-term growth driver.

As governments worldwide pledge to triple nuclear capacity by 2050, the British engineering giant’s SMR programme offers the potential for growth that could substantially enhance Rolls-Royce shareholder returns over the coming decades.

The Nuclear Opportunity: A £54 Billion Prize

The numbers surrounding Rolls-Royce’s SMR venture are nothing short of extraordinary. Each SMR power station will generate 470 megawatts of low-carbon energy—equivalent to more than 150 onshore wind turbines—providing stable, affordable, and emission-free power to one million homes for at least 60 years.

This represents more capacity and longevity than any other SMR currently in development.

The economic potential is equally impressive. A fleet of Rolls-Royce SMRs could contribute up to £54 billion to the UK economy between 2025 and 2105, according to the company.

With global demand for nuclear power surging as countries including the United States, Canada, France, Japan, and Sweden commit to ambitious nuclear expansion plans, Rolls-Royce appears uniquely positioned to capture a significant share of this growing market.

First-Mover Advantage: Racing Ahead of Competition

Rolls-Royce SMR has established a commanding lead in the regulatory approval process, sitting up to eighteen months ahead of competitors in European regulatory frameworks. This first-mover advantage became even more pronounced when the company achieved a significant milestone by completing step two of the Generic Design Assessment (GDA) regulatory process in the UK and progressing to the third and final step on 30 July 2024. Crucially, Rolls-Royce is the only company to have reached this milestone, further cementing its competitive advantage.

The company’s nuclear credentials are built upon more than half a century of engineering heritage, developed by a team with an unrivalled track record in nuclear design, regulatory engagement, manufacturing, and assembly. This deep expertise, combined with the regulatory head start, positions Rolls-Royce SMR as the UK’s premier green export technology and a potential world leader in SMR deployment.

Recent New Markets Division Activity

Rolls-Royce has been particularly active in securing strategic partnerships and advancing commercial opportunities. A standout achievement came in September when Rolls-Royce SMR was named as the preferred supplier for SMR construction by the Government of the Czech Republic and the Czech State utility, ČEZ Group. This landmark agreement includes a strategic investment by ČEZ into Rolls-Royce SMR and an exclusive commitment to deploy up to 3GW of electricity capacity in the Czech Republic.

The division’s momentum continues with its shortlisting by Vattenfall as one of two companies potentially selected to deploy a fleet of SMRs in Sweden. This programme forms part of Vattenfall’s strategy to meet rising electricity demand whilst helping Sweden achieve its goal of creating a fossil-free economy by 2045. Additionally, Rolls-Royce SMR is engaged in various selection processes with multiple international counterparts, indicating strong global interest in the technology.

With first power still planned for the early 2030s, contingent upon securing orders from the UK Government’s SMR procurement process, the company is well-positioned to capitalise on the growing nuclear market.

Although SMR’s are still in their early stages, recent activity demonstrates demand for Rolls-Royce products that is likely to pick up in the coming years.

SMR Investment

The development of cutting-edge nuclear technology requires substantial investment. The Rolls-Royce New Markets division reported an underlying operating loss of £177 million in the most recent period, compared to £160 million in the prior year. This £17 million increase reflects planned expenditure to meet crucial development milestones in the SMR programme.

Trading cash flow presented a more significant outflow of £181 million compared to £63 million in the previous year, representing a £118 million increase in cash investment. Whilst these figures may appear concerning to some investors, they should be viewed in the context of the substantial long-term opportunity and the critical importance of maintaining the company’s competitive advantage in this emerging market.

The question investors will have to answer for themselves is whether the anticipation of future contribution to the bottom line from SMRs is enough to support shares and drive them higher as the rollout gathers pace.

Of course, Rolls-Royce isn’t reliant on its nuclear ambitions for growth. Civil Aerospace revenue grew 24% over last year, while Power Systems operating profit surged 40% to account for 20% of group profits. Rolls-Royce has multiple sources of growth, but there is a feeling that the group’s PE Ratio of 33 requires a sharp uptick in profit before long.

Like all FTSE 100 housebuilders, Barratt Redrow had a tough year in 2025. The housing market staggered along, hampered by higher interest rates and economic uncertainty, while investors and housebuilders themselves waited for the Labour government to act on their pledge to boost the housing market.

Barratt investors are still waiting. The housebuilder completed 16,565 homes during the year, down 7.8% from Barratt and Redrow’s combined total of 17,972 in the previous year.

Despite the drop in completions, there are reasons to be optimistic. Net private reservations per active sales outlet climbed to 0.64 per week – a notable improvement from the aggregated performance of 0.55 for both Barratt and Redrow in FY24.

However, the London market proved particularly challenging. Lower than expected completions from international customers and private rental sector investors affected Q4 performance, pushing total completions slightly below the company’s guided range.

The group announced a share buyback, but it wasn’t enough to offset the disappointment around slow completions. Shares were down 8% at the time of writing.

“Barratt’s £100m buyback will please shareholders, but it does little to mask the challenges facing Britain’s biggest housebuilder,” said Mark Crouch, market analyst for eToro.

“As completions for the year missed guidance, management pointed to softer investor and international demand in London, another sign that the capital’s housing market is faltering. The merger with Redrow was pitched as a sector-defining move, yet the market response has been largely indifferent. Strategic logic around scale and land pipeline depth is sound, but synergy alone isn’t enough to lift sentiment.”

Forward sales improvement

Investors will be pleased to see the forward sales position improving during FY25. Total forward sales reached £2.92bn at year-end, representing 9,835 homes. This compared well to the aggregated position of £2.64bn for 9,426 homes in the previous year.

Contractually exchanged homes comprised 67% of the order book, providing visibility for future deliveries. The total average selling price increased to approximately £344,000, with private sales averaging £380,000.

The Redrow acquisition is yielding tangible benefits ahead of schedule. Barratt Redrow has confirmed £69m of cost synergies against its target of at least £100m. Approximately £15m of these synergies contributed to FY25 profits, with a further £45m expected in FY26. The group is well placed for the eventual pick-up in the UK housing market.

Outlook

The slowdown in activity during 2025 was well telegraphed. There were few surprises in today’s numbers, and investors will look to the future for reasons to be optimistic.

For FY26, the company anticipates total home completions between 17,200 and 17,800, including approximately 600 from joint ventures. This would represent a welcome increase on 2025’s completions, but would still lag the combined total of completions in 2024.

“Although demand during the year has been impacted by consumer caution and mortgage rates not falling as quickly as hoped, there remains a long-term structural under-supply of housing in this country,” said David Thomas, Chief Executive of Barratt Redrow.

“Our increased scale, three market-leading brands and strong land pipeline put us in a unique position to rapidly accelerate volume delivery as consumer confidence strengthens and the benefits of planning reform materialise at a local level. We remain confident in our medium-term ambition to deliver 22,000 high-quality homes a year, and in the long-term demand for our high-quality homes.”

Helix Exploration PLC has officially kicked off construction at its flagship Rudyard Project in Montana, marking a significant milestone in the company’s journey toward helium production.

The helium exploration and development company, which operates within the ‘Montana Helium Fairway’, announced that civil works began in early July 2025.

Ground clearance and compaction activities are currently underway to prepare for a reinforced concrete pad installation.

PSA plant and membrane modules from Texas are on track for delivery to Montana in August 2025, with compressor units expected to follow shortly after. The company said everything they need to begin production will soon be on site.

“We are now fully underway with construction at the Rudyard Plant site, another important step toward being the first helium producer in the State of Montana,” said Bo Sears, CEO of Helix Exploration.

“With four production wells already drilled, a fifth in progress, and equipment mobilisation underway, Helix remains focused on delivering one of the most cost-effective and rapid developments in the North American helium sector.”

After a series of updates throughout 2025, Helix is nearing its first helium production, just over a year since it listed in London.

The firm listed off a checklist of ‘things to do’ before commencing production, including compressor installation completion, plant hookup, and successful regulatory inspection. Investors will be looking forward to further updates in due course.

Helix shares have rallied more than 100% over the past two months as investors gear up for production in Montana.

Pennant International (LON: PEN) has announced a partnership with Siemens for the distribution of the GenS module of the Auxilium software suite. This help to reassure potential clients of the quality of the software and provides a route to new customers. There are also distribution agreement in South Korea and Japan. These are non-exclusive agreements. The share price increased 13.5% to 29.5p.

Orosur Mining Inc (LON: OMI) is starting mineral resource estimate drilling at the Pepas prospect within the Anza gold project area in Colombia. This area may offer near term production opportunities. The share price rose 11.8% to 8.55p.

Ariana Resources (LON: AAU) expects the Tavsan mine to reach operational status by late July. There is a year of full ore production stockpiled. The share price moved up 10.2% to 1.625p.

Eco Animal Health (LON: EAH) reported a drop in full year revenue from £89.4m to £79.6m, but non-core disposals helped pre-tax profit improve by one-third to £4m. Net cash was £25m at the end of March 2025. North America was the only region where sales increased. The share price is 9.65% higher at 62.5p.

Eco Buildings Group (LON: ECOB) has secured an offer of litigation funding for the €195m arbitration proceedings by subsidiary Fox Marble against the Republic of Kosovo. Atticus Litigation Financing is a new fund launching in August. The share price recovered 8.82% to 3.7p.

FALLERS

Alba Mineral Resources (LON: ALBA) is acquiring a majority stake in Motzfeldt critical metals project in south Greenland. Motzfeldt is a niobium tantalum zirconium rare earth project, and it has very large deposit status. The inferred resource is 340Mt, containing 41,000t of tantalum, 629,000t of niobium, 1.56Mt of zirconium and 884,000t of total rare earth oxides. The 51% stake will cost £30,000 in cash and £945,000 of shares at 0.02414p each. A placing has raised £550,000 at 0.017p/share. The share price deceased 11.4% to 0.0195p.

Primorus Investments (LON: PRIM) has been accused of beaching the lock-in agreement by selling shares in Pri0r1ty Intelligence (LON: PR1). The lock-in period lasts until 30 December 2025. In June, Primorus Investments sold its 8.05% stake raising £977,000. The Primorus Investments share price declined 7.23% to 3.85p. The Pri0r1ty Intelligence share price improved 5.56% to 4.75p.

Vast Resources (LON: VAST) is still working on cleaning and sorting the recently received package of diamonds to get them ready for tendering. The share price dipped 7.04% to 0.33p.

Investment company Tern (LON: TERN) has launched an underwritten one-for-nine open offer to raise £642,000 at 1p/share. The closing date is 28 July. This will cover overheads and the costs of being on AIM. The share price slipped 4.98% to 1.05p.

The FTSE 100 was the only major European equity index to rise on Monday amid a heavy sell-off following Trump’s targeting of the EU with 30% tariffs.

London’s index was 0.2% higher at the time of writing, while the German DAX slid 0.8% and the French CAC lost 0.6%.

Although most European equity indices were trading negatively on Monday, the losses were minor compared to the fallout after Trump’s initial tariff announcements. Many European equity indices are also trading very close to record highs and were due a bout of profit taking.

“A fresh tariff war of words erupted over the weekend and it’s blown a cloud of pessimism over European markets but London’s FTSE 100 remains resilient,” said Susannah Streeter, head of money and markets, Hargreaves Lansdown.

“Investors are lurching from hopes that Trump’s threats are just a big negotiating tactic, to fears that his impatience will turn more vengeful and big hikes will come into force in August. He has vowed to slap 30% tariffs on the EU and it’s sending a wave of apprehension through the DAX and the CAC 40.”

Streeter continued to explain that volatility could pick up if there is any weight to reports of a coalition of tariff-hit economies to hit back at the US.

“There is speculation that a coalition of defiance could be forming, with nations facing the most onerous tariffs threats, ganging up against the US, which could intensify the trade turmoil.”

London’s weighting towards defensive sectors and miners helped the index outperform on Monday. The UK’s seemingly ‘safe’ trade deal with the US will also play a part in investor thinking.

“Unlike their counterparts across the Channel, British companies should be able to operate with greater certainty around trade, and exports may be diverted through the UK. This might act as a push for foreign companies to invest in manufacturing and logistics facilities in the UK,” said AJ Bell investment analyst Dan Coatsworth.

Most FTSE 100 shares were down at the time of writing, with 60 of the 100 constituents trading in the red at the time of writing.

However, the FTSE 100’s mining sector came to the rescue on Monday and helped offset losses elsewhere in the index. Precious metals miner Fresnillo rose nearly 3% and was the top riser. Antofagasta, Glencore, and Rio Tinto were also higher.

A 2% gain for AstraZeneca added a significant number of points to the index and played a part in London’s rally. AstraZeneca is London’s largest company by market cap.

WPP was again among the losers as investors continued to dump the stock after a profit warning last week.

Introduction – has the market stopped caring about value?

The very essence of value investing is the search for securities which are incorrectly priced – where the market price is trading at a substantial discount to the intrinsic value of the underlying business. Sometimes this happens because investors are prone to behavioural biases such as extrapolation, herding and risk aversion, which can lead them to make emotional decisions, such as selling a cyclical stock at the low point of the economic cycle, unable to see how things will ever improve.

Mispricing can also occur when investors are forced – or choose – to invest in a ‘valuation agnostic’ way, without incorporating any fundamental analysis into their decision-making process. For example, UK pension funds have reduced their exposure to UK equities from above 50% in 2000 to around 3% today1, despite the UK equity market appearing to be one of the lowest valued in the world. This shift was largely driven by regulation, so the low valuation of UK equities was completely irrelevant (as was the low yield and high valuation of the fixed income securities they were buying).

For investors like us, who use valuation as a cornerstone of their process, this behaviour is welcome. When investors buy or sell indiscriminately, they push share prices further away from intrinsic value, creating opportunities to purchase significantly undervalued securities.

In this article, we explore how the rise in valuation-agnostic investing is influencing the opportunity set for those investors like us, who remain focused on fundamentals. We consider how the growth of passive investing, fast-trading hedge funds and retail speculation have increased the number of stocks trading far from their long-term value.

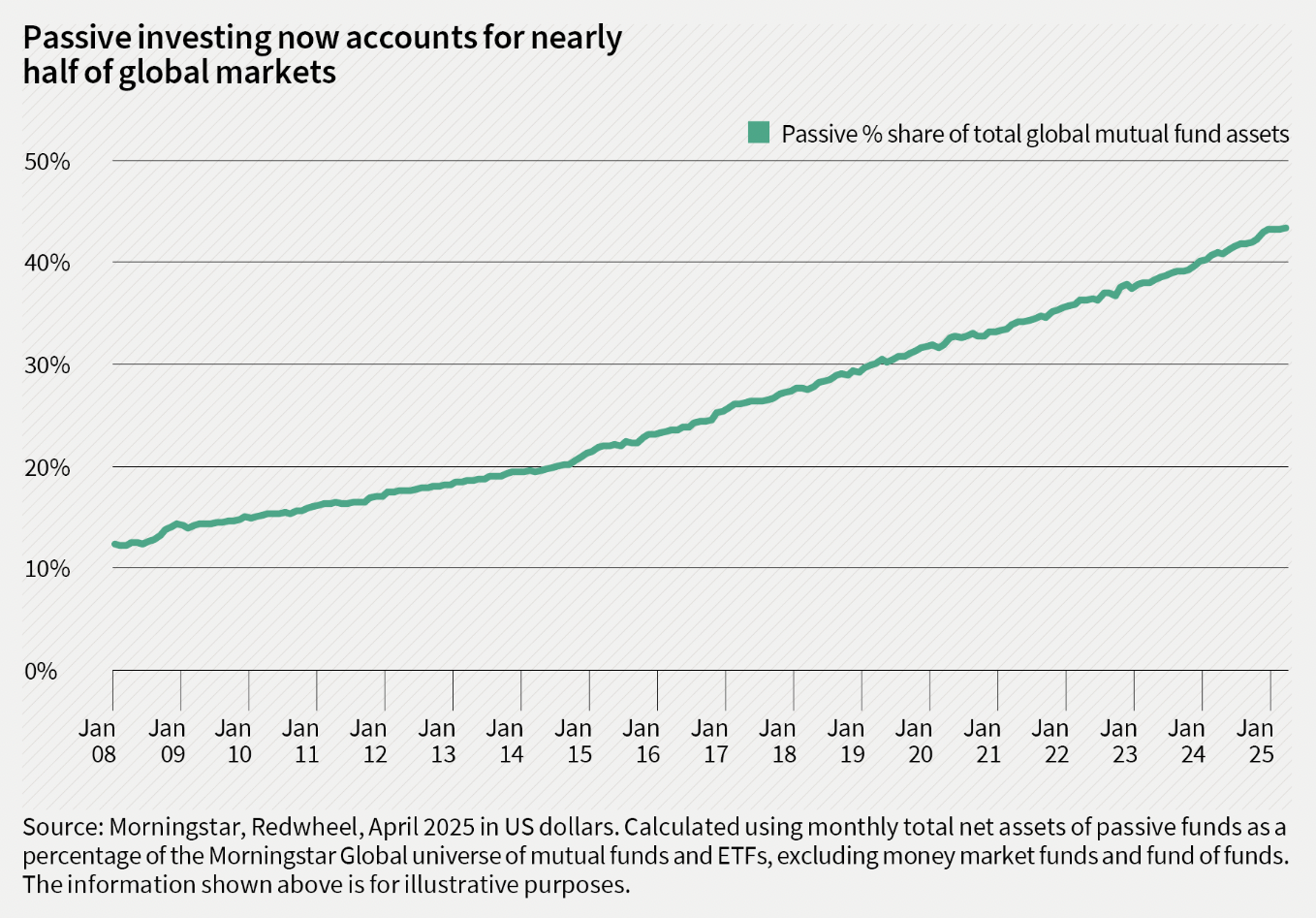

The rise of passive investing

Passive investing has grown very significantly over the last twenty years and now accounts for almost half of all equity invested in mutual funds and exchange-traded funds (ETFs) globally2. Some of the largest index-tracking vehicles are now very big indeed, with the SPDR S&P 500 ETF Trust, iShares Core S&P 500 ETF and Vanguard 500 Index Fund each holding more than $500 billion in assets3.

As the share of market participants who care about fundamentals shrinks and is replaced by those who are indifferent to valuation, it must inevitably lead to mispricing. Mike Green of Simplify Asset Management sums it up as follows:

“Passive is really just the world’s simplest algorithm. Investors who analyse a company’s prospects and attempt to value businesses have been replaced by machines that are simply saying, ‘Did you give me cash? If so, then buy. Did you ask for cash? If so, then sell’.”4

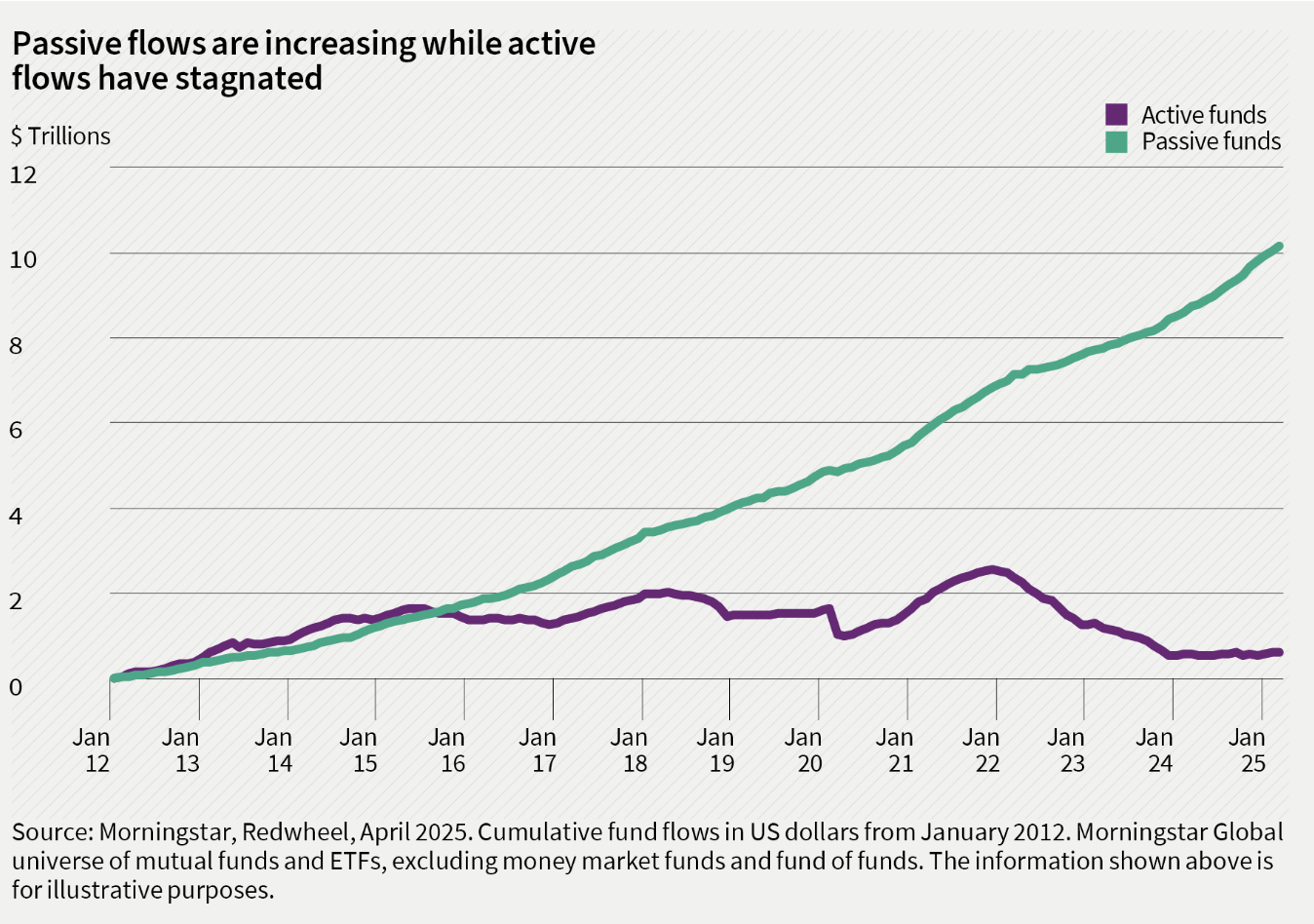

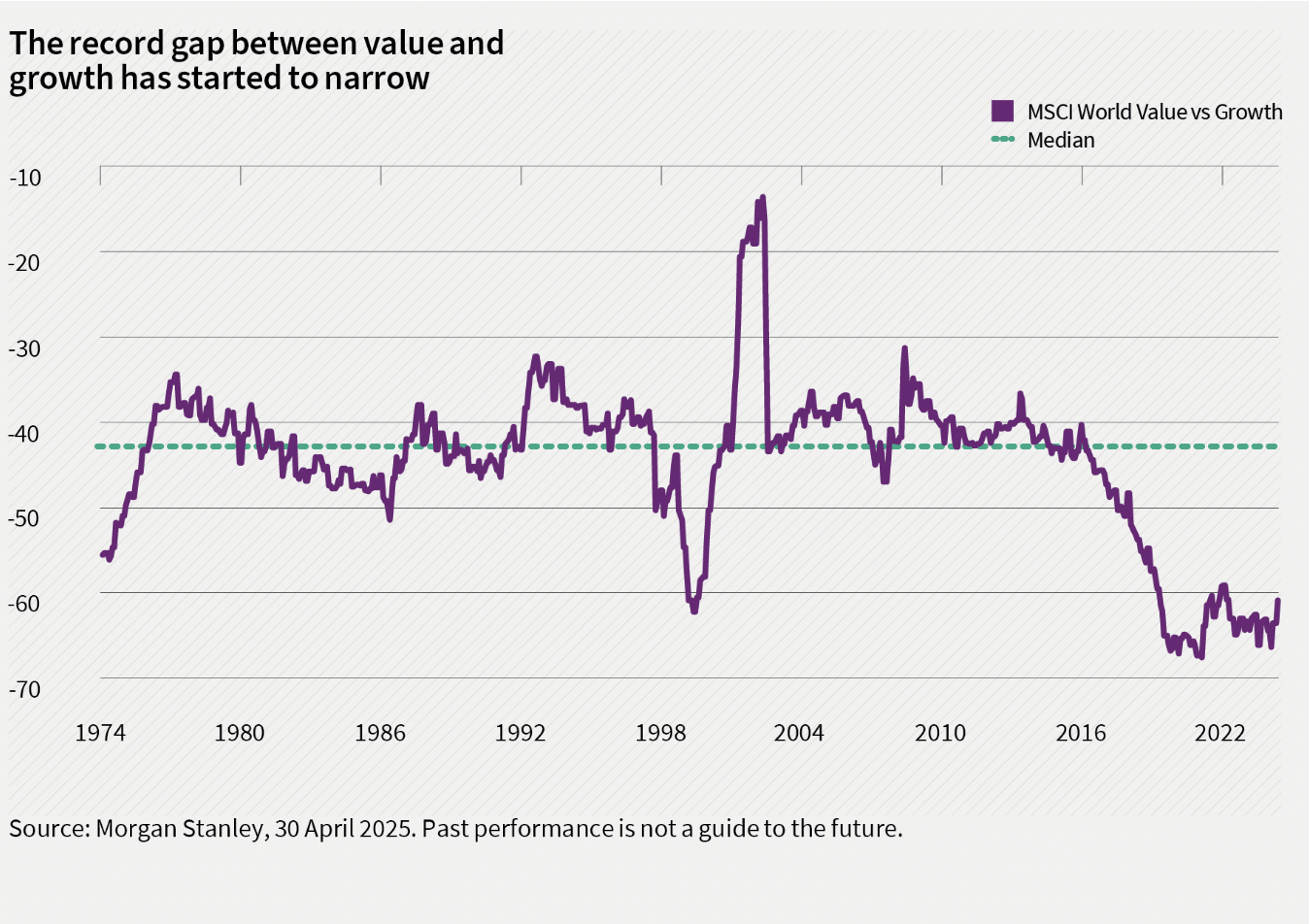

When those with no interest in valuation crowd out investors focused on what a stock is worth, the market’s price discovery mechanism begins to break down. The extent to which this is happening is visible in the chart below, highlighting the huge disparity in funds flowing into passive strategies compared to active strategies. Active managers, particularly those with a value-driven approach, are typically underweight expensive mega caps and overweight smaller, cheaper stocks5. As assets move from active to passive, these undervalued stocks are sold and the proceeds are increasingly allocated to larger more expensive stocks.

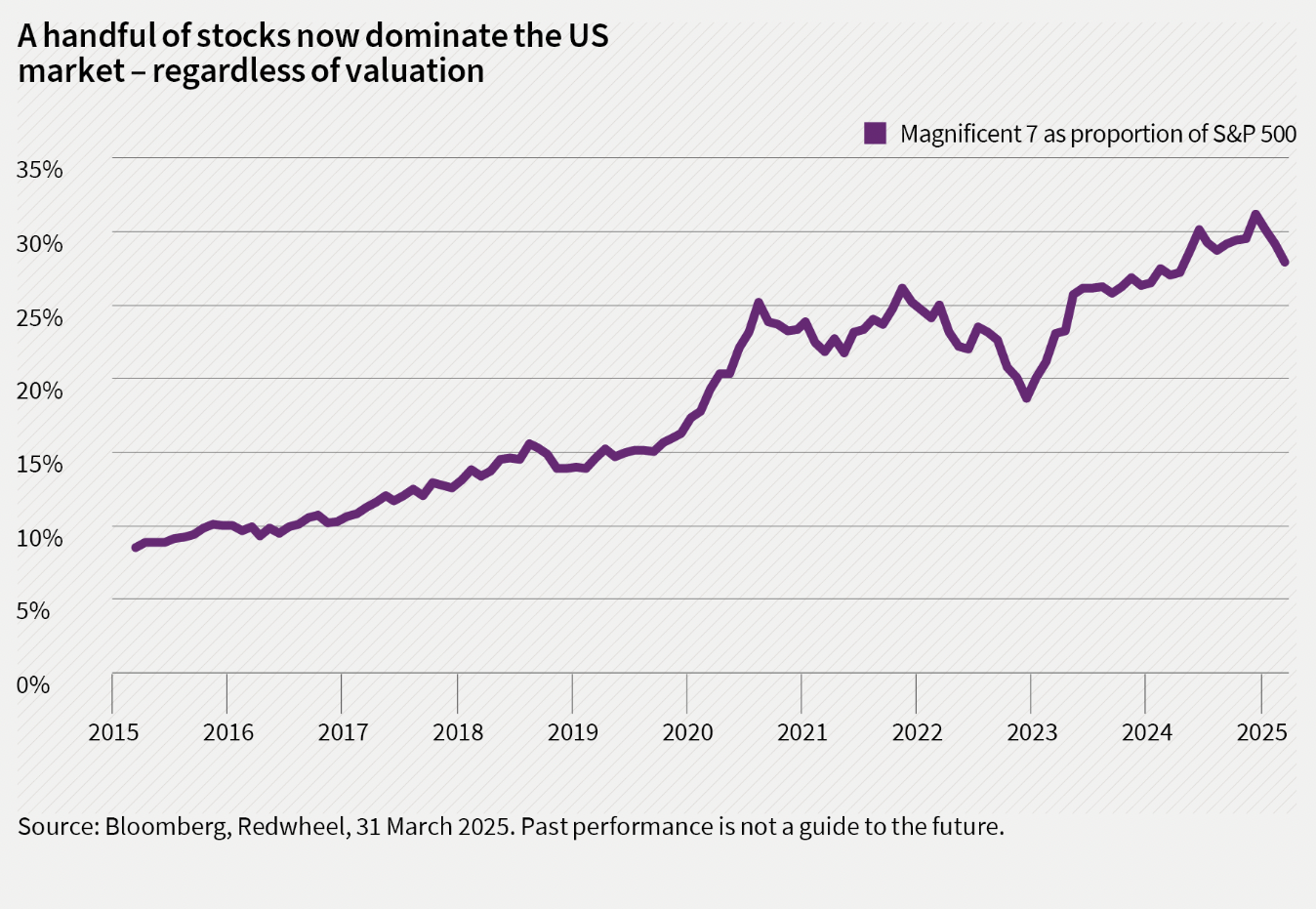

Passive has, in essence, become a giant momentum strategy – rewarding size and valuation indifference. The result is a self-reinforcing cycle where a handful of very large companies have come to dominate the index, regardless of fundamentals.

The growing influence of pod shops

‘Pod shops’ are hedge fund platforms that allocate capital to many independent portfolio managers, or ‘pods’, each running their own strategies, often with a sector or event-driven focus. The parent fund encourages its pods to focus on relative differences between stocks – buying one stock while shorting another (betting that its share price will fall) – rather than taking big bets on where the overall market is heading. This ‘market neutrality’ means they can apply leverage across the strategies while keeping risks tightly controlled. The structure aims to deliver consistent, low volatility returns – a key draw for institutional investors.

The incentive structure within pod shops is built around short-term, risk-adjusted performance. Portfolio manager compensation is closely tied to recent results and many pod shops even penalise managers for holding positions beyond a set period – often just 30 days. This encourages rapid turnover and a focus on near-term catalysts such as earnings releases, guidance updates or analyst revisions.

The scale of pod shops is significant. The two largest firms, Citadel and Millennium, manage $65 billion and $73 billion, respectively6. Their collective headcount has tripled since 20157, and their influence extends far beyond their assets due to high turnover and gearing. Gross leverage across multi-strategy funds has risen from 4x a decade ago to 12x today8. As a result, it is estimated that pod shops now account for more than 30% of US equity trading volume9.

This concentration of capital and trading activity makes them highly influential in determining short-term share price moves. Their activity is particularly visible around earnings season, where the reaction to results has become faster and more extreme. Positive surprises can trigger sharp rallies as the pods pile in, while disappointments often spark steep falls as they race to exit or take short positions.

The effect is particularly pronounced in the most liquid, widely followed stocks where pod shop activity is most concentrated. But, more broadly, the result is a market increasingly shaped by short-term flows and rapid reaction, rather than long-term fundamentals – further contributing to the mispricing of securities.

Retail day traders

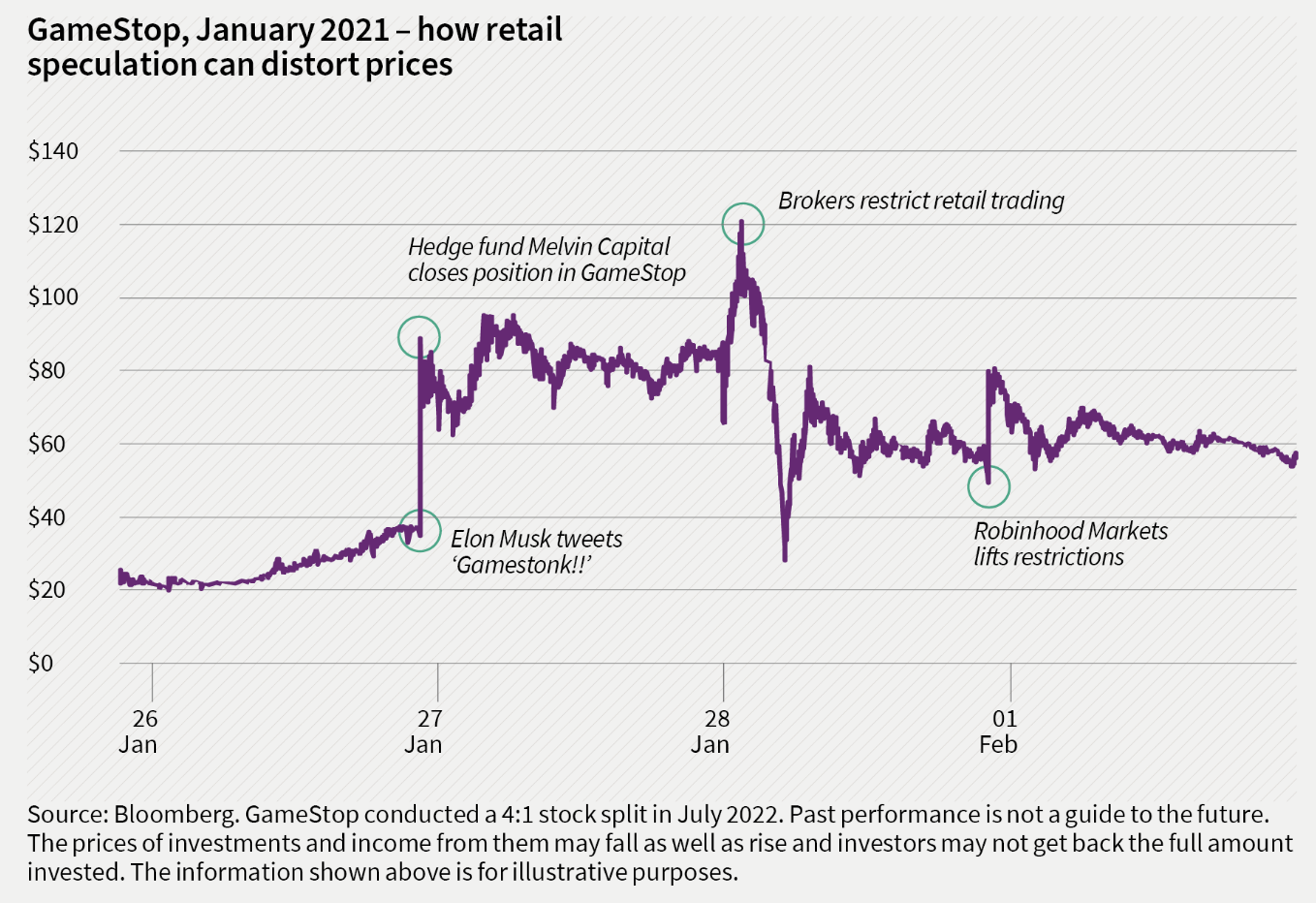

Meanwhile, the proliferation of retail day trading, fuelled by platforms like Robinhood and Reddit’s WallStreetBets community, has reshaped market behaviour in ways that extend far beyond previous cycles of rising individual investor participation.

Since 2020, retail trading volumes have grown dramatically. In 2021, retail investors accounted for 25% of total US equity trading volume, nearly double the share reported a decade prior10.

Several factors have contributed to this shift: easier access via commission-free apps, heightened market volatility during the pandemic, the influence of social media and government stimulus cheques that gave many individuals the means – and the motivation – to speculate.

The impact has, at times, been extraordinary, as best illustrated by the trading in GameStop in January 2021, which saw the stock swing wildly within hours – rising 82%, falling 77%, then jumping 150% – as coordinated retail buying overwhelmed institutional players.

How this creates opportunity

We believe the growth of passive investment strategies has driven the valuations of the largest stocks in the most popular markets – those receiving a disproportionate share of passive flows – significantly above their intrinsic value. Conversely, they are driving the valuations of many other stocks being sold down by active managers significantly below their intrinsic value.

The momentum-driven, valuation-agnostic approach of pod shops only reinforces this, as does the activity of retail day traders. The focus of all three groups is often on the same narrow set of stocks.

For disciplined, long-term investors, this can be frustrating – but it is also the source of opportunity. When share prices are driven further below the underlying value of the business, the potential for future returns increases.

What this means for Temple Bar

Whilst it is possible to view passive flows as an unstoppable steamroller, flattening anything that tries to get in its way, we believe this is a finite process. At some level of undervaluation, entire companies are bid for by competitors or private equity firms. Others use their low valuation to create enormous value by buying back their own shares. And eventually, the upper hand returns to the surviving stock pickers, and money flows out of passive and back to active.

Perhaps that point has already been reached. The recent increase in takeovers and share buybacks suggests that, in the UK at least, we may have reached the lower limit on valuations – and others appear to be stepping in to take advantage of the value on offer.

As far as Temple Bar is concerned, our approach is rooted in long-term fundamentals and a disciplined focus on valuation. Market dislocations of any sort can help widen the opportunity set for investors like us. If we are now entering a period where valuation starts to matter more, that should prove a favourable environment for our strategy.

Conclusion: why value still matters

The growing influence of valuation-agnostic investors presents both challenges and opportunities for fundamentally driven investors. A key challenge is that, for periods of time, valuation may be ignored. Share prices can move significantly on short-term momentum or flows, while robust undervalued businesses are overlooked. This can be frustrating for disciplined, long-term investors. But it also creates opportunity. If fundamentals are being sidelined, the number and scale of pricing anomalies should increase, offering more chances to buy good businesses well below their intrinsic worth.

Although fund flows still appear to favour passive strategies, there is strong evidence that fundamentals are reasserting themselves in markets. The valuation gap between value and growth stocks, which had reached historic extremes, has started to narrow. Outside the US, value has been outperforming growth consistently. Even in the US, there have been periods this year when value has shown clear relative strength. As far as the UK stock market is concerned, the recent uptick in takeovers and share buybacks also suggests that others are beginning to take advantage of the abundant value on offer.

For Temple Bar, this environment is encouraging. We continue to focus on fundamentals and valuation – and we believe that, as the market continues to rediscover the importance of value, our approach is well placed to benefit.

Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so.

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Nothing in this document should be construed as advice and is therefore not a recommendation to buy or sell shares. Information contained in this document should not be viewed as indicative of future results. The value of investments can go down as well as up.

This article is issued by RWC Asset Management LLP (Redwheel), in its capacity as the appointed portfolio manager to the Temple Bar Investment Trust Plc. Redwheel, is authorised and regulated by the UK Financial Conduct Authority and the US Securities and Exchange Commission.

The statements and opinions expressed in this article are those of the author as of the date of publication.

Redwheel may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. Redwheel seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is directed only at professional, institutional, wholesale or qualified investors. The services provided by Redwheel are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.

The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by Redwheel; or (iv) an offer to enter into any other transaction whatsoever (each a Transaction). No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party. Redwheel bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction.

In early April last year, I featured the investment attractions of Premier Foods (LON:PFD) with its shares then trading at around 147p, noting the possibility of a bid for the group at 180p or thereabouts.

Three months later, ahead of the group holding its AGM to approve the 2024 Report & Accounts, as well as announcing its First Quarter Trading Update on the same day, the shares were up to 166p, having touched 180.20p within those intervening three months, but I then noted that its shares were underrated and could so easily break up over the 200p level.

Now, one year later and...

Bitcoin smashed through $120,000 on Monday to trade at a fresh record high as traders geared up for ‘crypto week’ in the US amid inflows into Bitcoin ETF.

Congress will debate the future of cryptocurrency and its integration into mainstream finance this week. The GENIUS act could see the formation of a framework for pegging stable coins, while the CLARITY act seeks to lay down a regulatory framework with bodies such as the SEC.

The debates in Congress take place against a backdrop of heavy support for crypto from the US President, whose family have profited in a big way from various coins since he won his second term.

“Bitcoin extended its advance on Monday, breaking above the USD 122,500 mark as optimism surrounding regulatory developments in Washington and sustained institutional inflows continued to underpin sentiment,” said Kudotrade’s Konstantinos Chrysikos.

“The move coincides with the start of “Crypto Week” in the U.S. House of Representatives, where lawmakers are set to debate a trio of bills, the GENIUS Act, CLARITY Act, and Anti-CBDC Surveillance State Act seen by market participants as a foundational step toward comprehensive digital asset regulation.”

Konstantinos continued to outline key purchases of Bitcoin that were supported by prices, including inflows into US Bitcoin ETFs.

“Investor appetite has also been amplified by fresh corporate interest. Tokyo-listed Metaplanet Inc. disclosed the purchase of 797 Bitcoin, lifting its reserves to over 16,000 and indicating a continued shift toward corporate treasury adoption of digital assets. Meanwhile, spot Bitcoin ETFs in the U.S. have registered important inflows, exceeding USD 1 billion two days in a row. However, the surge in price could expose the market to price corrections if traders move to take profits. Otherwise, a continued bullish sentiment could drive the asset to new highs.”

Georgina Energy’s subsidiary Westmarket Oil & Gas has received preliminary approval for its Well Management Plan at the Hussar site from Western Australia’s Department of Mines, Petroleum and Exploration.

However, the London-listed company cannot begin site preparation or drilling until it secures final approval for expanded environmental management plans under state regulations.

The environmental hurdle represents the remaining barrier before drilling can commence at the Hussar-2 well.

Once environmental approval is granted, Georgina Energy will repair the Hussar airstrip and access roads, construct drilling and camp facilities, and install water wells ahead of operations.

“Georgina’s operations team has worked on all the required obligations for the Hussar drilling permit approval in cooperation with the indigenous community representatives,” said Anthony Hamilton, Chief Executive Officer of Georgina Energy. “We await approval for our extended environmental plan, and look forward to receiving the final drilling approval once all obligations and approvals have been obtained.”

Georgina Energy shares were flat at the time of writing.

The company completed a reverse takeover in 2024, raising £5m at 12.5p during the height of London’s helium hysteria. Georgina Energy shares are down 50% to 6.6p since the reverse takeover was completed.

Filtronic plc, the RF solutions designer and manufacturer, has won a £13.4m contract to supply high-performance modules for an electronic sensor system to a defence prime contractor.

Today’s deal is the latest in a string of high-value contract wins by Filtronic, which have helped push the stock to all-time highs this year.

Filtronic shares were 3% higher at the time of writing.

The contract’s delivery is scheduled to begin in mid-2026, with production taking place at Filtronic’s secure automated hybrid microelectronics facility in Sedgefield, County Durham.

“We are proud to continue strengthening our defence portfolio, which highlights the market’s ongoing confidence in our ability to execute complex programmes to the highest standards,” said Nat Edington, Chief Executive Officer.

“Aerospace and defence remains a key sector in our growth strategy, and this latest order reflects Filtronic’s proven track record of successful project delivery, collaborative partnerships, and manufacturing excellence.”