Video games publisher Frontier Developments (LON: FDEV) published a trading statement showing revenues ahead of expectations. There was 3% growth in the second half and Panmure Liberum has raised its forecast revenues from £85.9m to £90m, compared with £89m the previous year. A loss had been expected, but this is now a pre-tax profit of £3.3m, although that includes a £3.5m gain on the sale of rights to one of its games. The share price rose 7.02% to 244p.

Peptide drug conjugates developer Avacta (LON: AVCT) has appointed David Bryant and Zeus founder Richard Hughes as non-executive directors. Yesterday, Avacta reported delays in its audit and results for 2024 have delayed to 4 June. The share price recovered 8.87% to 33.75p.

Shearwater Group (LON: SWG) subsidiary Brookcourt Solutions has become one of the first UK organisations to achieve certification against ISO 42001, the pioneering international standard for Artificial Intelligence Management Systems (AIMS). The share price increased 8.05% to 47p.

Mixed signal ASICs developer EnSilca (LON: ENSI) has established a new engineering hub in Cambridge, the fourth one in the UK. Six engineers have been recruited. The share price moved up 6.15% to 34.5p.

Engineering company Avingtrans (LON: AVG) revealed in an unexpected trading statement that has led to a profit upgrade. Although forecast revenues are unchanged at £161m, the pre-tax profit estimate has been raised from £6.5m to £8.1m due to the product mix and cautious forecasting. The share price improved 5% to 420p.

FALLERS

Diagnostics company Angle (LON: AGL) increased 2024 revenues by 31% to £2.9m, although the product mix and early discounts to pharma customers meant that gross margins declined. The loss was reduced by 29% to £14.2m after cost savings. Net cash was £10.4m at the end of 2024 with £2.3m of tax credits due, of which £1.4m have been received. The cash should last until the first quarter of 2026. There is uncertainty about timing of new deals that will help to further improve revenues. The share price lost its recent gains and is 18% lower at 8p.

Mosman Oil & Gas (LON: MSMN) has sold its interest in the Billy Goat lease to Desert Eagle in return for 5% of helium revenues from future production. Mosman Oi & Gas will no longer have to pay 100% of the first well as previously. There is no commitment for any additional spending. Cash will be spent on developing nearby interests. The share price dipped 6.1% to 0.0385p.

Jubilee Metals (LON: JLP) says trials on the Roan concentrator near Idola in Zambia show recoveries on waste of 65% copper. The production target is up to 40,000 tonnes of material per month at grades of up to 1.5%. The Munkoyo open pit is being drilled to define the resource. Non-core assets have been identified, and one has been sold for $12.3m payable over 12 months. The share price declined 8.14% to 3.95p.

Medical devices supplier Inspiration Healthcare (LON: IHC) reported results for the year to January 2025 in line with expectations. Revenues were slightly higher at £38.3m, while the loss increased from £600,000 to £2.2m. A return to profit is expected this year. The share price slipped 5.13% to 18.5p.

The FTSE 100 was trading in a holding pattern on Wednesday after a strong rally in US stocks overnight as markets paused for breath and investors geared up for the release of Nvidia results after the US bell later tonight.

London’s leading index was trading flat at the time of writing after trading in a tight range for most of the session.

Nvidia’s results have become a major event in traders’ calendars due to their importance to the AI trade that has propelled US equity market higher over the past two years. A significant beat or miss of Nvidia earnings expectations has the power to drive global equity trade, and investors are becoming increasingly wary going into the release.

“The FTSE 100 ticked higher after an increase in US consumer confidence and a delay on the punishing EU tariffs announced by the Trump administration helped US stocks to surge overnight,” said AJ Bell investment director Russ Mould.

“However, with US futures pointing to some retrenchment when Wall Street resumes trading later, it’s clear there is still some latent nervousness in the market.

“Quite a lot may ride on Nvidia’s results later, with investors likely to be watching the numbers and particularly the outlook closely to see what impact, if any, tariff uncertainty is having on the business.”

In the UK, there was a nearly 50:50 split between FTSE 100 gainers and losers at the time of writing, with little in the way of major movers.

Kingfisher was the top corporate story. Shares fell 2.3% after the DIY group released Q1 results that confirmed the positive impact of favourable UK weather conditions, but poor performance in France gave investors a reason to be cautious.

“There were some rays of sunshine in the first quarter for B&Q and Screwfix owner Kingfisher, with sales rising 1.8% across the group but there’s still concern about the longer-term picture,” said Susannah Streeter, head of money and markets, Hargreaves Lansdown.

“The update indicates there was strong demand for seasonal products in the UK and Ireland, even before the May heatwave took hold. This has helped boost revenues by 5.9%, sharply higher than forecasts.”

Endeavour Mining is regularly in the FTSE 100’s top losers or gainers as traders use the stock as a risk sentiment proxy. The potenital risk presented by Nvidia’s results and the general risk-off positioning sent the gold miner to the top of the leaderboard with a 1% gain.

It’s sometimes better to travel to arrive when investing in equities, and that has proved to be the case for Kingfisher shares after a strong start to the year.

Kingfisher shares had rallied going into the release of today’s Q1 trading update after peers reported strong results amid better weather conditions in the UK. Kingfisher produced similarly strong results with UK & Ireland reported sales rising 6.1%, helping to offset a 4.9% decline in France.

“Although the deteriorating performance in France wasn’t quite as bad as expected, revenues from its operations in Poland were much weaker than forecast, with both markets showing sales decline of 3.2%,” explained Susannah Streeter, head of money and markets, Hargreaves Lansdown

Kingfisher group Q1 sales came in at £3.3 billion, rising 2.2% at constant currency, despite a negative 0.9% calendar impact. This represented underlying total sales growth of 3.1%. Like-for-like sales increased 1.8%, with underlying growth of 2.7%.

Volume and transaction growth were driven by seasonal categories, which had a positive mix impact on average selling prices. Retail price inflation remained flat during the period.

“It seems Britons’ first impulse on seeing the sun is to start doing some DIY, if Kingfisher’s results are any indication,” said Chris Beauchamp, Chief Market Analyst at IG.

“A set of poor numbers in France was offset by UK consumers spending their unexpected early summer in Kingfisher’s stores, helping to lift like-for-like sales by 1.8%. Up 16% so far this year, the shares have been a haven from tariff volatility, though the update didn’t offer much to extend the rally in the short term.”

As alluded to by Beauchamp, Kingfisher shares dropped over 2% as the group reaffirmed guidance and offered investors little to be excited about other than better weather in the UK.

If you are lucky enough to be in Abu Dhabi, in the United Arab Emirates, then perhaps this Thursday you should pop into the offices of Gulf Marine Services (LON:GMS) at the International Tower for 2.30pm (UAE time) to attend the company’s 2024 AGM.

If you do attend, then could you please listen to the proceedings intently and report your findings back to us?

I take the view that the shares of one of our UK Investor Shares for 2025 are looking very positive and offer some useful upside before the year is over.

Last night they closed up 4% at 18.80p and we see them rising a lot...

Pets at Home Group has announced its preliminary results for the financial year ending 27 March 2025, revealing a tale of two divisions as the company navigated challenging market conditions.

Shares were fairly flat on Wednesday after the pet retailer and veterinary services provider reported group consumer revenue growth of 2.7% to £1.96bn.

CEO Lyssa McGowan said the group was becoming a ‘true pet care platform’ after a period of transformation. The term ‘platform’ relates to a focus on subscriptions, which are up 30%, and recurring revenues. The strength in subscriptions and the vets business has been essential in offsetting disappointing performance in the retail stores.

The vets business delivered consumer revenue growth of 13% to record levels. This growth was driven by increased customer visits, higher average transaction values, and substantial expansion in Care Plan revenues. Statutory revenues for the veterinary division rose 16.8% to £175.3 million on a like-for-like basis of 16.2%.

In contrast, the retail division revenue declined 1.8%. The segment was impacted by subdued growth in the pet sector, reflecting a challenging UK consumer environment, deflationary pressures, and normalising levels of new pet ownership following the pandemic boom.

Retail revenues fell 1.8% to £1.31 billion, with like-for-like revenue down 2.0%.

Overall group statutory revenues increased marginally by 0.1% to £1.48 billion, with like-for-like revenue declining 0.4%. Group underlying profit before tax rose 0.7% to £133.0 million, in line with company guidance, representing a margin improvement of 5 basis points.

“A ‘tail’ of two halves for Pets at Home this morning, as the retail side of the business continues to struggle due to tightened discretionary spending caused by the increased cost of living. As such, the purchases of new collars, beds or other toys and accessories are being scaled back from the family budget,” said Adam Vettese, market analyst at eToro.

“Pets at home are putting their best paw forward with the veterinary side of the business, which is continuing to show robust growth. This has helped offset weaker retail performance and brought overall results in line with market expectations. Pre-tax profit and earnings per share rose, reflecting operational resilience despite a challenging macro environment.”

Defence Holdings shares rose on Tuesday after the recently pivoted company announced a five-year strategic plan designed to capitalise on Europe’s expanding defence priorities.

Defence Holdings’ plan will target high-growth segments within the global defence market, which is currently valued at approximately $2.2 trillion.

The company was formerly Guild Esports and has shifted focus after Guild failed to secure financing to keep operations running and disposed of its gaming assets. Guild Esports was backed by David Beckham.

Defence Holdings’ strategic framework centres on drone warfare and aggregation, AI agents for defence operations, information and influence warfare, and critical infrastructure defence. These pillars reflect Europe’s renewed emphasis on sovereign defence capability whilst maintaining full NATO interoperability.

James Norwood, incoming Chairman of Defence Holdings PLC, highlighted the timeliness of their strategic shift. “Defence Holdings’ Five-Year Strategic Plan arrives at a defining moment for the UK and European defence landscape,” he said. Norwood has an extensive military background as a Royal Navy officer and subsequent experience advancing next-generation programmes at Raytheon Technologies.

Defence Holdings has set out its shop against a backdrop of significantly increased European defence spending following geopolitical tensions and security challenges.

Defence Holdings outlined a product-studio and buy-and-build model designed to capture opportunities within software-led defence segments across the UK and continental Europe. The company explained its five-year timeframe provides Defence Holdings with ample time to scale operations whilst maintaining agility in responding to emerging security requirements across European markets.

“Our new 5-year strategic plan sets a clear path for sustainable growth and value creation,” said Brian Stockbridge, Board Member of Defence Holdings.

“By focusing on disciplined investment, innovative product development and proactive management, we are confident in our ability to deliver long-term returns for our stakeholders and position the company at the forefront of our sector. I am particularly proud of the exceptional calibre of board members we have assembled – leaders with deep expertise across defence, technology, and capital markets.”

Dr Graham Cooley has increased his stake in spirits company Distil (LON: DIS) from 18.1% to 19.15%. The share price jumped 25.9% to 0.17p. This is the highest the share price has been since last October.

Jangada Mines (LON: JAN) investee company Blencowe Resources (LON: BRES), where it owns 7%, has received further grant funding of $500,000 from the US International Development Finance Corporation with a further $1m to come. There had been a pause in funding as the new US government assessed spending. The funding does not have to be repaid. The share price was one-fifth higher at 1.2p, which is a new 2025 high.

Poolbeg Pharma (LON: POLB) has been granted orphan drug designation by the FDA in the US for POLB001 for treating cytokine release syndrome caused by T cell engager bispecific antibodies. This is a side effect of cancer treatments. POLB001 is ready for a phase 2 study. The status provides seven year exclusivity after US approval, plus tax credits for development spending. This is a $10bn market. There is potential for securing a partner for clinical trials. The share price rose 16.3% to 2.85p.

Energy supplier Chariot (LON: CHAR) has raised $6.1m at 1.4p/share and an open offer could raise a further $1m. The cash will be invested in wind generation, gas and upstream assets. Chariot plans to demerge its transitional power business in the second half of 2025. The share price improved 15.2% to 1.641p.

Energy assurance and optimisation services provider Inspired (LON: INSE) has received an indicative offer of 81p/share from HGGC managed funds. The Inspired board has indicated that it would be minded to recommend the bid if it was at this level and the acceptance condition did not rely on Regent Gas, which owns 29.4%, accepting the bid. Regent Gas Holdings is offering 68.5p/share in cash and says it wants Inspired to stay on AIM. This offer has been rejected. The share price is 9.15% higher at 77.5p.

FALLERS

Reduced frequency of services hit the ongoing business of cleaning services provider React (LON: REAT) hit ongoing interim revenues. There were also two paused contracts. In the six months to March 2025, revenues rose from £10.6m to £12.1m, but that was after a £2.8m contribution from 24hr Aquaflow Services, which was acquired in October last year. It also helped gross margin improve from 27.1% to 32%, which should be sustainable because contracts have been in cost increases from higher National Insurance rates. Admin expenses have increased ahead of growth and because of running two systems at LaddersFree while business is transferred to a new online platform. Underlying interim pre-tax profit was flat at £1.1m, excluding acquisition costs of £220,000. There are some positive signs, but management is cautious about the second half leading to a forecast downgrade. Full year pre-tax profit is expected to be flat at £2.1m, but earnings will be lower because of shares issued to finance the 24hr Aquaflow Services acquisition. The share price declined 22.2% to 56p.

Metals One (LON: MET1) has slipped 10.1% to 38.6525p even though proposed US policies will speed up nuclear reactor testing and boost US mining of uranium. Metals One has uranium projects in Colorado and Wyoming.

On Friday, DP Poland (LON: DPP) announced that auditing of its 2024 results has not been completed and the figures will not be announced until late June. The share price fell 5.26% to 9p.

ECR Minerals (LON: ECR) says initial drilling results from the Bailieston project confirm the presence of gold and antimony. Antimony was intersected in two of the first three holes. The share price dipped 4.65% to 0.205p.

The FTSE 100 surged higher on Tuesday after Donald Trump’s latest retreat in his scatter gun approach to trade policy.

In another seemingly manufactured dip buying opportunity, equities bounced back from a short, sharp selloff caused by the latest assault on global trade by Donald Trump.

Last week, a social media post outlining a 50% tariff on EU imports stopped the global equity market rally in its tracks, sending US and European equities into a one-day tailspin.

However, over the weekend, Trump eased market tensions by delaying the 50% tariffs from 1st June to 9th July. The delaying of tariffs is becoming a familiar playbook for the President, and global equity markets are becoming wise to the V-shape recoveries that have followed initial sell-offs.

Major equity indices recovered most of their losses after Donald Trump pulled back from the implementation of Liberation Day tariffs, and the latest attack on the EU has proved to be a smaller-scale repeat of the price action seen since the beginning of April.

Today’s rally has pushed the FTSE 100 within reach of its all-time highs at 8,871, with the index needing less than a 1% gain to trade at never-before-seen levels.

“A mood of cautious relief is spreading after the long weekend, amid hopes for more fruitful trade negotiations between the United States and its global partners,” said Susannah Streeter, head of money and markets, Hargreaves Lansdown.

“There are no post bank holiday blues for the London market, with the Footsie in striking distance of the record high reached in February. More positive vibes are pulsing about the outlook for the global economy, with hopes that more scores can be etched on the doors of trade talks.”

There were few losers on Tuesday, with 91 of the FTSE 100’s constituents trading higher at the time of writing.

Rolls Royce and BAE Systems were among the top risers after Donald Trump and Moscow traded verbal criticism over the weekend that hit hopes of a ceasefire in Ukraine in the short term.

Intermediate Capital Group was the FTSE 100 top riser, gaining 3.9%, as it bounced back from selling after the release of its final results last week. JD Sport was another recovery story that rose more than 2%.

The risk on feel to Tuesday’s FTSE 100 rally left safe-haven stocks out of favour. Precious metals miners Fresnillo and Endeavour Mining lost their shine and fell by over 2%. The pair are still among the best-performing FTSE 100 stocks of 2025.

It will be interesting to see what occurs within the next day for the £1.4bn-capitalised GlobalData (LON:DATA) following the recent announcement of two possible bid proposal approaches.

Especially interesting considering that the declared mission for the group is ‘to help our clients decode the future, make better decisions, and reach more customers’ – so will it help its investors to decide what they should be doing with their shares?

In accordance with the Takeover Code, ICG and KKR are each required, by not later than 5.00 pm tomorrow, 28th May, to either announce a firm intenti...

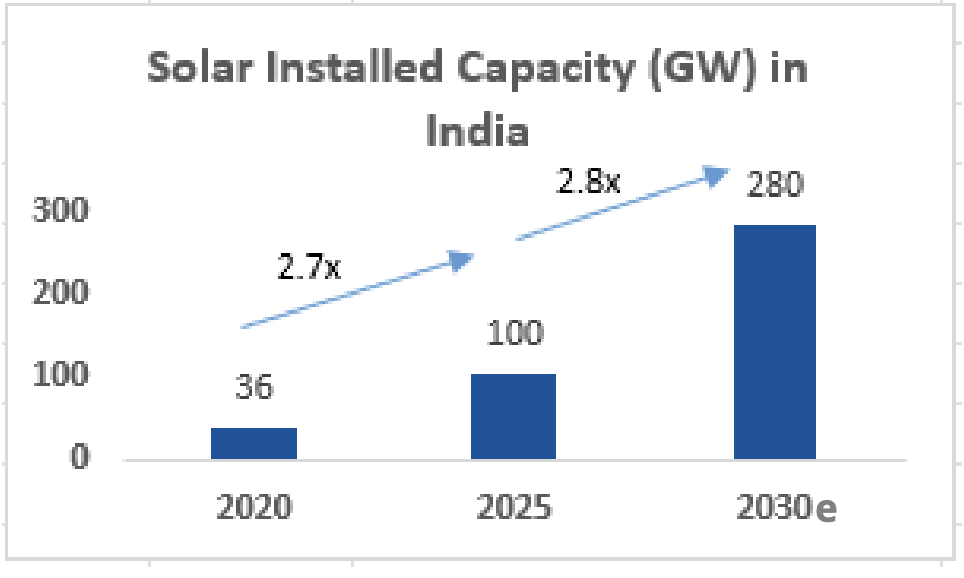

India stands at the cusp of an energy transformation. Once plagued by power shortages, the country now aims to become a global leader in renewable energy, targeting a massive 500 GW of renewable capacity by 2030, with solar energy contributing 280 GW to this ambitious goal. To give some context, UK’s renewable energy capacity stands at 60 GW in 2024. Traditionally a coal-driven energy market, this solar-first approach leverages India’s natural advantage of abundant sunshine and the continuously declining cost of solar power generation. With solar renewable energy cheaper than coalfired power, it presents a win-win positioning for India to simultaneously address climate change concerns while meeting the country’s growing demand for power.

Source: Govt of India – Press Information Bureau MNRE: Year End Review, Dec 20. MNRE: Press Release: 2100603, Feb 25. Grant Thornton Report, Achieving 500 GW of renewable energy capacity by 2030, 2024. e indicates estimate.

The Solar Value Chain in India

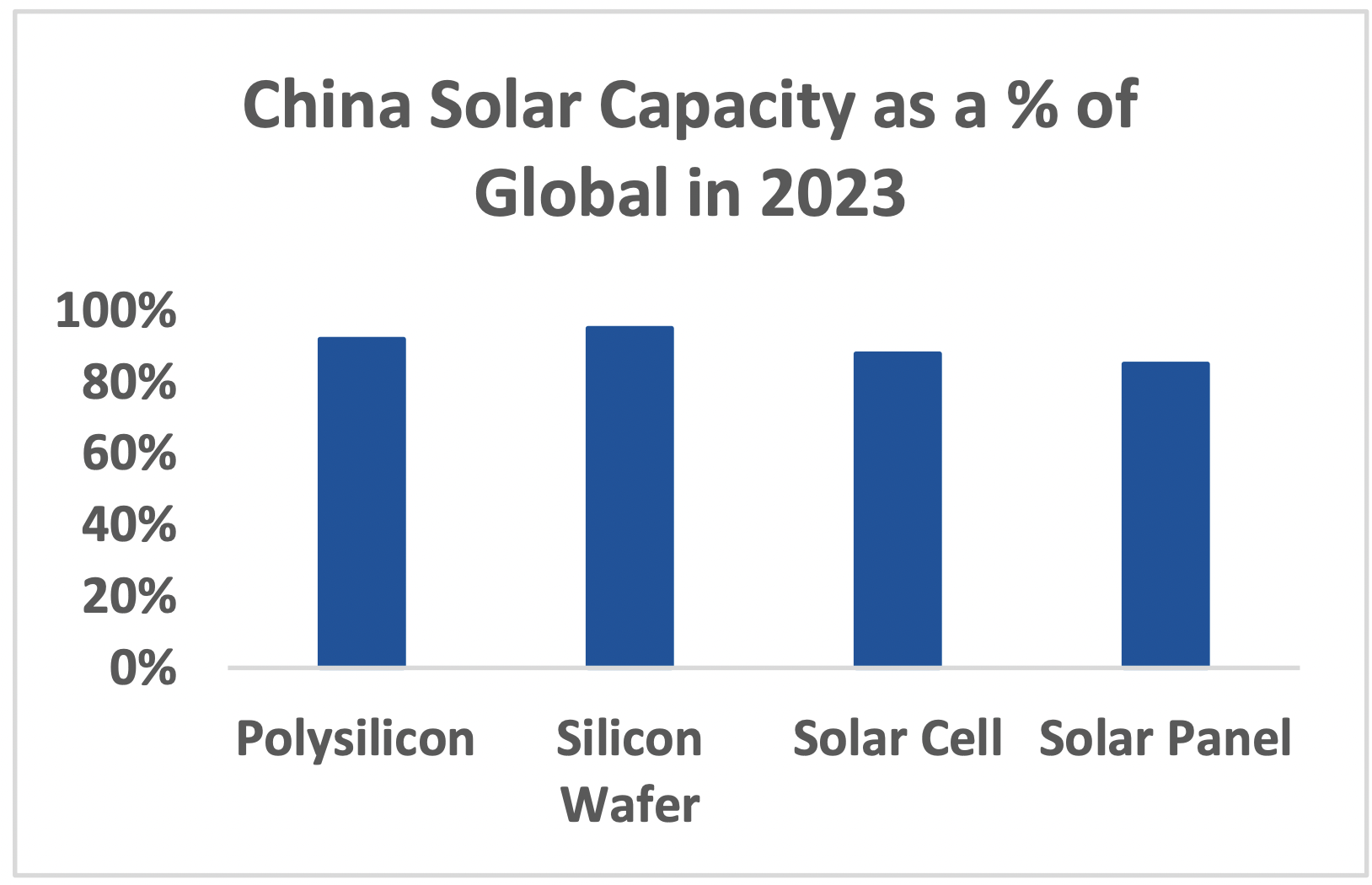

The solar industry value chain consists of multiple stages: polysilicon production, ingot and wafer manufacturing, solar cell production, and finally, panel assembly. Currently, most Indian companies operate only in the final stage of solar panel assembly—the least technologically and capital-intensive part of the manufacturing process. This limited participation in the value chain creates significant vulnerability and dependence on imports, particularly from China, which controls approximately 80% of the global solar supply chain.

This dependence is now changing with backward integration into silicon wafer and solar cell manufacturing becoming the new buzzwords among Indian companies. With companies having achieved scale and profitability in panel manufacturing along with end product prices stabilising, companies no longer see price declines as a risk to their capital investment and are thus investing in capital expenditure. This vertical integration process is accelerating thanks to the government. Not only has the government provided a long-term vision on the size of the opportunity, but it has also actively incentivised the growth of the industry through various initiatives such as domestic content requirements for government projects, substantial import duties (40% on imported solar panels and 25% on imported solar cells), and Production Linked Incentives (PLI) to encourage manufacturing scale-up. New market opportunities have also been created by incentivising solar pump and rooftop solar projects in both rural and urban India.

In an effort to understand Indian companies’ positioning, we visited the plants of two leading companies, Adani Solar and Waaree Energies and were amazed by the sheer scale and size of the state-of-the-art fully automated plants. Their investments demonstrate the seriousness with which Indian players are approaching vertical integration and technological advancement in this sector.

From an investor’s perspective, the Indian market offers diverse investment opportunities across the solar ecosystem with pure-play manufacturers, independent power producers (IPPs) that develop and operate solar plants, as well as engineering,= procurement, and construction (EPC) companies that implement solar projects. This variety allows investors to participate in different segments of the value chain according to their risk appetite and return expectations.

The story doesn’t stop here. India’s vision is to not only be self-reliant but also become an important export hub for renewables in the world for those looking for an alternative source to Chinese solar products. The US is one of the biggest importers of solar cells and panels. With restrictions on China, this opens up a great avenue for India and it is highly profitable too. In FY24, India’s solar products exports to the US were almost $2bn.

So, is it all Sunshine?

Having interacted with a dozen of the listed companies across the ecosystem, our main concern remains China and its dominance across the value chain ranging from polysilicon to cells.

Source: CLSA, CPIA, Companies, Dec 23

Irrational behaviour can have a domino effect. The dependency is not only in the supply chain but also in technological know-how where China is a leader and innovator. As Indian companies backward integrate, the capital intensity also increases, putting at greater risk the investment whenever there is a change in technology, which typically happens every five years. Our other concern stems from domestic competition. The entry barrier in module manufacturing is low, with the capital expenditure for 1GW of solar module manufacturing capacity at approximately $31 million (INR 2.5 bn). This has attracted a lot of companies, including first-time entrepreneurs, to set up capacities. Hence, it is a highly competitive industry. With the entire ecosystem backward integrating, the buyer/seller equation is itself undergoing a change. Supply is catching up with demand quickly. Consolidation seems inevitable.

The key question remains how we participate in this theme of renewables. We have absolutely no doubt that solar renewable energy is the answer to meeting India’s rising power demand of 6-7% per annum. Solar addresses all the fundamental requirements of cost, time, ease of usage, scalability and, of course, ample sunshine. As the industry evolves, we are in a wait-and-watch mode, closely tracking the business models and leaving no stone unturned to identify the eventual winners. There also remains an extended ecosystem of transmission, battery, glass and other inputs riding piggyback on the solar growth story.

Important Information: The information in this document does not constitute or contain an offer or invitation for the sale or purchase of any shares in the Fund in any jurisdiction, is not intended to form the basis of any investment decision, does not constitute any recommendation by the Fund, its directors, agents or advisers, is unaudited and provided for information purposes only and may include information from third party sources which has not been independently verified. Interests in the Fund have not been and will not be registered under any securities laws of the United States of America or its territories or possessions or areas subject to its jurisdiction, and may not be offered for sale or sold to nationals or residents thereof except pursuant to an exemption from the registration requirements of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and any applicable state laws. While all reasonable care has been taken in the preparation of this document, no warranty is given on the accuracy of the information contained herein, nor is any responsibility or liability accepted for any errors of fact or any opinions expressed herein. Past performance is not a guide to future performance and investment markets and conditions can change rapidly. Emerging market equities can be more volatile than those of developed markets and equities in general are more volatile than bonds and cash. The value of your investment may go down as well as up and there is no guarantee that you will get back the amount that you invested. Currency movements may also have an adverse effect on the capital value of your investment. Investing in a country specific fund may be less liquid and more volatile than investing in a diversified fund in the developed markets. This Fund should be seen as a long term investment and you should read the London Stock Exchange Listing Prospectus published in December 2017 (the ”Prospectus”) whilst paying particular attention to the risk factors section before making an investment. Please refer to the Prospectus for specific risk factors. Where reference to a specific Class of security is made, it is for illustrative purposes only and should not be regarded as a recommendation to buy or sell that security. This document is issued by RGI Fund Management (referred to as River Global) and views expressed in this document reflect the views of River Global and adviser Saltoro Investment Advisors Pvt Ltd as at the date of publication. This information may not be reproduced, redistributed or copied in whole or in part without the express consent of River Global and River Global Investors LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. River Global Investors LLP is a signatory to the UN Principles of Responsible Investment.