Tesla shareholders approve new “staggering” pay deal

The founder of Tesla (NASDAQ: TSLA) has had new approval for a new pay deal that could land him a bonus worth $55.8 billion (£40 billion).

Corporate governance experts have called the new pay deal “staggering” but it met approval from shareholders in California.

Elon Musk, who is the billionaire founder of the electric car company, must build the group into a $650 billion over the next decade. Tesla is currently worth $54.6 billion.

“Elon will receive no guaranteed compensation of any kind – no salary, no cash bonuses, and no equity that vests by the passage of time,” said Tesla.

“Instead, Elon’s only compensation will be a 100 percent at-risk performance award, which ensures that he will be compensated only if Tesla and all of our stockholders do extraordinarily well,” the group added.

Corporate governance group Institutional Shareholder Services did not agree with the shareholders’ approval of the deal and was strongly against the new plan, which will start in January.

Institutional Shareholder Services said that it will “lock in unprecedented high-pay opportunities for the next decade, and seemingly limits the board’s ability to meaningfully adjust future pay levels in the event of unforeseen events or changes in either performance or strategic focus.”

Shares in Tesla are down 18 percent from the year high the group reached in September.

Tesla has faced recent pressures including production delays and increasing competition.

Investors have also expressed concern that Musk is distracted by too many other projects including his SpaceX rocket launches – a reason shareholders may have voted in favour of the new pay plan.

Following Facebook’s data breach, Musk deleted the official Facebook pages for his Tesla and SpaceX companies.

Musk took to Twitter (NYSE: TWTR) to say he “didn’t realise” that his SpaceX brand had a Facebook page. “Literally never seen it even once,” he wrote. “Will be gone soon.”

Car sales set to plunge in 2018

Car sales in the UK are predicted to slide this year, adding to worries over a slowdown in consumer spending.

New car registrations may fall by up to 5.5 percent during the course of 2018, according to ratings agency Moody’s. The falling value of the pound since the EU referendum has had a negative effect on the market, making imported cars more expensive for UK consumers. It also said Brexit-related uncertainty was “weighing on consumer spending decisions”.

The figures are in stark contrast to those of Germany, Spain, France and Italy, which are all expected to see gains. According to Moody’s, the UK market is likely to be the “worst performing” market of any big European economy.

The industry has seen impressive growth of late, with a record 2.7 million new car registrations in the UK in 2016 according to SMMT figures. However the figures took a plunge last year, falling 5.7 percent as consumers began to spend less and avoid big diesel vehicles.

Facebook value plummets $58bn following drop in shares

Following the company’s data breach scandal, Facebook (NASDAQ: FB) saw the end of the week with a $58 billion drop in value.

After founder Mark Zuckerberg apologised for the data breach, which affected 50 million users, shares in the group fell from $176.80 on Monday to $159.30 on Friday.

Laith Khalaf, a senior analyst at Hargreaves Lansdown, has said that the controversy has been a “damaging episode” for the tech giant.

“One of the secrets of Facebook’s success has been that the more people who use Facebook, the more integral it becomes to its customers. Unfortunately for Facebook, the same dynamic cuts in the opposite direction if it loses a meaningful number of users as a result of this scandal,” he added.

The backlash for the tech giant has been widespread, with Elon Musk deleting the Facebook pages for his companies Telsa (NASDAQ: TSLA) and Space X in the spread of the #deletefacebook movement.

Since the data breach came to light, Zuckerberg has taken out full-page adverts in UK and US Sunday newspapers to apologise.

In the US, the ads appeared in The New York Times (NYSE: NYT), The Washington Post, and The Wall Street Journal (OTCMKTS: WSCO).

In the UK, the apology appeared in the Sunday Telegraph, Sunday Times, Mail on Sunday, Observer, Sunday Mirror and Sunday Express.

“This was a breach of trust, and I am sorry,” it read.

“I’m sorry we didn’t do more at the time. We’re now taking steps to make sure this doesn’t happen again.”

“We’re also investigating every single app that had access to large amounts of data before we fixed this. We expect there are others,” the social media giant’s chief added.

Shares in Facebook were initially priced at $38 each in 2012, which steadily climbed to $190 by February this year.

Auto Trader runs on autopilot

Auto Trader is the largest car listing website in the UK and is one of the most profitable businesses in the FTSE All-Share index. The company listed in March 2015 at 235p and has made solid financial progress since then.

A business earning a high return on capital employed (ROCE) will inevitably attract new competitors. The only way, therefore, that a company can sustain a high return on capital is if it possesses competitive “moats.”

Auto Trader generated a return on capital employed (ROCE) of 59% in the year to March 2017. This means that every pound invested in the group – debt and equity – earned 59p of profit before interest and tax.

Most companies can only dream of generating a ROCE at this level with 15% considered attractive. Auto Trader has sustained a high ROCE on the back of two competitive moats: networks effects and a strong brand.

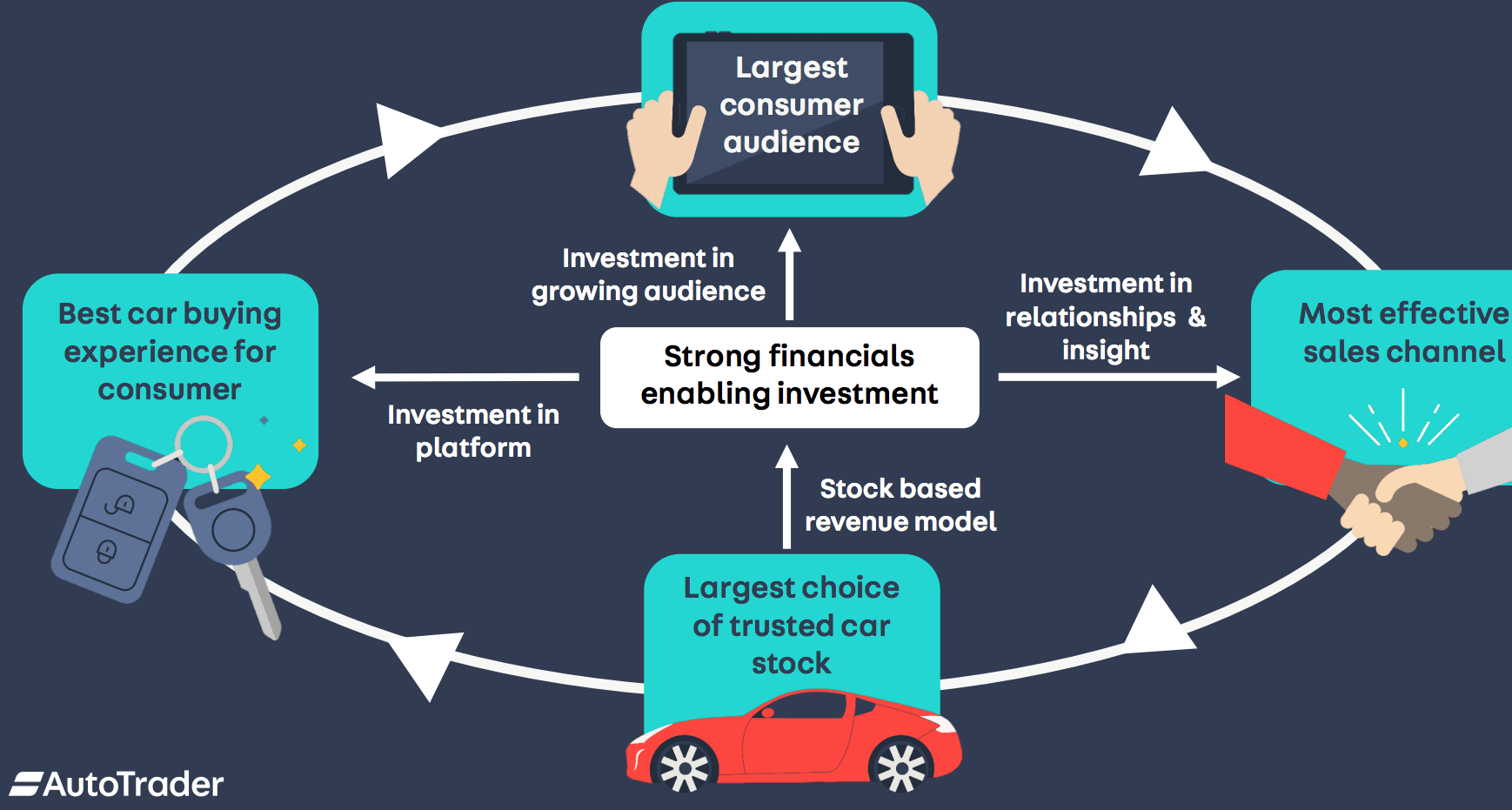

Auto Trader model & moats: network effects and a trusted brand

Source: Auto Trader investor presentation

Listing platforms generate Network effects because additional listings attract more users and additional users attract more listings. People gravitate to the leading listing platform and have little incentive to switch to move elsewhere.

Gumtree Motors is the nearest competitor to Auto Trader and is owned by US group eBay. In January 2018, UK car buyers spent 678 million minutes on Auto Trader’s platform versus 138 million minutes on Gumtree Motors.

Auto Trader also benefits from having a trusted brand, which is particularly important in the used car sector. According to research, only 7% of car buyers trust car dealers and 23% find visiting a car dealership “daunting.”

There is a risk that Amazon or Facebook could use their brands to make an aggressive move into the UK car listing market. Network effects, though, suggest that it would be hard to usurp Auto Trader’s market leading position.

The end market for Auto Trader is, however, mature with UK used car sales expected to decline 1-3% in 2018 to 7.9 million vehicles. This compares to 7.5 million in 2007, before the financial crisis, and 6.9 million used vehicles in 2009.

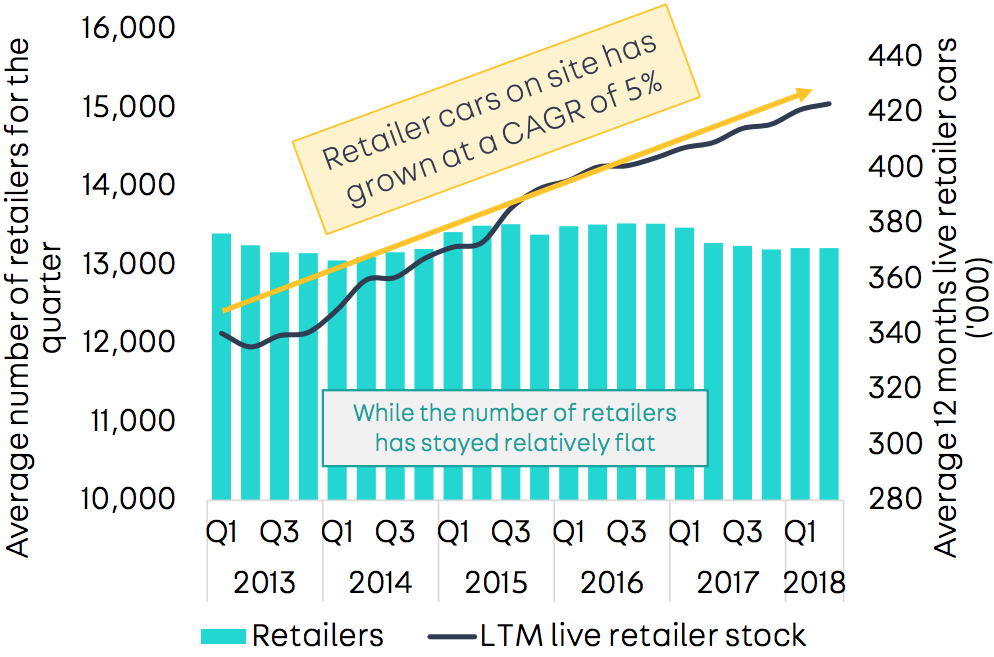

Retailers and last 12 months live cars on Auto Trader’s website

Source: Auto Trader

Physical stock on Auto Trader’s platform has grown 5% a year from 2013 with each car retailer listing more cars. In the six months to September 2017 there was a 3% year-on-year increase in vehicles on the platform to 451,000.

Auto Trader’s has seen solid top-line momentum recently with revenue up 8% in fiscal 2015, 10% in fiscal 2016 and by 9% in fiscal 2017. The operating profit margin has also improved from 57% in fiscal 2014 to 67% in fiscal 2017.

Turning to the balance sheet and the leverage ratio (net debt to EBITDA) declined to 1.55X at September 2017 versus 2.7X at September 2015. The company has been buying back shares since the IPO and looks set to continue doing so.

Auto Trader has delivered growth in a mature sector

Source: SharePad

When Auto Trader listed in March 2015 at 235p its forward P/E ratio stood at 18.3X. The forecast P/E ratio is currently 17.2X for the year to March 2019 and 15.5X for the year to March 2020 (using a share price of 340p).

Auto Trader is clearly a high quality business but the UK used car market is mature and cyclical. Revenue growth has been delivered on the back of increased listings per car retailer, new product offerings and price increases.

Disruption is a long-term risk with taxi apps like Uber, on-street car rental and autonomous vehicles reducing the need for car ownership. The independence that car ownership delivers, though, means that it is unlikely to disappear.

Disclosure: The writer does not currently hold shares in Auto Trader.

Source: Auto Trader investor presentation

Listing platforms generate Network effects because additional listings attract more users and additional users attract more listings. People gravitate to the leading listing platform and have little incentive to switch to move elsewhere.

Gumtree Motors is the nearest competitor to Auto Trader and is owned by US group eBay. In January 2018, UK car buyers spent 678 million minutes on Auto Trader’s platform versus 138 million minutes on Gumtree Motors.

Auto Trader also benefits from having a trusted brand, which is particularly important in the used car sector. According to research, only 7% of car buyers trust car dealers and 23% find visiting a car dealership “daunting.”

There is a risk that Amazon or Facebook could use their brands to make an aggressive move into the UK car listing market. Network effects, though, suggest that it would be hard to usurp Auto Trader’s market leading position.

The end market for Auto Trader is, however, mature with UK used car sales expected to decline 1-3% in 2018 to 7.9 million vehicles. This compares to 7.5 million in 2007, before the financial crisis, and 6.9 million used vehicles in 2009.

Retailers and last 12 months live cars on Auto Trader’s website

Source: Auto Trader

Physical stock on Auto Trader’s platform has grown 5% a year from 2013 with each car retailer listing more cars. In the six months to September 2017 there was a 3% year-on-year increase in vehicles on the platform to 451,000.

Auto Trader’s has seen solid top-line momentum recently with revenue up 8% in fiscal 2015, 10% in fiscal 2016 and by 9% in fiscal 2017. The operating profit margin has also improved from 57% in fiscal 2014 to 67% in fiscal 2017.

Turning to the balance sheet and the leverage ratio (net debt to EBITDA) declined to 1.55X at September 2017 versus 2.7X at September 2015. The company has been buying back shares since the IPO and looks set to continue doing so.

Auto Trader has delivered growth in a mature sector

Source: SharePad

When Auto Trader listed in March 2015 at 235p its forward P/E ratio stood at 18.3X. The forecast P/E ratio is currently 17.2X for the year to March 2019 and 15.5X for the year to March 2020 (using a share price of 340p).

Auto Trader is clearly a high quality business but the UK used car market is mature and cyclical. Revenue growth has been delivered on the back of increased listings per car retailer, new product offerings and price increases.

Disruption is a long-term risk with taxi apps like Uber, on-street car rental and autonomous vehicles reducing the need for car ownership. The independence that car ownership delivers, though, means that it is unlikely to disappear.

Disclosure: The writer does not currently hold shares in Auto Trader.

Source: Auto Trader investor presentation

Listing platforms generate Network effects because additional listings attract more users and additional users attract more listings. People gravitate to the leading listing platform and have little incentive to switch to move elsewhere.

Gumtree Motors is the nearest competitor to Auto Trader and is owned by US group eBay. In January 2018, UK car buyers spent 678 million minutes on Auto Trader’s platform versus 138 million minutes on Gumtree Motors.

Auto Trader also benefits from having a trusted brand, which is particularly important in the used car sector. According to research, only 7% of car buyers trust car dealers and 23% find visiting a car dealership “daunting.”

There is a risk that Amazon or Facebook could use their brands to make an aggressive move into the UK car listing market. Network effects, though, suggest that it would be hard to usurp Auto Trader’s market leading position.

The end market for Auto Trader is, however, mature with UK used car sales expected to decline 1-3% in 2018 to 7.9 million vehicles. This compares to 7.5 million in 2007, before the financial crisis, and 6.9 million used vehicles in 2009.

Retailers and last 12 months live cars on Auto Trader’s website

Source: Auto Trader investor presentation

Listing platforms generate Network effects because additional listings attract more users and additional users attract more listings. People gravitate to the leading listing platform and have little incentive to switch to move elsewhere.

Gumtree Motors is the nearest competitor to Auto Trader and is owned by US group eBay. In January 2018, UK car buyers spent 678 million minutes on Auto Trader’s platform versus 138 million minutes on Gumtree Motors.

Auto Trader also benefits from having a trusted brand, which is particularly important in the used car sector. According to research, only 7% of car buyers trust car dealers and 23% find visiting a car dealership “daunting.”

There is a risk that Amazon or Facebook could use their brands to make an aggressive move into the UK car listing market. Network effects, though, suggest that it would be hard to usurp Auto Trader’s market leading position.

The end market for Auto Trader is, however, mature with UK used car sales expected to decline 1-3% in 2018 to 7.9 million vehicles. This compares to 7.5 million in 2007, before the financial crisis, and 6.9 million used vehicles in 2009.

Retailers and last 12 months live cars on Auto Trader’s website

Source: Auto Trader

Physical stock on Auto Trader’s platform has grown 5% a year from 2013 with each car retailer listing more cars. In the six months to September 2017 there was a 3% year-on-year increase in vehicles on the platform to 451,000.

Auto Trader’s has seen solid top-line momentum recently with revenue up 8% in fiscal 2015, 10% in fiscal 2016 and by 9% in fiscal 2017. The operating profit margin has also improved from 57% in fiscal 2014 to 67% in fiscal 2017.

Turning to the balance sheet and the leverage ratio (net debt to EBITDA) declined to 1.55X at September 2017 versus 2.7X at September 2015. The company has been buying back shares since the IPO and looks set to continue doing so.

Auto Trader has delivered growth in a mature sector

Source: Auto Trader

Physical stock on Auto Trader’s platform has grown 5% a year from 2013 with each car retailer listing more cars. In the six months to September 2017 there was a 3% year-on-year increase in vehicles on the platform to 451,000.

Auto Trader’s has seen solid top-line momentum recently with revenue up 8% in fiscal 2015, 10% in fiscal 2016 and by 9% in fiscal 2017. The operating profit margin has also improved from 57% in fiscal 2014 to 67% in fiscal 2017.

Turning to the balance sheet and the leverage ratio (net debt to EBITDA) declined to 1.55X at September 2017 versus 2.7X at September 2015. The company has been buying back shares since the IPO and looks set to continue doing so.

Auto Trader has delivered growth in a mature sector

Source: SharePad

When Auto Trader listed in March 2015 at 235p its forward P/E ratio stood at 18.3X. The forecast P/E ratio is currently 17.2X for the year to March 2019 and 15.5X for the year to March 2020 (using a share price of 340p).

Auto Trader is clearly a high quality business but the UK used car market is mature and cyclical. Revenue growth has been delivered on the back of increased listings per car retailer, new product offerings and price increases.

Disruption is a long-term risk with taxi apps like Uber, on-street car rental and autonomous vehicles reducing the need for car ownership. The independence that car ownership delivers, though, means that it is unlikely to disappear.

Disclosure: The writer does not currently hold shares in Auto Trader.

Source: SharePad

When Auto Trader listed in March 2015 at 235p its forward P/E ratio stood at 18.3X. The forecast P/E ratio is currently 17.2X for the year to March 2019 and 15.5X for the year to March 2020 (using a share price of 340p).

Auto Trader is clearly a high quality business but the UK used car market is mature and cyclical. Revenue growth has been delivered on the back of increased listings per car retailer, new product offerings and price increases.

Disruption is a long-term risk with taxi apps like Uber, on-street car rental and autonomous vehicles reducing the need for car ownership. The independence that car ownership delivers, though, means that it is unlikely to disappear.

Disclosure: The writer does not currently hold shares in Auto Trader. House of Fraser funding talks fall apart

Concerns continue to mount over the future of retailer House of Fraser, after funding negotiation talks collapsed.

Department store House of Fraser is the latest in high street shops to feel the pinch in a difficult trading environment, amid stunted consumer spending and higher rents.

According to the Sunday Times, talks were held between the retailer and turnaround specialist Alteri Investors, a turnaround specialist.

However, the negotiations are understood to have failed to progress any further over debt concerns.

Specifically, House of Fraser is looking to refinance or extend the terms of £224 million in debt, which is set to be repaid in 2019.

A spokesman said: “House of Fraser is a privately-owned business. We have the full financial support of our shareholders.”

Back in 2014, the retailer was bought by Sandpower, which is owned by Chinese businessman Yuan Yafei.

In September it was revealed that Mr Yafei’s company injected £25 million in cash into the faltering department store, amid widening losses.

Since the acquisition, The high-street giant has sold off a portion of its brand names and intellectual property for £30 million, alongside identifying £26 million of annual cost savings, in a bid to turnaround its fortunes.

Fears are now mounting that House of Fraser may become the latest in collateral damage, following a string of high street closures, which have dominated the business news cycle in recent weeks.

Maplin and Toys R Us fell into administration last month, after both retailers failed to locate a buyer.

Similarly, restaurant owners in the U.K such as Cafe Rouge owner, Casual Dining Group, and Prezzo have announced the closure of hundreds of stores, in a bid to streamline costs.

Prezzo, which is owned by TPG Capital, announced on Friday the closure of some 94 restaurant locations.

As it stands, Debenhams has 59 stores across the U.K, employing some 6000 staff and an additional 11,500 concession workers.

Activist investors increase interest in Britain’s biggest firms

Barclays (LON:BARC) shares price shot up last week after it was announced that activist investor Edward Bramson would be taking a 5 percent stake in the bank, sparking rumours that the institution may be heading for a shake-up.

Whilst early indications suggest that Bramson doesn’t intend to be too much of an ‘activist’ with Barclays, the bank’s numbers show that it remains operationally and structurally inefficient. Given Bramson’s previous experience as an activist shareholder, it is likely that he is hoping to push for some changes to bolster Barclay’s performance.

Bramson’s company, Sherborne Investors (LON:SIGB), said it had invested £580 million in the bank’s shares and derivatives. With a regulatory disclosure said Sherborne owned 1.94 percent of the shares, controlling the remainder of its 5 percent stake through derivatives.

Bramson is just one of several activist investors advancing their interest in household names of late.

Earlier in March, American activist investor TCI increased pressure on the Altaba (NASDAQ:AABA) to wind down and sell off its $76 billion holding in China’s Alibaba. The shareholder said that the company, who own the legacy assets of internet group Yahoo, was trading at an unnecessarily large discount to the value of its assets and should “take advantage to recent US tax reform to liquidate.”

In the engineering sector, activist hedge fund Elliott Advisors has lent its support to Melrose in the bidding process for engineering giant GKN (LON:GKN). Elliott are one of the biggest shareholders in GKN currently and are campaigning for fellow shareholders to look kindly upon Melrose’ controversial offer. The investor also sent a letter to GKN’s board, saying it was “sceptical of the company’s ability to deliver on Project Boost for its aerospace business”.Instem shares rally after final results

Shares in Instem (LON:INS) ticked up on Monday, after the company reported a promising set of results for the financial year, alongside a significant extension to a contract deal.

The IT solutions provider posted a 19 percent increase in revenue to £21.7 million, compared to £11.7 million.

In addition, recurring revenues rose 9 percent to £12.8 million. Software as a service revenues increased 10 percent to £4.4 million.

The company also appointed a new chief operating officer, Ms. MaryBeth Thompson, to help oversee the business.

Moreover, the firm also announced a significant contract extension with respect to its SEND platform.

The deal has been extended by US$400,000 to US$500,000, in a boost to profits.

Phil Reason, CEO of Instem, said: “Instem products and services now address aspects of the entire drug development value chain, from discovery through to market launch, and are currently deployed by over 500 companies, including all of the largest 25 pharmaceutical companies in the world. Management estimate that over 50% of all drugs on the market have been through some part of the Group’s platform at some stage of their development.”

“While new software license revenue was particularly strong in 2017, we also focused on opportunities to increase SaaS revenues and were very pleased to deliver an increase of over 10% during 2017, with both new SaaS customers and existing clients switching from on-premise to SaaS deployment.”

He continued: “The current financial year has started strongly with the largest S outsourced services contract win to date and one of the world’s largest chemical products companies converting to the Company’s market leading SaaS delivery model”

Looking ahead, Mr Reason remained optimistic of future growth prospects, he added:

“The Board therefore looks forward to the coming year and beyond with increasing optimism on the back of an enhanced delivery platform, which promises to deliver significant revenue growth, enhanced profitability and improved quality of earnings.”

Shares in the company are currently trading up 19.89 percent as of 10.10AM (GMT).

JD Sports shares rise on Finish Line acquisition

Shares in JD Sports (LON:JD) climbed over 3 percent on Monday, after investors showed their approval of the group’s acquisition of US athletic footwear company Finish Line.

Finish Line is listed on the NASDAQ stock exchange with a market capitalisation of approximately $425 million, and has 556 stores in the US. It also has 188 unbranded concessions in Macy’s stores and employs 3,700 full-time and 9,300 part-time staff.

Peter Cowgill, JD Sports’ executive chairman, commented: “Finish Line has many similarities to JD with a strong bricks and mortar offering complemented by an advanced and well-invested digital platform.”

He said: “This is a landmark day for JD and will be transformational for the business.”

In a statement, the company said the acquisition offers the Company the opportunity to expand its market leading elevated proposition into the most significant global market, immediately gaining the benefit of a significant physical and online retail presence and increases the importance of the company to its major international brand partners.

Shares in JD Sports are currently up 3.15 percent at 367.00 (0954GMT).

Speedy Hire shares soar after another profit guidance upgrade

Speedy Hire (LON:SDY) shares soared on Monday after the group upgraded their profit guidance and reported an increase in revenue.

The tools and equipment hire company Speedy Hire said adjusted pre-tax profits were expected to be ahead of its previous expectations and that revenue had grown by 6 percent.

The increase was driven by a renewed focus on small business customers, the company said, with the return on capital employed for the year expected to be around 11 percent, up from 7.7 percent the year before, amid a continued reduction in the size of the group’s fleet.

Net debt at 31 March was expected to be approximately £80m after expenditure of £23 million on acquisitions.

The announcement comes after a similar one was made in September, telling investors to expect higher profits than initially anticipated.

Shares in Speedy Hire are currently trading up 7.41 percent at 51.88 (0916GMT).

Inchcape shares rise on Grupo Rudelman acquisition

Inchcape (LON:INCH) announced the acquisition of Central American automotive retailer Grupo Rudelman on Monday, sending shares up 1.2 percent.

The group confirmed it had offered $284 million for the retailer on a cash-free and debt-free basis. The acquisition is expected to boost Inchcape’s earnings in first full year post-acquisition by mid-single digit percentage, as well as increase their presence in Central America. Grupo Rudelman is the distributor and exclusive retailer for Suzuki in both Costa Rica and Panama.

Stefan Bomhard, Group CEO of Inchcape plc, applauded the acquisition for highlighting the group’s “commitment to investing for growth and allocating capital in a disciplined manner.”

“We are acquiring a strong, well-managed business and I am very pleased to welcome the Grupo Rudelman team to Inchcape. I am delighted to significantly enhance our relationship with Suzuki, a brand that is well positioned for growth and success in emerging markets, with whom we are proud to have partnered for over 40 years.

“With this acquisition we continue to actively position Inchcape towards higher growth markets and higher return Distribution businesses. Distribution trading profit, on a pro forma basis, now equates to 81 percent of total Group profit in 2017. In addition, Inchcape’s portfolio and presence in Latin America has been significantly strengthened, and I am excited about the future opportunities this presents.”

Shares in Inchcape are currently up 1.27 percent at 680.00 (0853GMT).