For those who believe in the long-term adoption of artificial intelligence, the recent sell-off of the world’s largest AI-focused names will present an opportunity.

Concerns about valuations and the circular nature of investments, partnerships, and commercial relationships have led to dramatic pullbacks in companies at the forefront of the AI arms race.

Frothy valuations have inevitably drawn comparisons to the Dotcom boom and bust, and a growing number of analysts are calling a bubble.

But many aren’t and still believe there are legs in the AI trade as the technology is implemented across the global economy.

If you’re in the latter camp, these three AI stocks are well worth a look.

Nvidia

Nvidia is an obvious choice, but we’d be amiss to omit the world’s biggest AI stock from the selection.

Recent results were initially well received, as the chipmaker beat revenue estimates and provided encouraging guidance. However, nagging doubts about supply chain constraints and whether they will be able to sell their most powerful chips to China helped fuel a reversal on the day of release.

Nvidia’s meteoric rise makes it an easy target for the naysayers. Softbank selling its entire stake hasn’t helped either. But you can’t argue against its scale and revenue generation.

The firm generated record revenue of $57.0bn in Q3, up 22% from Q2 and 62% more than a year ago. Growth was driven by data centre revenue, which rose 25% to $51bn.

The company is still experiencing soaring demand for its chips, especially for its flagship data centre Blackwell products.

“Blackwell sales are off the charts, and cloud GPUs are sold out,” said Jensen Huang, CEO of Nvidia, in their recent earnings release.

“Compute demand keeps accelerating and compounding across training and inference — each growing exponentially. We’ve entered the virtuous cycle of AI. The AI ecosystem is scaling fast — with more new foundation model makers, more AI startups, across more industries, and in more countries. AI is going everywhere, doing everything, all at once.”

The recent pullback sees Nvidia trading at just 23x forward earnings. That isn’t expensive at all.

ASML

ASML is a Netherlands-based company that manufactures the world’s most advanced lithography machines, which are essential equipment for producing semiconductors.

Their extreme ultraviolet (EUV) lithography systems are the only tools capable of creating the tiny, densely packed transistors needed for the most powerful AI chips from companies like Nvidia, AMD, and Taiwan Semiconductor Manufacturing Company.

Without ASML’s technology, it would be impossible to manufacture the sophisticated processors that power large language models, data centres, and AI training systems.

No ASML would mean no chips and no AI boom.

ASML’s deep moat is likely the reason its shares are trading just 15% below recent highs. The stock certainly isn’t in bargain territory, but the dip looks like one that could be bought into.

Vistra Corp

AI data centres are expected to consume around 12% of total US power by 2030, up from 4% in 2023.

Vistra Corp is one of the largest power generators in the United States, operating a diverse portfolio of nuclear, natural gas, coal, solar, and battery storage facilities that produce approximately 41,000 megawatts of electricity.

Imagine SSE with some fossil fuels and nuclear thrown into the mix.

Vistra has become increasingly important to AI development because data centers require significant amounts of reliable, constant electricity to power their servers and cooling systems.

Vistra’s nuclear plants are particularly valuable for AI infrastructure since they provide 24/7 carbon-free baseload power, making the company a key supplier for tech companies building AI data centers.

As well as using its existing capacity to power AI data centres, Vistra is exploring co-location partnerships to build new power facilities near new data centres to secure stable power flow.

After hitting a 52-week high of $219, Vistra shares have fallen to $168. Although shares are substantially lower than recent highs, their historical valuation still looks rich at around 40x trailing earnings. Analysts, however, expect earnings to pick up significantly in the coming years with forward earnings multiples around 20x.

Shares in Cyber security services provider Shearwater Group (LON: SWG) declined after its latest results announcement. Chief executive Phil Higgins bought 10,000 shares at 48.7p each, taking his stake to 11.2%. His previous purchase was in 2023 at 64p/share. The share price subsequently fell further to 43.5p.

Jonathan Hall also bought 10,000 shares but at a share price of 48.5p. In February, he bought an initial 13,500 shares at 36p each.

Business

Shearwater provides cybersecurity and professional advisory services to a broad range of companies and governments. It sells cybersecurity software ...

Watch the Majedie Investments Investor Presentation, featuring Marylebone Partners CIO and Founder Dan Higgins.

Majedie Investments is an investment trust whose purpose is to provide its shareholders with long-term capital appreciation whilst paying a regular dividend. Since its inception in 1985, the Company has sought to achieve this objective by investing for the long-term, with equities at the heart of the approach. In January 2023, the Company modified its investment policy and appointed Marylebone Partners LLP as its investment manager.

Watch the online presentation for Shires Income, featuring Fund Manager Iain Pyle.

The Company’s investment objective is to provide shareholders with a high level of income, together with the potential for growth of both income and capital from a diversified portfolio substantially invested in UK equities but also in preference shares, convertibles and other fixed income securities.

Atlantic Lithium (LON: ALL) shares improved 37.3% to 11.2p ahead of its AGM on 27 November. The main rise was on Monday when there were 11.4 million shares traded. Management believes that the mining lease for the Ewoyaa lithium project in Ghana could be granted soon.

David Nugent, who owns 16% of Genedrive (LON: GDR), has agreed the terms of a loan of up to £1m. It can be drawn down in two equal tranches. It will be secured against the company’s assets. The share price recovered 22.4% to 0.9p.

Sabien Technology (LON: SNT) says Korea-based partner City Oil Field has commissioned its first regenerated green oil production plant. The partnership is being progressed to a strategic agreement. Sabien Technology will acquire a 1.12% stake in City Oil Field for £600,000 in shares, and the UK sales agreement has been extended for ten years and will be expanded to other countries. There will also be a deal to sell products from the new plant. City Oil Field will own 15.9% of Sabien Technology. The share price increased 17.9% to 8.25p.

X-ray screening systems supplier Image Scan (LON: IGE) has secured a double-digit unit contract with its Indian partner for the ThreatScan-LS1 following a competitive tender. The share price gained 15.6% to 1.85p.

FALLERS

Bigblu Broadband (LON: BBB) is in talks with the buyer of Skymesh about the post-acquisition performance of the business and whether there is going to be any deferred consideration. Bigblu Broadband may have to compensate the buyer for debtors that have not been collected. Bigblu Broadband plans to ask for shareholder permission to leave AIM at a general meeting on 8 December. It could leave on 18 December. Management will seek to realise value form the remaining assets. The share price dived 70.3% to 5.5p.

Empyrean Energy (LON: EME) says Conrad Asia Energy has signed an agreement with PT Nations Natuna Barat for farming into the Mako gas field in the Duyung production sharing contract and the new partner will pay 100% of project development costs for a 75% non-operated participating interest in the Duyung PSC. The deal could be completed by the third quarter of 2026. Empyrean Energy is in dispute with Conrad Asia Energy about its interest in the Duyung PSC. The share price slumped 69.2% to 0.0425p.

Industrial equipment distributor HC Slingsby (LON: SLNG) is asking for shareholder approval to leave AIM. The shares are illiquid and the cost of being on AIM adds to the company’s loss, which was £237,000 in the nine months to September 2025. Net debt was £340,000. There is already support from shareholders owning 73.2% of the shares. HC Slingsby transferred from the Main Market to AIM on 24 May 2005. It has been on the London Stock Exchange for many decades. The cancellation could be on 23 December. No matched bargain facility is planned. The share price dipped 52% to 60p.

Defence consultancy RC Fornax (LON: RCFX) raised £2.25m in a placing at 6p/share and raised £70,000 out of the £500,000 retail offer. The cash will fund development of the Procure X Marketplace to connect small companies with defence buyers and provide working capital. Directors and management are investing £156,800 in new shares. This includes Paul Reeves and Daniel Clark who raised £1m in the flotation back in February, when the company raised £5.2m at 32.5p/share. Cavendish has increased its 2025-26 forecast loss to £2m and expects a lower loss next year. The share price slid 39.5p to 5.9p.

Kasei Digital Assets (LON: KASH) plans a return of cash to shareholders. There should be £3.4m in cash after selling assets and this should be returned to shareholders. A subscription of £200,000 at 1p/share will provide an additional £100,000 for distribution. The new investors include new executive chairman Kwasi Kwarteng, the former Chancellor of the Exchequer, new non-exec Paul Withers, Daniel Howe and Sam Daughtry, plus existing directors Jai Patel, who will become chief executive, and Brendan Kearns. Bryan Coyne, Steven Davis and Jane Thomason will resign from the board. The unsuccessful digital assets strategy will be adapted with a greater focus on Bitcoin, and more cash raised. The share price jumped 38.9% to 12.5p, which values the company at £4.2m.

Ajax Resources (LON: AJAX) says the terms of the conditional acquisition of the Paguanta zinc, silver and lead project have been revised. It will acquire a company with a 74.81% stake in the project for $37,500 in cash and $37,500 in shares. The seller will retain a 1% net smelter royalty capped at $500,000. The Environmental Impact Assessment has been submitted for the Eureka project and the company issued formal notices to relevant communities. The Environmental Impact Declaration should be issued in early December. The share price gained 19.4% to 5.375p.

Online consumer loans provider Amazing AI (LON: AAI) is exploring the options of quotations on the Mauritius Stock Exchange and/or the US OTCQB Market. This follows the decision not to go ahead with spinning off 80% of its subsidiary based in Mauritius and retaining the minority stake. Existing company shareholders will receive shares on a pro rata basis. The share price improved 16.7% to 0.35p.

Evrima (LON: EVA) investee company Eastport Ventures Inc has joined the TSX Venture Exchange. Evima owns 3.83% of the Botswana-focused critical minerals explorer and also holds warrants. The Evrima share price increased 14.3% to 0.4p.

Hot Rock Investments (LON: HRIP) has a portfolio of shares, as well as 150,000 shares in WeShop Holdings (NASDAQ: WSHP), which has joined Nasdaq. The share price was well above $200 at one point last week and ended at $113.40. The stake is valued at $17m. At 1.35p, up 12.5%, Hot Rocks Investments is valued at £2.8m.

Wishbone Gold (LON: WSBN) is holding a general meeting on 28 November to gain shareholder approval for a 100-for-one share consolidation. The share price rose 5.88% to 0.9p.

Dominic White has stepped down as a director of technology-based financial services company Eight Capital Partners (LON: ECP). He remains as an adviser. The share price edged up 1.27% to 79.5p.

FALLERS

Energy transition engineering Time To ACT (LON: TTA) says the main subsidiary Diffusion Alloys is likely to be profitable in 2025-26 and 2026-27, although this depends on timing. The order book of large project work is worth more than £4m and most of this will be recognised during 2026. There is enough cash for at least 12 months, but it appears it will not last as long as previously expected. Oberon Capital has been appointed joint broker. The general meeting was postponed. The share price slumped by two-fifths to 9p, which is a new low.

The Smarter Web Company (LON: SWC) has raised another £141,000 at 61p/share. The share price dived 26.9% to 39.5p.

Valereum (LON: VLRM) has completed a subscription to raise raised £600,000 at 5p/share. Chairman James Bannon and chief executive Gary Cottle contributed £225,000 each and they will each receive 2.5 million warrants exercisable at 50p each and 2.5 million warrants exercisable at 100p each. The rest comes from another investor, which will also receive warrants. A further £50,000 has been raised by the exercising of warrants at 4p each. The share price dipped 22.6% to 6p.

Mendell Helium (LON: MDH) raised £200,00 at 3p/share. This is a direct investment by an existing shareholder. The share price slid 17.9% 2.875p.

B HODL (LON: HODL) has taken its Bitcoin holding to 155.039 and the total cost was £13.1m. The share price decreased 13% to 11.75p.

Music agent All Things Considered (LON: ATC) is moving to AIM and raising £8.6m at 125p/share. The expected admission date is 17 December, which is four years after joining Aquis at 153p/share. Trading is second half weighted and is currently in line. The share price declined 10.7% to 125p.

Shepherd Neame (LON: SHEP) non-executive director Marion Sears bought 4,000 shares at 466p each. The share price is 5.72% lower at 464p.

WeCap (LON: WCAP) owns 11.8% of WeShop Holdings (NASDAQ: WSHP). That is 806,022 shares directly and 2.08 million shares via a 23.5% holding in Community Social Investments Limited (CSIL). At $113.40, the stake is worth $31m. Peel Hunt has cut its shareholding in WeCap from 18.4% to below 10%. Because of this, the share price edged down 2.04% to 2.4p despite higher trading levels during the week.

AI-based technology commercialisation company GenIP (LON: GNIP) has received 57 repeat orders. This includes 50 orders from two US universities and seven from a UK university. The share price gained 5.41% to 19.5p.

ITM Power (LON: ITM) has been selected as the partner to supply 710MW of its electrolysers to Stablegrid in Germany. The system will help to stabilise the German electricity system because of variable output from renewable energy. Final investment decision will be in 2028. The share price rose 4.19% to 74.6p.

GCM Resources (LON: GCM) had a cash outflow of £1.27m in the year to June 2025. Net debt was £4.9m at the end of June 2025. The company says that the Phulbari coal and power project is the most advanced and deliverable domestic coal project in Bangladesh. The share price improved 4.35% to 6p.

Safilo Group made an approach to Inspecs (LON: SPEC) to acquire the Eschenbach and BoD businesses. It made two non-binding cash offers, and they we rejected by Inspecs. The share price increased 2.74% to 75p.

Healthcare financial software provider Craneware (LON: CRW) has started the latest financial year positively. The alliance with Microsoft is bringing significant opportunities. Craneware is developing a product for the 340B drug rebate programme in the US. The share price is 2.12% higher at 2165p.

FALLERS

UK Oil & Gas (LON: UKOG) has raised a further £520,000 at 0.016p/share. The company has raised more than £5m since the beginning of October. This will help to accelerate the development of hydrogen storage projects and moving ahead with a potential electrolytic hydrogen generation project geared initially to decarbonise the energy use of a substantive Dorset-based industrial user. The share price slipped 18.8% to 0.0175p.

NWF (LON: NWF) says its businesses have had a mixed first half performance. Heating oil volumes have been lower than normal and the winter increase in demand is not likely to make up for this. Commercial fuels demand has also been lower, and this is higher margin. This has led to pricing pressures as the company rolls out a new regional operating model. The food distribution and feeds businesses are doing well, with the former picking up new contracts. The share price declined 18.2% to 130p.

Gold explorer Panthera Resources (LON: PAT) says test results on bulk composite samples from the Kalaka deposit in Mali. The ores are amenable and recoveries averaged 76.3%. CIL extractions can average 93.4%. The share price fell 5.46% to 22.5p.

Index over-discounting budget and interest rate concerns

2026 seen as year of outperformance for the junior market

AIM now appears to be over-discounting current budgetary and interest rate concerns. TPI is projecting the junior index to outperform the benchmark FTSE All-Share for the whole of 2026.

AIM had in fact been outperforming nicely until October, when it hit a rather unexpected ‘bump in the road’. You may recall back at the beginning of May 2025, TPI stuck its head above the parapet with its forecast that the junior index would outperform the FTSE All-Share between then and the year end. All was looking very good……until the wheels came off in mid-October, when it became clear that the Bank of England (‘the Bank’) had become so nervous about no. 11’s confused messaging that it was about to slam the brakes on its all-important rate-cutting cycle, leaving the market to fester as it pondered what more the Chancellor could do to impact it. The resulting sell-off turned what had been as much as a 8% relative gain over the session into a similar loss. In absolute terms the AIM All-Share has risen c.5.0% since 1 May 2025.

Sell on the rumour, buy on the news! Partly by design and partly by default, it now looks like AIM will in fact be a net beneficiary of the forthcoming Budget. Widely expected to refocus on growth (to the detriment of value), Rachel Reeves is likely to offer greater certainty for unlisted securities by sustaining benefits already in place through for the Enterprise Investment Scheme (‘EIS’) and Venture Capital Trusts (‘VCT’), while scotching rumours of further restriction of Inheritance Tax (‘IHT’) Business Relief on qualifying shares (such as capping or removing it entirely). While there remains reasonably high expectation that higher taxes will be imposed on dividends, AIM of course has never been a destination for income and so can be expected to bypass any hit taken by the other, more senior UK markets.

Starting on 18 December, a series of 25bp base rate cuts (from the current 4%) look almost certain to commence once again. This is key to confidence in AIM investment. With the UK’s GDP growth tumbling to just 0.1% in Q3 2025 and unemployment rising to 5% (Q2 2025: 4.7%) during the same period, the Bank’s current 2026 projection of just 1.2% economic expansion is now looking a bit stretched. So it will be forced to use the only tool it has to deliver an immediate boost to domestic confidence amid the UK’s ongoing political turmoil; as many as four more consecutive 25bp cuts could be needed to ward off a recession in 2026, with base rates even then being at a good premium to the ECB’s present Main Refinancing Operations (‘MRO’) level of 2.15%.

Chartists will also be interested to note the fact that the AIM All-Share has rebounded decisively no less than ten times from the 685 (±2.5%) support level over the past 15 years, suggesting significant downside protection

FTSE AIM All-Share Data Index Level: 737.41 Net Market Cap: £41,170m No of Constituents: 549 52 week high/low: 796.52/624.42 Past 7-months return: 4.84%

Constituent Sizes and Yield Ave. Market Cap: £74.58m Medium Mk Cap: £14.00m Largest Mk Cap: £2,608.52m Smallest Mk Cap: <£1m Index Yield: 1.94%

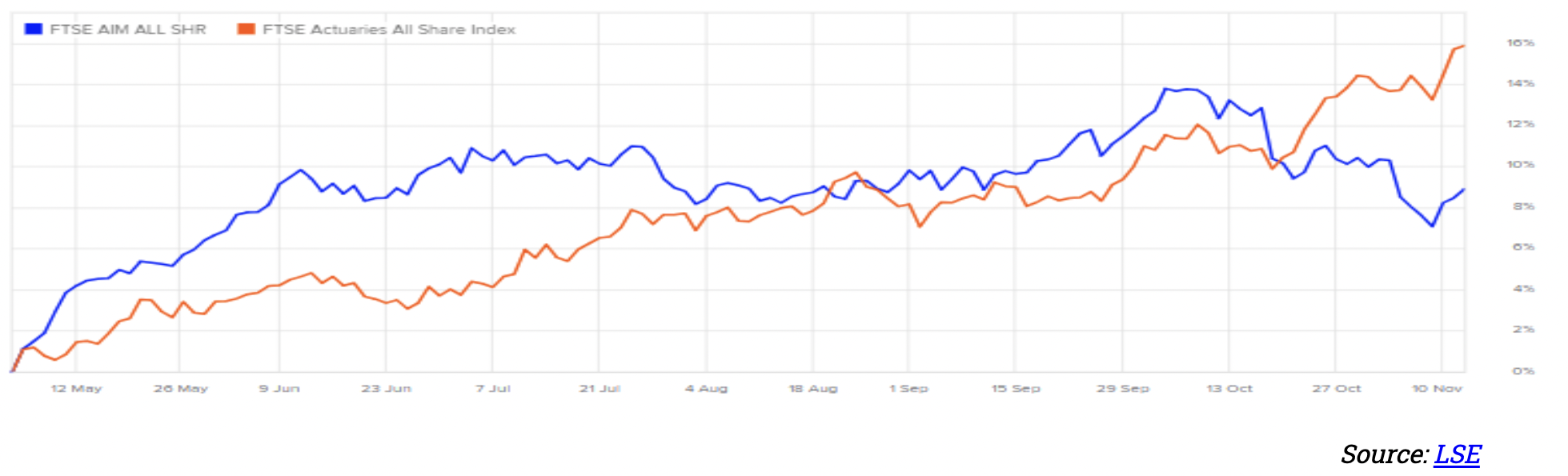

AIM All-Share – 15-year Performance Chart

AIM – Had been outperforming nicely ………until it hit a mid-October’ ‘bump in the road’

TPI stuck its head above the parapet back at the start of May 2025, with its forecast that AIM would outperform the FTSE All-Share between now and year end. Analysis suggested the Index was about to emerge from the ‘perfect storm’ it had encountered since peak Pandemic, with the interest rates finally heading downwards amid expectation of an extended series of cut, while UK-focussed equity fund outflows were slowing and the halving of the inheritance tax exemption also appearing to have been just about priced in.

AIM All-Share had Consistently Outperformed the FTSE All -Share Until Mid-October 2025

The scenario worked well for the following 5 months, allowing the Index to chalk up relatively consistent outperformance (of almost 10% at one stage), only to then hit a ’bump in the road’ in mid-October. This rapidly reversed AIM’s hard-won gains to now sit a similar amount below the benchmark. This coincided with the release of cautionary UK macroeconomic data including slowing GDP growth accompanied by stubbornly high CPI, resulting in a stalling of further interest rate cuts. With signs of sharply declining productivity, the Government’s escalating deficit will force the Chancellor to address a funding ‘gap’ estimated to be between £20 billion and £50 billion in her forthcoming budget. Given that this is almost certain to be affected through further punitive attacks on wealth, AIM‘s overwhelming dependence on the domestic economy meant that it was no surprise when investors chose to lock-in profits to date.

Sell on the rumour, buy on the news

UK markets have been trading under the shadow of 26 November for some time now. This is perfectly illustrated by nearly £7.3bn having been withdrawn from equity funds by UK-based investors since July, the largest outflow ever recorded in a four-month period. Not surprisingly, many were seeking simply to crystalise gains prior to, or in anticipation of, the imposition of new punitive taxes from April 2026.

UK Equity -Net Fund Flow

With such a dull picture being painted, it is not surprising that the UK continues to trade at relatively deep discounts to both the US and EU markets. The FTSE 100, for example, is presently valued at c.13-14 times earnings, or roughly half the 22 to 27 level S&P 500 enjoys even if this can be partly explained away by its traditional sector mix weighting heavily toward financials, energy and materials as opposed to high-growth technology shares. Since the COVID Pandemic peaked at the end of Q1 2021, AIM has tumbled by an extraordinary 67% relative to the FTSE All Share leaving it trading c.42% below its 10-year average.

Yet, partly by design and partly by default, it looks like AIM will in fact be a net beneficiary of the forthcoming Budget. As well as keeping current investment incentives intact, there is general expectation that the Chancellor will look for new routes to boost overall UK business investment; one such move (likely to be effective from April 2026) could be to reduce the current £20,000 allowance on cash ISAs in an effort to divert money to stock and shares ISAs instead; a further, potentially even more significant, initiative for the junior index was launched on 21 October 2025, whereby twenty of the UK’s largest pension providers and insurers (the ‘Sterling 20’, representing >90% of the UK’s active Defined Contribution scheme savers) voluntarily agreed with the government to channelling of a proportion of pension savings into unlisted UK growth opportunities (including those quoted on AIM), national infrastructure projects, etc. The timing by which AIM might see real inflows as a result remains uncertain, although the aim is to unlock at least 5% of their main default funds (>£25bn) by 2030 for investment in areas such as affordable housing, broadband connections and scale-up finance for early-stage growing businesses.

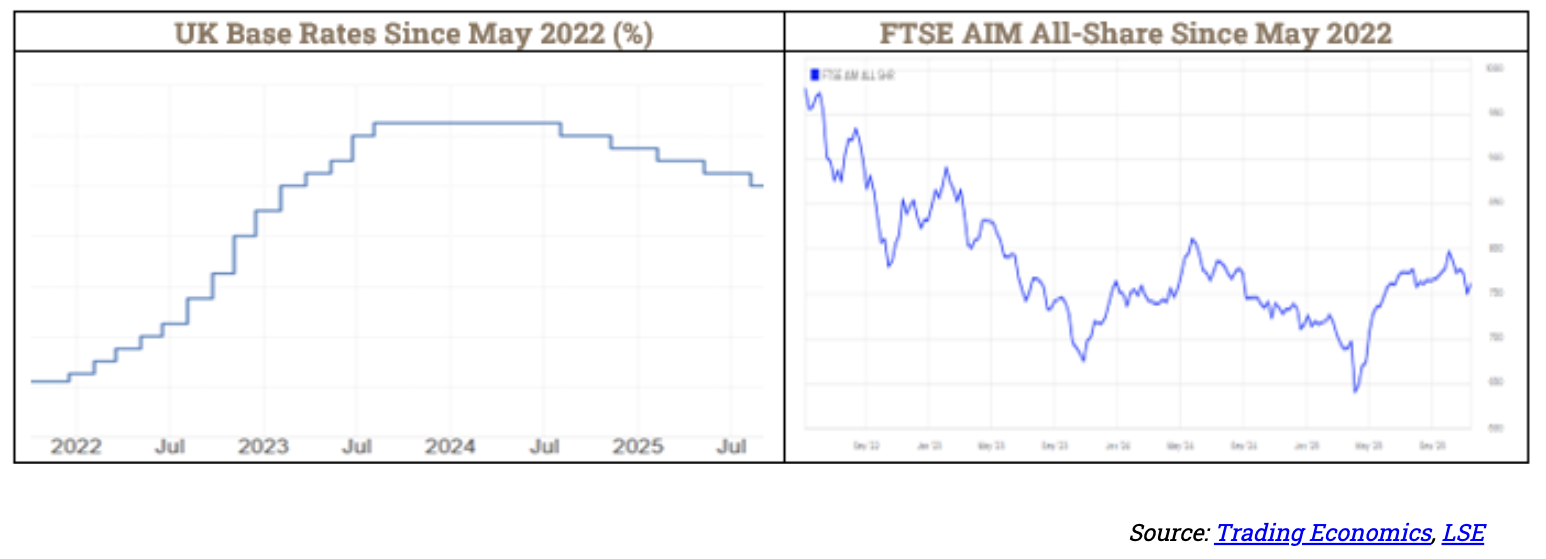

AIM Index Performance – A Mirror Image of UK Base Rate Moves

The charts above demonstrate AIM’s sensitivity to UK base rate cuts. Turner Pope projects the Bank to commence a series of four straight 25bp cuts, starting on 18 December 2025 and continuing through to the end of next year. The Bank recently stated its view that UK CPI has probably already past its peak (having now fallen back to 3.6% in October after plateauing at 3.8% in each of the three previous months) and went on to forecast consumer prices will fall back to about 2.5% next year, before touching its 2% target during the course of 2027. But with Q3 2025 GDP growth having tumbled to just 0.1% while UK unemployment rose to 5% (the highest since the end of the Covid pandemic) over the same period, its current projection that the economy will expand by just 1.2% in 2026 is now looking tenuous. Various pundits are taking bets on the UK falling into recession within the coming 6 months. So, in the absence of any unexpected new ‘shocker’ from the Chancellor just one week from now, an 18 December cut from 4.0% to 3.75% looks almost in the bag. Assuming also that the UK’s current political turmoil continues to compound in the coming months, the Bank will be obliged to do whatever it can to maintain a slither of domestic confidence in the hope of attracting incoming investment.

AIM – Stock picking still the key to winning

With most of AIM’s early-stage constituents remaining cash consumers, there is a wide disparity in terms of their operational risks, market positioning and the underlying quality of their management. This has always

meant that passive Index investing is less effective than a rigorous, active management approach (stock picking) to identify promising companies.

With this in mind, a tabulation has been provided below to detail the performance of a selection of the equity placings TPI has conducted for its Advised companies over the past couple of years, detailing gains registered both at the individual company’s share price peak and at its current level.

Performance Following Recent TPI AIM Equity Placements1

Name

Equity Placing Date

Amount Raised (gross)

Placing Price (p)

Subsequent Share Price Trading High (p)

%Profit/Loss from Trading High (p)

Current Share Price (p)

%PL on current price

Orosur Mining Inc.

Feb-24

£500k

2.95

29

883%

19.6

564%

Avacta Group plc2

Feb-24

£25.7m

50

82

64%

83.2

66%

N4 Pharma plc

Jun-24

£630k

0.5

1

100%

0.63

26%

Aptamer Group plc

Jul-24

£2.83m

0.2

1.57

685%

0.90

350%

Orosur Mining Inc.

Sep-24

£835k

2.78

29

943%

19.66

607%

Ironveld plc

Oct-24

£2.5m

0.036

0.08

122%

0.05

39%

Orosur Mining Inc.

Dec-24

£1.25m

6.6

29

339%

19.6

197%

Theracryf plc

Feb-25

£4.25m

0.25

0.275

10%

0.21

-16%

N4 Pharma plc

Apr-25

£1.75m

0.4

1

150%

0.63

58%

Alien Metals Ltd.

May-25

£1m

0.08

0.3

275%

0.12

50%

Metir plc

Jun-25

£1.75m

0.65

1.49

129%

0.80

23%

Ironveld plc

Jun-25

£900k

0.045

0.08

78%

0.05

11%

Zephyr Energy plc

Jun-25

£10.5m

3.00

3.3

10%

2.45

-18%

Aptamer Group plc

Jul-25

£2.0m

0.3

1.57

423%

0.90

200%

Avacta Group plc2

Jul-25

£3.25m

30

83.2

177%

83.2

177%

Orosur Mining Inc.2

Oct-25

£10.6m

18.09

29

60%

19.6

8%

Futura Medical plc

Nov-25

£2.75m

1

1.7

70%

1.25

25%

Risk Warning: Past performance is not a reliable indicator of future results.

THIS DOCUMENT IS NOT FOR PUBLICATION, DISTRIBUTION OR TRANSMISSION INTO THE UNITED STATES OF AMERICA, JAPAN, CANADA OR AUSTRALIA.

Conflicts

This is a non-independent marketing communication under the rules of the Financial Conduct Authority (“FCA”). The analyst who has prepared this report is aware that Turner Pope Investments (TPI) Limited (“TPI”) has a relationship with the company covered in this report. Accordingly, the report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing by TPI or its clients ahead of the dissemination of investment research.

TPI manages its conflicts in accordance with its conflict management policy. For example, TPI may provide services (including corporate finance advice) where the flow of information is restricted by a Chinese wall. Accordingly, information may be available to TPI that is not reflected in this document. TPI may have acted upon or used research recommendations before they have been published.

Risk Warnings

Retail clients (as defined by the rules of the FCA) must not rely on this document.

Any opinions expressed in this document are those of TPIs research analyst. Any forecast or valuation given in this document is the theoretical result of a study of a range of possible outcomes and is not a forecast of a likely outcome or share price.

The value of securities, particularly those of smaller companies, can fall as well as rise and may be subject to large and sudden swings. In addition, the level of marketability of smaller company securities may result in significant trading spreads and sometimes may lead to difficulties in opening and/or closing positions. Past performance is not necessarily a guide to future performance and forecasts are not a reliable indicator of future results.

AIM is a market designed primarily for emerging or smaller companies and the rules of this market are less demanding than those of the Official List of the UK Listing Authority; consequently, AIM investments may not be suitable for some investors. Liquidity may be lower and hence some investments may be harder to realise.

Specific disclaimers

This document has been produced by TPI independently. Opinions and estimates in this document are entirely those of TPI as part of its internal research activity. TPI has no authority whatsoever to make any representation or warranty on behalf of any of the markets or indices mentioned in this report

General disclaimers

This document, which presents the views of TPIs research analyst, cannot be regarded as “investment research” in accordance with the FCA definition. The contents are based upon sources of information believed to be reliable but no warranty or representation, express or implied, is given as to their accuracy or completeness. Any opinion reflects TPIs judgement at the date of publication and neither TPI nor any of its directors or employees accepts any responsibility in respect of the information or recommendations contained herein which, moreover, are subject to change without notice. Any forecast or valuation given in this document is the theoretical result of a study of a range of possible outcomes and is not a forecast of a likely outcome or share price. TPI does not undertake to provide updates to any opinions or views expressed in this document. TPI accepts no liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document (except in respect of wilful default and to the extent that any such liability cannot be excluded by applicable law).

The information in this document is published solely for information purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. The material contained in the document is general information intended for recipients who understand the risks associated with equity investment in smaller companies. It does not constitute a personal recommendation as defined by the FCA or take into account the particular investment objectives, financial situation or needs of individual investors nor provide any indication as to whether an investment, a course of action or the associated risks are suitable for the recipient.

This document is approved and issued by TPI for publication only to UK persons who are authorised persons under the Financial Services and Markets Act 2000 and to professional clients, as defined by Directive 2004/39/EC as set out in the rules of the Financial Conduct Authority. This document may not be published, distributed or transmitted to persons in the United States of America, Japan, Canada or Australia. This document may not be copied or reproduced or re-distributed to any other person or organisation, in whole or in part, without TPIs prior written consent.

The FTSE 100 dropped again on Friday as concerns about AI valuations returned with a vengeance overnight, with Nvidia giving up 6% gains to close negative.

The S&P 500 closed 1.6% lower, and the tech-focused NASDAQ shed 2.2%.

Such heavy selling was difficult for European traders to ignore, and the FTSE 100 lost 0.6% in early trade.

“It seemed, for a while, yesterday that everything was right with the world once again. Nvidia delivered strong earnings on Wednesday, reigniting some enthusiasm around the AI theme, and the September jobs report was a solid-ish one, albeit a report that had a few blots on the copybook under the surface,” explained Michael Brown Senior Research Strategist at Pepperstone.

While the lower start to trade on Friday will be a kick in the teeth for bulls that thought Nvidia had saved the day with a seemingly upbeat earnings report, London’s leading index did pick up from the worst levels as bargain hunters stepped in.

The FTSE 100’s cyclical sectors were heavily hit on Friday. Investors rotated out of miners, engineering firms, and technology-oriented investment trusts.

Babcock was also among the losers despite reporting a very respectable set of half-year results. Babcock shares were down 1.2%, most likely due to wider selling rather than any real disappointment given a 7% jump in revenue and higher profits.

“Babcock’s latest results will make even the most hardened defence investors sit up a little straighter. A 19% jump in first-half operating profit and a 25% dividend hike would be eye-catching in any sector; but in a business better known for long-cycle contracts and cautious guidance, it’s confirmation that Babcock is well and truly firing on all cylinders,” said Mark Crouch, market analyst for eToro.

“The British engineering and defence group has powered down debt, sharpened execution and turned itself into one of the London market’s most consistent outperformers. It helps, of course, that governments are rediscovering the urgency of naval capability. From Danish and Swedish frigate tenders to a Polish submarine partnership with Saab, Babcock is suddenly the name on every northern European admiral’s lips.”

JD Sports was another notable faller, as the decline after yesterday’s trading statement continued. JD is now trading at its lowest levels since July.

ASOS’s fall from grace continues with another year of losses and falling revenues. Once revered as the UK’s leading technology company, ASOS is facing multiple headwinds that are only showing marginal signs of improvement.

ASOS shares were down over 6% on Friday after releasing full-year numbers that revealed a 14% decline in revenue and an adjusted loss before tax of £98m.

“ASOS’s latest results continue to show an uphill battle to execute a turnaround with shares down sharply this morning,” said Adam Vettese, market analyst for investment platform eToro.

“The company missed profit expectations, largely due to subdued consumer demand, reflecting broader economic worries and tighter household budgets. Many customers appear to be delaying purchases, or waiting out for deeper discounts which is a habit ASOS would do well to avoid relapsing into.”

Looking past the disappointing headline numbers, there were some signs of improvement. Gross margins increased to 47.1% from 43.4% and the £98m loss before tax was an improvement on last year’s £126m loss.

“Long-suffering ASOS shareholders will hope that the improvement in gross margins in today’s numbers signals better times ahead,” explained Chris Beauchamp, Chief Market Analyst UK at IG.

“Crucially the firm expects this trend to continue too. While its perhaps not the week to go big on AI, the theme made an appearance in these numbers and might help drive sales. We have seen too many false dawns in ASOS over the years, but perhaps this morning’s numbers mark the start of a recovery back to the highs of a year ago.”

The progress in losses and margins was driven by a focus on higher-value sales and lower discounting. But lower overall sales aren’t anything to cheer about.