Broadcast technology supplier Pebble Beach Systems (LON: PEB) increased interim revenues by 13% to £5.9m and margins have improved due to cost cutting. Order intake was one-third higher. Cavendish has raised its full year pre-tax profit forecast from £1.9m to £2.4m on maintained expected revenues of £11.5m. The share price rebounded 52.8% to 13.75p.

Telematics services provider Quartix Technologies (LON: QTX) reported interim in line with the recent trading statement. Revenues were 10% ahead at £17.6m and pre-tax profit was 36% ahead at £3.6m. Zeus has upgraded for the third time this year. The new 2025 pre-tax profit forecast is £7.1m. The share price increased 8.16% to 265p.

EnergyPathways (LON: EPP) has engaged Costain to assess onshore facility options for the MESH project in the North Sea. The share price improved 7.61% to 4.95p.

Payments services provider Boku (LON: BOKU) increased interim revenues by one-third to at least $63m, with the fastest growth coming from digital wallets. There was also the benefit of higher pricing for a client during a launch phase. Stripping that out, the growth was 27%. Own cash was 16% higher at $87m. Full year pre-tax profit is expected to be $33.8m. The share price rose 6.97% to 222.5p.

Floorcoverings manufacturer Victoria (LON: VCP) reported full year results ahead of expectations. In the year to March 2025, revenues fell from £1.23bn to £1.12bn. There were declines in all regions. Gross margins have started to recover, but underlying operating profit fell from £73m to £29.5m. That is before £255m of one-off write downs and costs. A modest improvement in profit on flat revenues is anticipated this year. Net debt was £1.18bn at the end of March 2025. Senior secured debt is being refinanced so that the maturity extends to 2029, although the interest rate will be raised. The share price improved 1.29% to 74.55p, although it was near to 85p earlier in the day.

FALLERS

Judges Scientific (LON: JDG) says organic growth of interim revenues was 7%, helped by a Geotek coring contract. However, profit has declined because of US government cuts to research funding. There were also problems with other businesses. Full year earnings guidance is between 285p and 330p/share, compared with previous expectations of more than 360p/share. The share price slumped 16.2% to 6620p.

South American mining company Nativo Resources (LON: NTVO) says delays in receiving shareholder approval for bond restructuring plans means that it is technically in default. The adjourned shareholder meeting, which was not previously quorate, will be held on 30 July. Nativo Resources intends to have a digital asset treasury policy so that a portion of cash generated will be used to acquire Bitcoin. The share price slipped 9.09% to 0.25p.

IT services provider SysGroup (LON: SYS) reported a 10% drop in revenues in the year to March 2025 due to weaker hosting services income and the shedding of lower margin work. Pre-tax profit declined by two-thirds to £300,000. Customers are delaying spending on projects. Zeus has cut its 2025-26 pre-tax profit forecast from £1.3m to £400,000 due to lower revenues and margins. The share price dipped 7.5% to 18.5p.

GEO Exploration (LON: GEO) has completed the electrical geophysical programmes at the Juno project and this has upgraded the project on an IRGS perspective. Maiden drilling will start by the end of September. The share price declined 5.26% to 0.18p.

Ex-dividends

Celebrus Technologies (LON: CLBS) is paying a final dividend of 2.32p/share and the share price slipped 2.5p to 175p.

Calnex Solutions (LON: CLX) is paying a final dividend of 0.62p/share and the share price is unchanged at 49.2p.

Creightons (LON: CRL) is paying a final dividend of 0.5p/share and the share price fell 1p to 35.5p.

Facilities by ADF (LON: ADF) is paying a final dividend of 0.9p/share and the share price declined 0.5p to 21p.

Synectics (LON: SNX) is paying an interim dividend of 2.2p/share and the share price dipped 5p to 310p.

Touchstar (LON: TST) is paying a final dividend of 1.5p/share and the share price is unchanged at 90.5p.

M Winkworth (LON: WINK) is paying a dividend of 3.3p/share and the share price is unchanged at 208p.

IG has become the first platform globally to offer daily options on Tesla shares, introducing zero days to expiry (0DTE) contracts that provide traders with unprecedented flexibility for short-term positioning.

The innovative product, exclusive to IG and unavailable on any global exchange, including those in the United States, allows traders to trade the daily volatility in Tesla shares. The contracts settle at the US market close, enabling intraday risk management in a way that isn’t available anywhere else.

The launch addresses growing demand in the derivatives market, where daily options have gained significant traction. In the US, 0DTE index options now represent over 50% of total daily options volume, yet no provider has previously offered this structure for individual equities.

IG’s UK client base has demonstrated strong appetite for options trading, with activity increasing 27% year-on-year alongside a 9% rise in active options traders. The figures reflect broader market interest in sophisticated trading instruments that offer precise risk management capabilities.

Elliot Harris, Head of Options at IG, said: “We’re proud to be the first in the world to offer daily expiring Tesla options, giving our clients unmatched flexibility and speed. These contracts are a powerful new tool for short-term traders looking to capitalise on Tesla’s intraday price swings, which in recent times have been pretty dramatic.

“This is one of the fastest-growing areas in global trading, and we want to be at the forefront – driving innovation and giving our clients the tools they’re asking for. Daily Tesla options are just the beginning. We’re here to push boundaries and lead the way in delivering smarter, faster trading solutions.”

Available through spread betting and contracts for difference (CFDs) on IG’s platform and mobile application, the daily Tesla options will trade Monday through Thursday. Friday trading remains unavailable due to existing weekly options contracts on that day.

IG confirmed plans to extend daily options to additional major US equities in the near term, building on this pioneering launch in the individual stock options market.

The FTSE 100 soared to another intraday record high on Thursday as investors reacted to reports the US and EU were nearing a trade deal, and strong corporate results gave investors plenty of reason for cheer.

London’s leading index was 0.8% higher at 9,137 at the time of writing and was on the track for yet another all-time closing high.

Hot on the heels of a Japan-US trade deal, the EU appears to be the next in line for an agreement that would significantly alleviate investors’ concerns about 1 August tariff deadlines.

“European shares marched higher on Thursday as the positive sentiment generated by the trade deal agreed between the US and Japan continued to permeate the markets,” said AJ Bell investment director Russ Mould.

“The continued momentum came despite a mixed start to the big tech earnings season across the Atlantic as Alphabet and Tesla posted their numbers after hours, with some well-received corporate results helping support UK stocks as the FTSE 100 sailed through the 9,100 barrier.”

The corporate results mentioned by Mould were indeed very well-received.

Reckitt Benckiser soars

Reckitt Benckiser shares soared 9% on an upgrade to like for like sales growth guidance for their ‘Core Reckitt’ portfolio to ‘over 4%’ from ‘3% – 4%’. It’s the first piece of materially positive news Reckitt’s investors have had for some time.

“Kris Licht has donned his marigolds and got out the mop and bucket in an attempt to clean up the mess at consumer goods giant Reckitt. First-half results have got the market believing in his recovery plan,” Russ Mould said.

“Having recently announced the sale of its Essential Home portfolio, the company has now issued an eye-catching upgrade to revenue guidance for its core brands.

“The merits of focusing on its ‘Powerbrands’ is evident in the numbers with them delivering meaningful growth at a strong margin while the Essential Home component is finding life harder going.”

Howden Joinery

Howden Joinery was the FTSE 100’s top riser after reporting sales growth of 3.2% which represented an acceleration from the growth rate reported in the early stages of 2025.

“Howdens performed well in the first half, gaining further market share. The ongoing investment in our strategic initiatives is strengthening our competitive position, and our current trading performance gives us confidence in achieving our full year plans,” said Andrew Livingston, Howden’s CEO.

“We are well prepared for the second half, which includes our seasonally important peak trading period. This includes Howdens’ best-ever line-up for kitchens, available for 2025 in more colours, styles, and finishes to suit all budgets.”

Howdens shares were 9.8% higher at the time of writing.

BT shares rose 5% after the company reported improving Q1 results, punctuated by rising customer numbers.

Lloyds shares were little changed after reporting robust half-year results against the backdrop of a looming Supreme Court ruling on motor financing. The banking group enjoyed the impact of higher interest rates, with net interest margins increasing 10bps to 3.04%. Profit beat expectations but the nagging doubt of motor finance redress kept shares in check on Thursday.

“Lloyds’ 2Q 15% pre-tax profit beat on strong revenue momentum, deposit flow and provision reversals, could (together with reiterated guidance) drive modest consensus upgrades,” said Tomasz Noetzel, Senior Equity Analyst at Bloomberg Intelligence.

“However, narrowing the gap between consensus’ 12% ROTE in 2025 and the bank’s 13.5% view remains subject to a Supreme Court ruling on the UK motor loan probe due end-July and regulatory redress decisions. Lloyds didn’t set aside additional provisions for these loans in 1H, with consensus projecting £1 billion this year.”

Tekcapital has announced that its portfolio company Guident Corp has secured a new business agreement with Coastal Waste & Recycling Inc, a leading waste and recycling services provider operating across Florida, Georgia and South Carolina.

Today’s announcement strengthens Guident’s preparations for its NASDAQ IPO with another use case and additional customer.

The agreement will see Guident deploy its WatchBot™ solution across Coastal Waste & Recycling’s operations, providing autonomous patrols, AI-driven inspections and real-time safety alerts.

The WatchBot™ platform will handle thermal inspections, truck damage detection, PPE compliance monitoring and tank cage checks at Coastal Waste & Recycling facilities. The company expects the AI technology to deliver significant improvements in operational safety, risk mitigation and cost efficiency.

“This partnership exemplifies the remarkable teamwork between our organizations and demonstrates our shared commitment to safety and operational excellence. By combining our expertise with Coastal’s dedication to innovation, we’re setting a new benchmark for technology-driven safety in the waste and recycling industry,” said Harald Braun, Chairman & CEO of Guident.

“The collaboration between Guident and Coastal Waste & Recycling highlights the companies’ mutual focus on leveraging next-generation technology to drive meaningful improvements in workplace safety, operational efficiency, and overall business performance.”

Today’s Coastal Waste & Recycling deal adds to a growing list of deployments, which include a pilot autonomous shuttle service in West Palm Beach, covered by NBC News this week.

Tekcapital announced earlier this year that Guident had filed confidentially for a NASDAQ listing. Investors are eagerly awaiting further updates.

Lloyds shares were broadly flat on Thursday after the group reported profits that beat expectations but kept guidance unchanged.

Lloyds shares are up 40% year-to-date, and investors would have required an overwhelmingly strong set of half-year results to have the confidence to push shares higher.

The first half’s financial performance was steady, as opposed to a blowout, with Lloyds posting a statutory profit after tax of £2.5 billion, up from £2.4 billion in the same period last year.

The banking giant achieved a respectable return on tangible equity of 14.1%, underpinned by net income growth of 6% year-on-year.

“Lloyds is trotting along nicely as profits gallop past expectations. The reaction might be a little muted, though, given the lack of guidance upgrade off the back of a good set of numbers,” said Matt Britzman, senior equity analyst, Hargreaves Lansdown.

“Impairments continue to be the fuel sustaining these profit beats as default rates remain low and borrowers continue to show resilience.

“Lloyds offers a blend of strong underlying performance and potential upside for those willing to take on some risk. It’s an important period, not just because of today’s results, but also because the Supreme Court is expected to make a judgment on the motor finance case soon.”

The looming motor financing decision may have contributed to Lloyds’ shares’ tepid reaction to otherwise strong results, with Lloyds shares down marginally at the time of writing.

The group’s underlying net interest income rose 5% to £6.7 billion, driven by an improved banking net interest margin of 3.04% – up 10 basis points year-on-year. This was supported by higher average interest-earning banking assets of £458 billion.

However, profitability faced headwinds from rising costs and credit provisions. Operating costs increased 4% to £4.9 billion, reflecting inflationary pressures and strategic investments, though these were partially offset by cost savings measures. The group also recorded an underlying impairment charge of £442 million, up from £100 million in the same period a year ago.

Strong underlying performance provided Lloyds with the opportunity to hike the dividend and investors will be pleased to see the interim dividend increasing 15%.

Analysts point to the macroenvironment as the next big driver of Lloyds’ share price performance with the UK economy starting to show signs of stress.

“Our experts suggest that future results are strongly linked to the British economy, so if the British economy does well, Lloyds should do well,” said Max Harper, Analyst at Third Bridge.

“The Bank of England’s current stable interest rate policy is unlikely to significantly impact Lloyds’ dynamic hedging strategy, the primary risk for the bank is stagflation. A combination of a slowing economy and persistently high inflation would create a double-edged sword effect, simultaneously reducing appetite for new lending while interest rate hikes aimed at curbing inflation could turn the bank’s hedge into a source of financial loss.”

Next Tuesday morning, 29th July, will see the Morgan Sindall Group (LON:MGNS) report its Interim Results to end-June this year.

We have already been given strong guidance by the Partnerships, Fit Out and Construction Services group, that its Management is anticipating that its full-year results for 2025 will be significantly ahead of its previous expectations.

It is a group of specialist businesses, delivering housing and mixed-use partnership schemes, fit out and construction services across the UK for the public, commercial and regulated sectors.

The Business

Th...

The FTSE 100 reached a record high on Wednesday after the US and Japan struck a trade deal, removing uncertainty surrounding one of the most significant US trade agreements for global growth and signalled a willingness for the US to make concessions to avoid the more damaging tariff rates.

London’s leading index touched a fresh record high of 9,080 and was trading very close to this level at the time of writing.

“News of a trade agreement between the US and Japan is fostering optimism among investors that further deals might be reached before punishing tariffs come into force,” explained AJ Bell investment director Russ Mould.

“The news helped drive the FTSE 100 to a new record high and saw gains in other markets across mainland Europe – with focus likely to now turn to the prospects of an agreement being forged between the Trump administration and EU.”

However, some analysts cautioned that while the markets reacted positively on Wednesday, the longer-term consequences of the trade deal may have ramifications for markets.

“At 15%, the US tariff on Japanese goods does not give much cause for long term celebration, despite the positive initial market reaction. Much higher product tariffs are not included in the deal,’ said George Lagarias, Chief Economist at Forvis Mazars.

“The number will still likely contribute to an increase of US inflation and put pressures on real growth for both countries. Why are the markets jubilant this morning? Because even a higher tariff is preferable to continued uncertainty. But this is hardly a catalyst for long term optimism. If the deal with Japan is the standard by which the negotiation with the EU will go, then investors and businesses should begin to price in a deterioration of the macroeconomic backdrop.”

Despite potential pitfalls down the line, most FTSE 100 shares were higher at the time of writing, with 73 of the 100 constituents trading in positive territory.

JD Sports was among the top risers as investors cheered the Japanese trade deal and what it could mean for other US trade deals more closely related to JD’s business model. JD Sport was one of the FTSE 100 stocks most heavily hit by Trump’s Liberation Day announcements.

The risk on tone to trade was underscored by weakness in defensive sectors. Centrica was the FTSE 100 top faller with a loss of 1.8% while SSE lost 1.7%.

Fresnillo fell around 1% after announcing silver production fell in Q2 due to the cessation of activities at a mine and lower ore grades.

“Fresnillo has made investors a lot of money this year thanks to soaring precious metal prices. Unfortunately, investors have now had a wake-up call that the day job still matters for the mining group,” Mould said.

“It has reported a big drop in second quarter silver production year-on-year, partially down to geological issues where the rock being mined contained lower grades of metal.

“Mining is high risk and often unpredictable, and anyone invested in this area needs to be aware of what could go wrong as well as what could go right.”

CPP Group (LON: CPP) is selling its business in India for £15.7m, of which £11.8m is payable on completion. The rest is dependent on performance. Tax could be £2m. This means that CPP can concentrate on the Blink InsurTech platform, focused on travel disruption and cybsersecurity. The cash will accelerate investment and fund the restructuring of the group to cut costs. Blink has annual recurring revenues of £1.6m. Net cash was £8.1m at the end of June 2025. The share price rebounded 21.7% to 157p.

Iron replacement treatment provider Shield Therapeutics (LON: STX) had a strong second quarter with revenues of $12.8m doubled the previous quarter. This means it is on track to reach cash flow positive by the end of the year. Cash was $10.8m at the end of June 2025. The share price recovered 15.5% to 4.1p.

Governance and compliance software provider Skillcast (LON: SKL) increased annual recurring revenues grew 22% to £12.7m. Interim revenues rose 18% to £7.5m and net cash has reached £11.5m. This could finance acquisitions activity. The share price improved 13.8% to 53.5p.

MyHealthChecked (LON: MHC) is partnering with Patients Know Best to give people the option to use its at-home blood and DNA tests and access results via the NHS app. The agreement lasts an initial three years. The share price rose 10.6% to 13p.

Caledonia Mining Corporation (LON: CMCL) says 2025 profit will be much higher than expected, helped by the strong gold price. The forecast was $86.7m, up from $51.6m last year. The second quarter was profitable, and 2025 production guidance was recently raised to 75,500-79,500 ounces of gold. The share price increased 8.59% to 1770p.

Plant-based detergent ingredients developer Itaconix (LON: ITX) reported record revenues of £4.8m in the first half of 2025. Panmure Gordon has reduced its 2025 forecast loss from $900,000 to $700,000. The share price is 7.45% to 137p.

FALLERS

K3 Business Technology (LON: KBT) bought back 34.1 million shares in a tender offer at 85p/share. Dealings on AIM end on 30 July. The share price fell 15.4% to 55p.

CyanConnode (LON: CYAN) reported full year results in line with expectations. Revenue fell from £18.7m to £14.2m due to delays in deployments of smart meters in India. Gross margins improved and operating costs were flat, so the loss fell from £4.2m to £3.7m. In the first quarter of the new financial year, there were 568,000 MESH modules shipped, compared with 1.26 million in the previous full year. The share price slipped 4.62% to 7.75p.

Thomas Moore, Manager, Aberdeen Equity Income Trust

UK equities have outperformed US equities in the first half of 2025, led by higher yield stocks

For many years, investor allocations to US equities have grown at the expense of UK equities

Even a small rotation out of the US and into the UK could make a meaningful difference to returns

Within UK equities, we observe that smaller cap stocks could be starting a resurgence, making this a rich hunting ground for investors who can invest across the UK market.

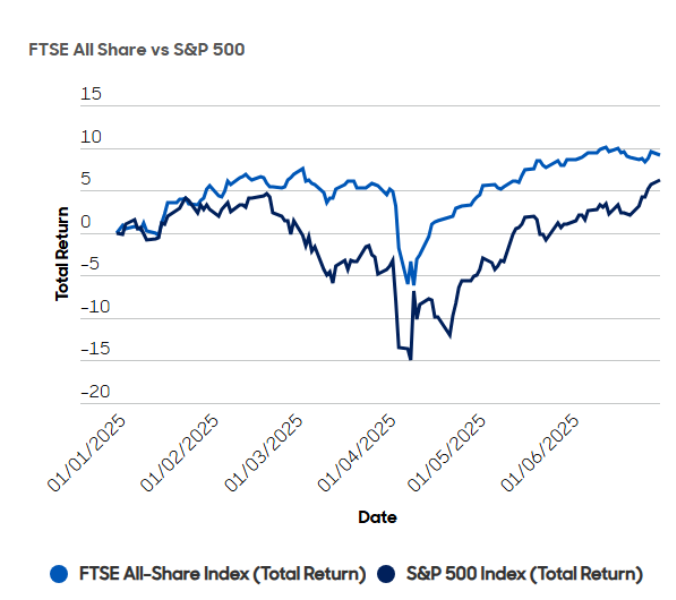

The resurgence in UK equities could come as quite a surprise for investors who have grown used to the dominance of US growth companies over the past decade. In the first 6 months of 2025, the FTSE All-Share index has delivered a total return of +9.1%, significantly outperforming the S&P 500 index delivered +6.2% in local currency terms. What’s even more surprising is that higher yield stocks have been leading the UK market. (Source: Bloomberg, 16 July 2025)

Our analysis shows that high dividend yield stocks have led the UK equity market over the first six months of the year, outperforming lower yield stocks and proving that dividends and capital growth can go hand in hand. Splitting the market into 5 equally weighted baskets, ranging from the highest yielding stocks to the lowest yielding stocks, a clear pattern emerges. The 2 highest yielding baskets, with an average yield of 5.9%, have generated a total return of +15.2%. In contrast, the 3 lower yielding baskets, with an average yield of 2.1%, have only managed to generate an average total return of +5.4%. (Source: Aberdeen, 1st July 2025)

Source: Bloomberg. For illustrative purposes only. No assumptions regarding future performance should be made.

Wavering sentiment towards US assets can be seen across a range of asset classes. The DXY index, which measures the performance of the US Dollar against a basket of other currencies, is down 10.7% in the first 6 months of 2025, breaking a long run of Dollar appreciation. Within the US equity market, the flagship ‘Magnificent 7’ technology companies are seeing their status questioned, removing one of the key pillars of support. Meanwhile US bond markets are also experiencing significant volatility on concerns over unsustainable pro-cyclical fiscal policies. Most recently, the “One Big Beautiful Bill” is creating a fiscal firestorm in the US, given concerns that it could add between $3 trillion and $5 trillion to the national debt over the next decade. In addition, investors are concerned by unpredictable policy making, in particular tariff policies, as well as institutional decay. All of this sits uneasily with the high valuations and heavy allocations to US equities.

The US has attracted a huge amount of investment from overseas investors in the past two decades. The US Bureau of Economic Analysis states that foreign ownership of US assets totals $62 trillion, far higher than the $36 trillion of overseas assets held by US owners. This makes the US the largest net debtor country in the world. To put these numbers into perspective, the FTSE All-Share (over 500 companies) totals $3.5 trillion. Another way of contextualising it is to consider that the market capitalisation of Apple, at $3.1 trillion (As at 16/07/25), is approximately the same as the whole UK market. What is clear is that it would not require a large shift out of US assets into the UK equity market for there to be a pronounced impact on share prices. UK stocks are cheap after years of weakness caused by macro concerns, but all the while, UK companies have been diligently taking action to improve their efficiency and grow their profits.

So, it’s against this backdrop that we believe that the current rotation out of US equities could have legs. Human beings tend to wait to see a trend develop before they start to feel the urgency to act on it. Investors have grown used to the US market delivering reliable, outsized returns. The weakness of the US Dollar also changes the calculation for non-US investors, exerting a further drag on returns. The trepidation starting to be felt by investors who are overly concentrated in US assets could become a catalyst for action.

There is also a strong case for increased diversification, particularly as some passive portfolios may have as much as 70% in the US. In the past, diversification meant selling UK equities to buy overseas equities, but investor allocations to UK equities have slumped over the past decade. As the reliability of US growth stocks fades, international and domestic investors could turn their attention to the UK.

The follow-on question for investors is what asset class they should consider rotating into. The strong performance of UK equities in the first half of 2025 might represent early evidence of a shift into UK equities. In a slow-growth world, every country has its fair share of challenges, but we see some emerging positives for the UK including the Government’s intention to make economic growth its number one priority, investing in infrastructure and defence, reforming planning controls and pushing through de-regulation of the Financial Services sector.

Within the UK equity market, we observe some interesting shifts going on beneath the surface:

First, income stocks are now doing all the running, with higher yield stocks outperforming lower yield stocks. High yield stocks have a natural appeal at a time of uncertainty. Rather than relying on unpredictable capital growth, investors can enjoy greater visibility of returns if they find stocks that offer dividend yields in excess of 6%, plus buybacks on top. The UK market has an abundance of companies that fulfil this brief.

Second, we are now seeing a shift in performance by size of company. Large cap stocks were first out of the blocks, as so often happens in early stages of a turnaround. Yet something interesting happened in April 2025 – smaller cap stocks started to outperform larger cap stocks.

Putting all of this together, we believe that this makes the UK a potentially rich hunting ground for income investors, particularly those who are willing to look all the way down the market cap spectrum. Our index-agnostic approach to income investing allows the Aberdeen Equity Income Trust to go anywhere, seeking out the best valuation opportunities across the market. This makes us poised and ready for this new era, as investors look to broaden out their allocations into small and mid-cap stocks.

Investors have always looked to the UK for dividend yield, but an improving corporate earnings backdrop can now enable dividend growth and capital growth to become a reality. This is why we see no compromise between the pursuit of income and capital.

Important information

Risk factors you should consider prior to investing:

The value of investments, and the income from them, can go down as well as up and investors may get back less than the amount invested.

Past performance is not a guide to future results.

Investment in the Company may not be appropriate for investors who plan to withdraw their money within 5 years.

The Company may borrow to finance further investment (gearing). The use of gearing is likely to lead to volatility in the Net Asset Value (NAV) meaning that any movement in the value of the company’s assets will result in a magnified movement in the NAV.

The Company may accumulate investment positions which represent more than normal trading volumes which may make it difficult to realise investments and may lead to volatility in the market price of the Company’s shares.

The Company may charge expenses to capital which may erode the capital value of the investment.

The Company invests in smaller companies which are likely to carry a higher degree of risk than larger companies.

Movements in exchange rates will impact on both the level of income received and the capital value of your investment.

There is no guarantee that the market price of the Company’s shares will fully reflect their underlying Net Asset Value.

As with all stock exchange investments the value of the Company’s shares purchased will immediately fall by the difference between the buying and selling prices, the bid-offer spread. If trading volumes fall, the bid-offer spread can widen.

Specialist funds which invest in small markets or sectors of industry are likely to be more volatile than more diversified trusts.

Yields are estimated figures and may fluctuate, there are no guarantees that future dividends will match or exceed historic dividends and certain investors may be subject to further tax on dividends.

Other important information:

The details contained here are for information purposes only and should not be considered as an offer, investment recommendation, or solicitation to deal in any investments or funds and does not constitute investment research, investment recommendation or investment advice in any jurisdiction. Any data contained herein which is attributed to a third party (“Third Party Data”) is the property of (a) third party supplier(s) (the “Owner”) and is licensed for use with Aberdeen. Third Party Data may not be copied or distributed. Third Party Data is provided “as is” and is not warranted to be accurate, complete or timely. To the extent permitted by applicable law, none of the Owner, Aberdeen, or any other third party (including any third party involved in providing and/or compiling Third Party Data) shall have any liability for Third Party Data or for any use made of Third Party Data. Neither the Owner nor any other third party sponsors, endorses or promotes the fund or product to which Third Party Data relates.

The Key Information Document for Aberdeen Equity Income Trust can be obtained here.

Issued by abrdn Fund Managers Limited, registered in England and Wales (740118) at 280 Bishopsgate, London EC2M 4AG. abrdn Investments Limited, registered in Scotland (No. 108419), 10 Queen’s Terrace, Aberdeen AB10 1XL. Both companies are authorised and regulated by the Financial Conduct Authority in the UK.

The Japanese Yen was slightly weaker against the dollar on Wednesday after the announcement of a 15% trade tariff on Japanese imports to the US.

The Yen had rallied against the dollar in the initial market reaction to the trade deal, but was quickly sold into by traders.

15% tariffs are significantly better than the previously touted 25% rate, but the muted reaction reflects the damage to trade between the US and Japan.

Stocks displayed the most enthusiasm for the trade deal, the Nikkei rallying around 3% overnight.

“Asian markets have rallied overnight, after the announcement of a trade deal between the US and Japan. The deal sees a 15% tariff imposed on all Japanese exports to the US. Traders reacted positively to the news, because President Trump had previously been threatening a 25% tariff,” said Steve Clayton, head of equity funds, Hargreaves Lansdown.

USD/JPY was 0.1% higher at the time of writing after the Yen strengthened against the dollar in the run-up to the deal.

The trade deal comes amid political uncertainties in Japan, with Prime Minister Ishiba suffering an election loss but vowing to remain in post.