Narrowband radio frequency communications networks developer CyanConnode (LON: CYAN) is raising £5m at 17p a share in order to strengthen the balance sheet and stock up with long lead time components. Three directors are investing £110,000 in the placing, which is at the current market price.

The share price has risen by more than 50% over less than four months, providing an opportunity to raise cash to finance expansion. In October 2022, there was a £500,000 share subscription at 12.25p a share. Earlier in the year, £2m was raised at 14p a share. In June 2021, £3.15m was generated from a placing and subscription at 9.5p a share.

CyanConnode has a strong order book and is participating in tenders for 75 million smart meters in India, which is equivalent to £1bn of revenues. Management hopes to win between 20 million to 30 million orders over five years. There are also opportunities in other countries.

In the six months to September 2022, revenues fell from £4.08m to £1.35m. The operating loss doubled to £2.4m. There was a £114,000 cash outflow from operations and there was more than £1m in the bank at the end of September 2022.

Revenues have already reached £5m in this financial year thanks to strong trading since the interims. The cash generated has already been invested in inventories.

Full year revenues of £12.5m are currently forecast and this is expected to rise to £16m in the year to March 2024, when a small profit is forecast.

The FTSE 100 gained on Monday as investors prepared to receive major economic updates later this week, including US GDP and inflation.

After a busy period of company results and updates, equity investors will be bracing for the macro consequences of insights into global economic growth from the US.

“The FTSE 100 ticked higher on Monday without suggesting it would threaten the all-time high which it briefly flirted with before a sell-off at the end of last week,” said AJ Bell investment director Russ Mould.

“The big economic announcements come on Thursday and Friday as the US releases GDP figures for the fourth quarter and core inflation numbers from the world’s largest economy are also released.”

“These will offer insight into two key and related factors which are grabbing the market’s attention right now. First, will the US avoid a deep recession and second, will inflation ease sufficiently to allow the Federal Reserve to ease up on interest rates before it has inflicted too much pain on businesses and consumers?”

FTSE 100 gains

The FTSE 100 was gaining with the usual high-beta suspects leading the index higher. Ocado, which has a beta of 1.75, was the top gainer, up 2.3%, at the time of writing. Ocado has become one of the fastest moving FTSE 100 constituents and is now regularly the top riser or faller.

St James’s Place was the FTSE 100’s top faller after the wealth manager’s rating was cut by analysts at both Barclays and HSBC. Barclays now has a price target of 1,507p with a hold rating. St James’s Place was down 2.5% to 1,203p at the time of writing.

Online fashion retailer Sosandar (LON: SOS) has secured its latest wholesale partnership with Sainsbury, which will sell part of its range of clothing and accessories online and in stores later in the year. Sainsbury is growing market share in non-food markets. Existing partners include NEXT and John Lewis. This will not have a significant effect on the year to March 2023 when revenues of £42.5m and a move into profit is forecast. The 2023-24 forecast does not include any contribution from Sainsbury and pre-tax profit of £3.1m is already forecast on revenues of £58m. The share price rose by 9.52% to 23p.

Intercede Group (LON: IGP) has sparked further upgrades with its latest trading statement. The identity management software company says it could get better if further sales close before the end of March 2023. Forecast 2022-23 pre-tax profit has been trebled to £600,000 on a 6% upgrade of revenues. The share price is still much lower than 18 months ago, but it recovered 20.4% to 68p.

Energy transition services company Getech Group (LON: GTC) says 2022 revenues were ahead of expectations at £5m and there is a record order book of £4.6m. Transitional petroleum contributes two-thirds of revenues with the rest coming from critical metals. There was cash of £4.3m at the end of 2022 and that is enough for current requirements. There are plans to raise more cash from selling Kitson House, but the disposal has been delayed. There are discussions with strategic investment partners. The share price increased 10.9% to 15.25p.

Invinity Energy Systems (LON: IES) says existing contracts underpin growth in in 2023. There are £22m of vanadium flow battery systems due for delivery in 2023 and a further £7.4m order book for 2024. There was £5.1m in the bank at the end of 2022. Pilot projects with Siemens Gamesa should begin in the summer and a next generation product should be available in the first half of 2024. The share price is 11.5% ahead at 43.5p.

Surgical Innovations (LON: SUN) says 2022 revenues will be 5% ahead of expectations at £11.3m and this should enable the surgical instruments supplier to breakeven as gross margins recover. The UK grew significantly and momentum in the fourth quarter is carrying on into this year, although trike action could hit demand. International sales should continue to recover. The share price is 9.38% higher at 1.75p.

Vast Resources (LON: VAST) expects litigation in Zimbabwe relating to diamond joint ventures to be concluded this month. This could lead to the release of a parcel of 129,400 carats of rough diamonds. This litigation started in 2009. The share price is 5.26% ahead at 0.2p, having been 0.24p earlier in the day.

Podcast content platform operator Audioboom (LON: BOOM) increased revenues by one-quarter to $75.5m in 2022. However, this is lower than forecast and pre-tax profit has been downgraded to £3.2m, compared with £2.7m in 2021. Advertising spending has been weak because of economic conditions. Net cash was better than expected at $8.1m. The share price declined 6.03% to 397.5p.

Textile wholesaler Leeds Group (LON: LDSG) reported flat interim revenues of £15.6m, but the loss was more than halved at £224,000, although that includes a £138,000 gain on a property sale. Net debt is £6.13m, but that includes cash that will be used to pay the creditors of subsidiary KMR, which is in the hands of an insolvency administrator. The share price fell 7.14% to 13p.

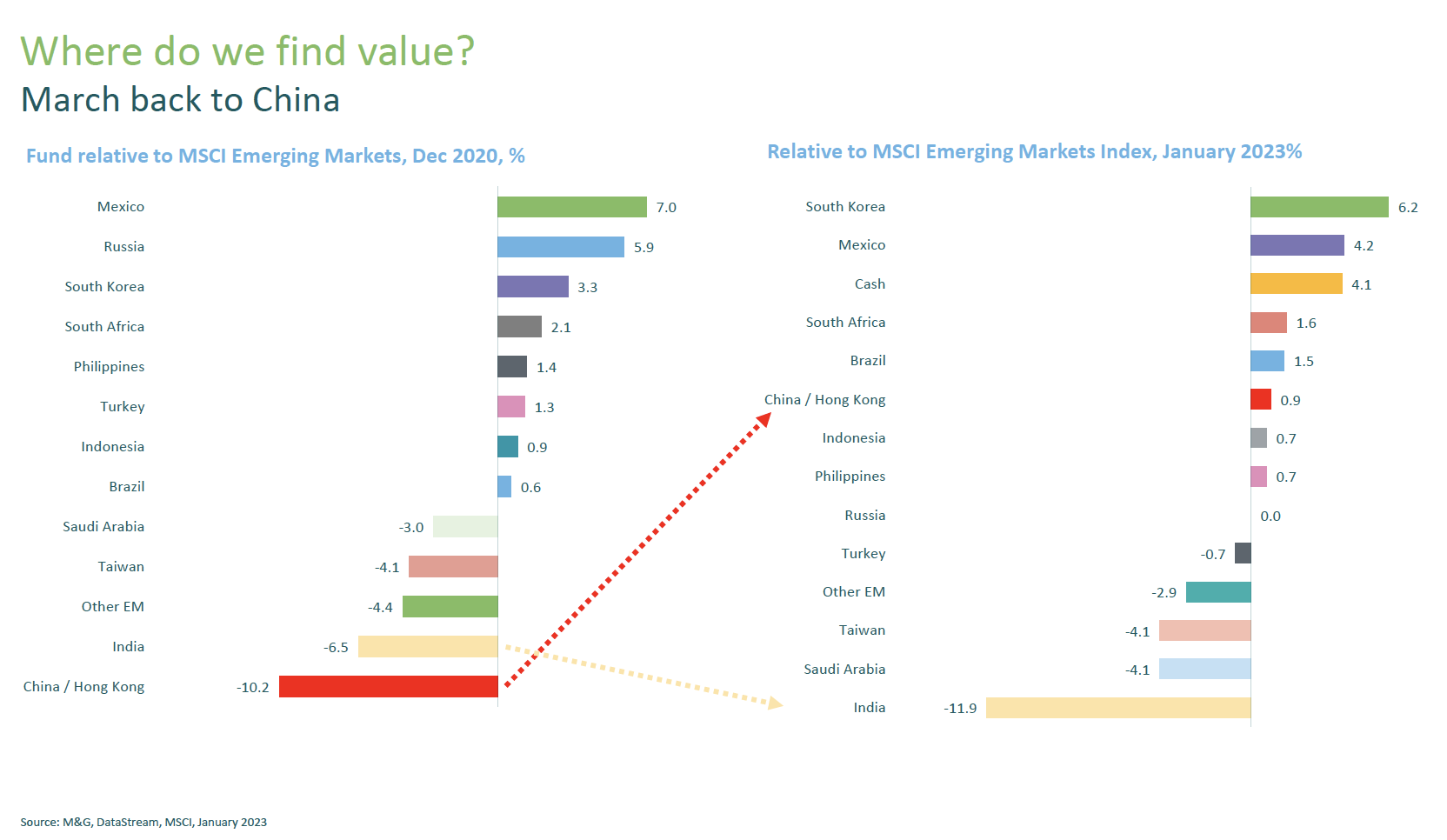

The M&G Global Emerging Markets Fund is increasing exposure to China and sees the world’s second largest economy as a potential source of outperformance in the coming year.

As we start the Chinese New Year – the Year of the Rabbit – China is dominating headlines and gaining the attention of investors.

The end of Zero COVID policies promises to boost the Chinese economy and provide support for mainland and Hong Kong equities. Indeed, the leading Hong Kong indices have rebounded some 40% from last year’s lows.

The dramatic shift in the approach to COVID highlights the Chinese leadership’s desire to pursue growth. Their willingness to roll back COVID policies they had previously been steadfast in delivering has demonstrated economic health is still the CCP’s main priority.

Having scrapped lockdowns and restrictions at the end of last year, the Chinese New Year may mark a new chapter in the Chinese economy and returns for investors in Chinese equites.

Increasing China Exposure

Speaking at an M&G event held in London last week, Fund Manager Michael Bourke alluded to a rotation towards China in their portfolio as a result of the Chinese reopening and valuation of Chinese equities.

The extent to which managers of the M&G Global Emerging Markets Fund have increased their exposure to China is illustrated below. From being underweight China compared to the MSCI EM benchmark by 10.9% in December 2020, the fund is now overweight China by 0.9%.

Being significantly underweight China through 2021 and early 2022 meant the M&G Emerging Markets Fund significantly outperformed the benchmark. Sharp losses in Chinese tech names were a major drag on Emerging Markets over the past 18 months and avoiding the sector helped produce M&G’s outperformance compared to the benchmark.

However, the losses in Chinese stocks are now being seen as major opportunity – and a sustained recover in Chinese equity may provide the M&G team with third consecutive year of outperformance.

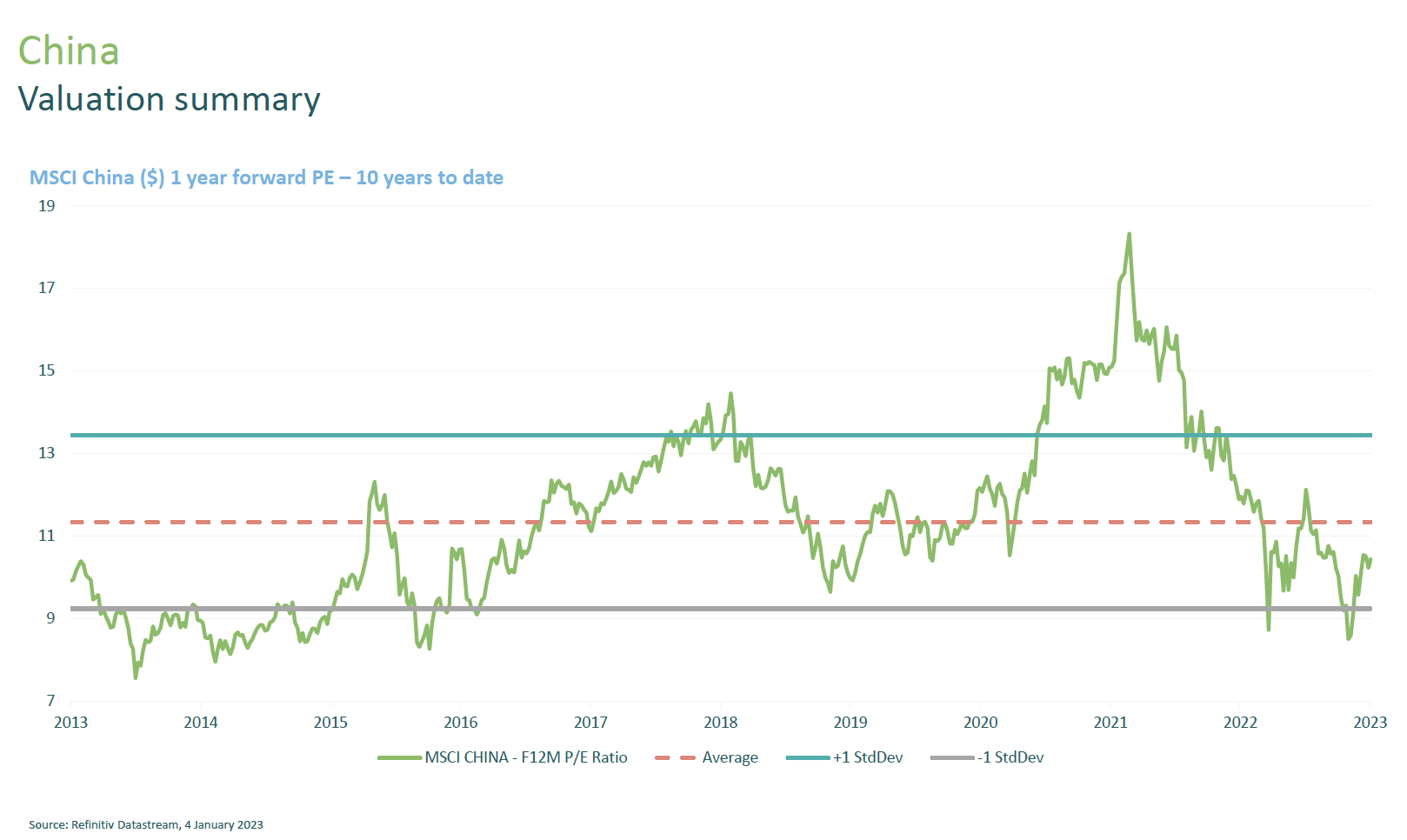

The valuation argument is compelling. Bourke explained that Chinese equity valuations have spent a considerable period trading one standard deviation away from the average price-to-earning ratios, and are ripe for a rebound.

Alibaba accounts for 3.9% of the M&G portfolio while Chinese finance conglomerate Ping AN Insurance Group earns a 3% weighting.

In addition to China, Bourke detailed their interest in Mexico and South Korea, while saying they saw little value in India currently.

Mexico’s proximity to the US and manufacturing capabilities has driven a 4.2% higher weighting in the M&G EM portfolio compared to the benchmark.

South Korea’s traditional tech names and semi conductor companies have been swept up in the global tech sell off are also providing fairly attractive valuations.

Samsung and Taiwan Semiconductor were the top two holdings as of 31st December.

Producing material growth – that is exactly what Plant Health Care is all about, not only in helping farmers globally to sustainably grow more, but also in building up its own sales and profits.

The Business – Cost-effective products for sustainable agriculture

Established way back in 1995, the Holly Springs, North Carolina-based Plant Health Care (LON:PHC). Plant Health Care leading provider of novel peptides for plant protection to global agriculture markets

The company offers its various products to improve the health, vigour and yield of major field crops, such as corn, soybeans, potatoes and rice, and specialty crops, such as fruits and vegetables. As the impact of climate change is increasingly felt throughout the globe, for example, the growing problem of drought in certain regions, then the need for increase yield becomes critical, increasing demand for Plant Health Care’s solutions.

It operates globally through agreements with major distributors of agricultural products.

Its innovative, patent-protected biological products help growers to protect their crops from stress and diseases, and to produce higher quality fruit and vegetables, with a favourable environmental profile.

It offers products to enhance the yield and quality of crops, such as corn, soybeans, citrus, sugar cane, and rice, as well as fruits and vegetables.

The company provides Harpin aß, a recombinant protein, which acts as a bio stimulant to enhance the yield and quality of crops; and Saori, a vaccine for plants that promotes healthy growth of soybeans and helps them fight disease. Saori is the first product from the company’s PREtec (Plant Response Elicitor Technology) platform. Derived from natural proteins, PREtec is an environmentally friendly technology which stimulates crop growth and ability to withstand a variety of abiotic stresses as well as to improve disease control, plant health and yield. PREtec is compatible with mainstream agricultural practices.

The Products– Strong pipeline

Using environmentally friendly peptides derived from natural proteins, its innovative, patent-protected products help growers to protect their crops from stress and diseases, and to produce higher quality fruit and vegetables, all while being compatible with mainstream agricultural practices.

Plant Health Care’s core patented products act as “vaccines for plants”, making plants healthier, better able to resist disease and stress, thereby improving crop yield and quality.

Harpin aß

Plant Health Care’s Commercial business is driven by sales of Harpin αß, a recombinant protein which acts as a powerful bio-stimulant, promoting the yield and quality of crops. The group sells Harpin αß through specialist distributors around the world. In Mexico, the group also distributes third-party biological products.

Sales of the group’s Harpin αß product increased by 55% in 2021, as market shares grew in core markets; the Commercial business is profitable and cash generative.

PREtec

Plant Health Care’s PREtec (platforms are generating numerous promising products.

The group is currently focusing on three products targeting very large market opportunities with a value of more than $5bn. These products are under current evaluation with six potential commercial partners.

The PREtec technology platform is proving to be a reliable source for new products. The pipeline is poised to launch one new PREtec product each year going forward.

The first PREtec product, Saori™, was launched in Brazil in 2021, through PHC distribution partner Nutrien, generating a very positive response from growers.

Saori™ promotes healthy growth of soybeans and helps them fight disease; Brazilian soybean growers spent $2.5bn on fungicides to control disease in 2021, so this is a huge opportunity for Saori™. [Recently announced further plans in Brazil to expand Saori into sugar cane and coffee for disease control.

The Markets

Plant Health Care plc, provides agricultural biological products and technology solutions in the Americas, Mexico, and internationally.

The group has negotiated and tied-up distribution agreements with major sector players globally.

It recently registered Harpin ab in France, which will enable expansion into the European market, considered to be the biggest globally for biological products.

Early in January the company signed an agreement with Novozymes South Asia for the exclusive distribution of Harpin ab for sugar cane production in India, first sales of which are expected in the second half-year of 2023.

Growth Strategy

The group intends to drive revenue in the short term by focusing on distribution of Harpin αβ by aligning with large distributors with broad market access. It plans to expand sales in broad acre crops where Harpin αβ provides the most benefit to farmers, including sugar cane, corn, soy, citrus, rice, almonds and grapes.

With the launch of Saori™ in Brazil, it has gained access to the largest soybean market in the world.

The target is to launch at least one PREtec product in a major market every year. Saori™ in Brazil in 2021 was the first, followed by the launch of PHC279, for control of orange rust in sugar cane and coffee leaf rust, into specialty crops in the USA with PHC distribution partner Wilbur-Ellis.

PHC949, a seed treatment for control of root-lesion nematode in soybean, has recently been submitted for registration approval.

It has made a significant capital investment by building a pilot plant facility in its Seattle location, allowing the production of peptides on a pilot scale and assisting with developing and optimising manufacturing methods.

It has also secured a production facility for PHC279, which led to the achievement of volume cost targets.

There is an extensive library of PREtec peptides, which can be further expanded. PHC is well positioned to take a lead in consolidating this fragmented sector, due to its strong portfolio and market access.

The group has now been granted fifteen global patents for PREtec peptides and numerous filings are in the process of being reviewed around the world, enabling the building up of its intellectual property portfolio. .

The company’s products have been classified as “low toxicity” products and qualify for ‘fast track’ regulatory approval in the USA and Brazil.

The Share Capital (as at November 2022)

There are 304,662,482shares in issue.

Larger holders include Ospraie AG Science (17.88% of the equity), Richard Griffiths (13.95%), Janus Henderson (9.92%), Lombard Odier (7.41%), Scobie Ward (5.72%), and Management, Directors and related parties (2.11%).

In addition, there some 33,291,306 Stock Options alive, subject to various performance conditions, such as share price hurdles.

Totally fully diluted, there would be some 337,953,788 shares in issue.

Analyst Opinion – the shares are a Buy, looking for 33p

Ahead of the group issuing a Trading Update and Investor Presentation on 6th February, together with any further guidance being given by the company, analyst John-Marc Bunce at Cenkos Securities is rating the group’s shares as a Buy.

His estimates for the year to end December 2022 are for revenues to have improved nearly 36% to $11.4m ($8.4m), helping to substantially reduce the group’s pre-tax loss by a third from $4.6m to $3.0m.

For the current year Cenkos Securities, the group’s NOMAD and Broker, is looking for sales to rise over 39% to $15.9m, severely reducing the company’s loss to just $0.3m.

It is in the coming year that the broker envisages a significant advance by the business, with expectations of a 56% revenue increase to $24.5m, generating adjusted pre-tax profits of $5.2m, worth 1.6c per share in earnings.

The analyst states that “we see Plant Health Care as well positioned in the agritech industry and highly undervalued compared to its intrinsic value and peers” giving a 33p price target for the group’s shares.

Conclusion – substantially undervalued

Following years of development this group now has massive upside potential.

As this group aids farmers in increasing crop yields in the face of climate change and growing populations, its model of distributing globally its products through major partners will shine through.

Today it is a leading provider of proprietary biological products for agriculture, with itspeptides poised to enter large markets.

In the meantime, its strong cash reserves and strict control of expenses should be sufficient to enable it to boost global sales over the next year or so, bursting the group into cash breakeven in 2024.

By the end of next year this company could well be reporting sales of over $25m, have some $5.5m net cash and making $5.2m profits.

With its shares at around the current 11.5p, the group is substantially undervalued at only £36m.

England’s leading and largest winemaker, the £60m Chapel Down Group (AQSE:CDGP), has reported fizzier trading in its full year Trading Update for 2022.

Based in Kent, in the heart of the Garden of England, Chapel Down produces an award-winning range of sparkling and still wines of the highest quality and which the winemaker believes offer the best expression of England.

A record 790,000 bottles of traditional method sparkling wine were sold to its customers in 2022 up from 522,000 bottles in 2021.

Net sales revenues were up 10% at £15.64m (£14.72m), reflecting a strong growth in traditional method sparkling wine sales, some 70% by value.

Group CEO Andrew Carter stated that:

“We are delighted by the sales performance achieved in 2022, driven by our premiumisation strategy which supported stellar growth in our traditional sparkling wines sales.

We look forward to updating the market on the continued growth in the profitability of our business in our full year audited results.

This performance, and the excellent harvest we enjoyed in 2022, means we carry momentum into 2023 and are on track to meet our target of doubling the size of our business by 2026.”

Analyst Opinion

Sahill Shan at Singer Capital Markets considered that the year end update news was excellent, noting the stellar growth of 53% in the higher margin sparkling wine category being the stand out feature.

It builds upon the positive harvest news given out in October and shows growth has accelerated in the second half of the group’s year.

Conclusion – medium-term investment

The group’s shares, backed by net assets of at least 20p a share, are quoted on the Aquis Exchange, and have been as low as 20.5p in the last year, they are currently trading at around 38p. An interesting but medium-term investment.

Battery technology developer Ilika (LON: IKA) plans to complete a manufacturing licence deal with Cirtec Medical, which will enable a significant boost in production for the Stereax miniature battery. There is plenty of cash in the bank for Ilika’s immediate requirements and it will be able to satisfy demand from medical companies for the battery.

There are already customers interested in the Stereax battery with initial orders from 18 medical companies. Once the full details of the deal are sorted out, Cirtec Medical can set up production of Stereax cells and it will pay a royalty to Ilika. T...

Tap Global (LON: TAP) continues to rise following the previous week’s completion of its reversal into Quetzal Capital last week. There was £3.1m raised at 4.5p at the same time, even though the market price had not been that high since May last year. Chief executive David Carr acquired 190,000 shares at 4.1p each and finance director Anthony Quirke bought 135,135 shares at 4.4p each. The share price ended the week up 11.4% to 4.9p.

Quantum Exponential (LON: QBIT) had £2.48m in cash out of net assets of £4.85m at the end of October 2022. There was a cash outflow of £313,000 in the previous six months. The share price increased by 7.14% to 1.5p.

Oberon Investments Group (LON: OBE) is acquiring 63% of Logic Investments Ltd, which provides back office services to investment managers. Logic has funds under management and administration of more than £275m and Oberon Investments will merge its own back office operations with Logic. A placing raised £1.75m at 3.5p a share. Chairman Alex Hambro subscribed for 1.14 million of the shares, taking his stake to 1.64 million shares. The cash will be used to accelerate growth. The share price rose 4.62% to 3.4p.

Guanajuato Silver Company Ltd (LON: GSVR) has restarted processing at the Cata mill at the Valenciana mine. The initial processing rate is around 8,000 tonnes/month. The share price edged up 1.92% to 26.5p.

==========

Fallers

Healthy snacks supplier S-Ventures (LON: SVEN) says full year revenues were £8.7m, but the inability to obtain ingredients hampered sales income. The operating loss is £2.6m. The revenues were one-fifth down on initial expectations for the year to September 2022. Supply problems have eased, and price rises have helped to offset higher costs. The share price slumped 30.9% to 11.4p.

Marula Mining (LON: MARU) has appointed Geofields Tanzania to commence copper exploration at the Kinusi copper project, where Marula Mining owns a 49% interest, and £80,000 has been raised from a warrant exercise. Initial exploration results should be published in the second quarter of 2023. The share price fell 16.5% to 5.8p.

Hydrogen Future Industries (LON: HFI) is investing in hydrogen production facilities developer Tower Green. It has spent £100,000 in cash and shares on a 20% stake and has the right to invest a further £50,000 for another 10% stake. Tower has an agreement with Element 2 to supply hydrogen fuel to fleet operators. Hydrogen Future Industries has developed wind-based hydrogen production systems. The share price slipped 3.77% to 6.375p.

On Friday, there were the second highest trading volumes in Plexus Holdings (LON: POS) shares since flotation in 2005. There were 13.57 million shares traded. The most significant trade was worth £11,200. The highest level of trading was one year ago. The share price jumped 155% on the week to 4.15p.

China-based Hainan Mining is funding the Bougouni lithium project that is wholly owned by Kodal Minerals (LON: KOD). A $100m investment will be made into a joint venture providing Hainan Mining with a 51% stake. The work on the construction of the mine will be overseen by Kodal Minerals. Hainan Mining is also subscribing $17.75m for a 14.8% stake in Kodal Minerals and that money will be spent on other projects. The share price jumped 58.3% to 0.3925p.

Grafenia (LON: GRA) is acquiring care home management software provider Care Management Systems for £3.5m. The developer gets 95% of its revenues from recurring fees and made an operating profit of £120,000 last year. Grafenia is seeking software acquisitions to diversify the group. Grafenia raised £2.55m after expenses from a bond issue with a nominal value of £3m. The share price is 37% ahead at 7.875p.

Harland & Wolff (LON: HARL) has recovered some of its recent share price loss following the confirmation of the £1.6bn contract for the Fleet Solid Support Programme. Harland & Wolff is part of the consortium, and it still has to complete negotiations for the sub-contract work. The share price rose 27.5% to 20.15p.

Caspian Sunrise (LON: CASP) says that its drilling vessel has won a tender to drill a deep well in the Caspian Sea. The share price is 21.5% higher at 5.4p.

==========

Fallers

The first Southwark well had a disappointing gas flow rate and that hit the IOG (LON: IOG) share price, which is down 55.4% to 7.36p. A second well will be drilled. There is concern that the Southwark field, where £100m has been invested, may not be commercially viable. A €100m Nordic bond matures in September 2023 and this will need to be refinanced.

BlueRock Diamonds (LON: BRD) says diamond production at Kareevlei in South Africa was below target and prices continue to fall. Repayment of a £231,250 loan from Mr T Leslie has been requested and he has threatened to present a winding-up petition. The company will also find it difficult to reduce the amount drawn under another loan facility, which is required by the end of February. This will hamper the turnaround plans for the mine. Te share price halved to 2.25p.

In December, online women’s fashion retailer In The Style (LON: ITS) was hit by price cutting by rivals and difficulties in delivering orders. Revenues in the quarter to December 2022 fell by 22%. Full year revenues are expected to be £46m, which is not much more than the £44.7m generated in the year before flotation. The EBITDA outcome is likely to be a loss of between £4.25m and £4.75m. There was £3.2m in cash at the end of 2022. On 8 December, In The Style launched a strategic review and that continues. The share price slumped by 32.6% to 8p.

Scotgold Resources (LON: SGZ) produced 1,805 ounces of gold at the Cononish gold and silver mine in Scotland. Production in the year to June 2023 is expected to be between 11,500 ounces and 13,500 ounces. Once changes in mining are completed production levels should rise next year. Scotgold Resources requires more working capital. Net debt is £12.6m. The share price slipped 28.3% to 40.5p.

Great Western Mining (LON: GWMO) has raised £800,000 at 0.08p a share. This will be used to build a mill at Mineral County, Nevada to produce gold and silver concentrates and further exploration. The share price declined by 27.4% to 0.0835p.

Maternity wear supplier Seraphine Group (LON: BUMP) was the worst performer in the FTSE Fledgling index with a 96% decline. The company floated in July 2021, and it is recommending a bid of 30p a share from Mayfair Equity Partners. That is treble the previous market price.

Seraphine joined the premium list on 16 July 2021 when it raised £61m in new money at 295p a share. That valued the company at £150.2m.

Mayfair Equity Partners owns 42.7% and raised £10.9m by selling shares in the flotation. The bid values Seraphine at £15.3m, so Mayfair Equity Partners use less than the cash it raised to pay for the shares it does not own.

Mayfair originally invested in December 2020 and wanted to help Seraphine to grow its business in new markets, as well as further exploiting existing ones. The slump in the share price made it more difficult to raise additional cash and an additional £5m will be provided by Mayfair Equity Partners.

Trading

The core market is mothers between 25 and 40 years old. Europe and North America are the main regional markets. A lack of stock had hampered progress prior to flotation.

In 2021-22, revenues increased from £34.2m to £44m, but gross margin slipped from 65.9% to 63.2%. Higher distribution and admin costs, the latter partly due to being listed, meant that there was an underlying loss even before £29.9m of exceptional costs. There was a £2.13m cash outflow from operating activities. Net debt was £153,000.

The latest interim revenues slipped from £21.8m to £19.7m, but while gross margin was maintained admin expenses continued to rise and there was a swing from a small underlying operating profit to a £3.76m loss. Inventory levels nearly doubled to £17.6m. Net debt was £2.6m.

The second half was expected to be better than the first half even though trading was still tough. It is likely to be remain difficult well into 2023.