Klarna was set to be one of this year's headline IPOs, providing investors an opportunity to secure a slice of the leader in the rapidly expanding world of 'buy now, pay later' (BNPL).

Then, Donald Trump and his tariff announcement came along and sparked a wave of volatility that led to a number of US listings, including Klarna's, to be postponed.

The impact of the postponed IPO was felt in this London-listed investment company that holds a stake in Klarna and other exciting and well-known technology companies.

The recent dip in the investment company's shares presents an opportunity for inve...

Next shares rose on Thursday after the retailer released another encouraging trading update and increased it’s full year guidance.

Next has delivered another strong performance in the first quarter of 2025, surpassing its own sales growth estimates by £55m.

The company reported full price sales growth of 11.4% for the thirteen weeks to 26 April 2025, considerably higher than their original forecast of 6.5% growth.

The retailer attributed much of this impressive performance to the favourable weather conditions during the period, which particularly boosted sales of summer fashion lines.

The surge in spending has prompted Next to raise its full-year profit forecast by £14 million to £1,080 million, representing a 6.8% increase compared to the previous year.

“Next continues to deliver for investors, with yet another profit upgrade continuing its hot streak. Sales over its first quarter were well ahead of expectations, nearly double the group’s forecasts,” said Aarin Chiekrie, equity analyst, Hargreaves Lansdown.

“In the UK, both online and in-store sales powered higher at mid-single digits. There had been some weakness from in-store sales of late, but it looks like the better weather has convinced shoppers to head to stores to try before they buy.”

Despite a note of caution that the weather-induced strong performance of Q1 would not be continued throughout the year, Next shares jumped over 1% in early trade on Thursday.

Next’s online sales

Next online sales growth is certainly gathering pace. Next’s UK online business grew by 8.9%, with the LABEL UK platform—which hosts third-party brands—showing eye-catching growth of 15.7%.

Most impressive was the international online segment, which surged by 29.6%, highlighting the company’s successful expansion beyond British borders.

Despite the challenging high street environment that has troubled many retailers in recent years, Next’s physical retail shops also performed reasonably, with sales increasing by 5.2%.

Looking ahead, Next management expressed caution about the second half of the financial year, noting that comparative figures from Autumn Winter 2024 present a higher benchmark. Additionally, they anticipate that the full effects of April’s National Insurance increases will begin to impact consumer spending in the latter part of the year.

The retailer’s updated guidance for the full year now anticipates total sales growth of 6%, up from the previous forecast of 5%. This translates to expected total group sales of £6.6 billion and pre-tax earnings per share growth of 10%.

Next also confirmed its ongoing share buyback programme, having purchased £81 million of shares to date, with plans to buy back a total of £316 million during the financial year, subject to share price conditions. The company has set a buyback limit of approximately £116 per share, based on its latest profit guidance.

Swindon-based newspaper and magazines distributor Smiths News (LON: SNWS) is pushing forward with trials of potential new operations that will make up the decline in the core business and could grow the overall business.

There is a customer base of more than 22,000, which can be offered additional services. These can be large chains of retailers or independents. The distribution infrastructure can be used for other products.

Smiths News Recycle is already offering a recycling service to its clients, where it collects paper and plastics from them. A regional trial has started broadening the cus...

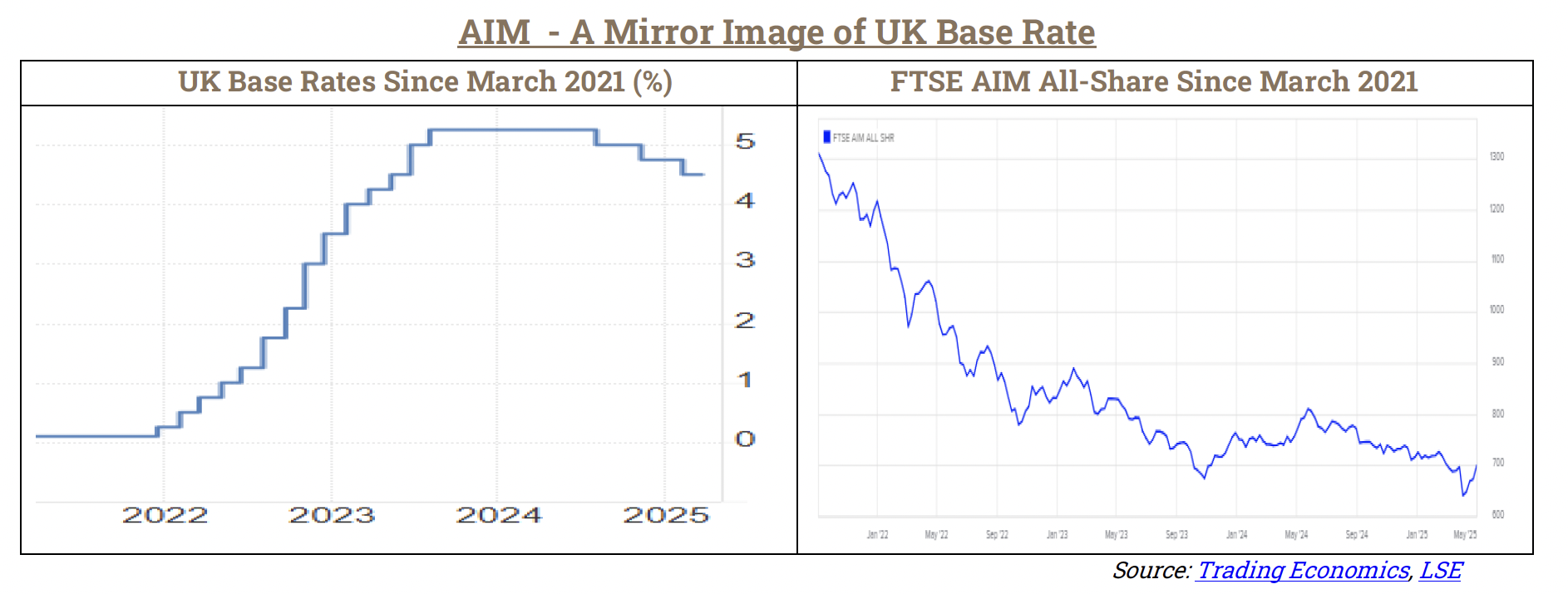

AIM is set to outperform the All Share for remainder of CY2025

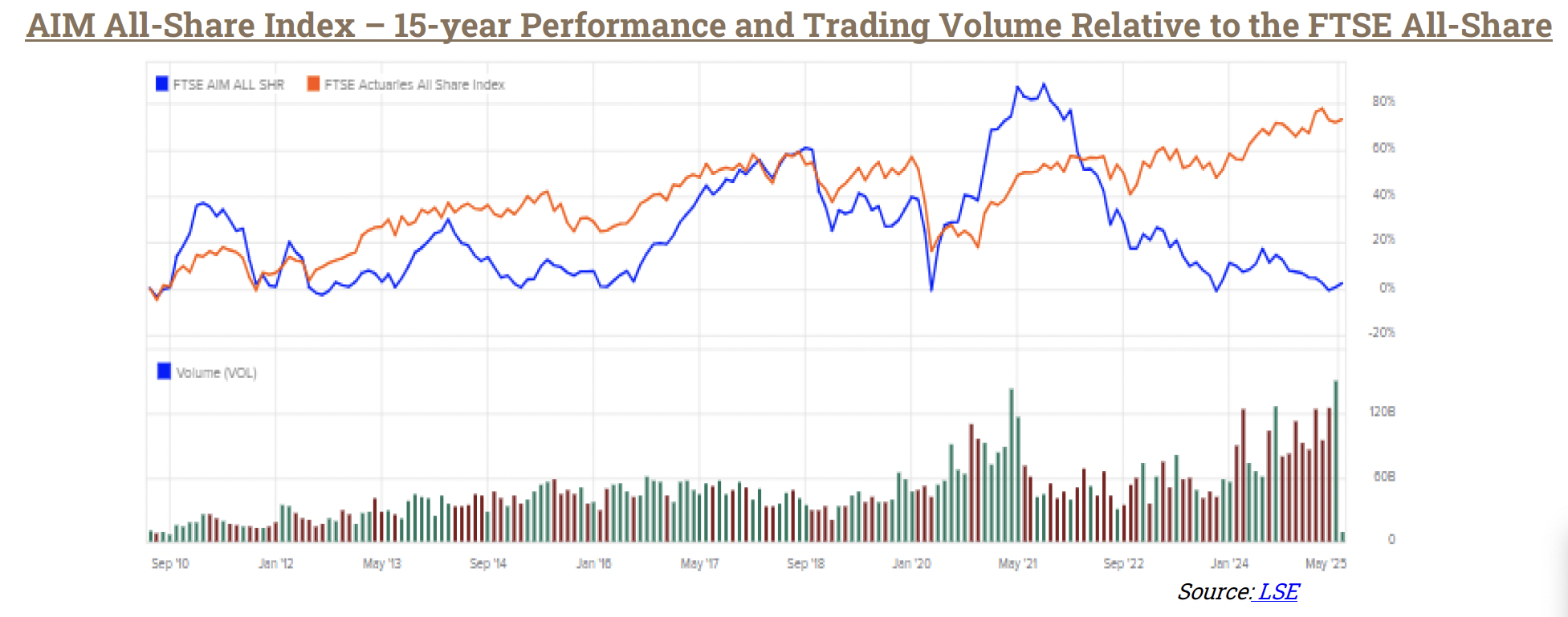

The perfect storm that hit London’s AIM following peak-Pandemic in Q2 2021, has seen the index tumble by an extraordinary 60% relative to the FTSE All Share leaving it trading almost 40% below its 10-year average.

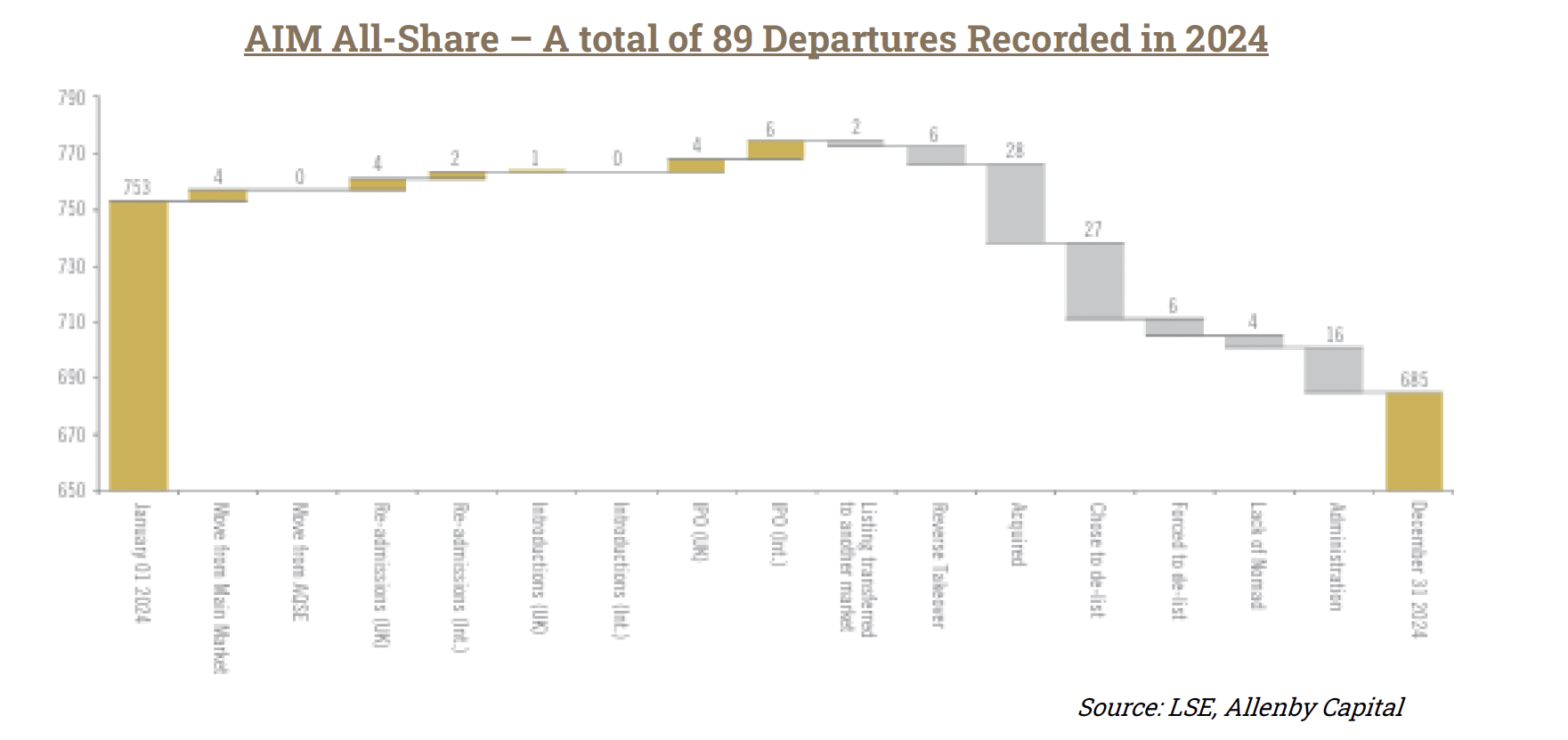

Total listings have thinned down to just over one-third of the number that was achieved back in 2007, due primarily to the index’s highly innovative, but cash-hungry constituents routinely finding themselves unable to secure the funding necessary to create value through fulfilment of their business plans.

The recent dearth of IPOs now leaves a surviving rump of much better positioned, higher quality businesses led by experienced management that have continued to progress their unique opportunities which are often supported by key assets and/or global IP.

The extent of the market’s perceived undervaluation has been highlighted by one key market player suggesting that as many as one-third of <£250m value AIM companies are now vulnerable to hostile bids.

The 41 consecutive months of UK-focused equity fund outflows that followed Brexit have been one of the principal drivers of AIM delistings. This now appears to be slowing sharply and, with the recent halving of the inheritance tax exemption also having been priced in, focus is likely to return to the index’s cost of capital, which is widely expected to track a series of UK base rate cuts downward between now and the year end.

As part of its ‘Plan for Growth’, the Labour party is also said to be considering UK pension and ISA reform as a route to unlocking significant new investment in domestic growth businesses. The suggestion a set proportion of this will be directed specifically to unlisted securities offers scope to significantly reinvigorate the AIM index.

Contrasting with the FTSE100, AIM has almost negligible direct exposure to Trump Tariffs. Yet it and the wider UK market will clearly benefit from more competitive pricing from China as production originally destined for the US gets redirected, along with potential to exploit trans-shipment trade opportunities resulting from the country’s relatively low 10% imposition and its position amongst the most advanced nations in terms negotiating a US free trade deal.

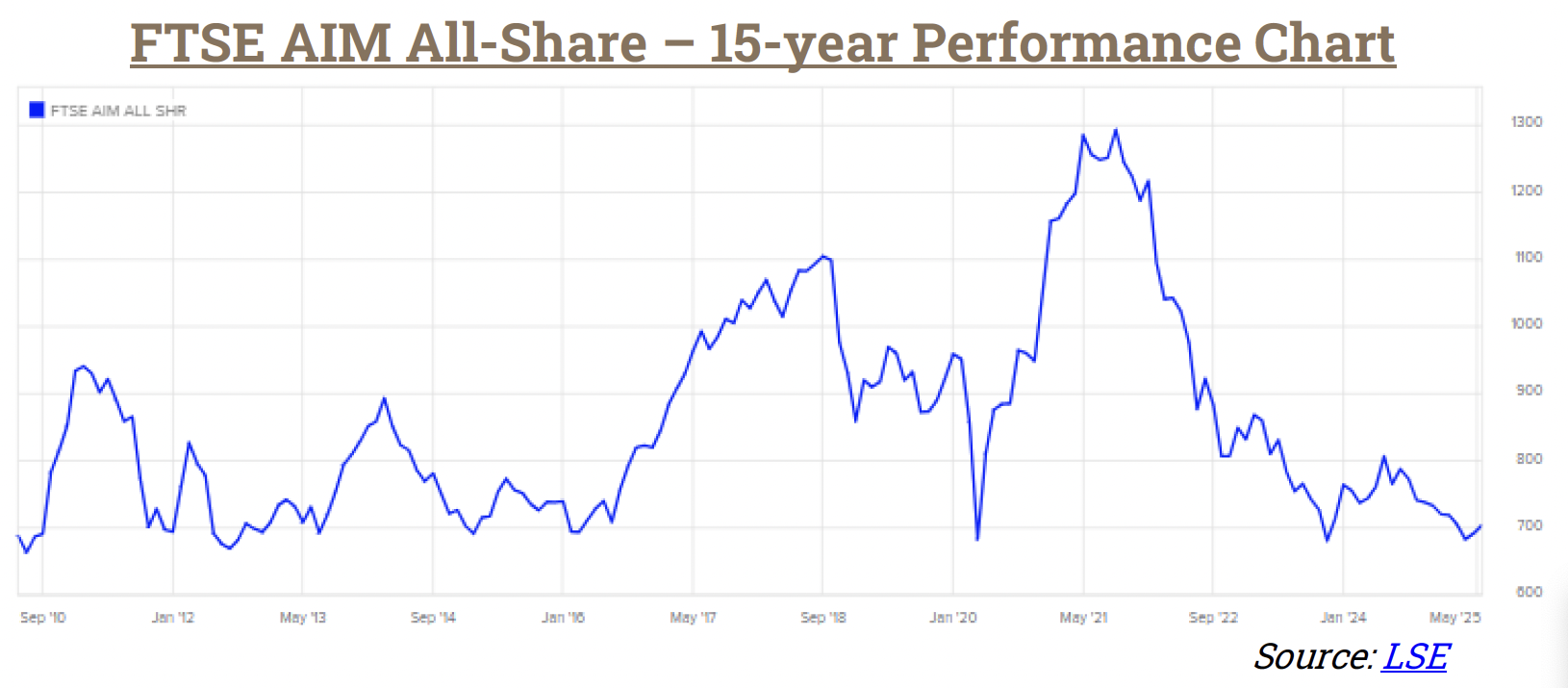

Chartists will also be interested in the fact that the AIM All-Share has rebounded decisively no less than nine times from its current level (±3.0%) over the past 15 years, as can be seen in the long-term chart below:

FTSE AIM All-Share Data Index Level: 709.22 Net Market Cap: £41,301m No of Constituents: 586 52 week high/low: 810.02/624.42 1-year Return: -7.13%

Constituent Sizes and Yield Ave. Market Cap: £70.48m Largest Mk Cap: £3,587.50m Smallest Mk Cap: <£1m Index Yield: 1.21%

Trump’s perspective for his second 100 days – Respite for global equity and bond markets

The current 90-day tariff pause may well be extended beyond 8 July as intense negotiations continue

Adoption of a flexible, country-by-county approach offers possible route to limit net economic damage

US’s softening stance on China is key and could result in major concessions/agreements from both sides

Trump’s team looks to strike as many as 90 trade deals during the present 90-day pause with more to follow

Notwithstanding the above, anyone brave enough to tackle their country’s economic woes head-on in such an unorthodox manner will of course face significant risk from their political rivals – just ask Liz Truss!

The jury is still out in terms of what exactly President Trump truly expected his ‘Liberation Day’ to ultimately deliver. Face on he was blatantly forcing the US’s trading partners to his door as part of a ‘shock horror’ tactic to put himself firmly in the driving seat, kick off a reset in the way the global economy is run and provide a credible route to regain control of his nation’s spiralling deficit. The reasoning is simple enough. Decades of ineffectual tinkering by past presidents have seen the US’s national debt rise unsustainably (now >US$36 trillion) and the call was clearly out there for someone with ‘big enough shoulders’ to take the situation in hand.

But having promised Americans a “boom like no other” if he was elected president for a second time, Trump was certainly not handed a mandate to upend the US economy, become a world pariah and threaten domestic standards of living. On one hand, it might be possible to believe Trump was simply bamboozled by the White House’s sums pointedly failing to recognise the true price (in terms of faltering domestic growth, spiralling inflation, an exodus of international investment, reduced consumer choice etc.) that would need to be paid by the US electorate. On the other, numerous retreats/concessions/olive branches effected or offered rapidly after declaring his hand (incl. the 90-day tariff pause, numerous exemptions such as smartphones, pharma etc. and a 2-year tariff offset on auto parts, while reaching out for discussions with China etc.) along with a declared ambition to strike as many as 90 trade deals (with India, Japan and South Korea looking likely to be the first) during the current 90-day tariff pause, suggests the true gameplan may always have been to adopt widespread negotiated policy flexibility. Trump possibly never expected to actually receive what his team’s apparent tariff algorithm originally set out, but at the very least believe it will enable him to eventually conclude a long list of country-by-country agreements predicated on formal, longer-term understandings regarding their future investment in and prospective trade balances with the US.

While Liberation Day will undoubtedly leave the global economy with some residual damage, the successful conclusion of such negotiations could potentially limit the net domestic/international impact, while placing the US on a more sustainable long-term footing and endorsing its role as the world’s sole superpower. His stance is most definitely courageous and will take some years to play out. So, the question could instead be, does he really have that long? There are very few brave enough to challenge him head-on over his running of his economy, but his team are already said to be preparing for an impeachment fight in case the Democrats take control of the House in 2026. Liz Truss, who very briefly assumed the UK’s premiership in 2022, would of course be the first to testify that those taking such giant economic steps (or gambles?) on anything but a highly measured and carefully negotiated basis involving all stakeholders along the way, can find themselves on a very short fuse.

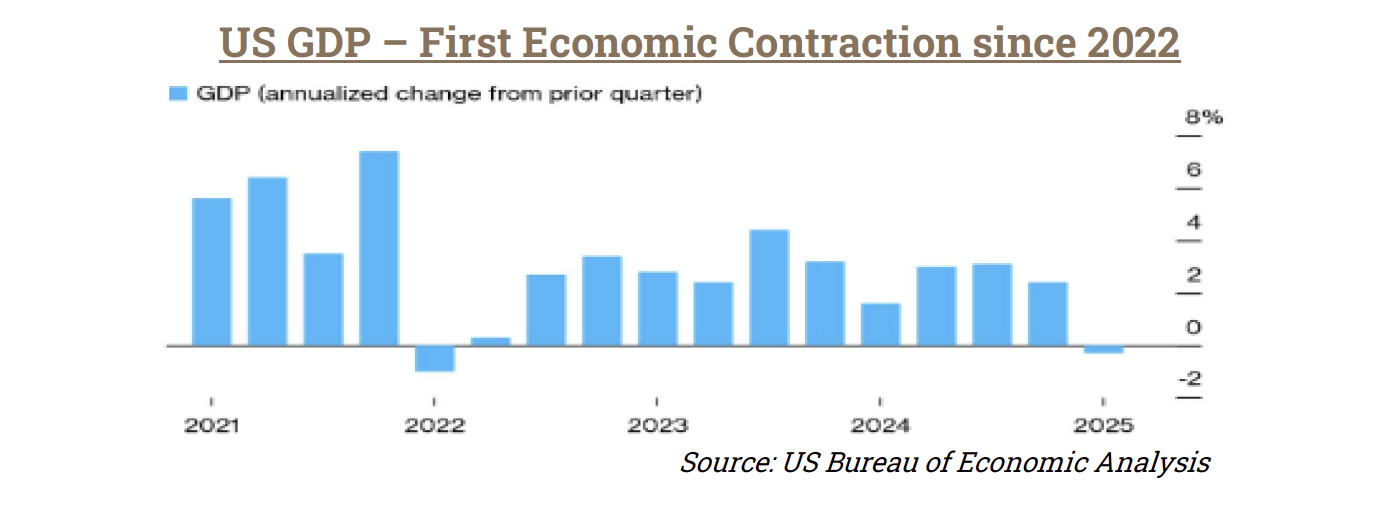

Marking his 100th day in office at a rally in Michigan on 29th April, Trump declared he had “… delivered the most profound change in Washington in 100 years” and that he had “just gotten started.” But having promised Americans a “boom like no other” if they elected him president, the 78-year-old Republican’s performance for consumers, companies, the economy and workers, is now clearly much less celebratory. For someone who feeds foremost on public adoration, the flipping of his approval rating from positive to negative since his inauguration must be leaving its mark. The majority of Americans are voicing concern about a recession and how a trade war will affect the economy/employment, the value of their savings after the S&P500 briefly entered ‘bear market’ territory earlier last month and the rising price of goods amid a tumbling US$. Driving this home the same day, Conference Board data confirmed that April’s consumer confidence had fallen to an almost five-year low, followed one day later by the Commerce Department estimating US economy (GDP) had suffered its worst quarter since Covid, contracting 0.3%in the first three months of 2025 (Q4 2024: +2.4%). While this may reflect a surge of imports from US firms seeking to front-run the tariff impositions, the fact that initially defiant trade responses were registered all around the world (particularly from the main battleground, China) and the fact that trade resolutions are likely to take much longer to negotiate than Trump wishes, means that the situation should be expected to get quite a lot worse (including an inflationary spike) before things start to stabilise.

The relative resilience of global market indices following an initial shock reaction, however, reflects foremost a growing belief among traders that the worst may be over following the chaotic rollout on 2 April. Recognising that he is standing on a cliff-edge, Trump’s second hundred days will almost certainly see him move from the offensive to the accommodative when dealing with international trading partners. For the most part they are already forming a long orderly queue outside his door, ready to show willing with packages of carefully crafted proposals. The wild card of course is China and many, particularly amongst other Asian economies, will choose to follow its lead in any discussions. The fact that China has signalled willingness to talk so soon after the US’s outreach through multiple channels, suggests comprehensive exchanges will get underway shortly. International markets will heave a huge sigh of relief once this becomes apparent. The risk for anything else is simply too big; both are aware of the prospective damage a long-term standoff between the world’s two largest economies would have to their future prosperity and that the wounds would be largely self-inflicted.

So, the second 100 days is look set to be the President’s most dangerous period. Warning signals are coming from all corners. The near-term economic impact his policies on the US’s domestic economy and national well-being is likely to painted large for all to see. Trump’s ongoing feud with Jerome Powell suggests the Fed is unlikely to run to his rescue, first seeking to gauge the effects the existing base and proposed tariffs will have on consumer prices and the US$ before responding to the slowing economy. Tumbling popularity in the opinion polls will compound issues still further, with potential to culminate in a second major sell-off of equity and bond markets. This leaves the President pedalling furiously uphill as he looks for agreement across multiple counties/territories, that reduce or eliminate the tariffs altogether (his team have already indicated their aim to strike 90 trade deals during the present 90-day pause), in exchange for negotiated future direct US investment, job creation and prospective trade balance reductions on a sliding scale. There appears to be a few already willing to comply with such demands and their early delivery will likely be highly trumpeted as a successful new framework for dealing with the US. The problem of course is that the list is very long and individual negotiations are likely to become extended, particularly with China. 8 July is the date on which the 90-day tariff pause is due to end. It seems a reasonable guess that it will need to be extended several times in order to get a reasonable quorum onboard. In the meantime of course, the baseline 10% tariff remains in place.

AIM – Now quite dramatically oversold with liquidity gradually improving

In terms of relative valuations, a chart highlighting AIM’s 15-year performance against the FTSE All-Share paints a stark recent picture:

The perfect storm that hit the index after the Pandemic peaked in Q2 2021 has seen it tumble by an extraordinary 60% relative to the FTSE All Share, leaving it trading almost 40% below its 10-year average. Significantly, however, liquidity has gradually started to improve as weaker participants have been forced out and the average market cap/free float rises.

Since 2010, the index has passed through five phases of quite dramatic relative outperformance as value in its constituent’s ability to create significant value through innovation has been recognised. The Pandemic is one such example. AIM is home to a number of highly specialised life science companies that are developing unique solutions for global problems; they demonstrated capability to rapidly refocus their expertise in the search for therapeutics and related products (including vaccines, anti-virals, diagnostics etc.) as part of the international fight against the coronavirus disease (COVID-19). From the global condition first being formally recognised in March 2020, to UK peak mortality (Delta variant) in April 2021, the sector was one of the principal drivers behind the index’s c.90% rerating.

Subsequently, however, the index has been hit with a perfect storm. As the public health emergency began to pass in Q3 2021, AIM experienced a generalised sell-off of companies that had been significantly chased up during the crisis. Almost coincident with this Brexit spurred a medium-term sell-off of UK-focussed equity funds, resulting in 42 consecutive months of outflows which were, of course, often focussed on the markets’ less liquid participants. This particularly drained AIM investment, resulting in an extended run of delistings amongst its weaker, cash-starved constituents which continues today.

As the charts below demonstrate, the cost of capital required to fund growth amongst these young, often pre-revenue, cash-consuming enterprises is also key to their continuing prosperity. Having enjoyed more than five years of exceptionally low base rates (range 0.1% to 0.75%), the post-COVID inflationary spiral that saw UK annualised CPI spike from just 0.7% in March 2021 to a 41-year high of 11.1% by October 2022, resulted in no less than 14 base rate hikes between December 2021 and August 2023. To make things worse, the index’s dilemma was then capped in the Chancellor’s Autumn Budget 2024, with a halving of the effective inheritance tax relief on AIM shares (effective from April 2026) despite the longer-term investment support that it was known to provided. This in turn contributed to a number of its traditional investors and dedicated small/microcap funds being forced to exit, with their sell-down helping to produce a quite extraordinary valuation gap in the process.

The situation, however, appears to have passed its worst and AIM now offers potential for a sharp rebound relative to the UK’s principal indices over the remainder of 2025.

Firstly, it’s important to note that the pace of UK fund redemptions slowed towards the end of 2024, with December recording the lowest level of outflows in several years. UK equity funds specifically experienced just a £1.4 billion outflow in February 2025, easing from £1.7 billion in January, according to The Investment Association. This change appears to be partly due to the FTSE 100’s obvious valuation discount relative to Europe and the US (price-to-earnings ratios of 11x vs. 13x and 21x resp.) and partly due to the Brexit-inspired sell-off finally starting to tail off. Indeed, the recent fund outflow from the US that immediately following last month’s Liberation Day announcement is seen generating net UK inflows in the coming months, as international investors look to park their cash in relatively safer, undervalued, more traditional income generating investments and away from premium-priced growth/tech stocks that will remain vulnerable until the global situation can be clarified.

UK Base rates are also headed downward. Back in January Morgan Stanley, for example, forecasts no fewer than five cuts (of 25bp each and one of which has already been delivered) in 2025. Clearly this could accelerate faster still if Trump tariff’s result in the sharp near-term contraction across the major western economies that is now widely projected.

Having already seen the index price in next year’s reduction in inheritance tax relief, there now appears to be

more positive signals coming from HM Government. It appears to recognise that further weakening or sidelining of AIM would be an effective admission that Britain is not interested in supporting entrepreneurs, start-ups and growth businesses. While vague threats to Enterprise Investment Scheme (‘EIS’), Venture Capital Trusts (‘VCTs’), Entrepreneurs’ Relief etc., appear to have dissipated, different means for more direct for incentivisation are being sought. Various routes to drive willingness to take risk are being considered, including UK pension and ISA reforms that could potentially unlock billions of liquidity for such assets. Talks of replicating the so-called ‘Canadian’ model of pension ‘mega-funds’, which would merge the UK’s 86 local authority pension schemes, is one idea. The so-called Mansion House Compact, which was signed by 11 of the country’s large pension providers in 2023, also commits them to a target of investing 5% of their pension fund assets into unlisted equities by 2030. The eventual timing of such any such moves of course remains uncertain and care has to be taken not to overwhelm a junior market that has shrunk quite dramatically in recent years. Nevertheless, early indication of moves in this direction could significantly reinvigorate AIM, creating a rush of new IPOs in the process.

With the total count of AIM All-Share constituents now down to just 586, a little over one-third of the 1694 achieved at the index’s peak, the recent dearth of IPOs leaves the ‘surviving’ constituents with far more experienced management who continue to progress opportunities that are often backed by key assets and unique, global IP. The value this has to potentially introduce for larger, cash-rich acquisitive enterprises was highlighted by UK investment bank, Peel Hunt, at the end of last year when its head of M&A anticipated a ‘wave of demand’ from private equity and foreign buyers looking to take-out small and mid-cap UK stocks. It considered up to one-third of sub-£250m market cap firms quoted on of London’s junior stock market to be vulnerable to a takeover in 2025 in a “major and sustained” deluge. Of the 28 takeovers concluded in 2024 (vs. 22 in 2023), the average bid premium when compared to the prior day’s close was +66% (median +50%) with a range of -63% to +252%.

THIS DOCUMENT IS NOT FOR PUBLICATION, DISTRIBUTION OR TRANSMISSION INTO THE UNITED STATES OF AMERICA, JAPAN, CANADA OR AUSTRALIA.

Conflicts

This is a non-independent marketing communication under the rules of the Financial Conduct Authority (“FCA”). The analyst who has prepared this report is aware that Turner Pope Investments (TPI) Limited (“TPI”) has a relationship with the company covered in this report. Accordingly, the report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing by TPI or its clients ahead of the dissemination of investment research.

TPI manages its conflicts in accordance with its conflict management policy. For example, TPI may provide services (including corporate finance advice) where the flow of information is restricted by a Chinese wall. Accordingly, information may be available to TPI that is not reflected in this document. TPI may have acted upon or used research recommendations before they have been published.

Risk Warnings

Retail clients (as defined by the rules of the FCA) must not rely on this document.

Any opinions expressed in this document are those of TPIs research analyst. Any forecast or valuation given in this document is the theoretical result of a study of a range of possible outcomes and is not a forecast of a likely outcome or share price.

The value of securities, particularly those of smaller companies, can fall as well as rise and may be subject to large and sudden swings. In addition, the level of marketability of smaller company securities may result in significant trading spreads and sometimes may lead to difficulties in opening and/or closing positions. Past performance is not necessarily a guide to future performance and forecasts are not a reliable indicator of future results.

AIM is a market designed primarily for emerging or smaller companies and the rules of this market are less demanding than those of the Official List of the UK Listing Authority; consequently, AIM investments may not be suitable for some investors. Liquidity may be lower and hence some investments may be harder to realise.

Specific disclaimers

This document has been produced by TPI independently. Opinions and estimates in this document are entirely those of TPI as part of its internal research activity. TPI has no authority whatsoever to make any representation or warranty on behalf of any of the markets or indices mentioned in this report

General disclaimers

This document, which presents the views of TPIs research analyst, cannot be regarded as “investment research” in accordance with the FCA definition. The contents are based upon sources of information believed to be reliable but no warranty or representation, express or implied, is given as to their accuracy or completeness. Any opinion reflects TPIs judgement at the date of publication and neither TPI nor any of its directors or employees accepts any responsibility in respect of the information or recommendations contained herein which, moreover, are subject to change without notice. Any forecast or valuation given in this document is the theoretical result of a study of a range of possible outcomes and is not a forecast of a likely outcome or share price. TPI does not undertake to provide updates to any opinions or views expressed in this document. TPI accepts no liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document (except in respect of wilful default and to the extent that any such liability cannot be excluded by applicable law).

The information in this document is published solely for information purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. The material contained in the document is general information intended for recipients who understand the risks associated with equity investment in smaller companies. It does not constitute a personal recommendation as defined by the FCA or take into account the particular investment objectives, financial situation or needs of individual investors nor provide any indication as to whether an investment, a course of action or the associated risks are suitable for the recipient.

This document is approved and issued by TPI for publication only to UK persons who are authorised persons under the Financial Services and Markets Act 2000 and to professional clients, as defined by Directive 2004/39/EC as set out in the rules of the Financial Conduct Authority. This document may not be published, distributed or transmitted to persons in the United States of America, Japan, Canada or Australia. This document may not be copied or reproduced or re-distributed to any other person or organisation, in whole or in part, without TPIs prior written consent.

In content advertising company Mirriad Advertising (LON: MIRI) continues to recover some of last week’s share price decline and is 60.7% higher at 0.045p, although 86.8% lower on the week.

Staffing company Empresaria Group (LON: EMR) has received a bid approach from a consortium of individuals, including the boss of the offshore services division of the company. The 60p/share indicative offer comprises 10p/share in cash and 50p/share in loan notes to be redeemed on the third anniversary of the acquisition. The Empresaria board believes the offer undervalues the company. However, two major shareholders are keen for options to be explored to realise value in the business and the initial approach may encourage others. The share price jumped by two-fifths to 35p.

Automotive interior components supplier CT Automotive (LON: CTA) improved margins in 2024 through cost reductions and greater efficiency. That enabled pre-tax profit to edge up from $8.3m to $8.7m even though revenues declined. A rise in pre-tax profit to $10.5m is expected this year. There is uncertainty about US tariffs, but the company can move supply from China to Mexico. The share price increased 25.5% to 29.5p.

Paper and advanced materials manufacturer James Cropper (LON: CRPR) expects to report flat EBITDA of £6.7m for the year to March 2025. Growth in advanced materials did not fully offset the lower paper and packaging contribution to revenues, which is set to remain flat this year. The new chief executive is cutting costs to help profitability of the paper and packaging division, and he will provide an update on strategy in June. The share price recovered 13% to 152.5p.

Vast Resources (LON: VAST) says that there were an additional 6,000 carats of gem quality stones in the parcel held by the central bank of Zimbabwe. This takes the total to 135,000 carats. They will be sold in phases. The share price rose 5.95% to 0.445p, having been as high as 0.485p.

FALLERS

Seaweed-based animal feed Ocean Harvest Technology (LON: OHT) says first quarter revenues grew 65%, but it remains loss making. Further funds are being sought from investors, but it has not yet secured any commitments. There is enough cash until mid-June. The share price slumped 76.2% to 1.25p.

Delays in decision making by customers has led to a downgrading of expectations for 1Spatial (LON: SPA). The geospatial software provider is still growing with annualised recurring revenues growing 14% to £19.7m at the end of January 2025. Group full year revenues were 3% ahead at £33.4m with lower services revenues offsetting software growth. Underlying pre-tax profit improved fell from £2.1m to £1.2m. Despite a downgrade, pre-tax profit is still expected to be £2m this year. The share price dipped 12.8% to 44.5p.

Oil and gas producer Angus Energy (LON: ANGS) has deferred the first principal repayment of £1.25m for the Trafigura loan facility. Discussions continue on changes to the repayment schedule. Tests are going on for the new booster compressor at the Saltfleetby field and Angus Energy is assessing ways of boosting production. The share price fell 6.52% to 0.215p.

Zephyr Energy (LON: ZPHR) published positive initial results from the State 36-2 LNW-CC-R well in the Paradox Basin in Utah. During a two day period steady production rates were equivalent to 700-1,066 barrel of oil equivalent/day. This fits with the P50 estimate of reservoir properties. Further results will be announced. The share price declined 9.18% to 4.45p.

The FTSE 100 slipped ok Wednesday as investors erred on the side of caution as trade concerns crept back in ahead of interest rate decisions from the Fed and Bank of England.

After closing higher for 16 consecutive sessions, London’s leading index fell 0.15% in early trade on Wednesday.

“Concerns about how Trump’s tariff wars will play out are still causing jitters, even though the door is open to a deal with China, with talks scheduled for this weekend,” said Susannah Streeter, head of money and markets, Hargreaves Lansdown.

“The FTSE 100 is lower in early trade, after its record run of success, having netted higher closes for 16 sessions in a row. There’s a pause for breath for the Footsie ahead of key interest rate decisions from the Fed and the Bank of England, as investors await the take from central bankers about the current risks to the global economy.”

Despite the clear risks to the global economy, the Federal Reserve isn’t expected to cut interest rates this evening amid frosty relations between Donald Trump and Jerome Powell, the head of the Federal Reserve. Trump is pressuring Powell to cut interest rates while Powell is doing his best to remain politically independent and pointing to the risk of inflation if rates are cut too quickly.

Meanwhile, the Bank of England looks set to cut interest rates to 4.25% tomorrow.

China helped provide some support for the FTSE 100 through fresh stimulus measures that sent Glencore, Prudential and Rio Tinto higher.

However, it was the pharma giants AstraZeneca and GSK that dictated trade on an index level on Wednesday as the pair suffered from the latest comments from the US suggestion the introduction of tariffs on pharmaceuticals in the near future.

GSK was the FTSE 100’s top faller, losing 3%, while AstraZeneca gave up 1%.

BAE Systems was flat after saying it had a ‘strong start’ to the year and was sticking with previously issued guidance.

“BAE Systems is a rare beast on the UK stock market in that it is one of the few companies not to be derailed by tariff and economic turmoil,” said AJ Bell investment director Russ Mould.

“Governments in many parts of the world have pledged to increase defence spending, thereby creating a richer backdrop for BAE to bid for contracts. Most of the equipment delivered to US customers is made domestically with parts mostly sourced from American suppliers, so tariffs aren’t applicable in these cases.

“Trading is ticking along as expected and there is no change to earnings guidance. It intends to hire more people, including the training of many individuals to create tomorrow’s skilled workforce.”

BAE Systems is up 53% so far this year and is one of the best-performing FTSE 100 companies in 2025. Today’s update gave no reason for investors to book these gains as reduce exposure to the stock.

Ahead of today’s AGM Synectics (LON:SNX) has issued a Trading Update stating that its recent wins across all key sectors continue to support the company's solid order book and encouraging sales traction.

The Business

This group is a leader in advanced security and surveillance solutions that help protect people, property and assets around the world.

It transforms customer operations by seamlessly integrating systems, technologies, and data into a unified solution-enhancing safety, improving efficiency, and enabling smarter, faster decision-making and response capabilities.&nb...

Cepro, an award-winning Bristol-based renewable energy company, is crowdfunding to scale its mission to decarbonise and decentralise home energy – and disrupt the energy sector.

Cepro partners with housebuilders to deliver all-electric, future-proof homes at lower cost. They are already operating the UK’s first fully operational residential smart grids and are winning awards for their innovative approach.

Drawing on expertise in the energy sector, retro-fitting and housing, the Cepro team has established a model that finances and installs solar panels and batteries into new-build properties, then manages the fully renewable smart grid for residents.

Their aim is to remove the biggest barriers facing house builders when it comes to installing clean energy in new builds. In so doing, they want to pave the way for the UK’s urgent transition away from fossil fuels. Although the UK government has made a legally binding commitment to eliminate fossil fuel reliance by 2050, residential energy use, which accounts for 23% of current emissions, is a major challenge.

Cepro’s model meets this challenge by benefitting housebuilders, homeowners and occupiers alike.

For housebuilders, it lowers the upfront cost of installing renewable energy systems, reduces demand on the grid – easing constraints and speeding up development – and supports Scope 3 carbon emission reductions. For homebuyers and occupiers, the model offers both environmental and financial benefits: they avoid emissions from fossil fuel energy sources and receive a guaranteed lifetime discount of at least 15% on their energy costs, compared with grid prices. All of this is delivered at no additional cost to them.

Cepro is an ambitious company – they also want to disrupt the energy sector by providing a locally sourced and managed solution. Founder and Managing Director Damon Rand says: “having spoken to leaders within most of the major UK housebuilders now, there is a genuine willingness to deliver solar and batteries once presented with cost-neutral ways to do so”.

Also contributing to Cepro’s momentum is the imminent implementation of the long-delayed Future Homes Standard, which will tighten Part L regulations governing the construction of new homes. By 2030, Cepro aims to capture 18% of the UK residential smart grid market.

The company’s eight person team is based out of central Bristol and is set to grow rapidly to deliver this exciting work. Damon says “We can and should build both the housing AND the clean energy we need at the same time, in the same place. Help us make this possible for housebuilders creating more affordable and resilient communities.”

To learn more about Cepro and how to get involved, visit their website.

New exchange platform will improve investment environment in Vietnam

The Ho Chi Minh City Stock Exchange (HoSE) reopened yesterday 5 May after the Reunification Holiday with an upgraded trading platform. It’s both a necessary and welcome move which will yield immediate benefits for anyone who wants to invest in one of Asia’s most dynamic economies.

Over the longer term, it will help Vietnam’s bid to gain emerging market status in global indexes, a designation that would open up the markets to a far larger pool of investors.

A better way to trade

The new system is based on Korea’s KRX platform. The upgrade has been a long-running project, and not everything has gone smoothly. In fact, the exchange conducted trial runs in April last year before announcing it would temporarily suspend plans to transition.

Now that it’s live, investors can expect an immediate improvement. The new exchange will be able to handle 1,000 orders per second (compared with just 400 on the old platform), transaction speed will improve from 25ms to 10ms and traders will now be able to amend an order without cancelling it.

The new system should also help shorten settlement cycles and lay the foundation for a central clearing counterparty system, which would improve market stability and make trading more efficient and secure.

The upgrade is crucial, as the old system was groaning under the weight of increasing volumes. A surge in volume forced the HoSE shut for several days in 2018 and again in 2021. Temporary improvements by local digital champion FPT allowed trading to continue, but the exchange clearly needed an upgrade to handle the growing number of domestic investors. At last count, there were 9.7 million Vietnamese investors, with close to 150,000 signing up for accounts within the last three months alone.

While domestic investors make up the bulk of trading volume on the exchange, the changes will also be better for investors overseas too. The great majority are brokerages or institutional investors. In the short term, it’s unlikely the new platform will enable overseas retail investors to trade Vietnamese stocks directly using an app.

But for brokerages and institutional investors, the new platform will be better suited to buying and selling without prefunding. Previously, overseas investors were required to prefund trades, which required investors to put money into a local account and wait for it to clear.

This rule was an obstacle for passive exchange-traded funds (ETFs), which usually spread their investments across several markets, replicating the constituents of an underlying index. In order to remain fully invested, they might have to sell shares in one market and then wait several days for the funds to clear in Vietnam, impacting how well they track the underlying index.

The regulators dropped the requirement in November, but that created issues too, because it meant brokerages effectively needed to offer credit in order to settle the trade. The new KRX system will be built to handle the removal of prefunding, making the whole process easier.

From frontier to emerging market

The upgrade to the exchange is part of a broader plan. It will help Vietnam make a case to global index compilers FTSE Russell and MSCI that the country should be treated as an emerging market rather than a frontier market.

This reclassification isn’t just academic. If Vietnam were to attain the designation, it would be a significant transformation with far-reaching impacts. Listed Vietnamese companies would be included in a number of emerging market indexes, which would make them available to a far larger pool of investment capital.

Initially, it might push company values higher as more emerging market funds buy into local stocks to reach their quota of Vietnamese stocks. That would certainly be a bonus for those who are already invested.

Vietnam has been on the watch list for FTSE since 2018, and an upgrade could mean $6 billion in capital inflows from passive and active funds. An upgrade on the MSCI would be worth substantially more, but Vietnam isn’t on the watchlist yet.

Frontier markets are often characterized by poor liquidity, low transparency, limited access for foreign investors, potential for corruption, and weaker regulatory and legal frameworks. But sophistication varies hugely within the category.

Some European countries with small exchanges (Iceland, Romania, the Baltics and Croatia) are included in the MSCI Frontier Markets Index. A number of larger Asian economies like Bangladesh and Pakistan are on it too, while minnow markets like Cambodia and Laos don’t make the cut.

Vietnam seems like a prime candidate for inclusion in the emerging markets index. The economy is one of the strongest performers in Southeast Asia, it’s a key manufacturing hub and the stock market has shown impressive growth. Vietnam is by far the largest constituent of the MSCI Frontier Markets Index, making up 24% of the index.

Even so, the institutional investors, brokers and custodians who decide on classifications for MSCI have so far ruled that Vietnam doesn’t meet the 18 criteria for inclusion. The prefunding requirement was one obstacle to achieving emerging market status. The exchange itself was another.

Now that those two obstacles have been removed, the largest remaining impediment is the limit on foreign ownership of key stocks. In fact, currently more than 10% of the market is subject to such restrictions.

The indexing organisations require that each country spend a year on a watchlist before moving into a new category. That means Vietnam is at least a year away from achieving the upgrade on the MSCI index. FTSE Russell has had Vietnam on its emerging markets watch list since 2018, so its reclassification may come as early as September.

Either way, the upgrade is good news. It will strengthen Vietnam’s case for both, while delivering benefits to investors.

JD Wetherspoon has announced a 5.6% increase in like-for-like sales for the 13-week period ending 27th April 2025, compared to the same period last year.

The pub chain also reported year-to-date like-for-like sales growth of 5.1%.

Total sales for the quarter rose by 5.0%, with year-to-date figures showing a 4.2% increase. The slight difference between total and like-for-like sales reflects the company’s disposal of seven pubs during this financial year.

Despite these closures, Wetherspoon continues its expansion plans with two new pubs that have already opened this year. The company intends to launch an additional four or five establishments before the financial year ends, with approximately ten more planned for the following year.

In a significant development, Wetherspoon has expanded its franchise operations, with four new franchise locations opening during the last quarter. All new franchise pubs are operated by Haven Holiday Parks, bringing the total number of franchise establishments to seven.

The company currently operates 795 pubs across the UK and has acquired seven freehold reversions at a total cost of £17 million in locations where it was previously a tenant.

While the headline sales number will be welcomed by investors, it’s Wetherspoon’s costs that are likely to have the biggest impact of the bottom line this year. The market will have to wait until the group’s next set of results for insight into how rising taxes and staffing costs are hitting profits.

“The company’s main ambition, as always, is to improve its appeal to staff and customers,” said the chairman of JD Wetherspoon, Tim Martin.

“In this connection, for example, the company has invested in new staff facilities in 520 pubs (49 in the current year), including staff rooms and changing rooms, with approximately 270 planned for the future. The investment per pub is approximately £100,000.

“The product range for customers continues to evolve. For example, the company has recently introduced, nationwide, the highly regarded Jaipur traditional ale from the Thornbridge Brewery, as well as renowned international beer brands, Kronenbourg 1664 Biere and Poretti.

“As regards the menu, new initiatives include a gourmet burger offer, which has proved extremely popular in the pubs in which it has been trialled.

“Bearing in mind that recent trading has been helped by favourable weather, the company anticipates a reasonable outcome for the financial year, notwithstanding previously reported wage and tax increases of approximately £1.2 million per week.”