Rumours on social media were the driving force behind gains in the FTSE 100 today with cyclical sectors rallying on hopes the Chinese economy would soon reopen and boost the global economy.

Social media posts suggested the Chinese had created a committee dedicated to seeing China through the end of the pandemic and reopening their economy.

Miners were the standout sector on Tuesday with Rio Tinto, Glencore, Anglo American and Antofagasta all gaining in excess of 4%.

A reopening of the Chinese economy would spur demand for natural resources and support mining revenues after a period of intermittent lockdowns in the world’s second largest economy.

China has been responsible for a large proportion of global over the past 15 years and any hints at expanding economic activity ignites interest in risk assets.

Ocado

While the miners were the standout sector on Tuesday, the standout company in terms of performance is undoubtedly Ocado, gaining over 30% on the day.

As we recently explained, Ocado’s strength is in their Ocado solutions business and today’s signing of a partnership with Lotte Shopping further demonstrates the scalability of the business. Lotte operates supermarkets and department stores in South Korea with annual revenue of £9.5bn.

The partnership will see Lotte build six of Ocado’s Customer Fulfilment Centres utilising the Ocado Smart Platform by 2028. Ocado shares were 36.6% higher at 646p at the time of writing.

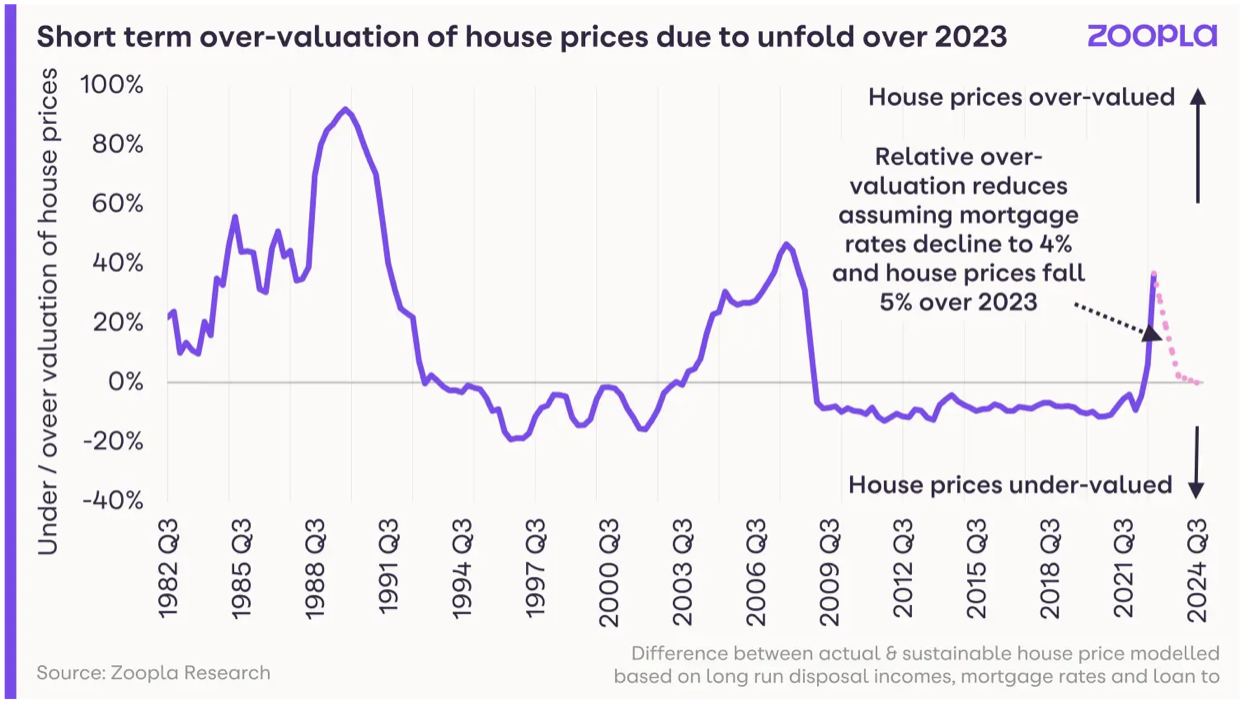

UK House Prices

A day after Zoopla said the housing market may not suffer as much a previously thought, the Nationwide House Price Index indicated house prices were indeed starting to slow.

“The UK property market is in sharp focus again, hit with yet another picture of sharply weakening demand. Although prices still rose 7.2% year on year in October, it was the smallest increase since April 2021, and a rapid slowdown from the 9.5% rise in September,” said Susannah Streeter, senior investment and markets analyst, Hargreaves Lansdown.

“The picture on a monthly basis is even more stark with prices falling 0.9% in October, the largest drop since the depths of the pandemic in June 2020.”