The FTSE 100 fell on Thursday as European stocks tracked a sell-off in US shares sparked by rising concerns about US debt.

London’s leading index was down 0.7% at the time of writing.

“The growing mountain of US debt is causing ripples of worry across financial markets, with signs investors are baulking at financing the Trump administration,” said Susannah Streeter, head of money and markets, Hargreaves Lansdown.

“These concerns have hit sentiment in Europe, given the repercussions that financial difficulties in the world’s largest economy would have on the global economy.”

After a record-breaking run of consecutive up days as the FTSE 100 recovered from Trump’s Liberation Day, the pace of London’s gains has slowed this week as the market pauses for breath and concerns about long-standing risks such as the US debt mountain serve as a reality check.

Nonetheless, we are in an infinitely better position than we were in the days following the announcement of Trump’s trade policies, with many market participants remaining bullish on global stocks, despite a number of risk events in the near term.

“Peak trade uncertainty remains in the rear view mirror, incoming data remains resilient for the time being, with incoming earnings also not as bad as had been feared,” said Michael Brown, Senior Research Strategist at Pepperstone.

“That said, I’d imagine that the risk of Nvidia (NVDA) earnings next Wednesday is starting to play on a few minds, and wouldn’t rule out the chance of a bit more de-risking into that report.”

De-risking was rife in London on Thursday, with 86 of the FTSE 100’s constituents trading negatively at the time of writing.

“The FTSE 100 was dragged down by energy stocks and a negative reaction to BT’s results. Marks & Spencer extended yesterday’s small advance as investors saw a path out of the cyber-attack disruption,” explained Russ Mould, investment director at AJ Bell.

BT shares were down 3% as investors booked short-term profits after the group released a mixed set of full-year results.

“A clear sign a company is lacking in focus is when they attempt to do too much and BT is a classic example. Typically, it is the job of new management to come in and streamline operations and bring their attention back to what they are good at,” Russ Mould said.

Housebuilders were among those firmly in the red with Taylor Wimpey, Persimmon and Barratt Redrow all down around 2%.

JD Sports was the FTSE 100 top riser as the sports retailer recovered some of the losses suffered yesterday after issuing a disappointing set of results.

Inheritance Tax receipts are on the rise again. The government’s IHT intake hit £800 million in April 2025, according to data released by HMRC this morning.

This is around £97 million more than the government took from estates in the same period last year, and sets a course for another record year of Inheritance Tax receipts.

“The 2025/26 financial year opens where the previous one left off, with a predictable and substantial annual rise in Inheritance Tax receipts. Estimates last month revealed that IHT receipts for the 2024/25 financial year were 10.8% up on the previous one, and there’s nothing to suggest the current one will be any different,” said Ian Dyall, Head of Estate Planning at wealth management firm Evelyn Partners.

News of higher IHT receipts this morning is a particularly thorny subject, not least because the government doesn’t seem content with how much it is pocketing from people’s estates and is planning a fresh raid on investors to bolster IHT receipts further.

“What has stirred up some interest in the Government’s intentions for IHT – aside from those announced at the October Budget – is the memo from the Deputy PM to the Chancellor leaked this week,” Dyall explained.

“That called for – among other tax rises – IHT relief on AIM shares to be removed altogether, which would go further than the current cut to 50% due for April 2026, and would save the Treasury £1billion. Whether this suggestion carries any weight with the Chancellor is unknown, but with the PM also rowing back on cuts to the Winter Fuel Allowance this week, questions are bound to arise around tax if the fiscal outlook doesn’t improve before the Autumn Budget.”

Changes to the IHT exemption scheme for AIM shares would be a major blow to AIM, a market whose companies create thousands of jobs for the UK economy.

“These businesses need investment in order to grow, and investors need incentives in order to be prepared to take the additional risk associated with them. Removing the inheritance tax incentive entirely could undermine investment in the market,” said Sarah Coles, head of personal finance, Hargreaves Lansdown.

Morningstar’s Michael Field has highlighted ‘three standout European stocks that present significant potential for investors seeking growth’.

The selection is made against Morningstar’s view that there is around 6% upside in European equity markets currently. All three of Morningstar’s standout stocks have fair value estimates that would suggest upside that far outstrips the wider market.

Michael Field, chief equity strategist at Morningstar, outlines the investment case for each of the three stocks in his own words:

Remy Cointreau

Morningstar views Remy Cointreau, French alcoholic beverage group, as 60% undervalued compared to the market price. Morningstar’s Fair Value Estimate for this stock is EUR 119.

“The tariffs placed directly on spirits as part of Trump’s trade war, alongside a weak economy impacting consumer spending, have collectively hurt luxury alcohol brands like Remy Cointreau. Although sales have been impacted by lower high-end consumer spending, this is only temporary, and we believe these shares could more than double in the longer term. For patient investors we believe this will recover in 2026, creating a real opportunity for investors looking to snag a cheap deal,” Michael Field noted.

Mercedes Benz

Morningstar sees value within Mercedes Benz, German automotive company, outlining the stock as 40% undervalued compared to the market price. Morningstar’s Fair Value Estimate for this stock is EUR 90.

“Despite Mercedes Benz being an already established and popular brand, we believe this stock is undervalued, in contrast to other market views. Although automakers have had a rough time recently with lower consumer spending and Trump’s targeted tariffs on the sector, we believe shares could almost double. Mercedes Benz is working on upgrading its S-class models and expanding its offerings of electric vehicles which should boost its sales in 2026,” Michael Field commented.

Rheinmetall

Morningstar see opportunity in Rheinmetall, German automotive and arms manufacturer, with 20% upside compared to the current market valuation. Morningstar’s Fair Value Estimate for Rheinmetall is EUR 2,220.

“Despite the sector rallying since the Russia/Ukraine war broke out, we believe the structural growth story has further to go. Over the next five years we see European defence budgets rising by 35%, which will massively benefit incumbent defence players like Rheinmetall. Countries, like Germany, who have supplied arms to Ukraine will need to replenish stock, which often takes a seven-year cycle, further adding legs to the longevity of this investment opportunity,” Michael Field said.

Revolution Beauty Group (LON: REVB) has received a preliminary bid approach and a formal sale process has begun. The cosmetics supplier requires more funding, and it is still talking to key shareholders. The share price rebounded 30.8% to 6.8p.

Peru-focused gold mining company Nativo Resources (LON: NTVO) is about to publish proposals for the restructuring of its loan notes. This would allow the €10m of capital plus interest (the interest rate is 0% from the beginning of 2025) to be converted into shares at a 10% discount to the volume weighted market price over ten days. The notes are convertible from the beginning of 2032 or when the company market capitalisation exceeds £35m for ten consecutive days. The share price moved up 18.2% to 0.65p.

Artisinal Spirits Company (LON: ART) says revenues grew in double digits in the first four months of 2025 even though the US and China markets remain tough. The growth is coming from bottled whisky sales in Europe and cask sales. The US importing model is being changed. Full year revenues are forecast to grow by 10% to £26m. The share price improved 8.91% to 55p.

Cancer treatments developer Scancell Holdings (LON: SCLP) investor Volpes Testudo Fund, which is represented on the board by Martin Diggle, has bought a further 497,764 shares at 9p each. It owns 12.6% of the cancer treatments developer. The share price rose 8.1% to 10p.

FALLERS

Footwear retailer Shoe Zone (LON: SHOE) says interim trading is in line with expectations with revenues down by 6.5% to £71.5m, although second quarter trading was flat. Store sales were 10% lower. Online revenues were 6.5% higher. Stores are being closed. Shoe Zone fell into loss in the first half, but the second half should be better. Full year pre-tax profit is expected to halve to £5m. The share price declined 19.6% to 92.5p.

More disappointing news from Pantheon Resources (LON: PANR). The flow testing of the Lower Sag 3 reservoir level in the Megrez-1 well in Alaska. The well is suspended. The focus will switch to Ahpun West and the Dubhe-1 well will drill this year. Final investment decision on Ahpun West should be in 2027. The share price slipped a further 18.7% to 21.625p.

Time Out (LON: TMO) is reviewing the future of the original media division because of falling advertising revenues. The division is set to fall into loss this year. The company has eleven food and cultural markets. These revenues ae growing. The share price fell 6.9% to 27p.

Engineer recruitment company RTC Group (LON: RTC) says first quarter trading remains positive, but the second quarter is being impacted by National Insurance rate rises. RTC is focusing on sectors that will enable it to capitalise on growth opportunities. The share price dipped 5.13% to 92.5p.

The FTSE 100 was broadly flat on Wednesday as traders digested the latest set of UK inflation and a plethora of corporate updates.

UK CPI inflation jumped again in April and served as a reminder that the period of higher inflation endured in the wake of the pandemic is not yet over.

April’s reading of 3.5% was almost one full percent higher than March’s 2.6% figure and surpassed economist estimates of 3.3%.

While the jump in inflation is certainly a headline grabber, it wouldn’t have come as much of a surprise to markets. The impact of higher energy bills was well telegraphed, demonstrated by economists’ forecasts going into the release of the data of inflation rising to 3.3%.

“We should always take April’s data with a pinch of salt, but higher inflation leaves the Bank of England happy to carry on at its relatively sedate pace of cutting once per quarter. This uptick in CPI has been on the cards and well discounted already,” said Neil Wilson, Investor Strategist at Saxo UK.

The higher-than-expected reading sent the pound higher against the dollar and weighed on the FTSE 100 in early trade.

However, London’s leading index shook off the impact of higher inflation and recovered early losses as the morning progressed to trade relatively flat at the time of writing.

The FTSE 100’s resilience was on display again as it shook off a number of disappointing earnings updates, including a warning of the impact of the M&S cyber attack and JD Sports outlining plans for slower growth amid challenging trading conditions. M&S shares fell 0.8% while JD Sports was the FTSE 100’s top faller with losses of 6% on the session.

There was strength in Severn Trent and SSE, which helped offset losses elsewhere.

“Utilities did their best to prop up the UK stock market and they were helped by defence contractors once again being in vogue,” says Russ Mould, investment director at AJ Bell.

“Updates from Severn Trent and SSE were well received by the market. The utilities sector has found itself the centre of attention in recent months as investors look to avoid the drama associated with a global trade war and seek solace in defensive areas.

“Water company Severn Trent might lack the go-go growth associated with big name US tech stocks, but it is delivering the kind of performance many businesses can only dream of. Profits and dividends are going up, it is creating new jobs, and demand for its services is unaffected by any fluctuations in the economy.”

The threat of higher inflation and interest rates staying higher for a longer period was inevitably felt by the housebuilders. Barratt Redrow shares were down 2%.

There was interest in defence-related stocks amid disappointment at the progress in Russian ceasefire talks. BAE Systems added 2% and Rolls Royce rose a little over 1%.

This morning’s Interim Results announcement from Avon Technologies (LON:AVON) reported a 16.8% increase in group revenues to $148.7m ($127.1m), while pushing its adjusted pre-tax profits up an impressive 70.1% to $14.8m ($8.8m), with its earnings 76.4% higher at 38.8c (22.3c) per share, with only a small 5.6% increase in its interim dividend to 7.6c (7.2c).

The £528m-capitalised group is a world leader in protective equipment, trusted to protect the world's militaries and first responders, with a reputation for innovative design, high quality, and specialist materials expertise.

In...

We’ve all been there. Picked some great stocks with conviction. Run our winners. Been delighted with the gains. Only to see those gains drain away.

It hurts, it’s galling and you are left wondering where you went wrong.

Worse than that, by the time it happens you may have started counting on those gains as part of your future planning. How are you going to pay for that big ticket item – that home purchase, a children’s education, or that early retirement. It’s very real.

In this piece, I’ll introduce the three mistakes we can all make, and the three solutions.

But first, a personal tale…

(NB – If you’re curious how to build a smarter, rules-based portfolio, join me for a live webinar on Thursday 22nd May at 5pm (BST) – and read on to learn more).

An early education

For me, my big lesson came in the global financial crisis. I was young enough to be reckless, but old enough to have known better.

I had a silly amount of my capital riding on two big picks. Both were AIM listed stocks. One was called Renesola (SOLA) – a solar energy company that was absolutely smashing it on sales growth. The other was RC Group (RCG) – a biometrics company. I’m sure some of you remember these stocks.

I’d bought really well. And I’d bought more as they rose. At their peak, I had 50% of my portfolio in RCG, and probably 30% in SOLA. They really were motoring – they had both already tripled. I couldn’t have been more confident.

It was 2007… what could possibly have gone wrong?

The mistakes we all make

There’s an eye-opening academic research paper by Barber and Odean titled “The Behaviour of Individual Investors”. When I first read it I was gobsmacked. It was a mirror of every mistake I’d ever made, and hugely influential in shaping my future mindset.

I’ve thought long and hard about their findings, and grouped them into three themes:

1. We suffer “perverse stock selection”

That quoted phrase is their words. We often pick risky stocks for the wrong reasons.

We often talk about the perils of story stocks at Stockopedia.com. Stories are how the human mind makes sense of the world, but projecting a hollywood ending onto a share is not rational.

Whether we’re chasing headlines, themes we know a lot about or jumping on a bandwagon so not to miss out. We seem to have a “taste for stocks with lottery-like payoffs”.

But lottery tickets have negative returns!

2. We underdiversify

We buy a share and get to know the theme. The price goes in the right direction, and we buy more. We buy another benefiting from the same theme.

One highlight from the paper showed that “on average investors hold only four stocks” which tend to be “highly correlated” – i.e. too few stocks in too few sectors.

I ended up in 2007 with a portfolio 80% in Chinese AIM stocks. Hindsight is wonderful isn’t it.

3. We buy and sell recklessly

We’re human. We’re prone to want to do something. This action bias might have helped when we were chased by lions, but in volatile markets it’s an extremely expensive tendency.

It’s so easy to buy and sell these days. A trade is just a thumb press away. But ease of trading does not a disciplined investor make. 20% of investors turn over their portfolio almost three times per year – which is not only hugely costly in terms of transaction and tax costs, but can’t be good for mental health.

Beyond this, we’re terribly prone to hanging onto our losers, and snatching at profits. And even worse, we tend to pull all our capital out of the market at lows, and reinvest at highs.

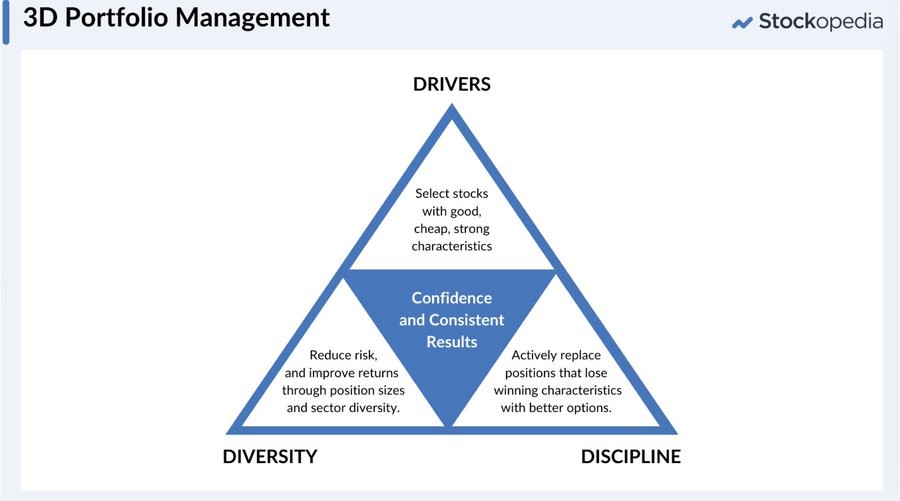

The 3D framework that solves for these

I’m sure we can all recognise some of these behaviours in our own habits. But as John Templeton once said “If you want to have a better performance than the crowd, you must do something differently from the crowd”.

So in this vein, I propose three dimensions of intelligent investing that can guarantee you invest contrary to the three mistakes that almost all investors make.

Invest in stocks exposed to proven Return Drivers.

The simple solution to “perverse stock selection”.

Buy good (quality), inexpensive (value), rising (momentum) shares.

These kinds of shares are highlighted by the Stockopedia StockRanks – which score every share for their quality, value and momentum. These kinds of shares are remarkably ignored by the crowd, but have consistently outperformed over the last decade.

Ensure you have enough Diversity in your portfolio construction.

In ten years of tracking portfolios the highest probability shares, only 7% are likely to double in a single year. So we don’t diversify just to reduce risk, we diversify to maximise our chance of owning a big winner. These are the stocks that can make a real difference to your portfolio.

Own at least 14 stocks to give yourself a better chance of holding a multibagger.

Own stocks across at least 6 (out of 10) sectors, and make sure you own both cyclicals and defensives. Think of your portfolio like a football team – you need strikers and defenders. And be careful going all-in on a favourite theme – we are not so smart!

Avoid huge positions. Start with equal weights.

Pre-commit to buy and sell Discipline.

Have a plan for every share purchase – a plan actively helps you avoid reactive over-trading and snatching at profits. This includes having a sell plan. Whether that sell plan is based on time (e.g. after a one year holding period – to accrue gains), thresholds (e.g. when value is realised, or the StockRank falls below a certain level), or events (e.g. selling immediately on a profit warning).

Only hold for the long term the highest quality securities. Be extremely wary of just holding because you’ve grown familiar with the story. The numbers must back it up. As Jim Slater would say – “be first in the line of disappointed enthusiasts” if something goes wrong.

Don’t hang onto your losers – have a bias to selling them (using a stop loss, or after a fixed time), or average down (but only if you have genuine insight – which you probably don’t). Doing nothing creates opportunity cost, and can turn a small loss into a big one.

The consistent application of simple rules is extraordinarily powerful. As Van K Tharp once said:

If you don’t have rules, everything you do is a mistake.

Putting the rules to work

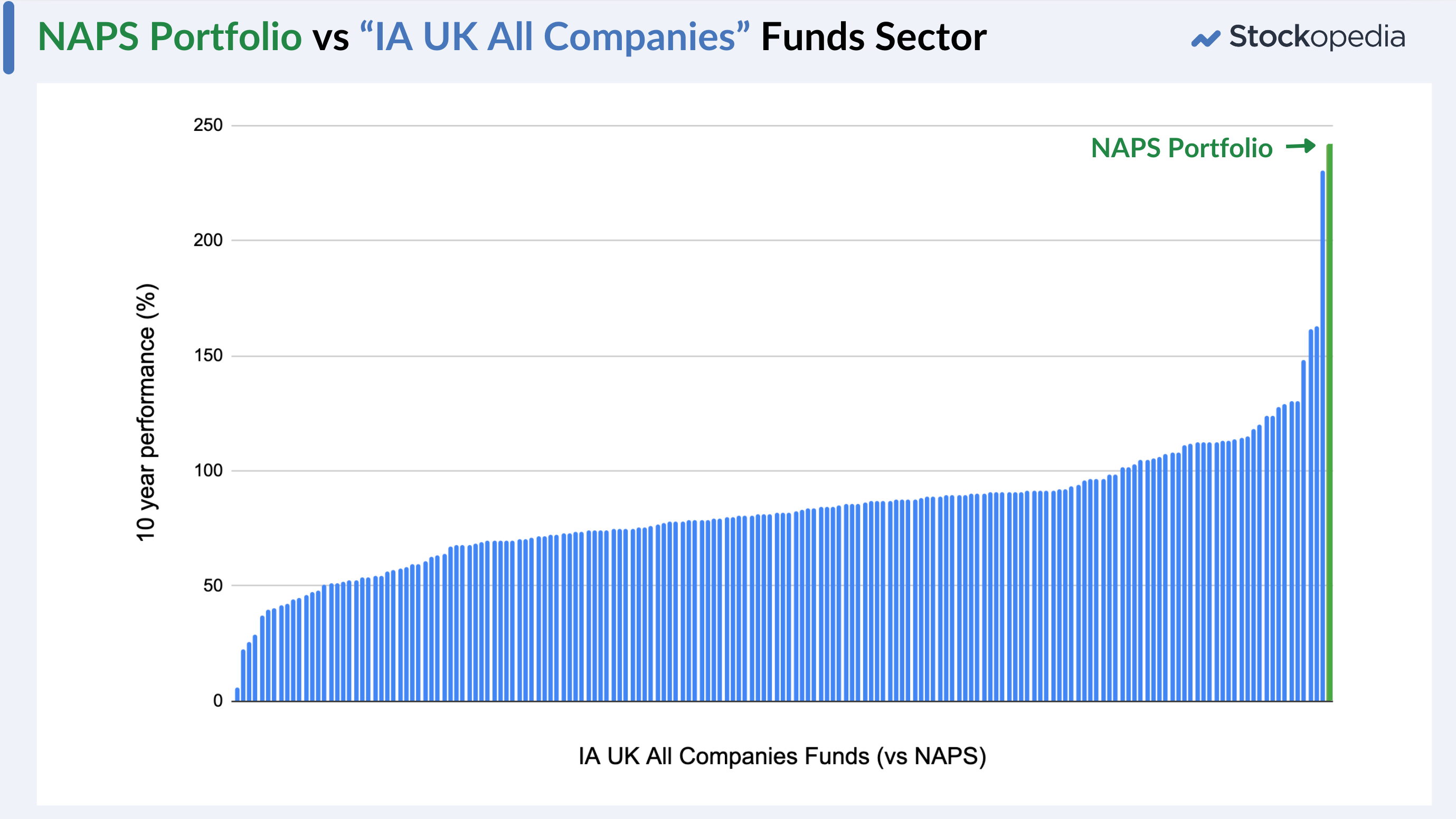

At Stockopedia, we’ve run a portfolio based on these principles for a decade. It’s an equal weighted 20 stock portfolio, populated with the highest quality, value and momentum stocks, refreshed once per year. There’s no stock picking. It’s a simple rules-based approach that works.

Known as the “NAPS” Portfolio – as it’s a “no admin portfolio system” – the portfolio has beaten every single fund manager in the UK over the decade to 2025.

To learn more about putting these ideas to work in your own investing, or to learn about how the NAPS Portfolio works – join us for a live session this Thursday 22nd May at 5pm – “The Smarter Way to Build a Market-Beating Share Portfolio” – or catch up on the replay if you miss the date.

A higher-than-expected UK CPI inflation reading of 3.5% sent the pound higher against the dollar on Wednesday as heating bills drove average prices up.

“Inflation is back with a bang: like an unwanted house guest, breaking down the door, emptying the fridge and bleeding you dry,” said Sarah Coles, head of personal finance, Hargreaves Lansdown.

“The spike in prices is the biggest we’ve seen since the cost-of-living crisis, and even larger than had been forecast.”

Economists had predicted CPI would rise to 3.3% in April from 2.6% March. The bigger-than-expected jump will bring into question whether the Bank of England has scope to cut interest rates further after reducing rates by 25bps at their last meeting.

Core inflation rose to 3.8% from 3.4% in March.

“The jump in inflation in April was always on the cards due to the rise in energy bills, but it has exceeded forecasts – marking the highest rate in over a year. It underlines the fact that the path back to target inflation is far from straightforward,” said Myron Jobson, Senior Personal Finance Analyst, interactive investor.

“Core inflation, which strips out volatile food and fuel prices to provide a clearer picture of the underlying trend, has also edged higher, raising questions over whether this could slow the Bank of England’s interest rate cutting cycle. That remains to be seen. What’s clear is that the need to turbocharge economic growth – particularly amid growing uncertainty stemming from Trump’s tariff war – remains a key priority.”

Taylor Wimpey and Barratt Redrow shares are a screaming 'buys' with one key financial ratio underscoring the deep value available to long-term investors.

The UK housing market has had a tough time during the period of rising inflation and higher interest rates. The impact on housebuilders is well-documented.

However, the challenging conditions have created opportunities in the sector. None more pronounced than shares in FTSE 100-listed Taylor Wimpey and Barratt Redrow.

There are various macro influences on TW and BTRW shares, but there is one metric investors should have at the front of their...

Chain manufacturer Renold (LON: RNO) has received two bid offers one is 77p/share in cash from Webster Industries and the other is 81p/share in cash from a consortium comprising Buckthorn Partners LLP and One Equity Partners IX, L.P. The share price jumped 40.5% to 76.7p.

Telecoms testing equipment supplier Calnex Solutions (LON: CLX) returned to profit in the year to March 2025 as revenues recovered from £16.3m to £18.4m. New product launches helped, as did greater focus on newer markets such as defence and cloud computing. There was a strong fourth quarter and net cash has improved from £10.9m at the end of March 2025. The order book has increased, and Cavendish forecasts an improvement in pre-tax profit from £700,000 to £800,000 this year. That is still well below peak profitability. The share price is 9% higher at 54.5p.

Medical imaging technology company Ixico (LON: IXI) grew interim revenues 26% to £3.2m. The loss reduced. Cash was £5m at the end of March 2025. The order book is £13.1m. Cavendish believes that Ixico can beat its full year revenues forecast of £6m. The share price increased 8.33% to 45.5p.

EKF Diagnostics (LON: EKF) says it is benefiting from its rationalisation process, and this has helped to offset tariffs and unfavourable exchange rates in the US. The pipeline for contract manufacturing and fermentation is improving. Hematology remains the focus of growth. Cash was £15.7m on 9 May and it should grow year-on-year. The share price improved 7% to 26.75p.

Metals One (LON: MET1) has staked 99 additional claims at the Swales god property in Nevada. The phase one exploration programme will be expanded. There will be detailed geological mapping, surface sampling and evaluation of historic workings. The share price rose 3.79% to 40.9975p.

FALLERS

X-ray imaging technology developer Image Scan (LON: IGE) was hit by delays in a defence contract in the first half and revenues slumped from £1.1m to £350,000 and the loss increased to £420,000. Zeus no longer expects a profit this year after reducing its revenues forecast by 37% to £2.2m. The share price slumped 21.2% to 1.3p.

Drug developer Poolbeg Pharma (LON: POLB) is raising £4m at 2.5p/share and could raise up to £100,000 from a retail offer. The cash will last into 2027. It will be spent on th POLB 001 phase 2a trial to “prevent cancer immunotherapy-induced Cytokine Release Syndrome, a severe, potentially life-threatening side effect of cancer immunotherapies”. Topline data is expected by the end of 2026. An Oral GLP-1 proof of concept trial for an obesity treatment. The share price dipped 8.77% to 2.6p.

Alien Metals (LON: UFO) has completed the joint venture transaction with Errawarra Resources, which is changing its name to West Coast Silver. This covers the Elizabeth Hill silver project in Western Australia. Alien Metals retains a 30% stake and does not have to contribute cash until a decision to mine. The share price slipped 7.89% to 0.0875p.

Fintel (LON: FNTL) confirmed at its AGM that it is trading in line with expectations. The provider of services to financial businesses has completed the acquisition of RSMR and gained six new customers after the launch of Matrix360 in the general insurance market. The share price slipped 3.97% to 278.5p.