LSE confirms rule change to allow Aramco listing

The London Stock Exchange has been accused of bending corporate governance rules in order to attract the huge Saudi Aramco listing, allowing the group to float 5 percent of the company instead of the 25 percent usually asked for.

Both London and New York have been competing to nab the listing, which could bu the largest in history. For London, it would underscore its reputation as a centre of global finance despite the uncertainty of Brexit.

In order to do so, the LSE has relaxed its requirements for admittance onto the stock exchange, with the FCA confirming that a new category will allow a smaller float for sovereign-controlled companies. Saudi Aramco is Saudi Arabia’s state-owned oil company.

However, the Institute of Directors criticised the decision, saying it would put the “UK’s global reputation as a leader in good governance” at risk. It added that it was “deeply disappointed”, and would lead to “a reduction in standards”.

Aramco has still not confirmed where it will float its shares, or even if it will do so at all.

Distil shares up 13pc as taste for premium gin continues

Drinks brand owner Distil (LON:DIS) saw shares rise over 13 percent on Friday morning, after reporting a jump in both profits and turnover.

The brand, who own Blavod Black Vodka, Blackwoods Vintage Gin and RedLeg Spiced Rum, saw operating profit jump to £0.16 million in the year to end of March, up from £0.01m the previous year. Turnover jumped 23 percent to £1.2 million, with margins unchanged at 58 percent.

“We are pleased to have delivered a strong set of results with significant growth in volumes, revenue and profits, supported by investment in our brands,” said Executive Chairman Don Goulding.

“We look forward to building on this success though further investment in our key brands in the coming year.”

Net operating cash inflow rose to £1.03 million, from £0.91 million the previous the year. Growth was driven largely by strong performances from Distil’s RedLeg spiced rum and Blackwoods Vintage gin, after launching new packaging for the Blackwoods 2017 Vintage gin in the final quarter of the year.

Shares in Distil are currently trading up 13.64 percent at 2.50 (1107GMT).

TSB board gives Paul Pester full support, despite calls for resignation

MPs have pushed for TSB chief executive Paul Pester to quit over his handling of the bank’s recent IT meltdown.

Earlier this week the Treasury select committee advised the bank’s board to give“serious consideration as to whether his position was sustainable”, adding that his comments at the time had been “complacent and misleading”.

The comments were made in a letter from Nicky Morgan, the committee’s chair, to TSB chair Richard Meddings. However, the bank’s board said Pester had their complete support, despite consistent calls for him to step down.

TSB suffered a major IT meltdown six weeks ago, with some customers still facing disruption. Fraudsters also took advantage of the problems, stealing money from teh accounts of 1300 customers.

In her letter, Nicky Morgan said: “This tone has been set from the top – by Paul Pester – and whether intentionally or not he has not been straight with the committee and TSB customers. Dr Pester’s statements that “everything is running smoothly for the vast majority of our … customers” and that “there will be no barriers” to customers switching accounts, and his denial that there were problems on TSB’s fraud reporting line, are all examples of this.

“The Treasury committee, therefore, has lost confidence in Dr Pester’s position as chief executive of TSB, and considers that the TSB board should give serious consideration as to whether his position is sustainable.”

The bank’s response underlined their confidence in Pester’s leadership, saying that the improvements had been made “under the leadership of Paul Pester, who continues to have the full support of the TSB board.”

Patagonia Gold shares edge up on output figures

Patagonia Gold (LON:PGD) shares moved up in early trading on Friday, after releasing output figures for its Cap Oeste operation in Argentina.

Cap Oeste is Patagonia Gold’s only producing asset and the group released no comparative figures. In the first quarter the mine produced 10,662 ounces of gold equivalent, with the average cash cost of production coming in at $693 per ounce, or $756 per ounce including depreciation and amortisation.

“The team at Cap Oeste continue with efforts to optimise the production process, while the installation of the new crushing circuit to reprocess the material already stacked on the leach pad is completed,” the company said.

“The production guidance for the year is currently being reviewed and the market will be updated once this exercise is complete”.

Patagonia Gold said it was using the proceeds from gold sales from Cap Oeste to complete the payment of the new crushing circuit, as well as reducing its net debt position.

Shares in Patagonia Gold are currently up 0.86 percent at 117.50 (0946GMT).

Fuller Smith & Turner shares drop on weak beer sales

Fuller Smith & Turner (LON:FSTA) saw shares sink nearly 3 percent in early trading on Friday, after flat sales in beer and cider pointed to uncertainty in the future.

The group reported a strong set of results despite the flat sales, with profit before tax increasing by 9 percent in the year to the end of March to £43.6 million. Revenue grew 5 percent to £403.6 million, despite the “challenging” market.

“While we are still in a time of national and global uncertainty – and we do not underestimate the related wider market and economic issues that we will have to navigate over the months ahead – we believe we are in a strong position,” said Chief Executive Simon Emeny.

Like-for-like sales in the the managed pubs & hotels division performed better, up 2.9 percent for the period, while like-for-like profit in the Tenanted Inns division rose 3 percent. Adjusted profit before tax rose 3 percent to £43.2 million, from £42.1 million.

Shares in Fuller, Smith & Turner are currently trading down 2.89 percent at 942.00 (0930GMT).

European markets down ahead of G7 meeting

The FTSE 100 opened down on Friday morning, with nearly every share trading down an hour after market open.

The FTSE is currently down 0.74 percent at 7,647.73, with the DAX also down 1.27 percent. Other European markets have followed suit, seeing the CAC40 fall 0.23 percent and the IBEX35 down 0.73 percent.

The impending G7 meeting has spooked investors globally, with Canada set to host the world meeting starting today. America is likely to face criticism over its trade policies from the UK, Germany, France, Japan, Italy and Canada, causing uncertainty.

The economic calendar is fairly quiet at this time of year, meaning G7 speculation is likely to have a bigger effect.

Jasper Lawler ofLondon Capital Group told The Guardian that investors were starting to show “unease” over the potential climate at the G7 Summit, culminating in a softer session for Asia and the weaker start in Europe.

BT shares rise as CEO steps down

BT shares soared on Friday morning, after the group’s CEO Gavin Patterson announced his departure from the company.

Investors cheered the news of Patterson’s decision, which came about after shareholders made it clear they had little confidence in his ability to implement BT’s turnaround plan.

The new plan was unveiled just four weeks ago, designed to breathe new life into the company after it missed both profit and revenue guidance in March. The strategy includes 13,000 job cuts and a move out of BT’s central London headquarters, in order to cut costs amid growing competition.

BT’s chairman, Jan Du Plessis, said:

“The board is fully supportive of the strategy recently set out by Gavin and his team. The broader reaction to our recent results announcement has, though, demonstrated to Gavin and me that there is a need for a change of leadership to deliver this strategy.”

Patterson, who has been the group’s CEO since 2013, said it had “been an honour to lead BT since 2013 and serve as a member of the board for the last 10 years”.

Shares in BT rose by around 2 percent following the announcement.

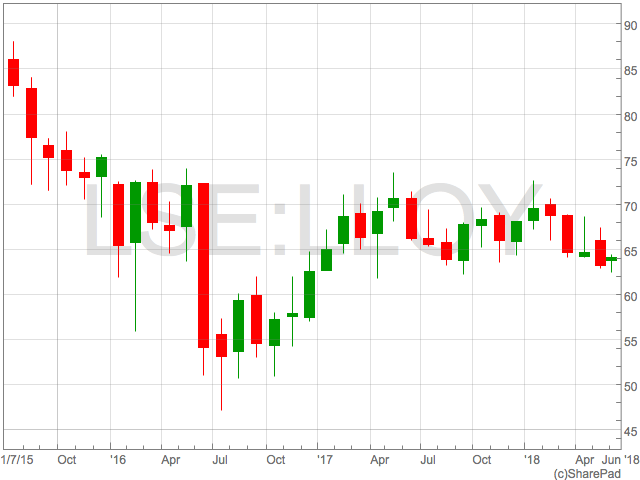

Lloyds share price bounces off strong support

Lloyds share price has remained in a tight range since the beginning of 2017, finding strong support in the 62p – 62.50p and resistance at 73p-74p.

The 200 day moving at 66.7p represents a potential magnet for the price in the short term, sitting neatly in the middle of the 2018 trading range. Technical traders will also be aware 14-day RSI has recently touched 30, signalling oversold, and has rebounded.

Strong results

The group boosted investor sentiment by raising its 2017 dividend by 20 percent at the start of the year, and announcing a £1 billion share buyback. In February the group reported relatively strong results, with statutory profit before tax up significantly to £5.3 billion, an increase of 24 percent on the year before. Underlying profit also increased by 8 percent to £8.5 billion, leading the group to boost its ordinary dividend per share by 20 percent. The banking group may also be set to benefit from a rising UK interest rate over the next couple of years. Despite it being expected to rise to just 2 percent by 2020, this would be an improvement on its current level and offer a boost to Lloyds.Contract tender

Lloyds has also gained the interest of several of the big investment management groups, after putting an investment contract up for tender. Goldman Sachs Asset Management joined rivals in the battle to win the £109 billion investment contract earlier this week, with BlackRock, JPMorgan Asset Management and Schroders all having already been selected to take part in a second round of bids in April. The contract is one of the largest ever to be put up for tender in Europe and has been managed by Standard Life Aberdeen since 2014.

Appscatter shares rise on maiden revenue report

App distribution platform Appscatter (LON:APPS) reported its maiden earnings on Thursday, after generating its first annual revenue.

The group, whose SaaS platform integrates with app stores to allow apps to maximise their distribution, reported full year revenues of £1.9 million. Its cash balance rose from £3.8 million to £226 million.

Net losses also narrowed throughout the year, dropping to £5.8 million in the year to the end of December, from £8.8 million the year previously. This comes after the group secured its first paying customers during the period, obtaining 16,835 registered users, by the end of May.

“Alongside investing in our core platform, we have also been successful in agreeing important partnerships with Airpush and IronSource, leaders in our industry who will broaden our horizons and increase our brand-awareness as we continue to focus on expanding our user base,” Philip Marcella, appScatter CEO.

Shares in Appscatter are currently trading up 2.56 percent at 60.00 (1059GMT).

How Reid Green & co generated a 75% return on Citigroup Inc

Sponsored by Reid Green & co

Citigroup Inc is a case study of an investment opportunity Reid Green & co highlighted to our subscribers. Over an 18 months period this idea generated a 75% return.

In this case study we will cover why we found the company attractive, what happened after we covered the stock and how Reid Green & Co approaches the investment problem.

What was it about Citigroup Inc that made Reid Green & Co rate it a buy a $43.15 per share and a sell at $74.05 per share?

What was it about Citigroup Inc that made Reid Green & Co rate it a buy a $43.15 per share and a sell at $74.05 per share?

Citigroup Inc. (Citi) is a financial services holding company. The Company’s whose businesses provide consumers, corporations, governments and institutions with a range of financial products and services, including consumer banking and credit, corporate and investment banking, securities brokerage, trade and securities services and wealth management. In 2016 due to a negative sentiment in the banking sector related to banks’ exposure to commodities which were in the doldrums at the time, Citigroup found itself trading at a 30% discount to its tangible equity and at more than a 40% discount to its reported book value. Some of the discount was also part of a punishment for Citigroup appearing to generate a meagre 8% return on its equity, meanwhile Reid Green & Co thought the correct to look at Citigroup equity was the same way the banking regulators look at their equity. Upon looking at the company’s regulatory equity, which as must lower than its stated equity, we concluded than compared to Citigroup’s earnings it was actually earning closer to 11% of its true equity and factoring the discount this set up an attractive investment situation. An excerpt of what we told our subscribers can be seen below: “However, we think Citigroup’s compliance with US GAAP accounting standards is masking the banks much higher return on equity, as items such preferred stock, deferred tax assets, goodwill and intangible assets bloats the banks equity. When you deduct the $16 billion in outstanding preferred stock and $25.5 billion in intangible assets from the company’s equity, you realise that the bank’s tangible equity is actually $179.5billion or $60.77 per share, which would indicate a return on tangible equity of 9.4%. In spite of the above, the regulators actually have an even more nuanced view on the banks equity, one that we think gets closer to revealing the banks true economic performance. In assessing the banks regulatory equity, not only do the regulators deduct the preferred equity and intangibles, but they also subtract $32 billion of the Citi’s deferred tax assets. This results in $147 billion in regulatory equity or $50per share and when compared to its 2015 net income results in an 11.5% return on equity. This is 50% higher than the headline numbers would suggest. In summary our basic valuation takes into account the fact that the bank generates an 11% return on equity, is well capitalised with 12% in regulatory equity, is growing its core lending business, has $30 billion deferred tax assets which allows it to earn $100 billion of tax-free profits, and its excess earnings either gets returned to shareholder via buybacks or increases the company’s tangible equity.What happen after Reid Green & Co covered the stock?

During October 2017 Citigroup announced: In the first three quarters of the 2017 financial year ended 30 sept Citigroup Inc:- Increased its tangible book value to $68 per share up 13% from $60 in 2015.

- Increased its common equity from 8.7% in 2012 to 13%

- Repurchased 140 million common shares and returned $10.8 billion to shareholders

- Maintained a 9% return on tangible capital and 11% return on regulatory capital