Lloyds shares are facing the doubled edged sword of higher rates as the benefits of a higher net interest margin are becoming increasingly threatened by any slow down in the Uk housing market.

The ECB has recently hiked rates and the odds are pretty high the Bank of England will follow suit and continue to increase rates at their next meeting.

Looking at the way inflation is progressing (13% according to the Bank of England, as high as 18% if you’re following Citibank’s expectations), aggressive rate hikes are likely to continue in the term and cause shifts in consumer and investor behaviour.

So, how are Lloyds’ shares holding up at the moment?

Lloyds shares

Lloyds has a very generous dividend yield of 4.7%, placing it above the other FTSE 100 bankers such as Barclays, with a 3.7% yield, HSBC at 3.6% and Standard Chartered at 1.8%.

Although, Lloyds is actually matched by NatWest, also boasting a 4.7% yield.

However, Lloyds has the advantage over NatWest in its dividend cover, with an encouraging 3.9 times cover against NatWest’s cover of 2.3, giving Lloyds the advantage in a volatile market environment.

Lloyds’ shares have a current PE ratio of 6 and a forward PE ratio of 6.3, indicating an approaching fall in earnings, so investors should be aware of that factor as the bank faces difficult economic circumstances in the coming year.

Lloyds’ share price has fallen 8.2% year-to-date, marking a potential opportunity to buy the stock at a dip. However, it’s worth noting that its competitors might be heading towards greener pastures than the blue chip bank.

Barclays has a PE ratio of 3.9 and a forward PE ratio of 5.1, indicating a drop in earnings. Yet the rest of the FTSE 100 banks are tapped for higher earnings going forward, with HSBC displaying a PE ratio of 8.6 to a forward PE ratio of 7.4, NatWest from 9.5 to 6.5 and Standard Chartered from 9 to 6.8.

Housing market slowdown

Lloyds is the largest mortgage lender in the UK, which spelled bad news for the bank on the latest housing market report from Nationwide this week.

Nationwide noted a house price growth to 10% in August compared to 11% in July, and while the figure remained in the double-digits, it did mark signs of a slowdown in the market as the cost of living crisis crunch reached the industry.

Surveyors noted a drop in new buyer enquiries in recent months, and the level of mortgage approvals fell below pre-Covid numbers, kicking a potential dent in Lloyds’ mortgage business.

“We expect the market to slow further as pressure on household budgets intensifies in the coming quarters, with inflation set remain in double digits into next year,” said Nationwide chief economist Robert Gardner.

Nationwide also noted the double-edged sword of rising interest rates on the housing market, as while higher rates means higher interest on loans, it also means a bucket of cold water thrown over the red-hot property demand as prospective home buyers throw their dream of a house on the back-burner for another time.

“Moreover, the Bank of England is widely expected to continue raising interest rates, which will also exert a cooling impact on the market if this feeds through to mortgage rates, which have already increased noticeably in recent months,” said Gardner.

Conclusion

Lloyds is not in trouble, and it will take a great deal to knock the bank into straits sufficiently troublesome to warrant panic.

Indeed, Lloyds’ shares are fairly well valued at 6x earnings and 0.6 Price-to-NAV.

Consumer stocks helped the FTSE 100 gain on Monday as the Uk economy returned to growth in July and falling natural gas prices increased hopes inflation may soon start to slow.

The FTSE 100 pressed ahead, rising 1.3% in late morning trading as a collection of consumer-focused stocks pulled the blue chip index higher.

Analysts commented the 0.6% growth in consumer-facing services output over July served to breathe fresh life into the FTSE 100’s top performers, following a rise in consumer spending due to the hot weather and a wave of entertainment events, including the country’s hosting of the Women’s Euros and the Commonwealth Games.

“Given all the talk of recession, businesses will be reassured to hear that the economy grew in July, at around its long-term trend rate. Consumer spending was reasonably strong, as hot weather, a strong sporting schedule and holiday bookings boosted retail and recreation activities,” said Institute of Directors chief economist Kitty Ussher.

PwC economist Jake Finney added: “The UK economy grew by a modest 0.2pc on a month-on-month basis in July, following its 0.6pc contraction in June 2022.”

“Consumer-facing services grew by 0.6pc in July, following a flat month in June. The sector was helped by record-high temperatures and one-off events, such as the UK’s hosting of the Women’s Euros and the Commonwealth games.”

Grocery shares gained, with Sainsbury’s rising 4.3% to 211.4p and Tesco climbing 4% to 249.5p, while B&M increased 3.3% to 362.5p and Associated British Foods rose 2.7% to 1,392.5p.

Fashion companies also climbed higher, with JD Sports Fashion rising 3.6% to 130.7p and Next gaining 2.8% to 6,050p.

Mining companies rise

Mining companies rose on the back of supply risks in China and a weakening dollar ahead of US inflation data on Tuesday, with Anglo American shares increasing 4.1% to 3,047p, Glencore climbing 3.2% to 504.1p, Antofagasta gaining 2.6% to 1,226.7p and Rio Tinto rising 2.5% to 4,985.5p.

Oil prices

Meanwhile, oil prices rose thanks to a weaker dollar and supply uncertainty, with the price of benchmark Brent crude increasing 1% to $93 per barrel.

Shell shares gained 1% to 2,323p and BP shares climbed 1.7% to 458.6p.

Helen Steers, Pantheon Partner and lead manager of Pantheon International Plc (ticker code: PIN), discusses the recent annual results of one of the longest established private equity investment companies.

Pantheon International Plc (“PIP”) is a FTSE 250 private equity investment company managed by Pantheon, a leading global private markets investor, and overseen by an independent Board of Directors. PIP provides investors with exposure to many of the best private equity managers in the world that may otherwise be difficult to access for many types of investors. These managers are backing high growth, exciting companies many of which are in niche sectors.

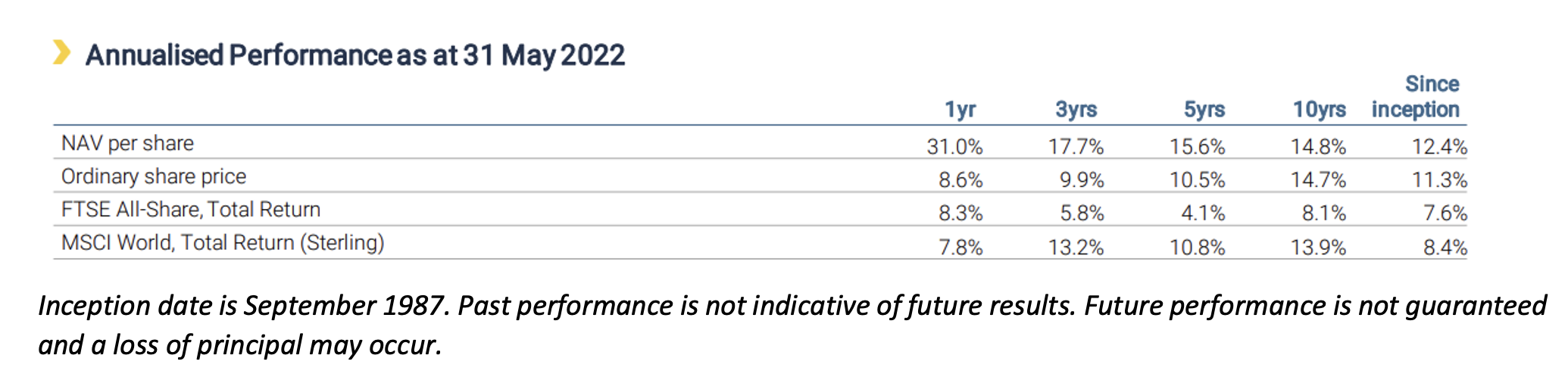

Consistent outperformance over 35 years

As shown in its recent annual results, PIP had an outstanding year, reporting record growth in the value of its net assets (“NAV”) as well as record net cash flow and investment activity for the 12 months to 31st May 2022. PIP’s NAV grew by 31.0% during the financial year and in the 35 years since PIP’s inception, it has grown by an average of 12.4% each year. This performance is stated net of all fees.

PIP has had an excellent year in terms of both new commitments and exits from existing companies held in the portfolio. PIP’s portfolio is being managed to provide ample cash that can be recycled into new investments. During the year, PIP received cash of £419m from its investments relative to £187m of calls from existing commitments to private equity funds, resulting in net cash flow of £232m. PIP made 70 new investments worth a combined £496m in the year and we expect its strong pipeline to continue to drive deal flow over the coming months.

We have continued to increase the number of direct company holdings in the portfolio and nearly 45% of the portfolio is now invested directly in companies. The increased concentration provides shareholders with greater exposure to the potential for individual companies to provide a boost to performance while, importantly, the benefits of diversification are not lost as PIP continues to invest in a well balanced portfolio of private equity funds and direct investments in companies.

PIP had its largest ever single company exit in its history during the financial year. PIP co-invested in EUSA Pharma, a pharmaceutical company focused on oncology and rare diseases, in 2015 alongside EW Healthcare which is one of the longest established private equity managers in the healthcare sector. EUSA Pharma was sold to a strategic buyer, Recordati, in December 2021, providing PIP with proceeds of £49.5m which equates to c.5.0x invested cost.

PIP has a strong balance sheet with good liquidity. We recently agreed a new, enlarged £500m five-year multi-currency, revolving loan facility to replace the previous lending agreement and there is an option to extend the facility by one year at a time beyond its expiration in July 2027. This facility, combined with £178m of cash at 31 July 2022, gives PIP even greater flexibility to meet its outstanding investment commitments and to continue to invest in compelling deal opportunities over the coming years.

Investing in exciting companies in growth sectors

PIP’s portfolio has been actively managed to be resilient in a variety of market conditions including in times of economic stress. The portfolio is tilted towards Information Technology and Healthcare, both of which are sectors that are benefitting from long-term secular trends that are not dependent on the macroeconomic environment.

The IT businesses that we invest in are typically mission-critical software and IT infrastructure businesses and those that are supporting the move towards automation and digitalisation across many sectors. These are high quality, cash generative companies with strong recurring revenues. For example, during the year PIP invested in TriMech, which is a provider of 3D design, engineering and manufacturing solutions in North America. We believe that this business is particularly interesting as TriMech is one of the few businesses operating at scale in an attractive 3D printing and design market which is set to continue to grow as companies utilise 3D software as part of their product development. TriMech has already made numerous acquisitions and they are likely to be a key component of its growth story.

We like Healthcare as a sector due to the positive tailwinds from ageing demographics and increased demand for high quality healthcare products and services from the growing middle classes in emerging economies. PIP has invested in Seqens which is a pharmaceutical ingredients manufacturer, headquartered in France, and is a leading supplier of pain relief ingredients for both the Paracetamol and Aspirin supply chains. Seqens is a great example of a company that is strongly positioned to benefit from western reshoring initiatives, which de-risk supply chains, and the growth in outsourcing of pharmaceutical supply chains.

We have continued to invest PIP’s capital in a thoughtful, responsible manner. Pantheon was an early signatory to the UN PRI in 2007 and we continue to enhance our ESG strategy. Sustainable investment can also create opportunities and we have invested in companies that have positive ESG angles. One such example is Satlink, a global leader in the development of technological solutions for the maritime sector with a focus on sustainable fishing. They recently won a United Nations Global Compact award in February 2022 for their contribution to a more sustainable fishing industry and the preservation of marine life.

The impact of substantially lower economic growth globally, coupled with supply chain issues, higher energy, food and input costs, and the lingering effects of the COVID-19 crisis, is creating an unenviable mix of challenges which are being faced by both individuals and businesses. While we are cautious in these difficult times, we believe that our industry will continue to experience significant growth in the coming years. Private equity managers have a long-term investment horizon and they offer access to subsectors that are generally under-represented in the public markets and that continue to innovate and offer compelling investment opportunities.

PIP’s portfolio is orientated towards small and medium-sized businesses and those in the growth phase of their development. Within those businesses, there are a number of levers that our private equity managers can pull to create value and there are also several routes for them to sell the businesses on. The majority of the exits in PIP’s portfolio are to corporate buyers, executing their M&A strategies, or to other private equity managers who have a different set of skills to take the business to the next stage of its growth. The managers we are backing are not dependent on the IPO market being open. In fact, just 7% of the exits in PIP’s portfolio during the financial year were due to companies being taken public. Furthermore, PIP’s portfolio is tilted towards asset-light companies, which typically have no debt (in the case of companies in the growth capital stage), or lower levels of debt (in the case of small and mid-sized businesses), compared with large and mega sized firms.

For the past 35 years, Pantheon has managed PIP through numerous economic cycles to deliver long-term outperformance over its public market benchmarks. Investors must assess carefully what is suitable for them and their investment objectives and tolerance/appetite for risk but PIP’s access, through Pantheon, to many of the best private equity managers globally provides us with confidence that PIP can continue to provide attractive returns to shareholders over the long term.

Important Information

This article and the information contained herein may not be reproduced, amended, or used for any other purpose, without the prior written permission of PIP. This article is distributed by Pantheon Ventures (UK) LLP (“Pantheon”), PIP’s manager and a firm that is authorised and regulated by the Financial Conduct Authority (“FCA”) in the United Kingdom, FCA Reference Number 520240.

The information and any views contained in this article are provided for general information only. Nothing in this article constitutes an offer, recommendation, invitation, inducement or solicitation to invest in PIP. Nothing in this article is intended to constitute legal, tax, securities or investment advice. You should seek individual advice from an appropriate independent financial and/or other professional adviser before making any investment or financial decision. Investors should always consider the risks and remember that past performance does not indicate future results. PIP’s share price can go down as well as up, loss of principal invested may occur and the price at which PIP’s shares trade may not reflect its prevailing net asset value per share.

This article is intended only for persons in the UK. This article is not directed at and is not for use by any other person. Pantheon has taken reasonable care to ensure that the information contained in this article is accurate at the date of publication. However, no warranty or guarantee (express or implied) is given by Pantheon as to the accuracy of the information in this article, and to the extent permitted by applicable law, Pantheon specifically disclaims any liability for errors, inaccuracies or omissions in this article and for any loss or damage resulting from its use. All rights reserved.

HgCapital Trust shares rose 4% to 383.5p in late morning trading on Monday, after the firm announced a total return NAV climb of 1.8% to a NAV per share of £4.43 and net assets of over £2 billion.

The Trust linked its results to strong portfolio trading and value creation, which reportedly offset a decline in valuation multiples of listed comparable companies.

HgCapital Trust invested £71 million alongside its other institutional clients, with an estimated additional £355 million invested post-period.

Meanwhile, HgCapital noted £29 million of returns realised on behalf of the Trust, with an anticipated additional £465 million returned post-period at an uplift of 29% to December book value.

The Trust highlighted an investment of £1,000 made 20 years prior in HgCapital would currently be worth £18,370 at a total return of 1,737%, with an equivalent investment in the FTSE All-Share Index worth £3,521.

“Despite the obvious challenges and uncertainty presented by the current macro-economic and geo-political environment, the Board remains optimistic about the future prospects for HGT,” said HgCapital Trust chairman Jim Strang.

“The businesses within the portfolio are resilient, and in such an environment as today’s continue to provide critical solutions to their clients and reduce the costs and complexity of doing business.”

“The long-term value creation prospects from owning such a portfolio remains attractive.”

HgCapital Trust declared a HY1 dividend of 2.5p per share against 2p the last year, which is scheduled for October 2022 payment.

The Sterling rose to 1.1682 against the dollar in Monday trading after analysts noted maintained hawkish sentiment from the US Federal Reserve ahead of US inflation data, which is scheduled for release on Tuesday.

Disappointing UK GDP growth of 0.2% in July did little to dent the Pound’s rise versus the dollar, with Prime Minister Liz Truss’ financial support package announced on Thursday lending some buoyancy to the Sterling after its spiral to 37-year lows earlier last week.

“In their last chance to provide guidance before the 20-21 September meeting, there was no push-back from any Fed official on the market view that is almost fully priced for a 75bp hike. Fed rhetoric remains hawkish with officials resolute in their commitment to bring inflation down,” said ANZ senior economist Tom Kenny.

The US last saw inflation drop to 8.5% from its multi-decade record high of 9.1%, sparking some hope the US Fed would ease off aggressive interest rate hikes.

However, Fed chair Jerome Powell quickly shut down such hopes at the Jackson Hole convention in late August, during which he confirmed continued hawkish rate decisions until inflation was tackled back down to the 2% target.

Cleveland Fed president Loretta Mester said she didn’t expect inflation to return to 2% until 2024, and advocated potentially more aggressive rate hikes than the Fed already had in sight if inflation hits another peak.

“My current view is that it will be necessary to move the nominal fed funds rate up to somewhat above 4 percent by early next year and hold it there; I do not anticipate the Fed cutting the fed funds rate target next year. But let me emphasize that this is based on my current reading of the economy and outlook,” said Mester to MNI News.

The UK economy grew 0.2% in July after a 0.6% fall in June, rising 1.1% above pre-Covid levels in February 2020.

However, UK GDP growth failed to meet analyst expectations, spelling trouble for the country as the cost of living crisis tightened its grip on household budgets.

The Office of National Statistics (ONS) noted GDP was flat in the three months to July compared to the previous three months.

“July’s rather anaemic growth came in below expectations, a factor which will add to concerns that the UK is slow marching towards recession,” said AJ Bell financial analyst Danni Hewson.

“Despite the package of support for households, which has just been announced by the government, the cost of living crisis hasn’t magically disappeared.”

“Energy costs are just one part of the equation – food prices, fuel prices and pretty much every single service we use has gone up and, even if inflation doesn’t peak at those eyewatering levels we’d been warned of, budgets are still very tight.”

The services sector rose 0.4% in July after a 0.5% drop in June, with information and communications growing 1.5% as the largest contributor to services growth over the month.

Meanwhile, production declined 0.3% following a 0.9% fall in June, primarly linked to a 3.4% decrease in the supply of electricity, gas, steam and air conditioning.

“It’s not surprising that the ONS flags up anecdotal evidence that demand for electricity fell in July,” said Hewson.

“Businesses and consumers have been making changes, cutting back, altering habits, preparing for those long winter days.”

The economy also saw a 0.8% decrease in construction following a 1.4% drop in June, with the decline in monthly output driven solely by a 2.6% fall in repair and maintenance.

“High prices for materials like concrete and bricks continue to be a huge issue for the construction sector and it is interesting that repair work and maintenance have dragged the sector down,” said Hewson.

“People will try and make do if they’re worried about cash, hoping that putting repairs off until tomorrow will result in lower quotes as inflation cools.”

The ONS confirmed a 0.6% growth in consumer-facing services output after flat growth in the previous month. However, consumer-facing services remained 4.3% below pre-Covid levels over July.

“And finding staff to do the jobs that need doing is still a huge concern across the board. How does a business take advantage of surges in demand if they don’t have enough workers?” said Hewson.

However, the cost of living crisis might soon be felt in the labour market as winter approaches, with the harsh season ahead sparking a potential sink-or-swim environment where employers chuck workers into the cold in a move to survive the energy costs surge.

“There are signs that the jobs market is relaxing and evidence that some businesses are now actively letting workers go as they try and create some kind of cushion going into the winter months,” said Hewson.

“Will the energy price freeze be enough to keep the economy chugging forward, or has intervention come too late to settle nerves?”

“Will consumers relax their tight hold on the purse strings enough now they’re no longer faced with the spectre of continually rising energy bills?”

The support package from Prime Minister Liz Truss might have avoided the worst of the energy crisis, however it remains to be seen if the energy price cap freeze will be enough to coax customer wallets out of their grip once winter arrives.

Antofagasta announced precautionary measures at its Los Pelambres project in Chile, following the collapse of a construction platform due to severe sea swells on the marine works of its desalination plant project.

The mining firm said there was no significant damage to the environment or to its project works, and it had recovered some of its lost equipment and materials.

However, the sea swells have reportedly persisted and impeded further recovery work.

Antofagasta confirmed the Chilean environmental authority required the company to put marine works on hold until the clean-up of remaining sunk equipment carrying fuel or lubricants had progressed to the point that any risk of environmental impact had been removed.

The commodities group said it expected recovery of lost materials and equipment to finalise once weather conditions improved.

Grainger shares gained 2% to 272.8p in early morning trading on Monday, following a reported acceleration in like-for-like rental growth across its portfolio in its FY 2022 pre-close trading update.

The home rental company announced a total like-for-like rental growth of 4.5% year-to-date, alongside a PRS like-for-like rental growth of 4.5%.

Grainger mentioned a 5.4% new lets climb and a 3.9% rise in renewals over 2022.

Meanwhile, the properties rental firm noted a regulated tenancy like-for-like increase of 4.4%, and a PRS like-for-like rental growth of 5.3% in the five months to August 2022.

Grainger highlighted prospective customer enquiries remained at record levels.

The group also confirmed a 98.2% spot occupancy at the close of August this year.

“Momentum in the business is continuing to accelerate and our mid-market strategy and in-house scalable operating platform has delivered a strong performance,” said Grainger CEO Helen Gordon.

“Occupancy remains at record levels at over 98%. At the same time, like-for-like rental growth across our national portfolio is continuing to build over the second half of our financial year and we are seeing the strongest rental growth we have seen in a decade.”

Bristol acquisition

Grainger mentioned a new Bristol acquisition over the FY 2022 financial term, with a £128 million acquisition of 468 new homes at Redcliff Quarter in the city.

The purchase brings the company’s total investment in Bristol to almost 900 homes, including 94 new affordable homes through Grainger Trust, its in-house affordable housing arm.

Cost of living

Gordon highlighted the cost of living crisis on its tenants, and claimed it would make efforts to alleviate its tenants’ financial pressures where possible.

“Despite the buoyant rental market, we are very mindful of the financial challenges facing many individuals. We are therefore taking a responsible approach to rental increases, ensuring affordability for our customers remains a central consideration and balancing rent increases with retention,” said Gordon.

“We are also supporting customers where we can with their other costs by continuing to invest in the energy efficiency of our portfolio, with nearly 90% of our PRS portfolio offering the highest energy ratings (A-C), saving our customers potentially thousands of pounds a year.”

“In our newer properties, we are also providing free broadband and complimentary gyms, and we are providing practical advice and support to over 20,000 customers on how they can reduce their energy usage and costs, and other bills. In addition to supporting our customers, we have provided financial support to all of our colleagues, excluding our senior executive team, through an additional £1000 cost of living payment.”

Greencoat Renewables shares climbed 1.6% to 109p in early morning trading, after the group announced net cash generation of €92.1 million in HY1 2022 against €40.2 million the year before.

The firm’s GAV grew to €2.1 billion compared to €1.4 billion, along with a NAV rise to €1.2 billion from €749 million.

Meanwhile, Greencoat Renewables delivered a total installed capacity growth to 1,028 MW against 686 MW the last year due to an increase in portfolio size to 28 wind farms from 23 year-on-year, alongside its Killala battery project becoming operational.

The company highlighted a €898.7 million aggregate group debt, equivalent to 42% of GAV.

Greencoat Renewables reported successful capital raising activity over the interim period, with gross proceeds of €281.5 million raised in an oversubscribed placing.

The group declared total dividends of 3.09c per share in HY1 2022.

“The six months to 30 June 2022 was another active period for the Company, as we added 217MW of new generating assets to the portfolio, taking our total installed capacity above the 1GW threshold. We achieved a further milestone with the acquisition of our first offshore wind asset in Germany and strengthened our European diversification with agreements to acquire new assets in Spain, Sweden and France,” said Greencoat Renewables non-executive chairman Ronan Murphy.

“Over the past 12 months we have committed €867 million into renewable generation assets, with elevated power prices supporting increased levels of reinvestment.”

“With Europe expected to require €1 trillion of new clean energy investment by 2040, the Company is well positioned to play a significant role in enabling and accelerating this transition, directly contributing to meeting emissions targets and reducing reliance on gas across Europe.”

There are 29% of AIM companies that currently pay dividends and distributions are back in growth mode. Payments have been growing and even in uncertain times there are companies that have an attractive yield with the cash flow to continue to pay the dividends.

AIM dividend payments have bounced back since the Covid lockdowns. The latest issue of the Link AIM Dividend Monitor shows a strong recovery in dividends in the first half of 2022.

Total dividends in the first half of the year were £674.7m, including special dividends, up from £535.6m last year.

The comparatives become tougher in the sec...