The FTSE 100 was treading water on Monday with US equity markets closed for the President’s Day holiday providing little new impetus for major repositioning in European stocks.

“Volumes are set to be more muted during the sessions in Europe given that Wall Street is closed for the President’s Day holiday, so traders are likely to be searching around for a bit of a sense of direction today, looking ahead to fresh data out this week,” said Susannah Streeter, head of money and markets, Hargreaves Lansdown.

There was strength in Asian markets overnight after the Chinese central bank kept rates on hold as their economy emerges from a prolonged period of covid restrictions.

“Asian stocks were higher as China’s central bank kept rates unchanged for a sixth consecutive month – hopes for a continuing recovery in demand from the world’s second largest economy helped support commodity prices,” said AJ Bell investment director Russ Mould.

Higher commodity prices helped provide support for miners sending Rio Tinto 1.2% higher while Anglo American added 1.7%.

Lloyds shares were 1% higher ahead of the release of their full year results on Wednesday. Both NatWest and Barclays had disappointing market reactions to their recent releases with shares falling heavily.

Tesco

Tesco shares were flat after reports it was exploring a potential demerger of their banking unit. A sale of their banking unit would allow for greater focus on their core operations at a critical point for supermarkets in the cost-of-living crisis and continued growth of the discounters, Lidl and Aldi.

“We’ve seen numerous demergers in recent years as companies streamline to have a sharper focus and unlock hidden value in their business. Doing less is more, as it provides management with an opportunity to make small incremental changes to operations and have the core business running like a well-oiled machine,” said Russ Mould.

“With that backdrop in mind, one should expect to see many companies like Tesco concentrate on what they do best and find someone else to take over activities on the periphery.”

“Offloading Tesco’s banking arm makes perfect sense. Supermarkets should concentrate on grocery and core essentials that fall under general merchandise, such as frying pans, greetings cards and a small line of toys to keep the kids happy while their parents shop. Things that people can pop into their basket without much thought.”

Medical disinfection products supplier Tristel (LON: TSTL) is back to past growth rates with all the regions growing in double digits, helped by price increases. The UK was the fastest growing market.

In the six months to December 2022, revenues were 15% ahead at £17.5m and the growth rate was greater if discontinued products are excluded. Pre-tax profit improved from £2.13m to £3.08m. The tax charge is higher, so earnings growth was slower. The interim dividend is maintained at 2.62p a share. Net cash is £8.42m.

Medical device decontamination sales were one-fifth higher at £14.7m, while cache surface disinfection sales were 13% ahead at £1.8m. Sales of other products fell.

FDA

Progress is being made by AIM-quoted Tristel with the FDA approval for medical device decontamination product DUO ULT. The latest FDA submission will be made before the end of March and the FDA has 75 days to announce its decision. That means that there will be no contribution in the current financial year even if approval is gained.

Tristel is spending £3m on FDA approval. To reflect that it has renegotiated the US distribution agreement with Parker Labs. The FDA approved royalty has been increased to 30% of gross profit, while the existing EPA approved royalty is raised to 20% of revenues.

There are more benefits to come from price increases in the second half. finnCap expects underlying pre-tax profit from £4.5m to £6m. Given the strong start to the year and the second half normally being stronger, that should be relatively easily achievable with potential for an upgrade later in the year. At 330p, the shares are trading on 31 times prospective earnings. The cash pile will continue to build up.

The existing business can continue to grow strongly, but FDA approval for DUO ULT would provide an additional boost, with other products likely to follow. News concerning FDA approval is likely to provide upward momentum for the share price.

Proteome Sciences (LON: PRM) says 2022 revenues were 53% ahead at £7.8m with particularly strong growth from the reagents business thanks to a milestone payment from Thermo Scientific. Profit is improving. The contract proteome services provider had cash of £4m at the end of 2022, up from £2.4m. The share price jumped 27.2% to 4.77p.

Mosman Oil & Gas (LON: MSMN) has received a sacred site clearance certificate for EP 145 in the Amadeus Basin, Northern Territory, Australia. The prospect could have gas, helium and hydrogen. The share price rose 13% to 0.065p.

Corcel (LON: CRCL) has broadened its strategy to include oil and gas as well as mining. There are also plans for investments in Brazil and other potential transformative acquisitions. A joint venture is being set up for the Asian interests. Ground magnetics have provided drill targets for the Mt Weld rare earths project in Western Australia and an eight-hole drill programme has been designed. Drilling could start by March. The share price increased 9.62% to 0.285p.

Keystone Law (LON: KEYS) says full year profit will be marginally ahead of current expectations of £8.5m. There are a total of 507 fee earners even though economic uncertainty hampered recruitment. The full year results will be published on 25 April. The share price is 8.72% higher at 530p.

Verditek (LON: VDTK) says that the termination of the solar equipment supply agreement with Bradclad takes effect from 3 March. Verditek is trying to recovery cash owed. The share price dived 24.1% to 0.55p.

Inland Homes (LON: INL) has renegotiated banking covenants and the share price jumped on Friday. Some of that gain has been lost with a 19.2% fall to 12.125p this morning. HSBC loan covenants relate to tangible net worth and gearing. They will revert to the original level from the end of June. A waiver of a historic breach of gearing on the Secure Trust loan has been secured and extended to the end of March.

Tekcapital (LON: TEK) has launched a £2.25m placing at 16p a share. That sparked a 16.1% decline in the share price to 17p. The cash will be invested in investee companies with £600,000 to help MicroSalt build up inventories and £1m to buy autonomous shuttles for driverless vehicle technology developer Guident’s clients. MicroSalt is planning to float on AIM.

Gold recovery company Goldplat (LON: GDP) shares returned from suspension following the publication of accounts for the year to June 2022 and a second quarter update. The share price immediately fell, although it has recovered slightly, but it is still down 11% to 9.125p. The full year figures were as expected with earnings of 2.3p a share. A deal has been secured with DRD Gold in South Africa to treat gold-enriched soil, plus other tailings. Problems with electricity supply in South Africa is the major problem. There are plans to set up a processing facility in Brazil.

By Julie Kleis, Director of RBC Wealth Management’s Fiduciary Specialist Team in the British Isles

Being a beneficiary of a trust is often a fortunate position to be in. But inheriting wealth can come at a cost. While a beneficiary may suddenly find themselves free of financial concerns and empowered to support passion projects or charitable causes, they may be inheriting more than just money.

Having worked hard to build a future for their family, wealth creators tend to hold strong views on how their assets should be managed, both during their lifetime and after they have passed away. Yet beneficiaries from younger generations may see things differently.

Julie Kleis

For example, beneficiaries may seek to distance themselves from wealth derived from certain industries or even wish to remove association to the wealth altogether. These reactions to wealth can lead to conflict and emotion.

Disharmony among the beneficiaries themselves can also occur. We recently worked with a family where a wealth creator had established a trust to support their grandchildren’s education. There were three children, however only two of the three had children of their own. Following the death of the wealth creator, the third child, who had not received support from the trust in the same way as their siblings approached the family and trustees to seek compensation for their ‘fair share’.

If such fractures are magnified, families should brace for potentially disastrous consequences, including strained relationships and assets being split and losing value in the process. If the conflict leads to litigation, it’s likely to be damaging and counter-productive, whatever the result.

The key to limiting conflict as a beneficiary is to be open and honest in all communication with the settlor, trustees and other beneficiaries. They should be clear about their goals, values and priorities, and actively listen to others’ points of view.

Trustees play a vital role in managing the conflicting opinions and wishes of beneficiaries. As stewards of the trust’s assets, their goal is to ensure the trust’s wealth is preserved and used for the greater good.

This can mean having difficult conversations. For example, it’s not unusual for the trustees to be asked to take on the sensitive task of telling the wealth creator’s children to sign a prenuptial/postnuptial agreement to prevent the money made during their lifetime becoming embroiled in divorce settlements.

All too often, beneficiaries lack an adequate understanding of what a trust is for and how it works, leading to unrealistic expectations and challenging conversations.

While trustees own the assets and have the ultimate control over what happens to them, they are in fact there to offer beneficiaries advice and support, to encourage their ideas for how to use the wealth, and to help them get what they want from the settlement, as long as it aligns with the principles and direction dictated by the settlor, and the long-term sustainability of the wealth.

A trust is not a legal entity; it’s a relationship. And like any relationship, it requires open and honest communication. By working with trustees openly and honestly, we can find the best way of passing it from generation to generation to benefit the whole family.

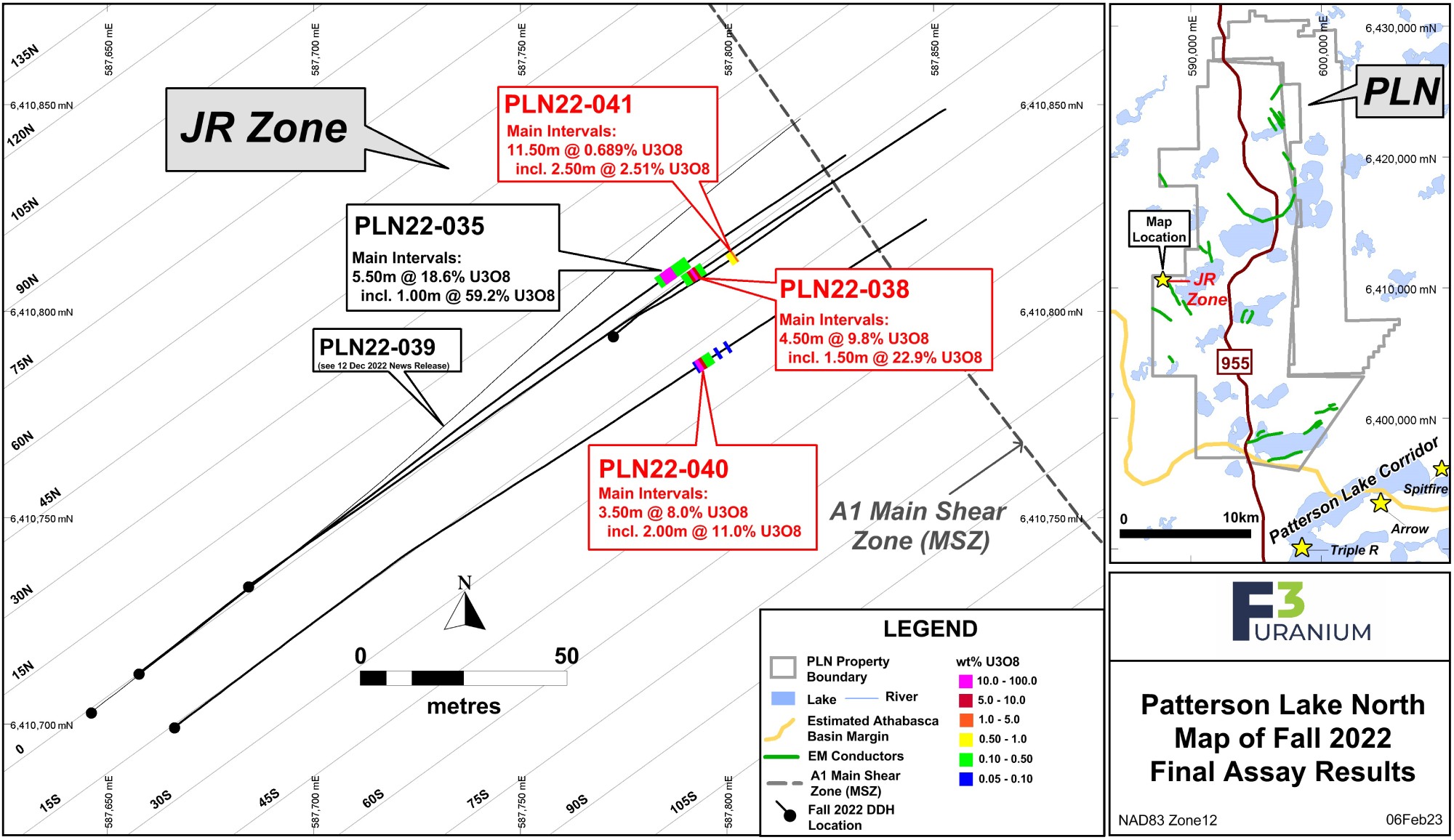

F3 Uranium’s CEO Dev Randhawa’s unerring mission is to deliver growth for his shareholders.

We recently met with the F3 Uranium CEO in London and enjoyed rigorous discussion about the need to increase nuclear power, uranium market dynamics and F3’s recent Patterson Lake North discovery. Randhawa was particularly chipper when discussing their recent high-grade uranium discovery and the significance of the grades encountered.

Dev Randhawa is a massive proponent of nuclear energy’s ability to help meet the world’s future energy demands and feels his company, F3 Uranium, has the potential to be instrumental in securing the uranium supply to facilitate nuclear power generation.

“I believe we need cheap, clean power; that’s what nuclear power is” – Dev Randhawa

Dev Randhawa, F3 Uranium CEO

Despite his very specific interest in nuclear power, Randhawa is realistic about nuclear energy’s place in a diverse energy generation mix.

It is now clear no one clean energy source can solely meet the world’s energy demands. However, nuclear provides many benefits over other forms of energy.

The first benefit of nuclear power the F3 Uranium CEO highlights is cost. Dev explains that once a nuclear energy plant is established, input costs are very low and resultant energy is cheap.

The second relates to the reliability of nuclear compared to renewables sources. As demonstrated here in the UK in recent years, although wind and solar inputs costs are zero, there is no guarantee the sun will shine or the wind blows.

F3 Uranium

F3 Uranium is a uranium project generator and exploration company with 16 projects across the Athabasca Basin in Canada. The region is famous for the world’s highest grade uranium discovery, the MacArthur Lake.

F3’s close proximity to premiere uranium producers means they have access to extensive infrastructure and improved project economics. Dev highlights the benefits of operating in an area near uranium processing plants.

Although all 16 projects have been identified as potential valuation opportunities, the focus is on their Patterson Lake North (PLN) project. The importance of PLN was evident and our conversation with F3 centred on this asset.

In late December 2022, F3 Uranium announced assay results at the PLN project that encountered one continuous 15.0 m interval averaging 6.97% U3O8 including a high-grade 5.5 m interval averaging 18.6% U3O8. In addition, the assay revealed an ultra-high core of 59.2% over 1.0m.

F3 Uranium’s shares soared on the news and Dev detailed why.

The geology in the Athabasca is very different to other uranium-rich region such as Niger or Australia.

Athabasca uranium deposits are typically concentrated in compact formations and inconsistently located along a corridor. This means finding the deposits in Athabasca is trickier than in other jurisdictions, typified by continuous mineralisation formations.

The value in Athabasca uranium deposits lie not in their size, but their grade.

And the F3 Uranium team has a history of high-grade discoveries.

F3 Uranium Technical Team

Randhawa has ensembled a world-class technical team with recent success of commercially viable uranium discoveries in close proximity to F3’s assets.

F3 Uranium’s technical team was instrumental in the Triple R discovery which has the potential to be one of the lowest cost uranium mines in the world. The current Triple R resource is 2.68mt at 1.94% U3O8.

F3 believe an experienced technical team is crucial for shareholder value creation.

Should the current PLN programme be anywhere near as successful as Triple R, the implications for F3’s shareholders will be profound. It will achieve the growth Dev has set out to achieve.

“The question is,” Dev says, “is how many beads of uranium we will find. We’re not going to know that until at least 50 holes have been drilled.”

The drill campaign currently being executed by F3 Uranium is an exciting period for the team and their investors.

F3’s share price reacted positively to early results from PLN and have since retraced, possibly providing an entry for investors seeking to embark on the F3 journey.

The presence of high-grade uranium at PLN has proved they have identified a highly prospective area. The next stage is establishing the size of a potential resource.

We ask the future plans for F3 and his strategy, should PLN prove to be an economically viable uranium producing mine. Dev reminds of us F3’s business model as a project generator but doesn’t rule out a scenario where PLN is developed by F3 beyond the early exploration phase.

The model dictates once F3 has extracted as a much shareholder value from the PLN project using F3’s internal resources, a partner is brought into to continue the journey towards production.

F3’s management have deep experience inking agreements with Korean and Japanese corporation and will know how to secure value in any PLN partnership.

Crystallising the value in PLN will be a milestone for F3 which would provide the liquidity to turn their attentions to one of their other 15 projects.

Tekcapital has secured £2.25m growth capital to be used to accelerate growth of their portfolio companies, namely MicroSalt and Guident.

The oversubscribed placing will provide MicroSalt with £0.6m to help build commercial inventory as the food technology company prepares for their IPO.

Guident will be allocated £1m to purchase autonomous shuttles for their autonomous vehicle safety technology clients. Guident will also further develop their regenerative shock absorbers. Guident’s regenerative shock absorbers capture irregularities in roads and braking forces to help increase the range of electric vehicles.

Tekcapital will use the remaining funds for working capital.

The placing was completed at 16p with £2.25m raised before expenses.

“We are pleased to announce this oversubscribed offering to facilitate the further good progress of our portfolio companies,” said Dr Clifford Gross, Chief Executive ofTekcapital.

Tekcapital shares had traded as low as 16.70p early on Monday but the dip was bought into and TEK shares traded as high as 18p at the time of writing.

Spirits company Rogue Baron (LON: SHNJ) non-exec Charlie Wood acquired an initial 600,000 shares at 0.846p each. He also has an interest in the 1.1 million shares owned by Orana Corporate, where he owns 25%. On Wednesday there was also a trade worth £2,990 at 1.37p a share, which helped to push up the share price, which doubled to 1.25p.

Shares in emissions reducing fuel additives supplier SulNOx Group (SNOX) rose 7.89% to 10.25p after it was announced that four directors have option agreements with 6% shareholder RemNOx Ltd. This would enable the company to acquire a total of 24.08 million shares at 30p each between 6 February and 28 February. That would mean that RemNOx would own 29.9% of SulNOx. Finance director Steven Cowin has given notice and will leave the board at the end of March 2023.

Digital asset investor Kasei Holdings (LON: KASH) raised £500,000 at 12p a share from Aalto Capital. This is a 12.5% stake. There were eight trades during the week, all worth around £50,000 each. The share price improved 7.41% to 14.5p.

Energy supplier Good Energy (LON: GOOD) has launched a new smart export product for Feed-in Tariff for FiT customers, which could help them to earn more from electricity they generate. There are plans for a new domestic export tariff for households in the next few months. The share price rose 3.13% to 165p.

==========

Fallers

Hemp and cannabinoid products supplier Yooma Wellness (LON: YOOM) shares continued to decline following the previous week’s news concerning the restructuring of the business due to the depressed market conditions. Unprofitable activities have been wound down and management is still trying to come up with a new strategy. Yooma Wellness requires more cash and other operations may need to be sold. If not, then there could be insolvency proceedings. The share price slumped 44% to 1.75p.

Trading in Pioneer Media Holdings Inc (LON: PNER) will end on the Aquis Stock Exchange on 9 March. Ahead of that date, the share price fell by two-fifths to 7.5p during the week. Trading will continue on the NEO Exchange in Canada.

EDX Medical Group (LON: EDX) acquired Torax Biosciences for the issue of 1.67 million shares at a notional 6p each. The share price fell 11.8% to 3.75p. Torax provides development and pilot scale fabrication of immunochemistry-based assays and diagnostic testing services. The experienced team at Torax was an attraction.

Marula Mining (LON: MARU) signed a co-development and relationship agreement with a subsidiary of South African mining and investment company Q Global Commodities, which had already agreed to subscribe £3.75m for shares. Q Global chief executive will become Marula Mining chairman, subject to regulatory approval and admission to AIM. Marula Mining is expanding its graphite interests through the proposed purchase of a 75% stake in ten licences comprising the Nyorinyori graphite project in Tanzania. The share price fell 4.63% to 5.15p.

Clontarf Energy (LON: CLON) is forming a joint venture with US-based NEXT-ChemX Corporation, which covers the deployment and marketing of the latter’s direct lithium ion extraction technology in Bolivia. There is limited water and energy consumption with this technology. The share price soared by 129% to 0.172p. Pilot testing and extraction starts in March. Clontarf Energy will contribute $500,000 towards the pilot plant for exclusive use of the technology and when that payment is made it will also issue 385 million shares to the partner. NEXT-ChemX will issue $500,000 of shares to Clontarf Energy in its next fundraising. A further 500 million Clontarf Energy shares will be issued to NEXT-ChemX on achievement of certain milestones. NEXT-ChemX has the right to invest £250,000 at 0.065p/Clontarf Energy share.

Inland Homes (LON: INL) has renegotiated banking covenants. The HSBC covenants relate to tangible net worth and gearing. They will revert to the original level from the end of June. A waiver of a historic breach of gearing on the Secure Trust loan has been secured and extended to the end of March. The share price recovered 79.6% to 15p. That is the highest it has been for more than three weeks. Total borrowings are £48.7m.

Medical devices developer Creo Medical (LON: CREO) raised £28.5m from the placing at 20p a share, which was more than the £25m initially targeted. With up to £5.2m more to come from the open offer, Cenkos believe that this is enough cash to fully commercialise the current product portfolio. The cash will be used for further development and commercialisation of Creo Medical’s minimally invasive electrosurgical devices. Revenues of £100m are forecast by 2027. The share price jumped 38.8% to 34p.

Promotional goods supplier software platform provider Altitude (LON: ALT) says results for the year to March 2023 will be much better than expected. Zeus has upgraded its pre-tax profit forecast from £500,000 to £800,000 and that is the second upgrade in three months. The US promotional products market is strong and favourable exchange rates helped. The share price jumped 26.1% to 42.25p. That is the highest the share price has been since June 2021. MI Chelverton UK Equity Growth Fund trimmed its stake from 5.47% to 4.9%.

==========

Fallers

PetroNeft Resources (LON: PTR) lost some of the previous week’s gains after chief executive Pavel Tetyakov was revealed as a potential buyer for its Russian assets. The share price slumped 47.6% to 0.55p, which is not much higher that before the announcement. Any deal will require shareholder approval. The current market capitalisation of £5.9m is well below the company’s $42.7m NAV at the end of June 2022, which includes loans to WorldAce Investments.

Esports company Gfinity (LON: GFIN) raised £2m at 0.15p a share, having originally sought £1.5m. The cash should last for 12 months. Technology platform Athlos still requires a strategic partner and there is enough funding for this for around four months. If not, then it could affect the restructuring and other plans for the rest of the business. At 0.1575p, down 33%, the current share capital is valued at Gfinity at £2.1m. Each placing share comes with a warrant to subscribe for one share at 0.15p and these warrants are exercisable between six and 18 months after the placing shares are admitted to AIM.

Deferral of contracts by clients has led to forecast downgrades for Jaywing (LON: JWNG) and 2022-23 pre-tax profit expectations have been more than halved to £1m, while next year’s forecast has been slashed from £3.7m to £2m. The digital marketing services provider won an Australian online education services contract which helps to offset some of the decline in forecast revenues in 2023-24. The share price slumped 26.9% to 5.025p.

Mkango Resources (LON: MKA) raised £3.5m at 12.5p and this will fund further development of the Songwe Hill rare earths project. The share price slipped 22% to 12.875p. Talks with potential funders for the project continue. Mkango Resources will also provide a €2.5m loan facility in HyProMag, which is developing a rare earth recycling production facility in Baden-Wurttemberg. The company’s stake in HyProMag could increase to 66.8%. Chief executive William Dawes acquired 400,000 shares at 12.95p each and 400,000 shares at 12.75p each. He owns 4.42%

Glencore, Legal and General, British American Tobacco, BP, and IAG could constitute the best FTSE 100 stocks to watch next week.

The FTSE 100 struck a record high this week, pushing above the symbolic 8,000-point high watermark for the first time ever. This performance tops an exceptional 2022, where the UK’s premier index outperformed virtually every other international peer, rising by 1% while many others declined into a bear market.

People living in the UK may be feeling perplexed — multiple dire economic warnings alongside a disastrous cost-of-living crisis are leaving much of the population in financial purgatory. However, while FTSE 100 companies are London-listed, they don’t rely too much on the country’s economic situation. By comparison, FTSE 250 businesses which are far more domestically focused fell by nearly 20% last year.

So, what’s driving the FTSE 100’s record growth? There are five primary factors, though there are also several esoteric elements that go beyond the scope of light weekend reading.

And these factors feed into what could be the five best FTSE 100 stocks to buy next week.

Best FTSE 100 stocks

1. Glencore (LON: GLEN)

First, and possibly most importantly, FTSE Russell data shows that the 100 largest UK-listed companies derive circa 82% of their income from overseas. This means that the likes of international giants like HSBC or AstraZeneca are reliant on the global economy, which while admittedly not in the prime of life, is doing far better than the UK, especially as wholesale energy costs fall sparking hopes that inflation has peaked.

Further, these earnings are usually earnt in US dollars — and because sterling has depreciated against the global currency over this past year, these earnings become inflated when converted back into pounds.

Glencore is a globally significant miner benefitting from the mining supercycle. FY22 saw GLEN make record pre-tax profits of £28.2 billion as coal and oil prices rocketed. Despite a myriad of scandals, the FTSE 100 company is promising to pay out £5.9 billion to shareholders. And unlike other miners on the index, it’s heavily invested in battery metals mining, making its future profits to some extent future-proof.

A severe global recession causing demand destruction, continued legal problems, and an overreliance on Chinese demand remain key risk factors in 2023.

2. Legal & General (LON: LGEN)

Second, the FTSE 100 has a strong reputation as the home of aristocratic dividend companies, which is attractive to investors looking for passive income, and a place to batten down the hatches as growth stocks take a hammering.

For context, FTSE 100 companies only rose by 1% last year because they paid out £79.1 billion in dividends and £50 billion in share buybacks. These are typically fully mature companies that do not need to invest in growth. In fact, Schroders analysis shows that between 1999 and 2019 the index increased by an average of 0.4% per annum, but returned a total of 122% over the vicennial when dividend returns are factored in.

While there are higher dividends available on the FTSE 100, Legal & General is rare in that it sets out dividend plans in advance — and expects to grow its dividend at low-to-mid single digits in percentage terms until 2025, with the yield currently at a very respectable 9.2%.

Cumulative dividends are expected to reach between £5.6 billion and £5.9 billion by 2024, and LGEN seems likely to deliver on this ambition, with a financially secure Solvency II capital ratio of between 225% and 230%. And with 10 million customers, the well-known brand is likely to experience growth in the longer term as ageing populations seek out its pensions and annuities products.

The sector is ultra-competitive, but LGEN has stood the test of time: there’s a reason it’s consistently one of the most popular FTSE 100 dividend stocks on the UK market.

3. British American Tobacco (LON: BATS)

Third, the FTSE 100 is dominated by oil, banking, tobacco, and mining stocks which account for a huge proportion of its total market value. The in joke among UK investors is that the UK’s best offering is a ‘dinosaur’ index, with companies focused on sectors that have remained relevant for centuries.

But what’s not a joke is their defensive qualities which is a primary reason for the consistent dividends. And these dividends could well increase further as oil prices remain historically elevated, net interest margins rise, and the mining supercycle continues.

For context, the NASDAQ 100 is the polar opposite, filled with the tech titans that make all the headlines — including Apple, Alphabet, Amazon, Microsoft, Meta, and Tesla — which rocketed in value during the days of ultraloose monetary policy and are now akin to a forest of overlarge houseplants on restricted water rations.

Of course, British American Tobacco is experimenting with — and promoting — new tech such as vaping, but the reality is that it makes its money from cigarettes. And smokers are addicted to nicotine, forgoing food for cigarettes if need be. A 7% dividend yield is made possible by FY22 revenue, which rose by 7.7% year-over-year to £27.7 billion.

There are ethical concerns, and the key risk is stronger clampdowns on its products, particularly in the US.

4. BP (LON: BP)

Fourth, it may not have escaped your notice that energy bills are a little higher than was the case in the past. Despite falling from previous highs, Brent Crude is still trading for around $83/barrel — and buoyant hydrocarbons prices induced by the pandemic reopening and intensified by the Ukraine War are significantly increasing the profits of the two FTSE 100 oil majors, BP and Shell.

Both companies have seen serious share price increases over the past year, and both generated record profits in FY22 — Shell to the tune of $40 billion, and BP $28 billion. Moreover, UK windfall taxes are something of a non-issue — combined taxes on UK profits are already at 75%, and neither company generates more than 10% of its revenue in the North Sea.

BP shares probably now have more room to grow than Shell, which currently ranks with AstraZeneca as the two most valuable companies on the index. UBS has a 630p target on the major, representing an upside on the current 564p share price.

As a caveat, Brent went negative for the first time in 2020. Peace in Ukraine, a return to lockdowns in China, a severe global downturn, or 1980s-style demand destruction are all in play.

5. IAG (LON: IAG)

Fifth, while most FTSE 100 companies are non-reliant on the UK’s economy, it is fair to say that things are looking up compared to only a few months ago. The disaster of the Truss-Kwarteng mini-budget is in the rear mirror, annual domestic energy bills will not hit the previously anticipated £7,000, and the bank rate is expected to increase to less than 5% as economists think inflation has peaked. Further, the Bank of England has reduced its recession forecast to just one year, down from two — though its divided MPC and poor forecasting track record leaves a lot to be desired.

Of course, inflation remains in the double-digits, it seems as though every sector is on strike, and the lagging effect of higher interest rates on consumer credit and mortgages could cause serious damage to consumer confidence through 2023. OECD data shows that UK investment remains below its 2016 level, and the IMF thinks that the country will fare worse economically than any other developed country in 2023. Then there’s the highest tax burden since Suez — maybe not so positive after all.

However, it’s sunshine and roses for IAG shares, which have risen by 30% year-to-date to 167p. With full-year results due on 24 February, investors have looked to FTSE 250 competitor easyJet for inspiration, which up 53% year-to-date, has performed even better.

The rival’s Q1 results saw revenue increase by 83% to £1.47 billion as pent-up travel demand was finally unleashed. The company expects to swing to profit for its full financial year, and both are now enjoying the opportunity to fight for further market share comprising Monarch and Thomas Cook’s former clientele.

Like always, there are risks. Interest rates are rising, and the company took on substantial debt to keep afloat during the pandemic. Fuel costs are likewise sky-high (forgive the pun), and if the recession is deeper than expected, scarring could be damaging.

But as much as investors might wish it, even the FTSE 100 is not risk free.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

After week dominated by UK corporate updates and inflation data from the US and UK, concern around the trajectory of interest rates hurt stocks on Friday.

Markets have very quickly priced in a more dovish approach to monetary policy as inflation begins to trend to the downside. However, investors hoping for slower rate hikes were dealt a blow by Federal Reserve members yesterday who suggested the Fed could indeed revert to 50bps rate hikes.

The Federal Reserve has two mandates; to achieve maximum employment and maintain price stability. The Fed has a 2% inflation target and US CPI inflation is currently 6.4%.

Couple this with the bumper 517,000 jobs added to the US economy in January, there is no real justification for slowing interest rates now.

This is at odds with recent moves in equity markets and the FTSE 100 dipped 0.2% to 7,990 in midday trade on Friday.

“It was only days ago that investors seemed confident we would only get one or two more small increases in US interest rates and then the Federal Reserve might start cutting rates later in the year. The rhetoric has now changed,” said Russ Mould, investment director at AJ Bell.

“Two Federal Reserve officials yesterday spoke in favour of a 50 basis-point interest rate hike in March from the US central bank. That took the market aback, sending US shares into reverse, and that negativity extended across Asia and Europe on Friday.”

“A rate hike of this proportion could easily stop this year’s stock rally in its tracks. Investors might have become too complacent, assuming that inflation is going to fall and the Fed will no longer have a reason to stay aggressive on rate hikes.”

Broad declines

The FTSE 100 declines were broad with 65% of constituents trading negatively at the time of writing, although individual losses were relatively benign.

NatWest was by far the biggest faller after raising concerns about their earnings potential in the year ahead. NatWest shares were down 6% at the time of writing and Lloyds shares fell in sympathy.

Segro was the top gainer after the logistics property company said pretax profit increased 8%.