As we move through 2026, the environment for US tech IPOs is heating up with some of the world’s most prominent technology companies preparing to go public.

From aerospace giants to artificial intelligence leaders, this year’s pipeline features companies at valuations that could reshape entire sectors.

Here are the most eagerly anticipated initial public offerings expected to hit the markets in 2026.

SpaceX

Est. IPO Valuation: >$1 Trillion Expected Timing: Q3-Q4 2026

SpaceX, founded by Elon Musk, has revolutionised the aerospace industry through its reusable rocket technology and ambitious satellite internet constellation, Starlink. The company provides commercial satellite launches, operates the world’s largest satellite broadband network, and is developing next-generation spacecraft for both cargo and crew missions to the International Space Station and beyond.

OpenAI

Est. IPO Valuation: $830 Billion – $1 Trillion Expected Timing: Late 2026/Early 2027

OpenAI has become synonymous with the artificial intelligence revolution through its groundbreaking ChatGPT chatbot and GPT language models. The company develops advanced AI systems designed to benefit humanity, offering enterprise AI solutions, research capabilities, and consumer-facing products that have transformed how millions of people work, create, and access information. The company completed a string a private rounds in late 2025 and will likely do so up until IPO. The valuation could be astronomical.

ByteDance

Est. IPO Valuation: $480-500 Billion Expected Timing: Considering 2026

ByteDance is the Chinese technology giant behind TikTok, the short-form video platform that has captivated a global audience of over one billion users. The company operates a portfolio of content platforms powered by sophisticated recommendation algorithms, including Douyin (TikTok’s Chinese counterpart), news aggregator Toutiao, and various other digital entertainment and information services.

Anthropic

Est. IPO Valuation: $350-$450 Billion Expected Timing: Preparing H2 2026

Anthropic is an AI company focused on building reliable, interpretable, and steerable AI systems, most notably its Claude family of large language models. Founded by former OpenAI researchers, the company emphasises constitutional AI principles and develops advanced AI assistants for both enterprise and consumer applications, whilst prioritising safety and alignment. Claude is popular for its coding capabilities and is attracting the interest of MircoSoft, Amazon, and Nvidia, who have participated in a recent fundraises, or are reported to be eyeing taking a stake in the near term.

Databricks

Est. IPO Valuation: $134-160 Billion Expected Timing: Likely Q1-Q2 2026

Databricks provides a unified data analytics platform that combines data warehousing and AI capabilities, enabling organisations to process and analyse massive datasets efficiently. The company’s lakehouse architecture helps enterprises break down data silos, streamline machine learning workflows, and derive actionable insights from their data across cloud environments.

Stripe

Est. IPO Valuation: $91.5-120 Billion Expected Timing: Signalled H1 2026

Stripe has built the financial infrastructure that powers commerce for millions of businesses worldwide, from startups to Fortune 500 companies. The company provides payment processing, fraud prevention, revenue management, and a comprehensive suite of financial tools that enable businesses to accept payments, manage subscriptions, and scale their operations across global markets.

Revolut

Est. IPO Valuation: $75-90 Billion Expected Timing: 2026 Target

Revolut is a digital banking platform offering a comprehensive range of financial services through its mobile-first app, serving over 40 million customers globally. The company provides current accounts, currency exchange, investment products, cryptocurrency trading, and business banking solutions, all designed to give users greater control and transparency over their finances.

Canva

Est. IPO Valuation: $50-56 Billion Expected Timing: Expected H2 2026

Canva has democratised graphic design through its intuitive, browser-based platform that enables anyone to create professional-quality visual content without design expertise. The company offers a vast library of templates, images, and design tools for creating everything from social media graphics to presentations and marketing materials, serving over 170 million users worldwide.

MicroSalt shares jumped on Monday after the low-sodium salt producer said 2025 sales exceeded management expectations and reaffirmed bumper revenue forecasts for 2026 and 2027.

The Tekcapital portfolio company announced that unaudited sales for the financial year ended 31 December 2025 reached $2.14 million, surpassing the board’s original target of $2.0 million and representing a 287% year-on-year increase from $745,000 in 2024.

MicroSalt shares were 9% higher at 51p at the time of writing.

The manufacturer of full-flavour natural salt containing approximately 50% less sodium said its B2B bulk business continues to advance, with strong growth driven by increased demand from its North American customer base.

Most interestingly for investors, the company projects sales of $7.0 million for 2026 based on current volume estimations and existing customer relationships, with revenue expected to exceed $15.0 million in 2027.

Although more is needed to understand margins as volumes scale significantly, MicroSalt’s current market cap of £29m will look very good value if these revenue forecasts are met.

Increased Volumes

MicroSalt highlighted continued momentum with Customer 3, one of the world’s largest food, soft drink, and snack manufacturers.

Following increased volume projections throughout 2025, a new product line is scheduled to launch in Q2 2026. The company has already delivered its first bulk order for this product to a specific end retailer of Customer 3, with further orders received on a broadly monthly basis, in line with management expectations.

“We are immensely proud to have exceeded Board expectations in 2025, delivering revenue growth of 287% compared to 2024,” said Rick Guiney, CEO of MicroSalt.

“This performance is a clear testament to the strength of our offering, the versatility of MicroSalt’s applications, and the successful execution of our strategy to build a sustainable and profitable organisation. Importantly, it reinforces our commitment to delivering healthier food alternatives globally while driving revenue growth and long-term value for our shareholders. Our final 2025 healthy servings totalled 830,735,462, providing clear evidence that MicroSalt is successfully delivering on its mission of enabling healthier foods by helping to reduce excess sodium consumption.

“We look forward to continuing our close collaboration with existing partners as we deepen relationships and expand our global reach. At the same time, we remain focused on establishing new partnerships that will support our next phase of growth. As we look ahead, we are confident in our ability to build on this momentum and continue strengthening the business for the benefit of both our customers and shareholders.”

Galantas Gold (LON: GAL) is acquiring 100% of the Andacollo Oro gold project in Chile. This is an open pit mine with a historical inferred mineral resource estimate of 5.06M ounce of gold. It has been in production in the past. The seller is owned by Galantas Gold executive Robert Sedgemore, so it is a related party deal. His company bought the mine from Dragones, whose former owner will receive payments of $27.5m in the four years to the end of 2029, as well as initially being issued 91.3 million Galantas Gold shares. Galantas Gold will assume $3m of debt and pay $1.5m to Robert Sedgemore. The share price jumped 185% to 18.5p.

Reabold Resources (LON: RBD) says that the Italian authorities have published the formal decree and positive decision on the small scale LNG development plan by 47.4% owned investee company LNEnergy Ltd for the project in Colle Santo. The share price rose 119% to 0.115p.

Shares in Malaysia-based e-commerce payment services provider Mobility One (LON: MBO) ae still rising and doubled on the week to 7p, having been as high as 12.25p. This follows conditional approval to carry on Islamic digital banking in Labuan in Malaysia.

CleanTech Lithium (LON: CTL) has applied for a Special Lithium Operating Contract for Laguna Verde in Chile. This means that the company can commercially produce lithium. The share price gained 59.8% to 9.75p.

FALLERS

In an update on the Barb Project in Manitoba, Canada, Gunsynd (LON: GUN) says field work is consistent with a structurally controlled orogenic gold system. However, none of the latest rock sample results produced grades of more than 1g/t gold. Funding of C$105,000 has been secured from the Manitoba Mineral Development Fund to help fund further exploration. Targeted exploration will enhance understanding of the project. The share price declined 30.3% to 0.115p.

Extended reality technology company Engage XR (LON: EXR) is still suffering from a tough market with contact delays and poor renewals. In 2025, revenues were €1.9m and net cash has fallen to €1.6m. Cash is being conserved and there are potential opportunities in education. Forecasts are under review. The share price dipped 26.3% to 0.35p.

Goldstone Resources(LON: GRL) operates the Homase gold mine in Ghana which produced 2,912 ounces of gold in 2025 and generated revenues of $10m. Heavy rainfall and inspections held back production. Avrage all-in sustaining cost was $2,781/ounce up until November and it is expected to be $2,500-$2,900/ounce in 2026. Production could reach 4,000 ounces this year. The share price decreased by one-quarter to 0.45p.

Geo Exploration (LON: GEO) is still falling following yesterday’s news that although maiden drill holes at the Juno project in Australia intersected gold and copper sulphide mineralisation, together with silver and zinc, it appears that the higher grade mineralisation could be to the south. The share price fell 24.7% to 0.1375p.

Quadrise (LON: QED) non-executive director Dilip Shah had sold 1,000 shares at 6.55p on 17 January 2025 and was transferred 35 million shares and not 34.16 million shares in December as previously announced. Because of his failure to comply with company share trading policy he has stepped down from the board. The share price increased 9.8% to 2.8p.

Pulsar Helium (LON: PLSR) says that the Jetstream #5 appraisal well at the Topaz project in Minnesota has encountered an additional pressurized gas influx at approximately 2,857 feet in depth. This new gas zone is estimated at around 1,292 psi, the highest recorded to date at Topaz. The drilling of the hole continues before moving to the next well. The share price improved 7.98% to 57.5p.

Biopesticides developer Eden Research (LON: EDN) has achieved a second regulatory authorisation this week with fungicide Novellus+ gaining approval in Chile. This is used in wine and table grapes to control grey mould (Botrytis cinerea) and powdery mildew (Uncinula necator). Earlier in the week Mevalone was granted approval in France to use on grapes to control downy and powdery mildew. The share price rose 8.2% to 3.3p.

FALLERS

Shareholders in Indus Gas (LON: INDI) voted in favour of leaving AIM and that will happen on 23 January. JP Jenkins will provide a matched bargains facility. The share price slumped 32.4% to 1.85p.

Galantas Gold (LON: GAL) has been hit by profit-taking after the jump following news that it is acquiring 100% of the Andacollo Oro gold project in Chile. The share price slipped 15.2%, but it has trebled over the week.

Sunrise Resources (LON: SRES) says that the option period for the sale of Hazen project without being exercised. Sunrise Resources will retain the project, which is non-core. The share price dipped 9.09% to 0.025p.

ValiRx (LON: VAL) has entered a nine-month, evaluation and material transfer agreement with The Royal Institute for the Advancement of Learning/McGill University and The Institute for Research in Immunology, and Cancer-Commercialization of Research in Canada. This will evaluate a RNA Helicase inhibitor. ValiRx will own the evaluation results, and they can be swapped for a 15% take in the company set up to commercialise the technology. The share price fell 4.88% to 0.39p.

(Analysis for informational purposes only. Capital at risk.)

Summary

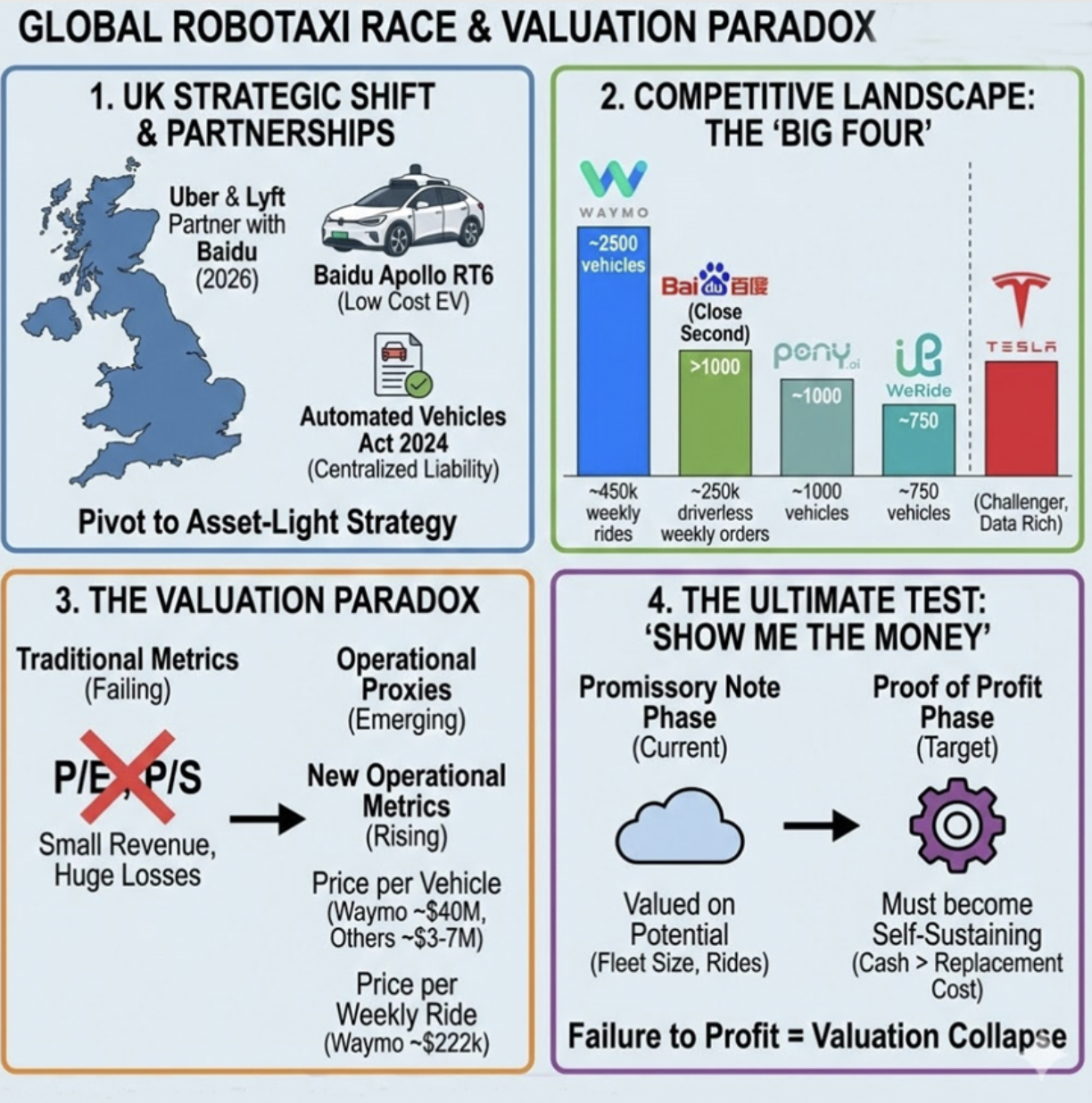

The Strategic Signal: Uber & Lyft’s 2026 Robotaxi partnership with Baidu in London underscores the competitiveness of Chinese low-cost autonomous driving solutions in the international market.

The Valuation Dislocation: At current levels, Baidu trades at a structural dislocation. Our Sum-of-the-Parts (SOTP) analysis implies the Apollo Robotaxi unit is effectively priced at ~7 cents on the dollar relative to Waymo’s private market benchmark.

The “Show me the money” Test: Ultimately, the sector is pivoting from “promise” to “profit.” Robotaxi platforms must pass the “show me the money” test by demonstrating sustainable unit economics to justify and sustain their valuations.

Uber, Lyft and Baidu signal a step‑change for UK robotaxi development

Uber and Lyft’s decision to partner with Chinese tech giant Baidu to test robotaxis in London in 2026 marks a major milestone for autonomous driving in the UK and an acceleration of Chinese autonomous driving expansion into Europe. The move follows Waymo’s recent entry into the UK market and suggests a wave of new entrants from 2026 onwards.

After earlier attempts to build in‑house autonomous driving systems, Uber and Lyft are now prioritising their core competency—network operations—while outsourcing vehicle autonomy to technology partners. Choosing Baidu rather than a U.S. supplier is notable given ongoing U.S.–China geopolitical tensions in technology and underscores the competitiveness of Chinese autonomous driving technology in the international market.

The ‘Regulatory Firewall”

While the partnership appears to be a technological and operational choice, it also serves as a risk-transfer mechanism that protects Uber’s and Lyft’s balance sheet under the UK’s Automated Vehicles Act 2024.

The Act shifts criminal and civil liability from the driver to the “Authorised Self-Driving Entity” (ASDE). Securing ASDE status requires significant capital reserves for insurance and safety validation. By partnering with Baidu, Uber and Lyft are constructing a “Regulatory Firewall”:

Baidu (The ASDE): Assumes the regulatory burden, insurance costs, and legal exposure as the manufacturer/operator.

Uber/Lyft (The Broker): Retains the customer relationship and booking fee while keeping the “crash risk” off their balance sheet.

This structure potentially allows the ride-hailing giants to remain asset-light and liability-remote, outsourcing the cost of UK regulatory compliance to Baidu. For Baidu, absorbing this liability is the strategic “cost of entry” required to deploy its RT6 fleet in Europe’s most valuable mobility market.

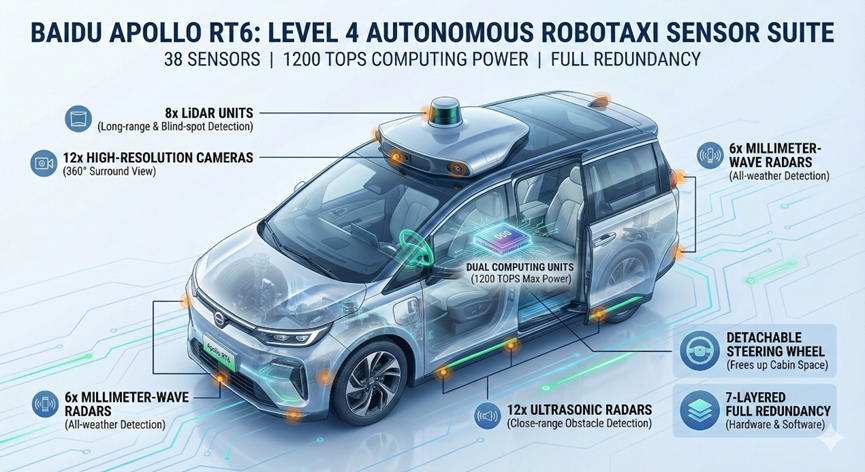

Baidu’s offering: Apollo RT6 and cost advantage

Baidu will deploy its Apollo RT6 — a purpose‑built EV for ride‑hailing — in the UK tests. The RT6 is equipped with 38 sensors, including eight LiDARs, and has an estimated cost of roughly £ 21k (CNY 200k), significantly lower than Western competitors like Waymo, which carries an estimated cost of over £80K.

Source: The company, AP

For Uber and Lyft, this effectively imports Chinese manufacturing deflation into the UK. Baidu has already achieved unit-economics breakeven in Wuhan. By utilizing an low-cost fleet, operators can achieve fleet profitability significantly faster than competitors burdened by high hardware cost.

Why the UK matters for L4?

The Automated Vehicles Act 2024 strengthens the UK’s position by shifting legal liability for Level‑4 (L4) autonomous operation from the user to the manufacturer once safety cases are approve1d, and by allowing scaling once regulators are satisfied. This single‑act approach also provides a more centralised, predictable framework than the more fragmented regulatory regimes in some EU countries, such as France and Germany.

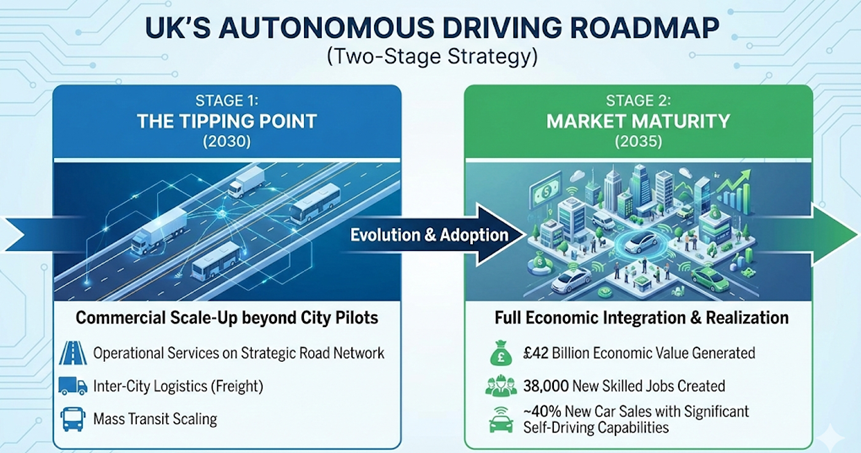

UK’s Autonomous Driving Roadmap

The UK government has established a long-term autonomous driving strategy anchored by 2035 targets, while the broader industry generally views 2030 as the “tipping point” leading up to that goal.

2030: Commercial self-driving services operational across the UK’s Strategic Road Network, moving beyond isolated city pilots to inter-city logistics and mass transit.

2035: The UK connected and automated mobility (CAM) sector is projected to generate £42bn in economic value and create 38,000 skilled jobs, with roughly 40% of new car sales expected to feature significant self-driving capabilities.

Source: UK government policy papers, SMMT, Frost & Sullivan

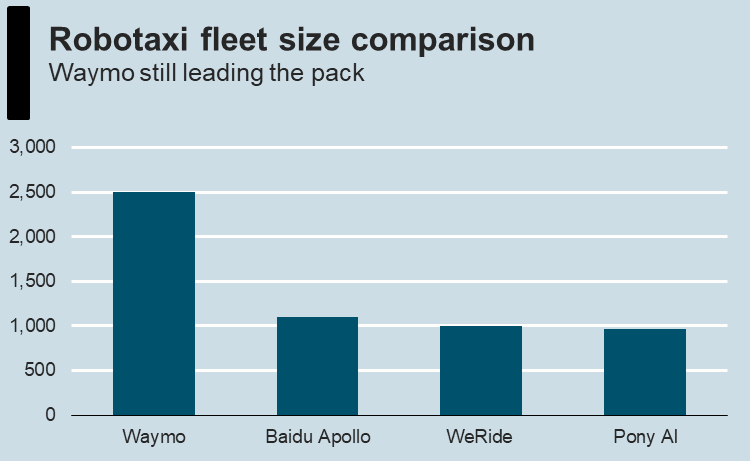

The “Big Four” in L4 autonomous driving

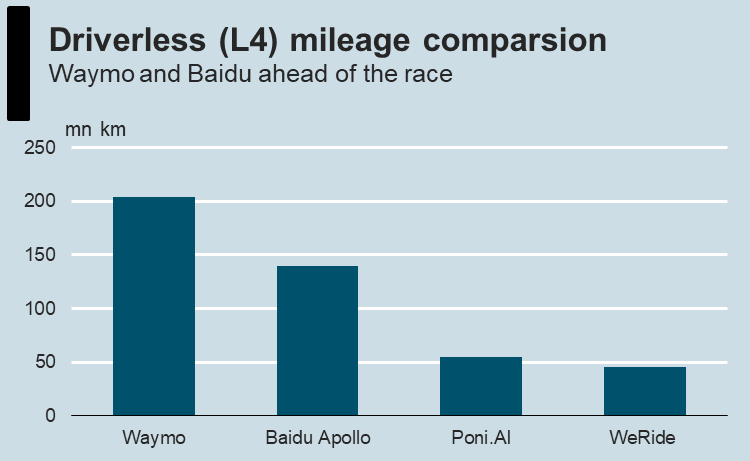

We identify four leading L4 players: Waymo (Alphabet), Baidu (BIDU / 9888.HK), Pony AI (PONY US/2026 HK), and WeRide (WRD US/800 HK). Waymo remains the leader in fleet size and driverless mileage, with Baidu a close second. Pony AI and WeRide are smaller individually, but collectively Chinese players operate at a comparable scale to Waymo.

Waymo: fleet ~2,500 vehicles, ~204m km driverless mileage, ~450k paid rides per week, ~20m km of total robotaxi rides in the U.S. Waymo’s vehicles (e.g., Jaguar, Zeekr models) are materially more expensive on a per‑vehicle basis than Baidu’s RT6.

Baidu: About 240m km of AV testing, of which 140m km were driverless. Apollo Go reportedly operates over 1,000 robotaxis, has completed over 17m rides, and now fulfills approximately 250k fully driverless orders per week.

Pony AI: About 1,000 robotaxis currently; target fleet of 3,000 by 2026; international expansion into Qatar, South Korea, Singapore, and Luxembourg.

WeRide: About 1,000 robotaxis and >1,600 L4 vehicles, About 55m km of L4 mileage, and international licenses across US, UAE, Saudi Arabia, Singapore, and several European countries.

Source: The companies

Tesla as a looming contender

Tesla is a credible challenger despite a later commercial robotaxi push (mid‑2025). Its advantages are a massive driving dataset (over 7bn miles of FSD usage) and market-leading FSD software. Currently, Tesla has about 1,000 robotaxis but still requires human safety drivers.

Commercialisation remains in an early stage

L4 robotaxi services are still at an early commercial stage; revenue contribution and profitability for most operators remain limited:

Waymo: Waymo’s standalone financials are not disclosed by Alphabet, but it is widely believed to be operating at substantial losses due to heavy ongoing investment in technology, fleet expansion, and operations. Reportedly, Waymo is in talks to raise over USD 15bn in a new funding round at a potential valuation of up to USD 100bn—more than double its reported USD 45bn valuation from October 2024. If completed, the deal would provide a new valuation reference for other L4 robotaxi platforms.

Baidu (BIDU US/9888 HK): By Oct 2025, Apollo Go recorded ~240m autonomous km (140m fully driverless). In 3Q25 Apollo Go delivered 3.1m fully driverless rides, up 212% YoY. Baidu has not disclosed material revenue from autonomous driving; its near‑term earnings remain dominated by online marketing (c.62% of revenue) and AI cloud/applications (c.38%).

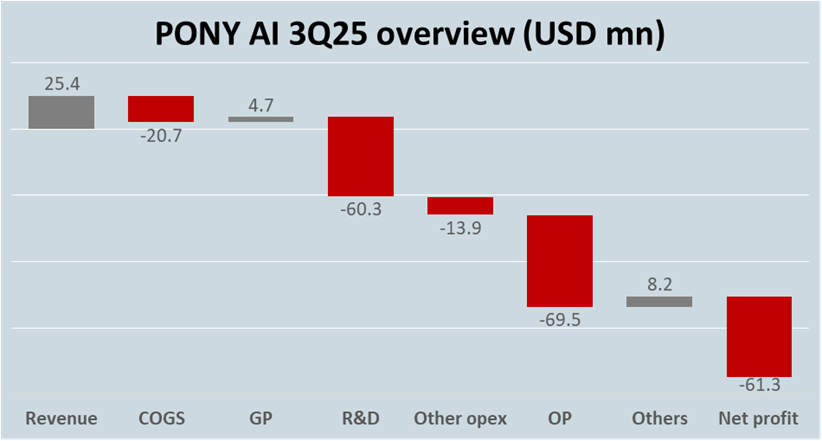

Pony AI (PONY US/2026 HK): Operating ~1,000 robotaxis and expanding internationally. 3Q25 revenue was ~USD 25m (+74% YoY), but the company posted a USD 61m net loss in the quarter (net margin ≈ -241%), with R&D (~USD 60m) heavily outweighing current revenue.

Source: The company

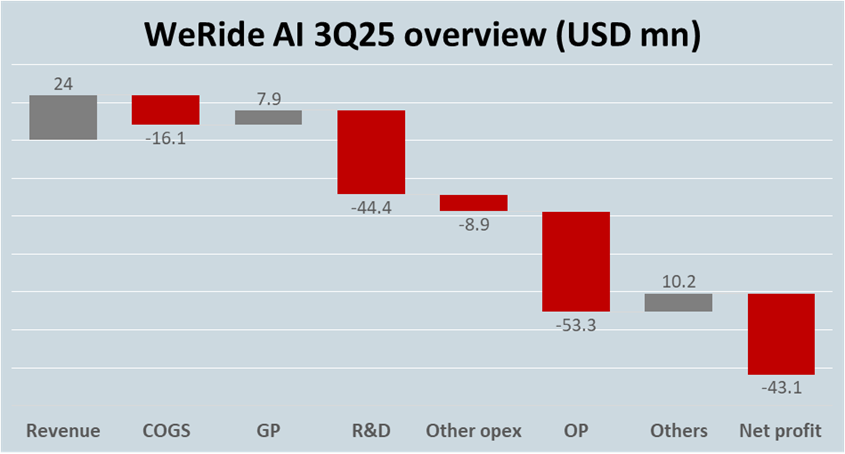

WeRide (WRD US/800 HK):As of Oct 2025, the company reported ~750 robotaxis, >1,600 L4 vehicles, and ~55m km of L4 mileage. 3Q25 revenue rose 144% YoY to ~USD 24m, but WeRide reported a USD 43m quarterly net loss (net margin ≈ -179%), again reflecting high R&D spend (~USD 44m). By end-2025, its Robotaxi reached 1,000 and company plans to reach hundreds of thousands of Robotaxis by 2030.

Source: The company

On a positive note, Chinese robotaxi operators are reaching or approaching unit‑economics breakeven in selected markets. Baidu has achieved unit‑economics breakeven in Wuhan, while Pony AI recently reached breakeven in Guangzhou following the rollout of its Gen‑7 robotaxis. WeRide expects to reach breakeven in Abu Dhabi after securing permission to remove the in‑vehicle safety officer. These milestones suggest robotaxi platforms are moving toward a “profitability inflection point” where proven unit economics in a few core cities can be replicated elsewhere.

Baidu’s Valuation Paradox: ‘Free Option’ on Autonomy?

The London pilot exposes a disconnect in global valuation multiples.

Waymo, the leading US player, has reportedly seeking valuations exceeding USD100bn in recent capital raises. On the other hand, Baidu—China’s leading player —trades at a market cap of about USD50bn. But Baidu is not a pure-play AV startup; it is a internet conglomerate with various segments.

To access the implied value of the autonomous driving unit (Apollo), we perform a SOTP analysis as below.

Net Cash & Investments: Baidu holds ~USD 21bn in net cash and long-term investments (after holding discounts).

Cloud Business: Valuing the AI Cloud division at a conservative 3x P/S yields ~USD 15bn.

Search business: Even applying a distressed 5x P/E multiple to the mature advertising business contributes ~USD 7bn.

The Implied Alpha: When these components are deducted from the market cap, the implied value assigned to Apollo is approximately USD 7bn.

At current levels, investors are paying a ‘distress price’ for the search business and acquiring the Apollo option for ~7 cents on the dollar relative to Waymo.

Asset Component

Net Value (USD bn)

Per Share (USD)

Methodology (with 25% holding discount)

Cash & Investments

21

63

Book Value

AI Cloud

12

36

2.5x Price/Sales

Core Search (Ads)

7

19

5.0x P/E (Distress multiple)

iQiyi

1

2

Sum of Non-Robotaxi Assets

41

120

Current Market Cap

48

142

Implied Value of Apollo

7

21

(Market Cap – Sum of Assets)

Benchmark: Waymo

100

Private Market Valuation

Discount to Waymo

93%

The risk-reward profile

As discussed above, the market has priced Baidu’s autonomous ambitions at low value. This creates an asymmetric risk-reward profile:

Downside protection: Supported by the profitable search utility and a net cash position covering ~40% of the market cap.

Upside optionality: Exposure to the only non-US autonomous fleet with global scale, entering a Tier-1 Western market with a structurally lower cost base.

Should Baidu can demonstrate positive unit economics in a high-labour-cost market in the long run, a re-rating of the Apollo asset might happen.

The Valuation regime: From ‘proxies’ to ‘profits’

While Baidu’s individual valuation appears dislocated, it suffers from a broader industry skepticism.

Valuing robotaxi platforms such as Waymo is challenging because commercialisation is still nascent and companies are investing heavily in R&D and fleet expansion. With “small revenue, big losses” profiles, conventional multiples such as P/E or P/S based on current or near‑term financials are often meaningless.

One approach is to build a long‑term financial forecast (for example, a 10‑year model), apply DCF techniques, or use EV/EBITDA or P/E on long‑dated estimates (e.g., 2030E) and discount back to today. However, these long‑horizon methods are sensitive to assumptions and less reliable when industry visibility is low and outcomes hinge on regulatory shifts, unit economics, and competitive dynamics.

Alternatively, investors can supplement traditional metrics with scale‑oriented proxies—for example, price‑per‑vehicle or price‑per‑ride—that capture fleet size and commercial activity.

Price per vehicle: This metric values the implied value for each autonomous vehicle as a revenue generating asset like a hotel room.

Price per weekly ride: This effectively values the volume of commercial activity, instead of just the asset (fleet) size. This is the “Facebook DAU (Daily Active User)” metric for Robotaxis.

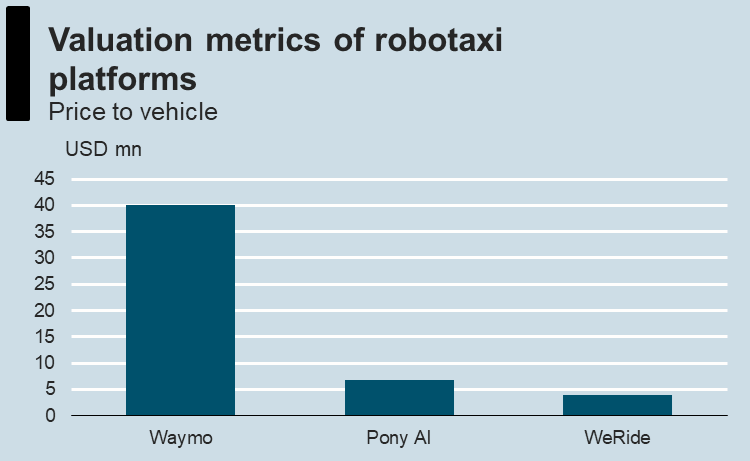

For instance, PE investors recently reportedly valued Waymo at about USD100bn, based on its 450,000 paid weekly rides and 2,500 vehicles, which implies a valuation of roughly USD222,000 per weekly active ride or USD40mn per vehicle. On the other hand, the public equity market is valuing USD6.8mn per vehicle and USD2.9mn per vehicle for Pony AI and WeRide respectively, much lower than Waymo.

Source: AP

On the flip side, these alternative metrics are essentially “proxy” valuations, focusing on top-line activities (rides and vehicles) and ignoring crucial fundamentals such as unit economy, cost-per-miles, utilization, cash flows, etc.

In addition, the market is applying a significant premium to Waymo, reflecting a perceived moat and first‑mover advantage. Should an emerging player like Tesla successfully enter the market and achieve scale, such premium (and implied per‑vehicle valuations) could compress sharply.

The Ultimate “Show Me the Money” Test

Ultimately, robotaxi platforms must pass the “show me the money” test. Currently, many valuations are premised on promise — fleet size, miles and ride volume — but over time investors will demand proof of sustainable profitability. In that phase, robotaxi platforms must generate enough cash to cover operating costs and capex. If unit economics do not improve, the sector would faces a de-rating. The market will stop valuing these companies as high-margin software platforms (based on P/S) and start valuing them as capital-intensive fleet operators (based on P/B).

This article is a “periodical publication” for information only and is not investment advice or a solicitation to buy or sell securities. This article does not constitute a “Personal Recommendation” or investment advice under UK FCA regulations. Investing in Asian markets involves significant risk. The author holds NO position in the securities mentioned. There is no warranty as to completeness or correctness. Please do your own due diligence or consult a licensed financial adviser. Please read the Full Disclaimer before acting on any information. Images created with the assistance of Gemini AI.

The FTSE 100 rose on Friday as investors reacted to confirmation that Glencore and Rio Tinto were in talks to create the world’s largest mining company.

London’s leading index was trading 0.4% higher at 10,084 at the time of writing.

“The FTSE 100 solidified its position above 10,000 on Friday after a mixed week which has seen the index attain fresh record levels,” says AJ Bell investment director Russ Mould.

“The mining sector continues to be a plus point for the FTSE 100 with Glencore and Rio Tinto confirming talks about a merger which would create the world’s largest miner.”

Glencore and Rio Tinto confirmed on Friday that they had resumed merger talks to bring together the FTSE 100’s two largest mining groups, with a combined market value of £149bn.

“Details are thin on the ground, but a deal could see Rio scoop up some or all of Glencore’s assets. A full combination would create a global leader in multiple industrial metals including iron ore and transition metals such as copper, cobalt and lithium,” Derren Nathan, head of equity research, Hargreaves Lansdown explained.

Glencore shares rose 9% on the news while Rio Tinto fell 2%.

“The divergent share price reaction would suggest the market thinks Glencore would be the bigger beneficiary of a deal. A key driver for the merger is the scramble for copper given its role in electrification and constrained supply,” Mould said.

Merger talks helped boost the rest of the FTSE 100’s diversified mining sector, with Antofagasta adding 3% and Anglo American rising 2.4%.

Elsewhere, Sainsbury’s shares were down over 4% after the retailer released its festive trading numbers that revealed another poor period of trading for its general merchandise business.

Grocery sales rose 5.4% in 16 weeks to 3 January 2026 but General Merchandise and Clothing fell 1.1% over the same period.

Analysts see Argos poor performance over the Christmas period as the final nail in the coffin for the unit, with Sainsbury’s likely to seek a disposal to focus on its more successful food business.

“Sainsbury’s has essentially hung up the ‘for sale’ sign over Argos today, after the chain spoiled a decent set of numbers for the supermarket’s core business,” said Chris Beauchamp, Chief Market Analyst at IG.

“The move to buy Argos looks increasingly like a wrong turn and an unnecessary distraction, especially when competition with Tesco over food sales is poised to heat up once more. Sainsbury’s has more important things to worry about, so the future for Argos is almost certain to see it become the target for yet another bidder.”

Marks & Spencer continued its rally, sparked by yesterday’s trading update, with another 2% rise. AB Foods gained 1% as it recouped a small proportion of losses sustained yesterday after issuing a profit warning amid slow Primark sales.

Sainsbury’s shares fell on Friday after releasing its festive trading update, with total retail sales (excluding fuel) rising 3.9% in the third quarter and 3.3% over the crucial six-week Christmas period.

But poor performance at Argos overshadowed robust food sales, sending shares down by over 4% at the time of writing on Friday.

Like-for-like sales grew 3.4%, driven by strong grocery performance, which increased 5.4% in the quarter and 5.1% over Christmas. The supermarket giant sold 20% more turkeys than last year as customers chose Sainsbury’s for their main Christmas shop, with Nectar loyalty scheme participants saving an average of £27 on their festive purchases.

Food sales proved the standout performer. Fresh food sales surged 8%, whilst premium own-label range Taste the Difference grew 15%, making it the fastest-growing premium own brand in the market.

The grocer launched over 260 new Taste the Difference products during the quarter, with party food items and festive desserts proving particularly popular. Groceries online sales jumped 14%, boosted by strong growth in on-demand delivery and improved availability.

However, while food sales were strong, Sainsbury’s was dragged down by its Argos business unit. Argos sales fell 1% in the quarter and 2.2% over Christmas, reflecting weak consumer confidence and subdued spending on higher-ticket items such as furniture.

“Keep in mind that Sainsbury’s is more exposed to general merchandise than its peers, owing to its ownership of Argos,” said Aarin Chiekrie, equity analyst, Hargreaves Lansdown

“General merchandise is the most cyclical area of the supermarket economy to be in, so being overweight in this arena can really slow sales down when things get tough. Recent initiatives are helping to drive higher sales volumes at Argos, but consumers remain cautious and are steering clear of big-ticket items.”

On Tuesday 20th January, the Kier Group (LON:KIE), whose vision is to be the UK’s leading infrastructure services and construction company, will be reporting a Trading Update for the first-half of its current year.

It should be more than positive and boasting of further growth in its Order Book – such news of which could help to boost still further the upward progress of its shares, now trading at 226p, up some 64% in the last year.

The Business

The £1bn-capitalised group, which is a leading provider o...

Rio Tinto and Glencore are in merger talks that could result in the creation of the world’s largest mining company, as deal-making in the sector picked up where it left off in the new year.

Following reports by the Financial Times overnight, Rio Tinto said in a statement on Friday that they: ‘note the announcement by Glencore and confirm that Rio Tinto and Glencore have been engaging in preliminary discussions about a possible combination of some or all of their businesses, which could include an all-share merger between Rio Tinto and Glencore’.

Glencore shares jumped over 8% in early trade on Friday, while Rio Tinto slipped 2%.

“Last year’s theme of consolidation in the natural resources sector has shown no sign of let up in the early part of 2026,” said Derren Nathan, head of equity research, Hargreaves Lansdown.

“In the same week we’ve seen Chevron make a swoop for Lukoil’s non-Russian fossil fuel assets, Rio Tinto and Glencore have confirmed that the mother of all mining deals could be back on the table.”

Rio Tinto and Glencore explored a potential tie around a year ago, but a deal couldn’t be struck at the time. Talks resume with many metals trading near all-time highs.

A successful merger would create a mining behemoth with exposure to pretty much every major metal group, as well as Glencore’s significant coal assets.

“Details are thin on the ground, but a deal could see Rio scoop up some or all of Glencore’s assets. A full combination would create a global leader in multiple industrial metals including iron ore and transition metals such as copper, cobalt and lithium,” Nathan explained.

The news of a potential tie-up between Glencore and Rio Tinto follows the merger of Anglo American and Teck Resources to form Anglo Tek, which is awaiting antitrust clearance.

FTSE 100 silver miner Fresnillo was also busy on the M&A front towards the end of last year, snapping up Probe Gold.

Cerillion (LON: CER) has won its largest ever contract for its BSS/OSS software suite and provide ongoing support and maintenance. The Oman Telecommunications contract is worth c.£42.5m over five years will underpin the current forecasts for this year and in the future. The share price jumped 11% to 1365p.

First Development Resources (LON: FDR) announced progress with the Selta project in Northern Territory, Australia. Lander West is prioritised as a key gold target following a Gradient Array Induced Polarisation geophysical survey. This will also help to refine and prioritise other potential drill targets. The share price improved 7.41% to 2.9p.

Digital health company MedPal AI (LON: MPAL) has integrated the MedPal app and the online MedPal Clinic. This will help to identify key indicators, such as weight loss and blocked metabolism. The targeting will be extended to all medications. The share price increased 5.88% to 6.75p.

Telematics services provider Quartix (LON: QTX) says 2025 revenues and profit will be ahead of expectations. Cash was £5.6m at the end of the year. Annualised recurring revenues are 14% ahead at £37m and net revenue retention is 98.1%. A final dividend of 7.5p/share is anticipated, taking the total to 10p/share. The share price rose 4.55% to 298p.

Kistos (LON: KIST) says pro forma exit production for 2025 was 22,700 boepd following acquisitions, Average production for the year was 9,000 boepd, Guidance for 2026 is 19,000-21,000 boepd. Net debt was $81m at the end of 2025. The share price is 3.18% higher at 178.5p, having been183.5p earlier in the day.

FALLERS

ECR Minerals (LON: ECR) has raised £1.5m at 0.26p/share. Initial gold production is expected at the Raglan project next month. Cash will be spent on finalising preparations for the Blue Mountain gold project in Queensland, exploration at the Lolworth Project, North Queensland and on other projects. The share price slipped 17.9% to 0.275p.

Rent guarantee services provider RentGuarantor Holdings (LON: RGG) increased full year revenues from £1.27m to £2.39m, which is 9% higher than expected. However, the loss is expected to be much more than the forecast of £446,000. Marketing spending was brought forward to 2025. The share price fell 5.65% to 29.25p.

Ex-dividends

Facilities by ADF (LON: ADF) is paying an interim dividend of 0.3p/share and the share price is unchanged at 17.5p.

Cohort (LON: CHRT) is paying an interim dividend of 5.8p/share and the share price fell 47p to 1077p.

Dotdigital (LON: DOTD) is paying a final dividend of 1.21p/share and the share price declined 0.1p to 66.5p.

FIH Group (LON: FIH) is paying an interim dividend of 1.25p/share and the share price is unchanged at 249p.

Jet 2 (LON: JET2) is paying an interim dividend of 4.5p/share and the share price slid 5.5p to 1415.5p.

Northamber (LON: NAR) is paying a final dividend of 0.3p/share and the share price dipped 1p to 31.5p.